{kind=link}

Housing Poised to Drive Up Inflation?

U.S. Housing Market Poised to Drive Up Inflation?

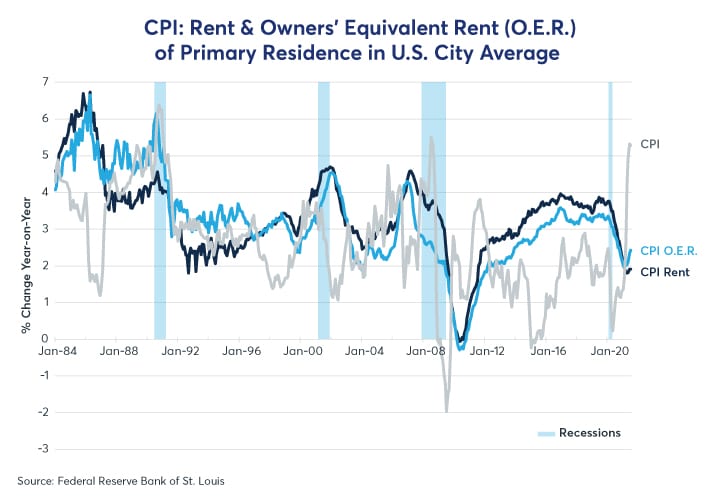

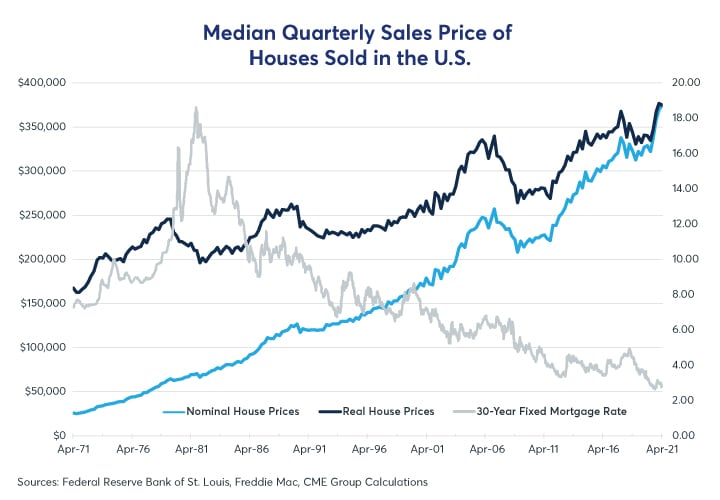

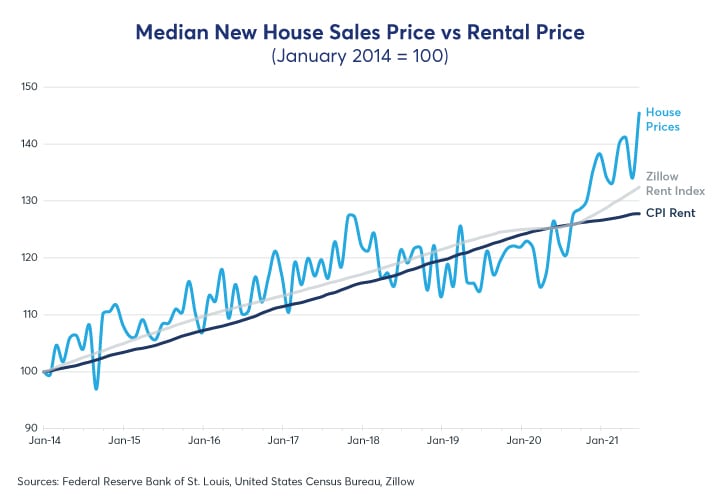

The U.S. consumer price index (CPI) has jumped to its highest annual rate since 2008, yet the housing components of the index (rent and owners’ equivalent rent) have decelerated considerably since the start of the pandemic (Figure 1). For the first time in nearly a decade, housing costs have risen more slowly than the overall CPI. While the headline inflation rate currently stands at 5.4%, the CPI for shelter (which includes rental payments and mortgages) has increased only 2.6% year on year. This is despite the housing market experiencing its broadest boom in at least two decades, with median sales prices reaching record highs in both real and nominal terms (Figure 2).

