{kind=link}

The Yield Curve - Unemployment Feedback Loop

Following up on our papers regarding the Yield Curve-VIX and Yield Curve-Credit Spreads cycles: here’s one more weird chart with which to inaugurate (and forecast likely developments in ) 2018.

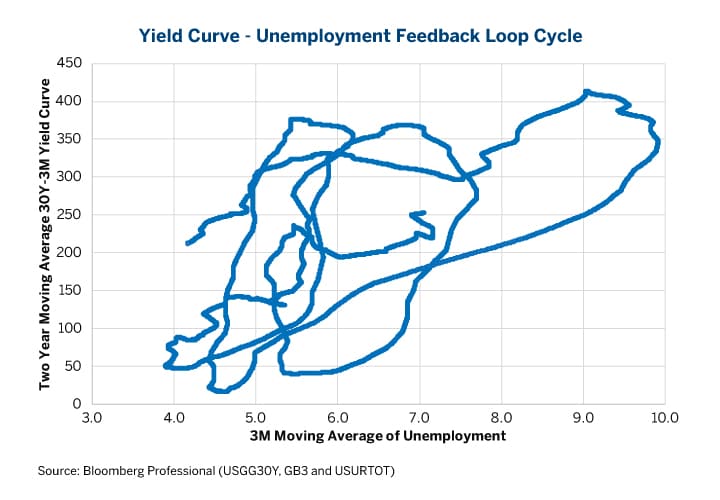

Figure 1: Three Successive Iterations of the Yield Curve-Unemployment Cycle

{kind=link}

Turns out that credit spreads and volatility aren’t the only things involved in a cyclical relationship with the yield curve. Since 1983, the cycle has repeated three times and can be broken down into four parts:

- Recession: flat yield curves precede rising unemployment.

- Early stage recovery: in response to weak labor markets, the Federal Reserve (Fed) lowers rates and steepens the yield curve. Easier monetary policy gets credit flowing again, stanching the rise in unemployment, which begins to fall.

- Mid-stage recovery: unemployment falls and the central bank begins to tighten monetary policy, flattening the yield curve.

- Late-stage recovery: the yield curve becomes very flat and unemployment stops falling, or declines at a much slower pace than before.

