{kind=link}

VIX-Yield Curve: At the Door of High Volatility?

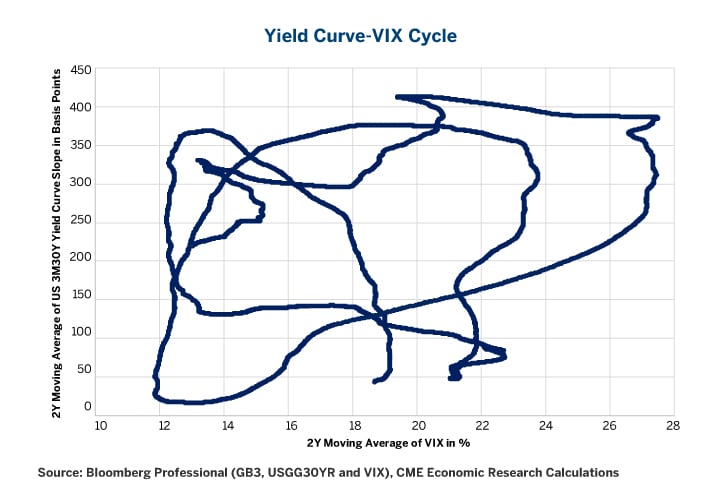

We freely admit: Figure 1 is probably the strangest chart that you will ever see, at least in finance. You may be wondering: did they throw blue spaghetti noodle on paper for inspiration and then write an economics article about it? Or, have they spent too much time with disciples of psychologist Timothy Leary, a proponent of experimenting with psychedelic drugs?

Figure 1: Weirdest Chart Ever

{kind=link}

We assure you that neither is the case. The above chart represents three successive iterations of the VIX-yield curve cycle, a strange but powerful economic phenomenon that has persisted since at least the end of the 1980s and to which every fixed income and equity volatility trader should pay attention. Keep reading. We will break it down in much simpler fashion.

What goes ‘round, comes ‘round

The cycle has four phases. As with any circular motion, where to begin is arbitrary, so we will begin at the bottom of the economic cycle and work our way to mid-stage expansion.

- Recession: yield curve moves from flat to steep (upward slope), equity volatility is relatively high.

- Early-stage recovery: yield curve remains steep, equity volatility begins to fall.

- Mid-stage expansion: the yield curve starts to flatten, equity volatility remains low.

- Late-stage expansion: yield curve becomes even flatter, equity volatility soars as fears of recession dominate investor behavior.

The VIX is the index of implied volatility on S&P 500® options and its daily time series is extraordinarily choppy. To see its relationship with the yield curve, we smooth them both by taking a two year (500 business day) moving average and then put the results into an “X to Y” scatterplot. The result is quite extraordinary: consistent counter-clockwise motion.