Figure 1: CPI-OER has lagged the headline rate for the first time since 2012

{kind=link}

Figure 2: As mortgage rates have tumbled, median sales prices have blown past $350,000

{kind=link}

Our research suggests that house-price growth is a meaningful indicator when studying the potential future inflation rates of rent and OER. However, past evidence suggests that rising purchase prices of homes is often not fully reflected in rental prices for around one to two years in the future. This time lag can be explained by the “sticky” nature of rent inflation, and how shelter costs are measured by the Bureau of Labor Statistics (BLS). Given that house prices began to accelerate in September of last year (Figure 3), this implies the possibility of significant increases in rental costs through at least the end of 2022. This might, in turn, contribute almost 1.5 percentage points to core CPI inflation, the strongest contribution of housing to the headline figure since 2007, and may be less transitory than many observers had initially expected.

Figure 3: House price growth is at a record high and accelerating

{kind=link}

There are three fundamental factors driving the overall upswing in house prices, amounting to high demand and low supply:

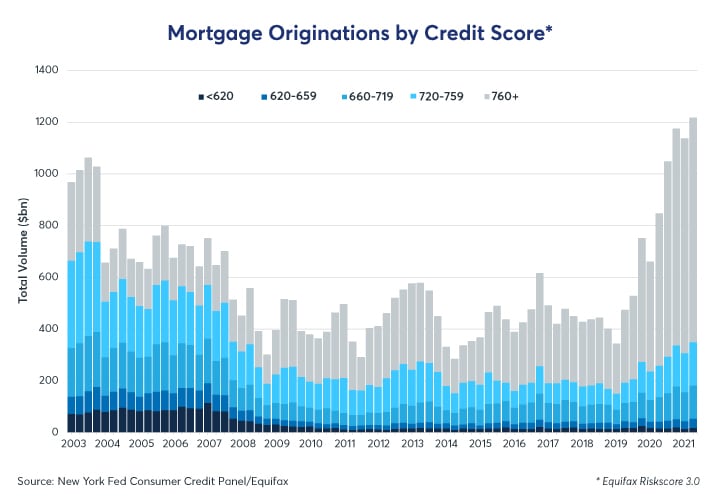

- Low mortgage rates as a result of the Federal Reserve’s $40 billion monthly purchases of agency mortgage-backed securities and $80 billion in U.S. Treasuries. Mortgage originations (Figure 4), in the three months to the end of June exceeded $1.2 trillion – amounting to $4.6 trillion over four quarters, and pushing the total mortgage balance to more than $10 trillion. Notably, the boom in mortgage lending has been driven by loans to those with the highest credit scores. As such, it appears that the Fed’s quantitative easing (QE) programs could be fuelling buying of second and third homes by those who are already quite well off.

Figure 4: 44% of the outstanding mortgage balance was originated in the past year

{kind=link}

- Nearly $4 trillion of savings accumulated during the lockdown (Figure 5), principally as a result of stimulus checks, rising stock markets, and fewer spending choices.

Figure 5: American households’ savings glut may drive up housing demand

{kind=link}

- Weak housing supply and construction (Figure 6 and 7), as a result of languishing confidence over the past decade. Even as confidence has recovered, prohibitively high resource costs – particularly in lumber markets – have delayed the construction of new housing. Structural factors are also at play, including inhibitory zoning and permit regulations, which have made housing supply more inelastic in certain markets.