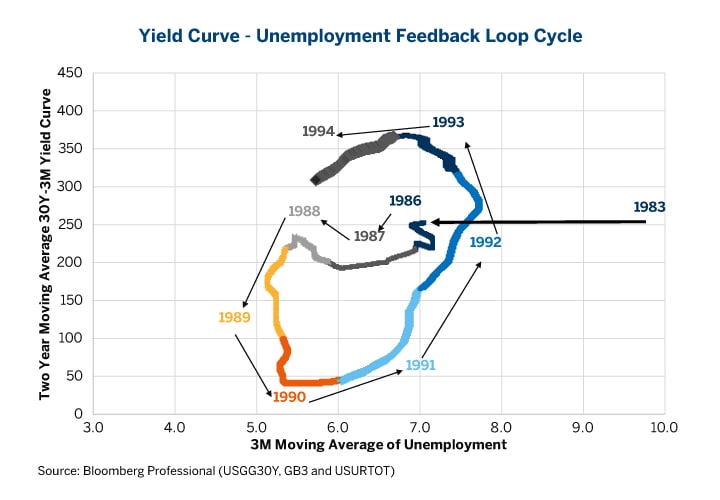

Figure 2: The 1980s Cycle

{kind=link}

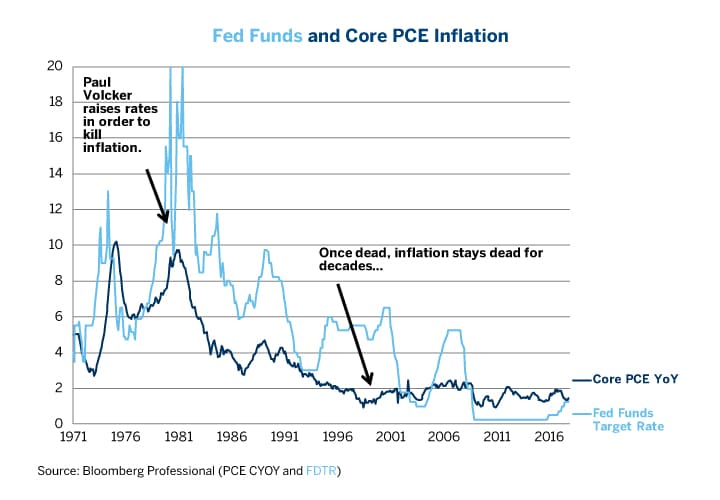

In 1979, President Jimmy Carter appointed Paul Volcker to head the Fed and entrusted him with the thankless task of killing inflation. Volcker succeeded. After he raised rates to 20% and put the economy into a double-dip recession that drove unemployment above 10% by 1982, inflation never returned to its pre-1980 levels. By 1982, the Fed was busy cutting rates. (From 1982 until 1988, 30-year U.S. Treasuries yielded about 200-250 basis points (bps) more, on average, than three-month T-Bills). The economy boomed. Unemployment fell. In 1988 and 1989, his successor, Alan Greenspan, began raising rates to prevent the economy from overheating. By 1989, the yield curve was flat, savings and loans institutions were going belly up and in 1990 the investment bank Drexel Burnham Lambert failed, creating chaos in the high-yield debt market.

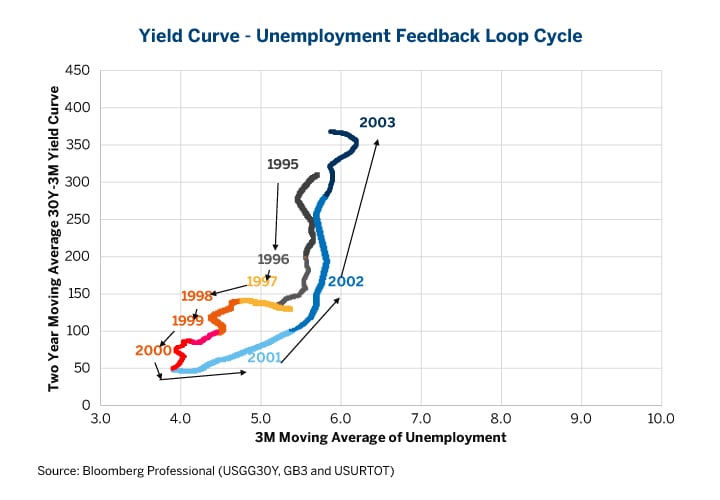

As the U.S. economy entered a recession in late 1990 and early 1991, the Fed vigorously cut rates as unemployment rose from 5.4% to 7.8%. By 1992, the U.S. had a steep yield curve and unemployment peaked in July of that year and began falling once again. The Fed maintained easy monetary policy through early 1994 when it began tightening again. By 1995, the Fed had achieved something rare: a soft landing. Unemployment stopped falling for a while but to the Fed’s astonishment, productivity was booming and there was little in the way of wage pressures. So, the Fed eased up slightly and didn’t bring the yield curve all the way to flat, instead leaving around 140 bps of steepness between 3M T-Bills and 30Y Long Bond yields. Unemployment started falling again in 1997 and dropped all the way to 3.9% by the time the Fed flattened the yield curve in early 2000 (Figure 3).

Figure 3: The 1990s Boom Extended With a Productivity Revolution.

{kind=link}

The flat yield curve helped to trigger a collapse in business investment and a rise in unemployment in 2001 to which the Fed responded by slashing rates to 1.75% by the end of 2001. When the economy failed to revive, the Fed eventually set rates at 1.25% by the end of 2002 and to 1% in June of 2003. The low rates set off a massive housing boom and a consumer-borrowing binge. With a steeper yield curve, the labor market finally began to recover in the second half of 2003.

