Navigating Uncleared Margin Rules

Are you ready for initial margin?

{kind=link}

Find Capital-Efficient Solutions to UMR Challenges

UMR Timeline

Getting ready for UMR can be a significant, time-intensive undertaking for firms not familiar with posting initial margin. Knowing if your firm is impacted is critical to plan accordingly.

Thresholds in the US & EU

| Thresholds [text-align: left] | ||

| UMR Phase | US (in USD), EU (in EUR) | Initial Margin Compliance Date |

| Phase 5 | 50 billion | 1-Sep-21 |

| Phase 6 | 8 billiion | 1-Sep-22 |

Observation Phases 5 & 6 in the US & EU

| Phase 5 - Sept 1, 2021 Compliance Date [text-align: left] | Phase 6 - Sept 1, 2022 Compliance Date [text-align: left] |

|

Observation Period: March, April and May 2021 |

Observation Period: March, April and May 2022 |

| Calculated daily on US, monthly in EU | Calculated daily on US, monthly in EU |

| AANA threshold: > 50 billion (USD, EUR) | AANA threshold: > 8 billion (USD, EUR) |

*New dates released by BCBS & IOSCO, and each are subject to respective jurisdictions.

What's In Scope for UMR

Average Aggregate Notional Amount (AANA)

AANA is what regulators use to determine whether a firm is in scope for IM in Phases 5 & 6. Asset managers, banks, hedge funds, corporates, pensions and more may be subject to the requirements.

Which derivatives are in-scope

AANA is based on the open gross notional value of all non-centrally cleared derivatives during the designated calculation observation period for the phase.

| Included: Uncleared OTC Derivatives |

Not Included: Cleared Instruments |

|

|

This is not an exhaustive list. For a detailed list, visit ISDA.

| Asset class | Initial margin requirement (% of notional exposure) |

|

Credit: 0–2 year duration [text-align: center] |

2 [text-align: center] |

|

Credit: 2–5 year duration [text-align: center] |

5 [text-align: center] |

|

Credit 5+ year duration [text-align: center] |

10 [text-align: center] |

|

Commodity [text-align: center] |

15 [text-align: center] |

|

Equity [text-align: center] |

15 [text-align: center] |

|

Foreign exchange [text-align: center] |

6 [text-align: center] |

|

Interest rate: 0–2 year duration [text-align: center] |

1 [text-align: center] |

|

Interest rate: 2–5 year duration [text-align: center] |

2 [text-align: center] |

|

Interest rate: 5+ year duration [text-align: center] |

4 [text-align: center] |

|

Other [text-align: center] |

15 [text-align: center] |

How and when AANA is calculated

Where you are located (US or EU) will help determine how your firm’s AANA is calculated, when/if you will be captured under UMR Phases 5 & 6, and when you must start posting IM.

Our Solutions

Find out how our global solutions can help you throughout the entire UMR process, from meeting IM requirements, adding capital efficiencies, to reducing costs and core business disruptions.

Reduce your total notional outstanding

If your firm is close to a UMR threshold, explore multiple ways to lower your AANA.

Use compression services

Use triReduce to compress notional outstanding and line items in your OTC derivatives portfolio, via multilateral compression cycles.

Scalable for use in multiple asset classes for cleared and non-cleared relationships:

- Rates

- FX

- Credit

- Commodities

Part of the market-leading TriOptima suite of solutions [link-bold]

Voluntarily clear OTC products

Use our multi-asset OTC cleared offering to add the margin efficiencies of clearing to your OTC portfolio.

Rates

Cleared IRS in 24 currencies USD swaptions.

FX

11 NDFs, 26 CSFs, 7 FX options.

Cleared

Use CME CORE to calculate and compare IM for listed and cleared OTC CME Group products.

Additional tools

Portfolio margining, coupon blending, compression services.

Move vanilla bilateral exposures to futures

Use our diverse futures and options lineup to replicate vanilla bilateral OTC exposures and reduce in-scope notional outstanding, as follows.

Rate swaps

Eurodollar and Treasury futures and options, MAC swap futures.

FX forwards

FX monthlies, FX options, FX Link.

Equity total return swaps

S&P 500 Total Return futures including new Adjusted Interest Rate (AIR) Total Return futures, Dividend futures, Select Sector futures.