Figure 6: As housing demand rises, there has been a persistent shortfall in supply

{kind=link}

Figure 7: U.S. monthly housing supply fell to 3.5 months in October 2020, a record low

{kind=link}

It is thus clear that there is a disconnect between house prices and the housing components of inflation indices in the short run; house prices do not move in tandem with OER and rent. This disconnect is due, in part, to the methodology by which inflation indices measure housing costs. Homes are considered as an investment rather than consumption items, as the value of the services they provide (shelter and security) are dwarfed by their price. While there are a handful of other goods in the inflation basket that provide services over a period of time, such as cars and refrigerators, these depreciate faster than property – thus the difference between the intrinsic value of the services and the initial price paid is insubstantial.

House prices were included in America’s CPI between 1953 and 1983 before being removed, as their volatility had profound implications on indexed benefits and pensions. Today, the index uses an estimate of the cost of the service that housing provides to its occupant, rather than changes in the asset price. This cost, referred to as “shelter,” is the sum of two components: a measure of the rents of primary residences (rent), and an estimate of the rent that owner-occupied housing could command (Owners’ Equivalent Rent). These components account for 7.9% and 24.3% of the weighted CPI index respectively, and tend to move together – as OER is typically estimated by observing actual rents on similar properties.

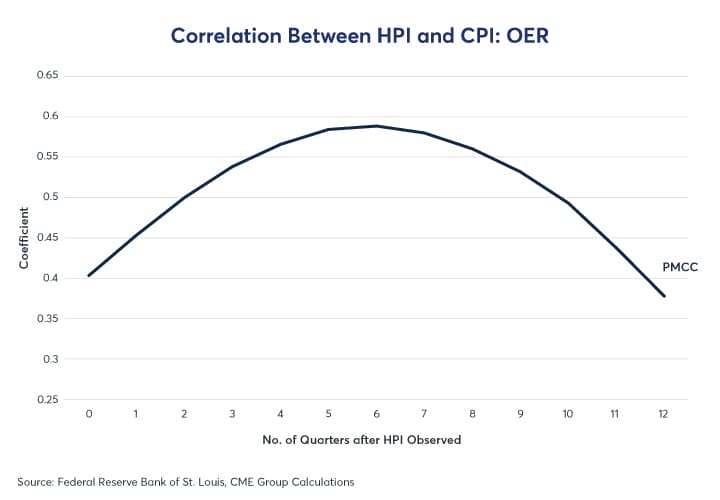

While soaring house prices and sluggish rents may seem counterintuitive, it is indicative of the long-term relationship between house prices and CPI. In reality, an increase in house prices may signal a bout of inflation between 5-7 quarters later (Figure 8).

Figure 8: There is a positive correlation between house prices and CPI-OER, with the highest correlation after 6 quarters

{kind=link}

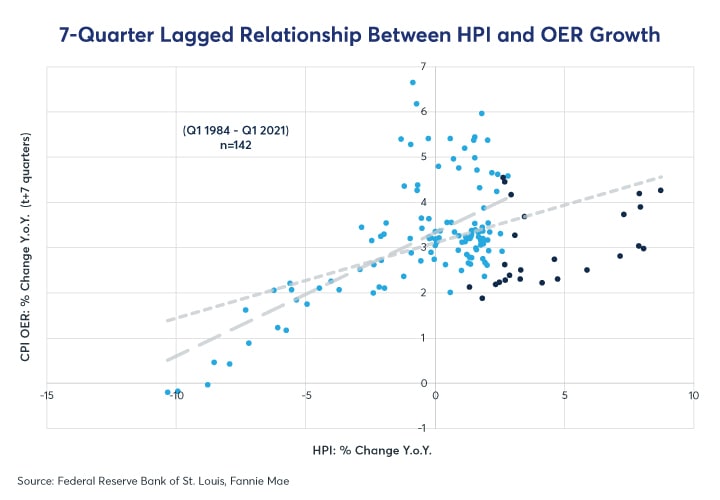

The correlation coefficient between the House Price Index (HPI) and Owners’ Equivalent Rent, measured 6 quarters later, is 0.589. This coefficient rises even further, to 0.749 if the Q1 2002 – Q1 2008 period is omitted. Thus, it appears that this relationship is less reliable when house prices rise quickly as they did from 2002 to 2007. (Figure 9). This is not surprising; just as equity prices can deviate from earnings, so too can house prices relative to the rents that they command. Housing is an investment vehicle that is subject to speculation, which is dependent upon future expectations, long-run interest rates, and risk appetites.

