{kind=link}

Credit Spread-Yield Curve: All Eyes on the Fed

Credit Spread-Yield Curve Cycle: All Eyes on the Fed

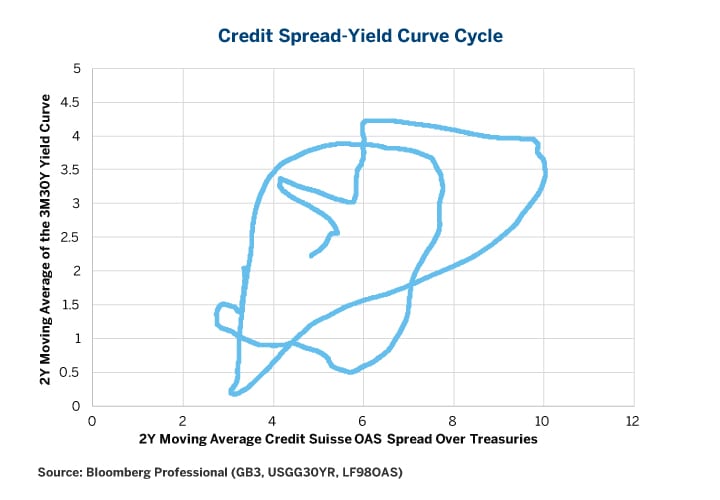

In our previous paper on the VIX-Yield Curve Cycle, we described a circular motion that occurs between the yield curve’s two-year moving average and the VIX’s two-year moving average, and that the cycle has been repeated three times since 1989. Turns out an extremely similar pattern arises between the yield curve and credit spreads, specifically with the Credit Suisse High Yield Bond Index and its option- adjusted spread (OAS) over U.S. Treasuries of comparable maturity. As with the VIX-yield curve cycle, looking at the overall cycle needs proper explanation (Figure 1). So, let’s break it down.

Figure 1: This Work of Modern Art Explains Everything (Just Kidding)

{kind=link}

The Credit Spread-Yield Curve Cycle

The cycle has four phases. As with any circular motion, the starting point is arbitrary; so, let’s begin at the bottom of the economic cycle and work our way around it.

- Recession: credit spreads are extremely wide and the yield curve has been flat. The central bank responds to the deteriorating economy by lowering rates, which steepens the yield curve.

- Early-stage recovery: yield curve remains steep; credit spreads remain wide but begin to narrow.

- Mid-stage expansion: credit spreads have narrowed considerably, economic growth solidifies and the central bank begins tightening monetary policy, flattening the yield curve.

- Late-stage expansion: yield curve remains flat and may even periodically invert; credit spreads begin widening and eventually blow out, signaling a coming economic downturn.

Credit spreads and yield curves are both somewhat choppy on a day-to-day and month-to-month basis. What we are interested here is not so much the exact state of the market on any given day but rather the overall climate. As such, to see the relationship between credit spreads and the yield curve, we smooth them both by taking a 500-day (two year) moving average and then put the results into an “X to Y” scatterplot. The result is quite extraordinary: almost perfectly consistent counter-clockwise motion.

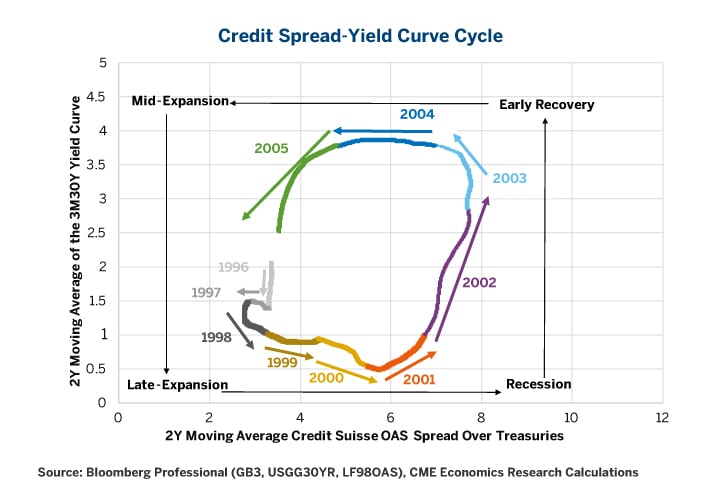

Since we don’t have a long timeseries for credit spreads as we have with the VIX, we will examine two full cycles from the middle of the 1990s expansion to the middle of the 2000s expansion (Figure 2), and then from the middle of the 2000s expansion to now (Figure 3). Currently, we appear to be in the mid-to-late stages of an economic expansion.

