{kind=link}

Riding the EV (Electric Vehicle) Evolution at CME Group

Source: Tesla & CME Group

- Driven by demand, the prices of copper and other precious metals are on the rise

- As technology accelerates, the role of fossil fuels evolves

- 2020 saw record inflows to ESG investments – projected to hit $53 trillion by 2025

- The EV race to market dominance is on, who will be the winner?

If there’s one market move to embody the progression towards a greener economy, one might certainly consider the meteoric rise of American electric car manufacturer Tesla (+4,000% since 2010 IPO) as the top contending bellwether indicator – but, that is not the only one.1 Take, for instance, the rising prices of copper, aluminum, and other precious metals which make up the constituent components of an electric vehicle, the evolving role of fossil fuels, and record inflows to new ESG (Environmental, Social, and Governance) investment vehicles such as CME Group’s E-mini S&P 500 ESG futures.

What is driving this evolution?

In 2010, there were less than 20,000 EVs sold. Fast-forward to today, there are over 8 million EVs on the road with a new one driving off the lot (or being delivered) every 15 seconds. According the IEA data, 47% of those sales are occurring in China, who is the world leader in terms of market share. In 2019 alone, the global EV market experienced a year-over-year increase of 40% and, in 2020, the industry defied Covid-19 to grow an additional 28%.2, 3

While technology and subsidies have been driving the growth of the market, there has been a monumental shift towards policy. China recently extended their subsidy scheme until 2022, while the UK and the EU have both made commitments to effectively ban petrol and diesel car sales by 2030 and 2025, respectively.4 In the United States, President Biden’s green economy proposal plans for 500,000 EV charging stations – a move that could spark the sale of close to 25 million additional EVs before 2030 according to Bloomberg.5

Electrification has created a new demand driver for certain metals

As renewable energy and power distribution grows, so does the demand for metals. Metal is a natural conductor of electricity and heat, and thus lends itself to play a pivotal role in the growth of an electrified economy with efficient green energy distribution. EV growth has already driven demand for certain base metals, leading some to predict a 37- and 18-fold increase in demand by 2030 for cobalt and lithium relative to 2015 levels. Significant demand increases are also predicted for copper, chrome, and aluminum.6

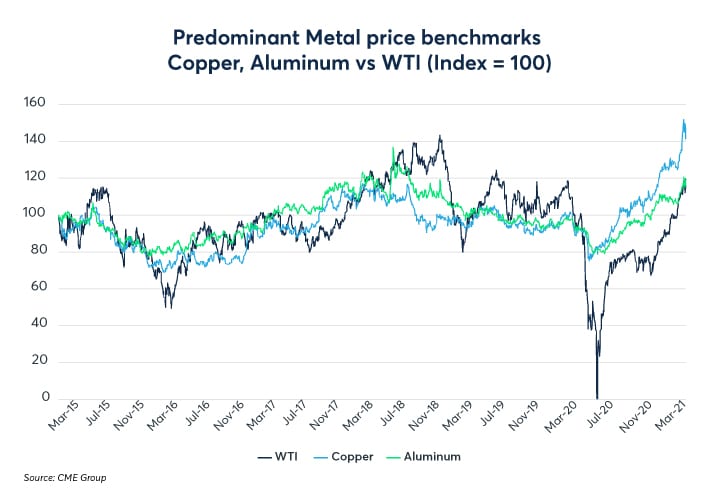

Figure 1: Predominant Metal price benchmarks Copper, Aluminum vs WTI (Index = 100)

{kind=link}

Industry estimates the average amount of aluminum used in electric vehicles is 30% higher than internal combustion engine cars, while copper is positioned to be a primary benefactor of greater decarbonization and electrification efforts.7

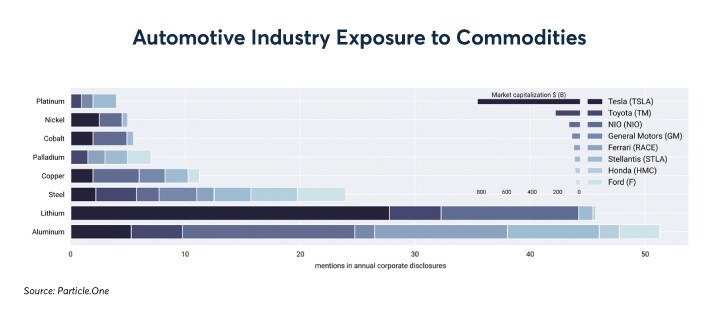

Of the largest 15 auto manufacturers by market cap worldwide (over $1.8 trillion in combined value), eight trade on US exchanges (at a combined value of nearly $1.4 trillion). Particle.One’s proprietary Knowledge Graph and NLP technology applied to annual corporate disclosures (forms 10-K and 20-F) from the past four years highlights the growing significance of metals required to produce EVs. Precious metals are mentioned most often in the filings of the most well-capitalized auto manufacturers, underscoring the market’s perception of the transformative importance of the EV-shift.