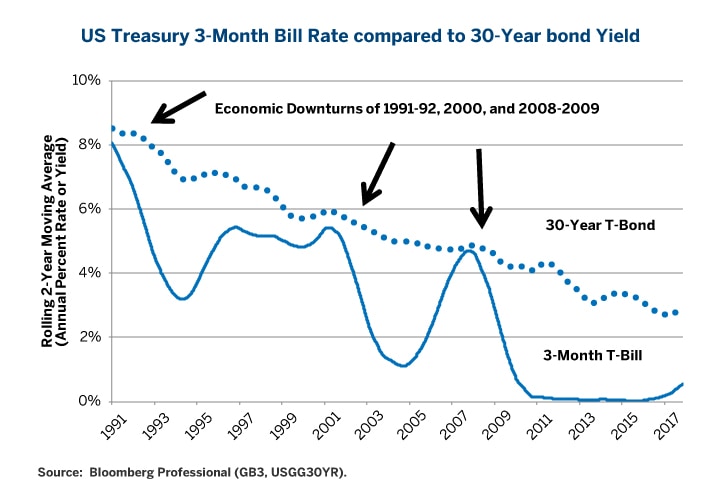

From our arbitrary starting point in a recession, the Federal Reserve (Fed) has responded to the economic downturn with much lower short-term rates. Steep, upward sloping yield curves with short-term rates much lower than long-term bond yields eventually are associated with an economic recovery and lower equity-market volatility. A sustained economic expansion, with relatively low equity-market volatility makes the Fed feel comfortable about removing monetary policy accommodation and flattening the yield curve (i.e., short-term rates moving higher with stable bond yields). A tight monetary policy, flat yield-curve environment finally is associated with an economic downturn and massive correction in the equity and credit markets which sends volatility soaring. High volatility and a crashing economy force the Fed to lower short-term rates and ease policy in order to assist in generating an economic recovery. Wash. Rinse. Repeat. (Figures 2, 3, 4).