Before we begin to dissect Figure 2, first a bit of background. After a period of flat yield curves in 1988 and 1989, credit spreads exploded in the late 1980s with the collapse of the “junk bond” market and it primary market maker, Drexel Burnham Lambert. By late 1990, the U.S. economy was in recession and the credit markets remained dislocated until the end of 1991. The Federal Reserve (Fed), lowered its Fed Funds target rate from 9.75% in 1989 to 3% by 1992 in order to generate a recovery. By 1991 the yield curve was extremely steep, and by 1992 credit spreads began to narrow.

A steep yield curve and narrowing credit spreads continued throughout 1993 and, in February 1994, the Fed took the bond market by surprise and began to tighten policy, raising the Fed Funds rate from 3% to 6%, achieving a soft landing for the economy in 1995 that allowed the central bank to bring rates back down to 5.25%, where they stood until 1997.

It’s in this period that Figure 2 begins. By 1996, credit spreads were as narrow as ever. The yield curve still had some steepness but was on a flattening trajectory. In March 1997, the Fed hiked rates once to 5.5% and shortly thereafter the first signs of trouble appeared. In June 1997, the Thai baht fell off its peg to the U.S. dollar, triggering a crisis that quickly sent most of Asia, excluding China, into a downturn that culminated in 1998 with the Russian debt default and the subsequent collapse of large hedge fund Long- Term Capital Management (LTCM). The Fed staved off a U.S. recession by lowering rates to 4.75% in the late summer and fall of 1998 but began raising rates again in June 1999, with the Fed Funds rate reaching 6.5% in March of 2000. During this time credit spreads widened considerably.

Figure 2: The Mid-1990s Expansion to Mid-2000s Credit Spread-Yield Curve Cycle

{kind=link}

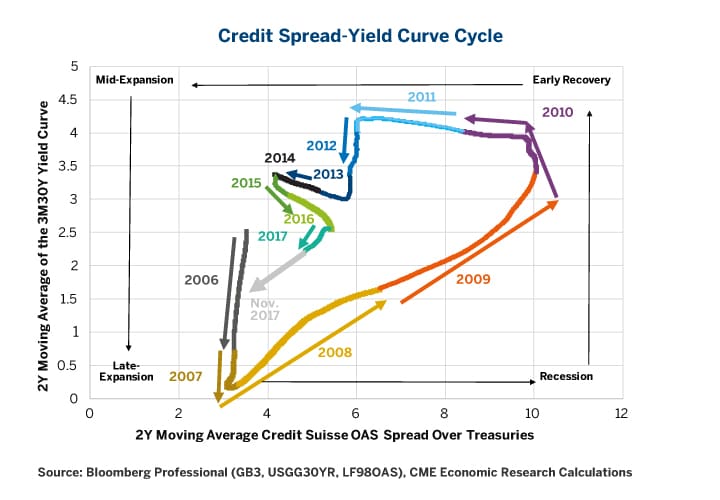

By 2001 the economy was in a recession, now remembered as the Tech Wreck and notable for a collapse in business investment. The NASDAQ 100 fell over 80%. Credit spreads were extremely wide. The Fed began slashing rates in January 2001, and by November 2001 the Fed Funds rate was at 1.75%. The Fed lowered rates to 1.25% by the end of 2002 and to 1% in June 2003. Dramatic cuts in the interest rates helped to isolate the recession to the business investment component of the gross domestic product while consumer spending grew slowly and housing boomed, spurred by low rates.

By late 2001 the yield curve was steep and remained so for three years. In the spring of 2003, credit spreads began narrowing and had tightened considerably by 2004. With credit spreads narrow, equity markets calm, economy growing and unemployment falling, the Fed, in June 2004, embarked on a series of interest rate increases that took rates from 1% to 5.25% by June 2006.

By late 2006 the yield curve was flat and credit spreads remained narrow, but not for long. The first signs of crisis emerged in February 2007 when some investors began to worry in earnest about subprime housing loans. In July and August 2007 credit spreads began to explode, eventually reaching far wider levels than in 1990 or in 2001. Our credit spreads-yield curve graph began making a sharp right turn across the bottom of the graph, signaling a coming end to the expansion. The Fed cut rates slowly at first, but then accelerated the pace until they reached 0.125% by the end of 2008.

The Fed’s rates cuts worked their magic. By 2009 the yield curve was steep, credit spreads began narrowing in March of that year and by 2011 had tightened considerably. Since then, however, a few factors have made our yield curve-credit spread cycle less smooth than in its previous iteration.