Get help meeting daily compliance needs

Explore solutions to integrate daily IM calculation, communication and reconciliation tasks into the collateral management process for your derivatives portfolio.

Calculate daily margin requirements

Agree to margin calls with your counterparties

Bilateral

Use triResolve Margin to calculate and automatically agree to your Initial Margin calls and collateral movements with your counterparties.

Resolve margin disputes with ease

Bilateral

Use Acadia’s IM Exposure Manager to help identify exposure differences and resolve disputes.

Minimize margin requirements

Minimizing exposure against each counterparty and optimizing net funding amounts can help lower bilateral margin requirements.

Optimize counterparty risk exposures

Use triBalance to rebalance bilateral and cleared counterparty risk for greater margin efficiencies and to keep your portfolio market-risk neutral.

triBalance takes the next step in portfolio optimization by innovating a trusted, simple, uniform process for managing your portfolio risk and counterparty exposure.

Use voluntary clearing

Use CME Group cleared OTC products where possible to lower requirements from 10-day margin on uncleared bilateral exposures to the 5-day margin on cleared OTC.

You also can add counterparty netting benefits by clearing all trades in a single account instead of bilaterally across multiple counterparties (UMR margins are calculated at the counterparty level).

Shift to futures

Use CME Group futures and options where possible in place of vanilla swaps to further reduce requirements to the 1-2 day margin of standardized listed products.

As with voluntary clearing, CME Group futures and options offer counterparty netting benefits.

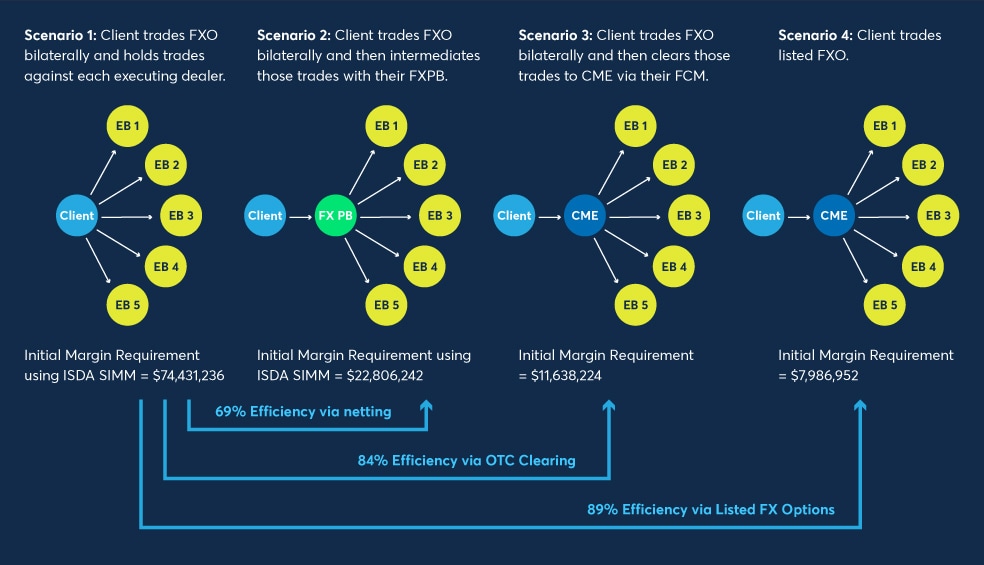

FX Case Study: Add Up to 89% Capital Efficiencies

See the difference UMR solutions can make to your IM costs. The example below shows a real portfolio of FX options. By applying one of our solutions to address IM costs, the client can add significant potential savings. Clearing delta hedges would add to the IM efficiencies of using OTC clearing or exchange-traded derivatives.

{kind=link}

UMR Resources

FCA Fact Checker

Find out more about the margin requirements for uncleared derivatives that started to be phased in 2017.

ISDA Checklist

View ISDA’s 8-Step Guide to getting ready for Initial Margin regulatory requirements.

Greenwich TCA Study

Buyside firms may save up to 70% in execution costs on some trades by using listed FX options.

ISDA Resource Hub

View tools, thought leadership articles and guides for your non-cleared margin rules needs