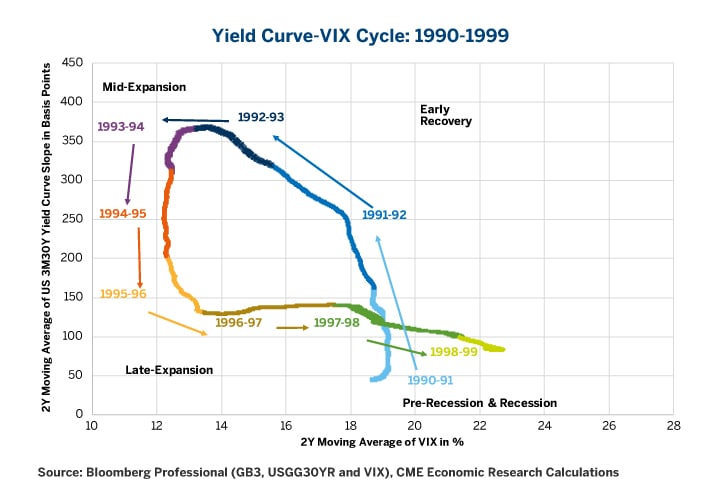

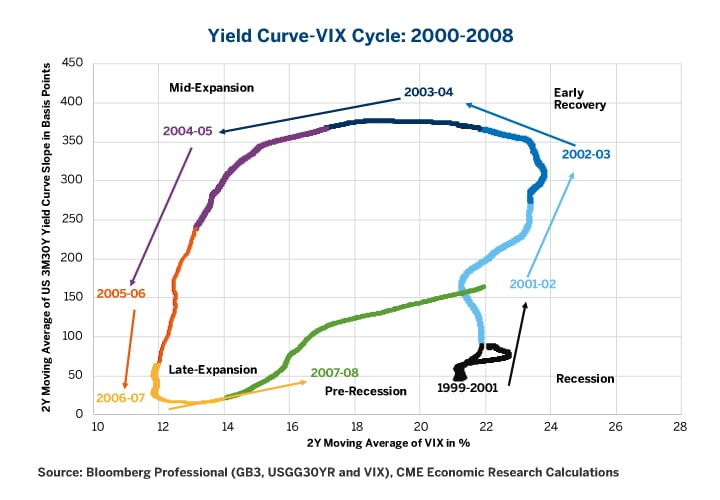

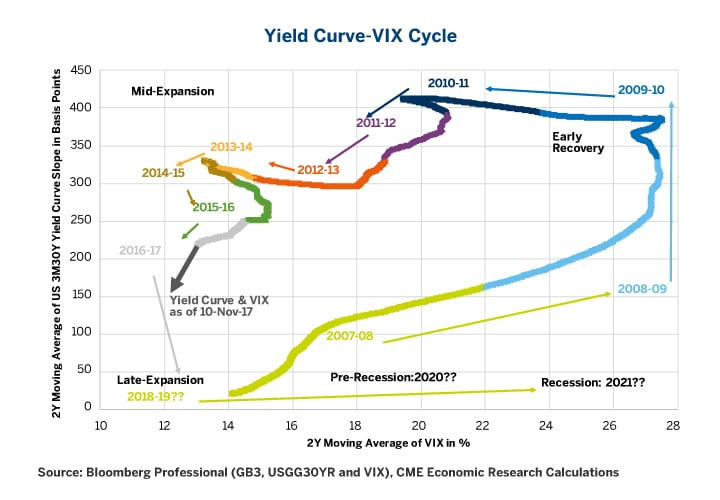

This same four-stage cycle occurred (1) in the 1990-1999 period, ending in the “Tech Wreck” on Wall Street and an economic downturn with rising unemployment; (2) in the 2000-2008 period, ending in the spectacular “Housing Bust” and Wall Street panic, triggering sharply rising unemployment; and (3) the 2009-??? period in which we are now in stage four, with the Fed raising short-term rates, the yield curve starting to flatten, and the economic expansion looking a little long in the tooth.

Figure 2: The 1990-1999 VIX-Yield Curve Cycle

{kind=link}

Figure 3: The 2000-2008 VIX-Yield Curve Cycle

{kind=link}

Figure 4: The Current VIX-Yield Curve Cycle

{kind=link}

That is, currently, the markets are in a phase that closely resembles the mid-expansion phases seen during the mid-1990s (1994-96) and the mid-2000s (2005-06). As already noted, the Fed has commenced removing monetary accommodation. Yield curves are flattening. VIX remains unperturbed at extraordinarily low levels. This phase may persist another year or so as the yield curve continues to flatten and the VIX, most likely, remains low for a while longer. How long this lasts depends upon the Fed and the economy. The faster the Fed tightens, the more quickly the yield curve will flatten, and the more likely the markets will move to the next phase.

The next phase is the late-stage economic expansion. By this time the yield curve will be quite flat. VIX will start to rise from its current two-year moving average of around 12% to much higher levels, perhaps as much as 50% to 100% higher depending on the degree to which market participants fear a future recession. The combination of a flat yield curve and higher equity volatility will probably also blow out credit spreads and choke off lending to certain sectors of the economy, which has the potential to provoke a sharp slowdown in economic activity and then another easing cycle.

The Interplay of Fed policy and Economic Downturns

What makes this cycle tick is the interplay of Fed policy and economic downturns. At the beginning of our cycle, rising unemployment in a recession triggers a Fed policy shift to much lower short-term interest rates. Treasury bond yields typically decline as well with lower inflation expectations, although the drop in short-term rates far outweighs any bond rally. Easier monetary policies are then associated with the end of the recession and start of the recovery. At the end of the cycle in the late-stage economic expansion, it is fears of rising inflation associated with very low unemployment which is the catalyst for the Fed shifting to a tighter monetary policy.

Figure 5: Economic Downturns and T-Bill Rates

{kind=link}

While displaying some consistent themes, every “VIX – Yield Curve” cycle also responds to different external forces. And, in some cases, the line of causality from late-stage economic expansion to recession is not so clear.

In the late 1990s, there was the exuberance of a market fueled by rising technology stock valuations even as earnings from these companies were only growing slowly. The general view of the progression of events was that the Fed tightening triggered the “Tech Wreck” in stocks and that was the catalyst for the economic downturn.

The 2008-2009 economic disaster had a different story to tell. This time, the 2003-2005 mid-stage expansion had featured a housing boom fueled by lax banking oversight and regulation, as well as, a 1% federal funds rate with a sharply upward sloping yield curve. The Fed removed the monetary accommodation in 2005-2006, taking the federal funds rate to 5% and flattening the yield curve. This action stalled the housing boom. The straw that broke the camel’s back, or the catalyst for the deep recession, however, was the financial panic that occurred in September 2008 when the U.S. Fed and Treasury collaborated to put Lehman Brothers into bankruptcy and bail-out AIG to ensure certain other investment banks remain solvent. Compared to the previous period of rising unemployment in 2001-2003, 2008-2009 was characterized by massive de-leveraging across many sectors of the economy, leading to an exceptionally deep recession, now known as the “Great Recession”.