Figure 3: The 2006 Till Now Cycle

{kind=link}

Three rounds of quantitative easing (QE) put some kinks in the yield curve. When the Fed could no longer lower rates, it began to buy bonds further up this curve. This might have led to a yield curve that was less steep than it would otherwise have been. Moreover, there is no clear evidence to suggest that QE benefitted the recovery. When the Fed embarked on QE3 in early 2012, growth did not accelerate, but the yield curve did flatten and credit spreads, for a time, stopped narrowing. When the Fed announced the tapering of QE3 in May 2013, credit spreads began narrowing again and by the end of 2014 had fallen considerably.

Credit spreads blew out again in 2015 as the price of oil collapsed from $90 to below $50 per barrel, falling as low as $26 by February 2016. During this time, the Fed worked up the courage to hike rates once in December 2015, without having much impact upon the yield curve.

By late 2016 oil prices had rebounded. Fears of an energy sector credit meltdown faded. With spreads narrowing again, the Fed embarked on a more aggressive pace of rate hikes, with one rate hike in December 2016 and two thus far in 2017. In addition, the Fed began unwinding QE, contracting its balance sheet, and will almost certainly hike rates one more time at its December 2017 meeting. This has resulted in some yield curve flattening that has brought us to a point in the credit spread-yield curve cycle that closely resembles where we were in 2005 on the chart but with important differences.

Now, economic imbalances are not as apparent as they were in 2005. There is no housing bubble. Although the S&P 500® has soared from 666 in March 2009 to around 2,600 today, it’s not clear if there is an equity market bubble or not. On the one hand, certain valuation ratios are high and on the other hand long-term interest rates used to discount those future earnings are low. So, relative to bonds, equities don’t look all that expensive. Some observers think that bitcoin and other cryptocurrencies are in a bubble but, for the moment, their total market cap is only around $250–$300 billion, which is probably too small to significantly damage the global economy even if they fell out of favor tomorrow.

From a macroeconomic perspective, U.S. unemployment has fallen to 4.1%, among its lowest levels over the past half century. Even so, there is scant evidence of wage pressures and both trailing consumer price inflation and inflation expectations remain tame.

As such, there is the mystery of what the Fed does next. Does it stay on auto-pilot and raise rates another 75 basis points (bps) each in 2018 and in 2019? This is what the Fed’s “dot plot” of Federal Open Market (FOMC) members’ expectations for Fed policy suggests. If it follows this course, look for a flat yield curve by the end of the year or at some point in 2019, followed by a widening and then explosion of credit spreads and a recession around 2020 or 2021.

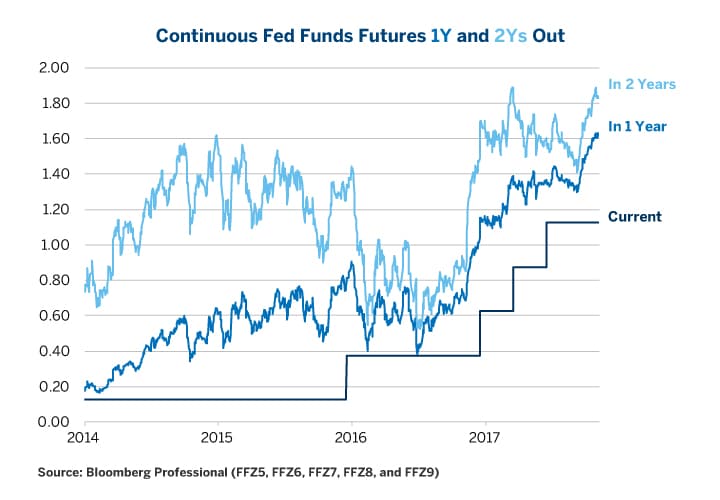

For the moment, the market does not believe this scenario one bit. Fed Funds are currently pricing one more rate hike in 2017 to 1.25-1.50% and are pricing a less than 100% chance of one more rate hike each in 2018 and 2019 (Figure 4). If traders are right and the “dot plot” is wrong, then the yield curve should maintain adequate steepness to compress credit spreads further – perhaps by 100 bps or more on the Credit Suisse High Yield OAS Index. This should keep the economic expansion going through 2018 and 2019 and perhaps well into the next decade, and unemployment could fall towards its 1968 lows of 3.2%. If it’s not broken, don’t fix it!

Figure 4: Fed Fund Futures Price That Fed’s Powell & Co. Won’t Be in a Hurry on Rates.