Figure 2. Automotive industry exposure to commodities

{kind=link}

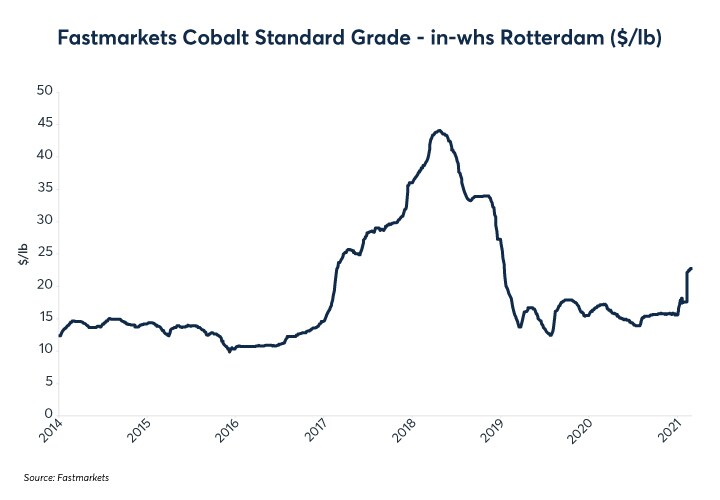

Battery metals and Intro to CME Cobalt

Cobalt is a key material in the manufacturing of lithium-ion batteries and various other industrial products. The rapid growth of electric vehicles and large-scale battery storage applications is expected to drive increasing demand for cobalt – and with it, greater price risk for the industry. To meet the growing need for efficient risk management, CME Group has launched Cobalt Metal (Fastmarkets) futures. The contract is financially settled based on the Fastmarkets Standard Grade Cobalt Metal in Warehouse Rotterdam assessment, which serves as the key industry reference for pricing cobalt across the supply chain. Cobalt Metal (Fastmarkets) futures have traded 105 MT since its launch in December 2020, making it the first-ever Cobalt futures contract to trade on exchange.

