{kind=link}

Seven of the Most Noteworthy Trading Days of 2016

With the big changes of 2016 still fresh in our memories, we take a look back at the year’s seven most interesting trading days to review what we may have learned (or not) about managing risk.

The U.S. elections and UK’s Brexit referendum highlighted the need to manage political event risk, especially since opinion polls proved unusually unreliable.

Monetary policy was on the move around the world. Following the Bank of Japan’s (BOJ) surprise move into negative rates at the end of January 2016, the European Central Bank (ECB) pushed further into negative rate territory in March 2016. In contrast, the U.S. Federal Reserve (Fed) hiked rates in December 2016 for only the second time since the financial panic of 2008. With the unemployment rate below 5% and inflation creeping higher, the Fed signaled that more rate hikes are to come in 2017.

Gold was challenged as sentiment rose that the Fed would hike rates, and as technical factors underscored the weakness. Energy markets were volatile. Oil dropped below $30 per barrel in February 2016, yet after the Organization of the Petroleum Exporting Countries (OPEC) deal on production cuts in late November, oil rose above $50. Agricultural markets were especially active in the spring of 2016 as U.S. corn exports rose while weather and political risks in South America roiled expectations of crop exports from Brazil and Argentina.

2016 was certainly a year of change, and all indications are that we may see more surprises in 2017. The focus on political event risk is shifting to Europe; fiscal/monetary policy contrasts among countries are sharpening, and commodity markets are in a tug of war between demand and supply forces pulling in opposite directions. Moreover, as the surprises in 2016 underscored, managing these risks requires robust and liquid markets in all time zones for the major global indices, such as those provided in the exchanges operated by CME Group.

And now, for our review of the seven most interesting trading days in 2016, in reverse order:

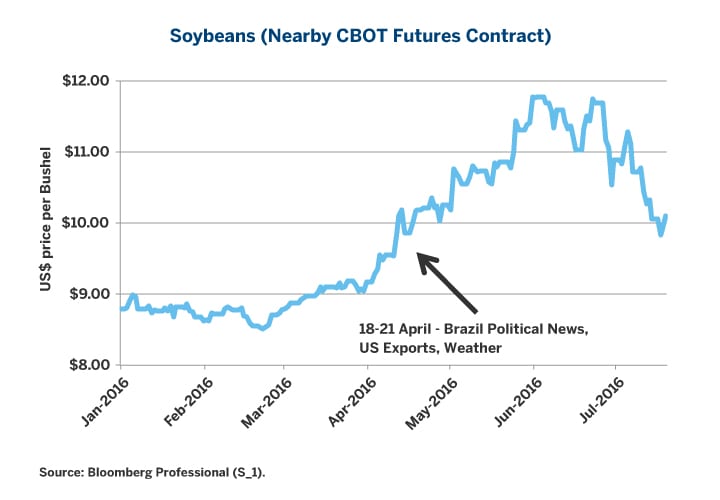

#7: Wednesday-Thursday, 20-21 April, 2016 – U.S. Exports, South American Weather, Brazilian Politics – Agriculture Futures and Options

The week of 18 April, 2016, was an exciting one for agricultural products. In the U.S., export inspections indicated larger-than-expected sales. In South America, weather patterns encouraged corn and soybean buying as a string of rainy days in Argentina coupled with dry heat during pollination in Brazil made U.S. corn and soybeans ever more attractive. Early in the week, Brazil’s Lower House voted to initiate impeachment proceedings against then President Dilma Rousseff. Later that week, Brazil eliminated its corn import tax. All of these factors combined to push prices higher.

In the CME Group suite of agriculture futures and options products, an all-time daily record of 2,989,799 contracts changed hands on April 21, well over twice the typical average daily volume of 1.3 million. Indeed, volumes on Tuesday April 19 (2.56 million contracts), Wednesday April 20 (2.97 million), Thursday April 21 (2.99 million), and Friday April 22 (2.68 million) demonstrated how remarkable the whole week was, with trading activity coming not just from the United States but from all over the world, in very deep and robust markets for corn, soybeans and wheat.

Figure 1.