{kind=link}

Moreover, the Fed’s current “dot plot” might not be very meaningful since there is a high turnover at the Fed. Although incoming Fed Chairman Jerome Powell doesn’t represent much of a change from his predecessor Janet Yellen, many of the other FOMC members around him will be changing. Will they continue to hike on autopilot and set the stage for what might be an entirely unnecessary and unjustified widening of credit spreads and a recession? Or, will they allow the economy to expand considerably further before taking away the punch bowl?

Also, what impact will the Fed’s unwinding of QE have on credit spreads? QE3 didn’t appear to help the credit markets, which healed themselves better both before and after QE3 than during it. Will contracting the balance sheet cause spreads to widen or will it keep the yield curve steeper than it would otherwise be and enable a narrowing? We don’t know the answer but it will be interesting to watch for the developments. Ultimately, the answer to that question could prove difficult to discern.

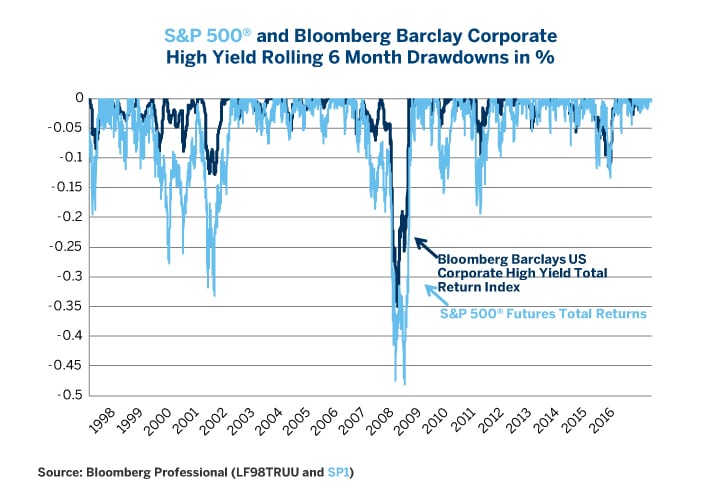

Either way, a credit spread explosion will occur eventually. When it happens, high yield bond investors will need a way of hedging it. This was the subject of an earlier paper which points out that high yield bond drawdowns and equity index drawdowns often coincide (Figure 5). Shorting equity index futures to hedge bonds can be an extremely painful trade. With credit spreads narrow, high yield bond returns are somewhat limited to the upside. This is not necessarily the case for stocks, which could experience a blow off end-of-decade rally. This asymmetry results from corporate bonds representing a short put option on the debt of a company, while equity represents a long call option. The most that the owner of a short put option can hope to collect is the premium of selling the option, in this case the principal plus the coupons on the bond. By contrast, the theoretical upside of a long call is unlimited.

That said, past drawdowns in yield high bonds have often coincided with equity drawdowns and, if one times it right, hedging high yield credit exposures with futures could reduce portfolio risk. To that end, the credit spread-yield curve cycle might provide one with a better sense of timing. If one is considering hedging high yield exposures with equity index futures, one might be better off waiting until the yield curve is considerably flatter than it is today. With the yield curve as steep as it is today (close to its long-term average), hedging high yield bond positions with equity index futures may be premature.

Figure 5: High Yield Bond and Equity Market Drawdowns Often Coincide

{kind=link}

Bottom line:

- Two-year average yield curve slopes and credit spreads levels move in a four-stage cycle.

- Currently we are in the mid-to-late expansion stage.

- If the Fed continues to tighten policy at the current pace in 2018 and 2019, as their “dot plot” suggests, it is likely that the yield curve will flatten, credit spreads will widen and the economy will go into a recession, perhaps around 2020 or 2021.

- If the Fed tightens more slowly, as Fed Fund futures are currently pricing, the mid-to-late expansion phase could last considerably longer and credit spreads might even continue to narrow.

- The best time to use equity index futures to hedge credit exposures might be when the yield curve is flat.

- Hedging high yield bond exposures while the yield curve is at average levels of steepness could be expensive given the asymmetries in the short put-like return profile of corporate bonds and the long call-like return profile of equities.

Recommended For You

Fed Watch

The Federal Reserve is widely expected to raise interest rates by 25 basis points on Wednesday, Dec 13. Our research shows that if the Fed raises rates by 75 basis points each in 2018 and 2019 as suggested by its 'dot plot,' the U.S. economy could slip into a recession in 2020 or 2021. Get a front row seat to the probabilities of the next Fed rate hike with the CME FedWatch Tool.