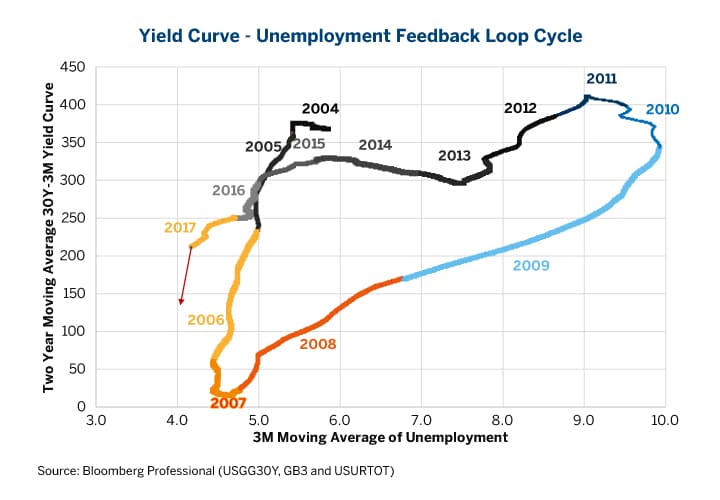

Confident it had things under control, the Fed began raising rates in June 2004. After 17 consecutive rate hikes, it had Fed Funds back at 5.25% by June 2006 and the yield curve back to being flat. The economy continued to grow until spring 2007 when unemployment bottomed at 4.4% and began rising, slowly at first. As the subprime mortgage crisis spun out of control, unemployment soared in 2008 and 2009. By the end of 2008, the Fed had rates close to zero. One year later, unemployment peaked at 10% and began slowly falling by about 0.7% per year (Figure 4). After having hiked rates once each in 2015 and 2016, the Fed began tightening policy more vigorously in 2017 with three rate hikes and a reduction in the size of its balance sheet.

Figure 4: The Yield Curve is Still Steep Enough to Give the Expansion a Couple of Years to Run (at least).

{kind=link}

With a 134-bps steepness between 3M and 30Y, the U.S. yield curve currently looks a lot like it did in 1988, 1996 and 2005 – when unemployment rates continued to fall for at least another 12-24 months. As such, in the current expansion, unemployment could fall well below 4% at some point in 2018 or 2019, perhaps going to 3.5% or even 3.0%. Any why not? With unemployment at 4.1% currently, there is scant evidence of upward pressures on either wages or inflation (Figure 5).

Figure 5: Why on Earth Would They Be in a Hurry to Raise Rates in the Absence of Inflation?

{kind=link}

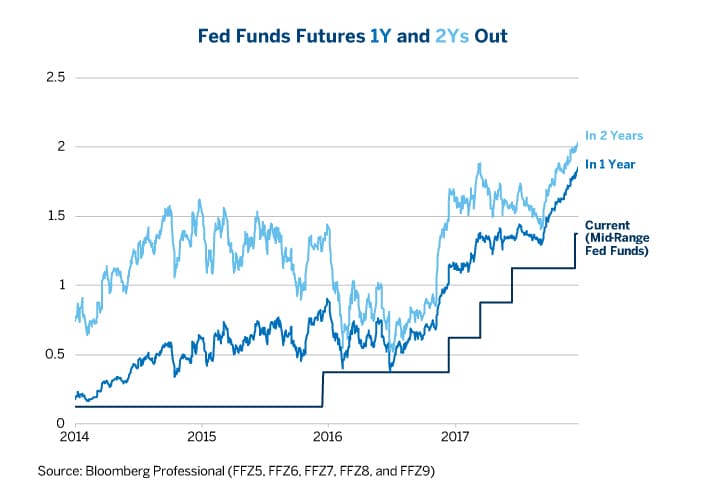

How long the recovery lasts depends upon the Fed. The faster it hikes, the more likely a recession in 2020 or 2021. The more slowly it goes, the longer the expansion can last. If the Fed hikes as fast as its “dot plot” suggests, three times in 2018 and three times in 2019, watch out for a rise in unemployment around 2020 or 2021. The forward curve, however, prices a go-slow approach (Figure 6).

Figure 6: Fed Funds Futures Price 2-3 Rate Hikes in Total for 2018 and 2019.

{kind=link}

Bottom line:

- Like with the VIX and credit spreads, unemployment is also involved in a cycle with the yield curve.

- The U.S. yield curve is not currently flat enough to trigger a U.S. recession in the near term.

- Unemployment probably has further to fall and might even go towards 3% by the end of the decade if the Fed doesn’t hike rates too quickly.

- If the Fed hikes three times in 2018 and three times in 2019, as its “dot plot” suggests, the yield curve would probably become flat by the end of the decade and the economy might be in a recession by the early 2020s.

- With inflation so low, the Fed, in our view, has no reason to be in such a hurry to hike rates and could responsibly take a slower approach unless it has some legitimate reason to think that higher inflation is just around the corner.

Recommended For You

Interest Rates

The Federal Reserve's policy-setting FOMC panel meets at the end of January to decide on raising interest rates for the first time in 2018. Get the pulse of market participants on whether the Fed will hike rates this month or defer to its next meeting in March by using the CME FedWatch tool.

Trading the U.S. Treasury Curve

Watch a video about trading the U.S. Treasury yield curve with 10-Year and 2-Year Notes – commonly known as the twos versus tens.