{kind=link}

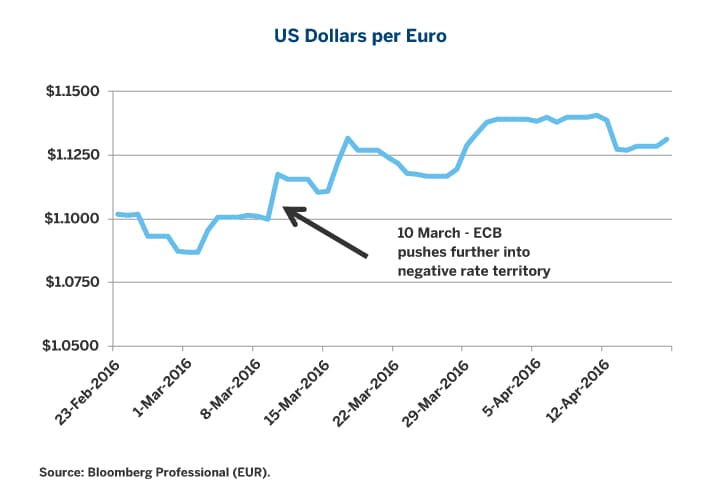

#6: Thursday, 10 March, 2016 –ECB Pushes Further into Negative Rates – FX Futures

At the ECB policy meeting on Thursday, March 10, 2016, the central bank pushed its deposit rates further into negative territory. The intent was to weaken the euro against the U.S. dollar and other currencies. And the euro did depreciate with the instantaneous market reaction, only to turnaround and appreciate to the surprise of many. Negative rates, however, work to penalize a capital-constrained banking system and may lead to a further disruption of credit markets rather than encouraging them to expand lending. That is, while counterintuitive to some, negative rates were treated by the market as a net tightening of credit, and the euro appreciated.

CME Group foreign exchange futures (not including options) hit an all-time daily record of 2,348,459 contracts traded on March 10, led by activity in the euro (versus U.S. dollar). This compared with a typical day in 2016 of an average of 787,000 contracts or about three times the average daily volume.

Figure 2.

{kind=link}

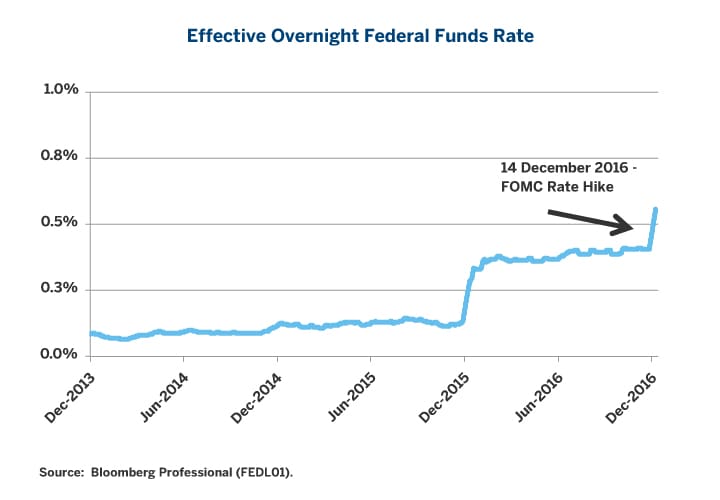

#5: Thursday, 15 December, 2016 – Federal Open Market Committee (FOMC) Raises Rates – U.S. Rates Options

The Fed’s Federal Open Market Committee (FOMC) raised its target range for the overnight federal funds rate by 25 basis points in its meeting on Wednesday 14 December. This was a widely expected rate hike as CME’s Federal Funds Futures had been signaling a near 100% probability of a rate hike in the weeks before the FOMC decision. Interestingly, even though the move was expected by nearly everyone, the day after the rate hike decision saw an all-time record day in CME Group rates options products, led by Eurodollar deposit options.