Figure 3. Cobalt Metal (Fastmarkets) futures

{kind=link}

Powering the EV evolution

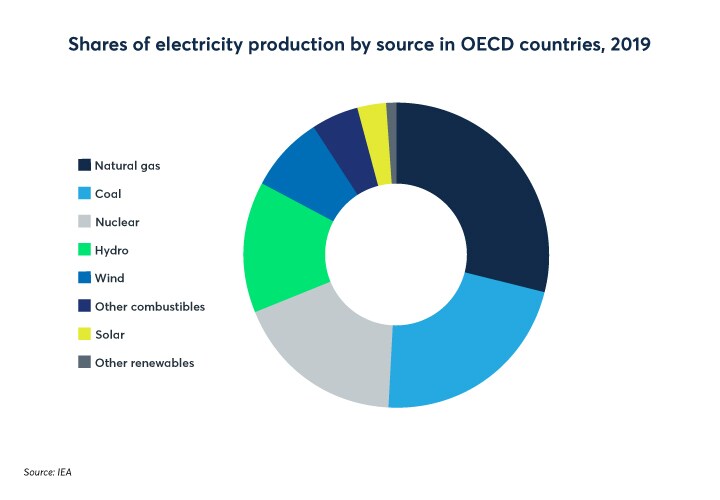

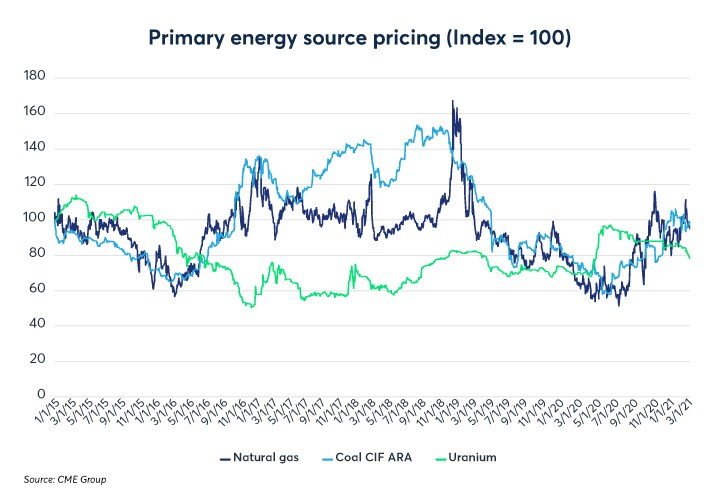

The landscape and use of fossil fuels is changing while technology is driving incremental efficiencies in renewable energy and energy distribution. The use of fossil fuels will be crucial in the energy transition specifically as it relates to growing EV adoption across the globe. According to the IEA, global electricity demand from electric vehicles will reach 550 TWh by 2030, rising approximately six-fold from 2019 levels. Natural gas constitutes 30% of electricity generation in OECD countries while coal and uranium represent 22% and 18% respectively.8 Collectively, these three sources account for nearly 70% of electricity generation across OECD countries, making them pivotal drivers in the EV evolution. The CME Group Energy complex provides access to all three of these markets through its Henry Hub Natural Gas, LNG, Coal, and Uranium contracts, with liquidity provided nearly 24/7 for market participants around the globe.

Figure 4. Shares of electricity production by source in OECD countries, 20199

{kind=link}

Figure 5. Primary energy source pricing (Index = 100)

{kind=link}

Conclusion: The EV race is on and the competition is electric

While Tesla’s market position at the forefront of the electric vehicle space is sure to be tested in the years to come, they have proven the market for EVs exists, it is poised for explosive growth, and reverberations of this evolution are just starting to express themselves in the affiliated commodities and related markets. Sector growth is sure to come with an accompanying set of evolving risks from untested supply chains, developing regulatory frameworks and new market entrants.

With the pressure on, the market can expect more announcements like G.M.’s recent commitment of $27 billion to introduce 30 new electric vehicle models by 2025 and only sell zero-emission cars and trucks by 2035.10 “To be ready by 2035, I need to build battery plants, I need to do battery development, I need to develop electric vehicles,” said Senior G.M. Executive Dane Parker.

Under competitive market scenarios, price makers generally become price takers. Those in the sector with sound risk management practices embedded in their operations will be at an advantage to handle the volatility of the EV-affiliated supply chain commodity markets as price formation shifts to the intersection of supply and demand. From cobalt and copper, to natural gas and coal, those wishing to manage this risk or express an opinion on the direction of this sector and its associated markets can do so using the CME Group’s multi-asset exchange listed derivative instrument portfolio.

CME Group EV Products

| Battery Metals: | |||||

|

Cobalt Metal (Fastmarkets) [link-bold] [text-align: center] |

[text-align: center] |

[text-align: center] |

|||

| Body Work & Electric Circuitry: | |||||

|

[text-align: center] |

[text-align: center] |

[text-align: center] |

|||

| Power Generation Fuels: | |||||

|

[text-align: center] |

[text-align: center] |

[text-align: center] |

[text-align: center] |

||

References

- https://www.cmegroup.com/2020/06/29/tesla-stock-up-4125percent-since-ipo-ten-years-ago.html

- IEA (2020), Global EV Outlook 2020, IEA, Paris https://www.iea.org/reports/global-ev-outlook-2020

- BNEF Executive Factbook: https://assets.bbhub.io/professional/sites/24/BNEF-2021-Executive-Factbook.pdf

- UK set to ban sale of new petrol and diesel cars from 2030 https://www.ft.com/content/5e9af60b-774b-4a72-8d06-d34b5192ffb4

- Joe Biden’s plan to fight climate change: https://www.bloomberg.com/news/articles/2020-12-02/joe-biden-plan-to-fight-climate-change-could-sell-25-million-electric-cars

- The EV revolution: The road ahead for critical raw materials demand: https://www.sciencedirect.com/science/article/pii/S0306261920305845

- Auto parts makers shine spotlight on aluminium’s role in electric vehicles: https://www.reuters.com/article/us-aluminium-electric-autos-analysis/auto-parts-makers-shine-spotlight-on-aluminiums-role-in-electric-vehicles-idUSKCN24S1QM

- https://www.iea.org/data-and-statistics/charts/shares-of-electricity-production-by-source-in-oecd-countries-2019

- https://www.iea.org/data-and-statistics/charts/shares-of-electricity-production-by-source-in-oecd-countries-2019

- G.M. Announcement Shakes Up U.S. Automaker’s Transition to Electric Cars: https://www.cmegroup.com/2021/01/29/business/general-motors-electric-cars.html