The current economic expansion, which started back in late 2009, is now the second longest on record in the post-WWII period. And, it has displayed a number of different characteristics from our two previous “VIX – Yield Curve” cycles examined here. As already mentioned, the 2008 crisis was a “financial de-leveraging” recession, which is typically deeper and does not display “V-Shaped” recoveries. And, the slow pace of economic growth in the expansion led to the use of unconventional monetary policy (i.e., asset purchases or Quantitative Easing) by the Fed. QE worked to raise asset prices and push volatility even lower but failed to encourage more economic growth or push inflation higher. The QE phase distorted the shape of the yield curve by pushing bond yields lower. The removal of monetary accommodation was delayed, although we are now observing this stage in action, and this time around it includes raising short-term rates as well as unwinding Quantitative Easing.

The last factor of note in this cycle is the persistence of low inflation. The Fed typically views inflation as being pushed higher by low unemployment and tight labor markets, and that has not happened in this cycle, at least not yet. Thus, the Yellen Fed has admitted to some confusion about the economic outlook and has been exceedingly cautious in raising short-term rates. Indeed, the -Fed under Jerome Powell may even consider raising its long-term inflation target from 2% to, perhaps, 3% or 4%. This would signal a desire by the Fed to stop raising short-term rates while it unwinds QE. And, it might prolong the period of an upwardly sloped yield curve.

The alternative scenario is that the Fed tightens by a total of 75 basis points (bps) in 2018 (in addition to the 25 bps it has signaled for December 2017), as its “dot plot” suggests. If rates were 100 bps or 1 percent higher by end of 2018, then that should put the current cycle on course to take a sharp right turn across the bottom of the graph. This might move up not only equity index volatility but also implied and realized volatility on all manner of products including high yield bonds, Treasuries, metals, currency and perhaps even energy and agricultural goods options.

As the saying goes: watch this space.

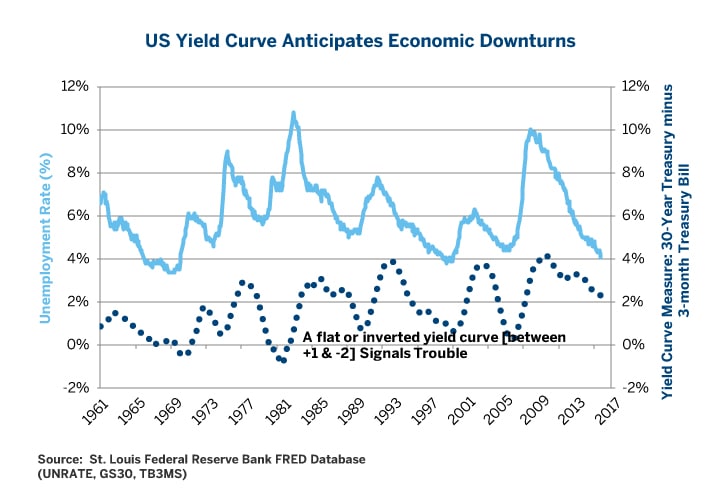

Figure 6: Yield Curve Anticipates Economic Downturns

{kind=link}

Bottom line:

- Two-year average yield curve slopes and VIX levels move in a four-stage cycle.

- Currently, we are in the mid-to-late expansion stage.

- Additional Fed tightening will flatten the yield curve more, which will eventually provoke an explosion in volatility as the VIX’s average level might double from current levels.

- It is likely the volatility will increase across a broad range of products including bonds, metals and currencies as well.

Volatility Ahead?

Our analysis of past economic cycles offers the view that the United States could be heading into a period of high volatility across a range of markets, including bonds, metals and currencies, as additional Federal Reserve tightening further flattens the yield curve. Hedge against uncertainty with a suite of CME Group products in all the significant asset classes.