A total of 6,192,237 rates options contracts traded on December 15, about 3.4 times the typical daily volume in 2016. While the FOMC rate hike was the catalyst, the press release from the Fed indicated three more rate hikes to come in 2017, and generally a more confident view that inflation was inching higher and would soon move above the Fed’s 2% target. As a result, the yield curve tilted upward with longer-dated maturities seeing higher yields compared to short-term maturities.

Figure 3.

{kind=link}

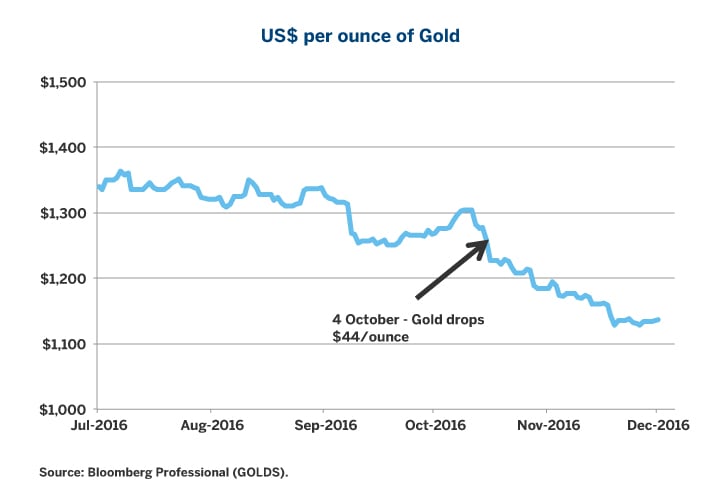

#4: Tuesday, October 4, 2016 – Gold Drops $44 (Market Technicals vs Fed Rate Speculation vs VP Debate) -- Gold Options

On Tuesday, October 4, gold precipitously dropped by $44/ounce. The catalyst was not so clear and subject to considerable debate. While there were Fed speeches suggesting a rate hike was coming in December (higher rates are not good for gold which bears no interest), there was the U.S. Vice-Presidential debate (which was not likely to have mattered) and technical indicators had been signaling the potential for a breakdown in the gold price.

Trading was intense in the Asian time zone even before U.S. traders woke up. October 4, 2016, was the highest volume day for gold options, with 147,514 contracts traded, although it was well below the all-time record for gold options set on April 15, 2013, of 227,516. Still, options trading on the October 4 was still 3.7 times the 2016 average daily volume, and the trading displayed deep liquidity in the Asian time zone.

Figure 4.

{kind=link}

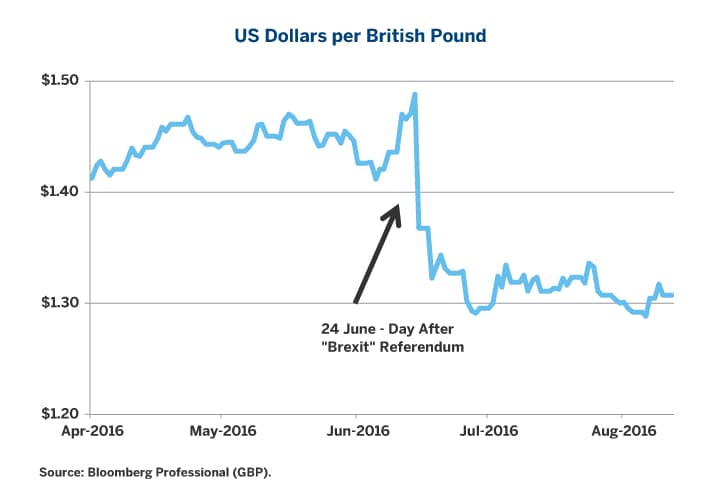

#3: Friday, 24 June, 2016 – Brexit Referendum – British Pound

On the June 23, 2016, the referendum in the UK delivered a decisive victory for the “Leave” camp in a rejection of membership in the European Union. At dawn on June 24 came the resignation of British Prime Minister David Cameron, who had called the referendum and advocated for the “Remain” camp. Before the polls had closed, there was a general sense that probabilities favored the “Remain” camp. Within hours after the polls had closed and the results started to trickle to the news media, it was clear that a big surprise was at hand. Markets aggressively took the value of the pound lower by about 7%. Equity markets across Europe sold-off in sympathy on the day, although they recovered in later weeks while the pound did not.

Across all CME Group futures and options products, Friday, June 24 was a very active day, with 29.4 million contracts traded – not a record, but still about twice typical daily volume. Not surprisingly, an all-time record was set for the British pound (versus U.S. dollar) futures and options at 546, 677 contracts traded, a little over four times the 2016 average daily volume. And, since the Brexit vote results were announced during the night in the U.S., this event again displayed the robustness of CME markets in non-U.S. hours.

Figure 5.

{kind=link}

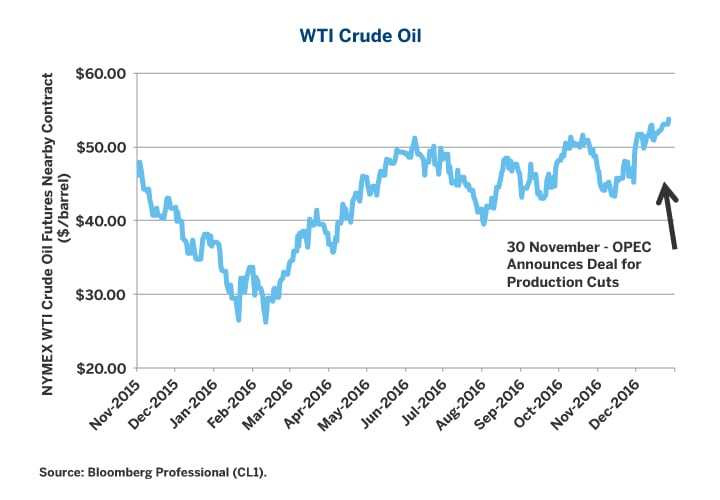

#2: Wednesday, 30 November and Thursday, 1 December, 2016 – OPEC Production Cuts Lead to Big Oil Rally

OPEC announced on Wednesday, November 30, that it had agreed to production cuts. There was considerable debate about whether Saudi Arabia could get other countries to go along, given that most nations in the cartel are seriously in need of cash flow. When OPEC delivered a deal to cut production, oil prices surged about 9%, reversing the price declines of late September and early October when the deal had appeared to fall apart.

On November 30, NYMEX WTI crude oil futures (not including options) traded an all-time record of 2,574,363 contracts, well over twice the typical daily trading volume for 2016. December 1 was not quite as busy, still about 2.1 million contracts changed hands.

NYMEX WTI options also hit an all-time record volume of 610,427, or three times typical daily volume, on November 30. In effect, the OPEC deal signaled a new phase in the tug of war between U.S. shale producers and Saudi Arabia as to who is the real swing producer. U.S. shale producers have become exceptionally efficient and can add rig count quickly when prices rise. Saudi Arabia, on the other hand, may display discipline in its production but the jury is still out as to how other OPEC members will manage their production targets.

Figure 6.

{kind=link}

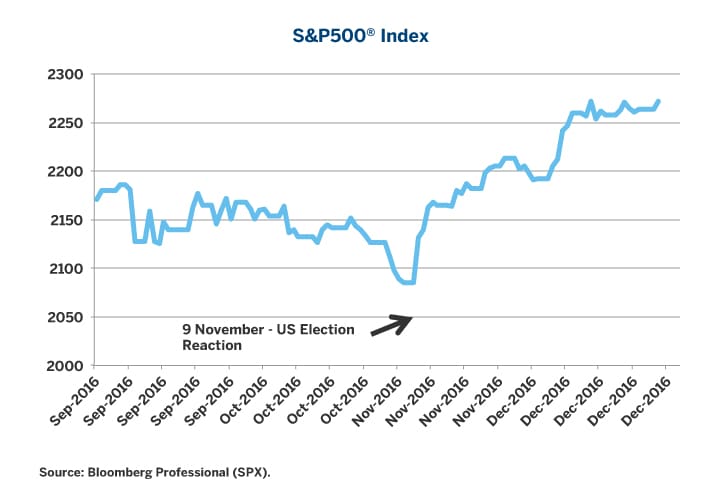

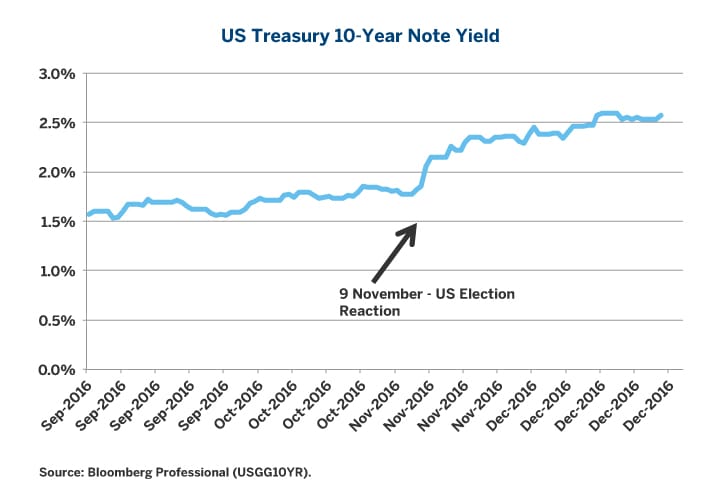

#1: Wednesday, 9 November, 2016 – U.S. Election – Rates, Equities, Gold

The U.S. election on November 8, 2016, like Brexit, delivered a surprise, with a clean sweep of the White House, Senate, and House of Representatives by Republicans. The instantaneous market reaction was to take equity index prices sharply lower, by about 5%. Overnight in U.S. time, however, a vigorous turnaround was initiated, and U.S. equities finished up on the day on Wednesday, November 9. Stocks kept on going higher into the year-end, as market participants realized that the Washington gridlock had been ended, and they cheered the prospects of lower tax rates on corporations, lighter-touch and less costly regulations, and the potential for infrastructure spending down the road. In contrast, as equities were rallying, U.S. Treasuries were seeing prices fall and yield rise on expectations that a stimulative fiscal policy meant large budget deficits, rising national debt, and more inflation ahead.

CME Group futures and options products set all-time records for total volume at 44,509,097 contracts traded on November 9, 2016, eclipsing the previous record of 39.6 million set on October 14, 2014. All-time volume records were also set for trading in the rates sector, and gold. Equities showed large volumes, but did not eclipse the previous record set on September 18, 2008, as the financial crisis started to unfold.

Figure 7.

{kind=link}

Figure 8.

{kind=link}

Risk Management Lessons

Our seven most interesting trading days in 2016 brought some useful lessons for risk managers.

Political risk was extremely high, as evidenced by the U.S. elections and the UK Brexit referendum. Political events often involve binary choices, which in turn mean that pre-event return expectations may display bimodal characteristics. That is, if “A” then prices up, if “B” then prices down, and very little likelihood of calm markets once the outcome becomes known. Options, with their focus on expected volatility, are well-suited for managing event risk, as 2016 demonstrated.

Policy risk was also in focus. In the U.S., post-election fiscal policy is moving toward stimulus, while the Fed is slowly removing policy accommodation. In contrast, the ECB and the BOJ remain committed to aggressive easing. A sharpening of policy divergences is very likely to move markets in 2017, including foreign exchange, gold, interest rates, and equities.

The tensions in the energy markets were highlighted all through 2016. Saudi Arabia attempted to reassert itself as the world’s swing producer – willing to cut production to support prices. While U.S. shale producers have grown ever more efficient and can ramp up rig count and production when prices rise.

Finally, weather patterns are likely to emerge as major influences on agricultural markets in 2017. The El Niño of August 2015 left the scene in 2016, and signs of a developing La Niña with colder-than-usual waters along the equator in the Pacific Ocean, as well as large swaths of colder waters in the Northern Pacific Ocean, are expected to shift jet stream, temperature, and precipitation patterns yet again.

With deep, liquid, and robust round-the-clock markets in major benchmarks ranging from U.S. rates, equities, currencies, energy to metals and agriculture, CME Group is where the world comes to manage risk.