Figure 9: Excluding 2002 Q1 – 2008 Q1 (dark blue), there is a very strong positive correlation between HPI and OER growth measured 6 quarters later

{kind=link}

Excluding the 2002-2008 period, a one-percentage-point increase in the HPI is associated with a 0.27 percentage point increase in the CPI-OER after 6 quarters. This is relatively low, as house prices tend to be more volatile than rents, as they are affected by factors beyond the underlying income stream – such as credit requirements, stamp duties, interest rates, mortgage insurance, homeowner association fees, and minimum down payments.

The basis for this lagged relationship is two-fold. Firstly, there is a lag between housing prices and market rents. Secondly, there is a lag between market rents and CPI indices.

The former is due to the “sticky” nature of rent inflation; leases are typically set for a year, and landlords are frequently hesitant (or legally prohibited) to raise rents significantly on existing tenants. This also explains why rent tends to be less volatile than housing prices: while rent is measured via lagging lease rates, house prices are measured via recent transactions.

The latter is due to the methodological weaknesses of the CPI – manifested in both the OER and rent components of the shelter index.

The OER component requires the owner-occupant to estimate the hypothetical rent on their own home, yet the expectations of these estimates are often adjusted at a slower pace than the housing market is to react to changes in supply and demand. Especially during periods of elevated volatility, households are not perfectly aware of the potential rent prices that their homes can command. As a consequence, their estimates tend to lag market rents.

Similar to the OER, the BLS rent index lags contemporaneous rent measures (Figure 10). This is because the index mainly captures modest changes in rents for existing tenants, and misses larger rental updates brought about by tenant turnover. These larger upswings are further obscured by the smoothing effects employed by the BLS index, which averages the rent for each survey month and calculates a six-month rolling average growth rate. In addition, if all rent leases are annual, then only a twelfth of the sample will reflect current market conditions, with a further twelfth of the sample reflecting economic environments nearly a year old.

Figure 10: The rent component of the CPI has not yet picked up the recent surge in market rental prices

{kind=link}

What does this time lag mean for future rent and CPI inflation? If the relationship between HPI and OER over the past 4 decades is anything to go by, then we may begin to see an acceleration in OER growth over the next 5 quarters. Our own regression model, accounting for recent overestimates, suggests that CPI-OER could reach 3.7% by the end of 2022. This would be the highest rate of growth since 2007, and could contribute as much as 1.2 percentage points to the CPI, and 1.5 percentage points to the core CPI. Naturally, such an estimate has a high degree of uncertainty as the model is less accurate when HPI growth is consistently above 6% - which has been the case over the past three quarters.

This effect is less pronounced for the personal consumption expenditures (PCE) deflator, which assigns about half the weight to shelter as the CPI. The PCE is the main index used by the Fed to measure inflation – but the CPI is closely linked to bond market measures of inflation expectations, which the Fed also watches closely. A rise in OER may elevate CPI and drive up survey-based measures of expected price growth, which will ultimately influence whether the Fed will reduce MBS purchases before year-end.

Shelter may contribute about two-thirds of a percentage point to Core PCE inflation, in spite of representing only 18% of the basket. Given the Fed’s 2.0% target for Core PCE inflation, there is little room for growth among the items composing the other 82% of the index. Even if other transitory effects were to wane, inflation in 2022 and 2023 could be well above the Fed’s target. Thus, housing will play a major role in influencing the Fed’s policy tightening.

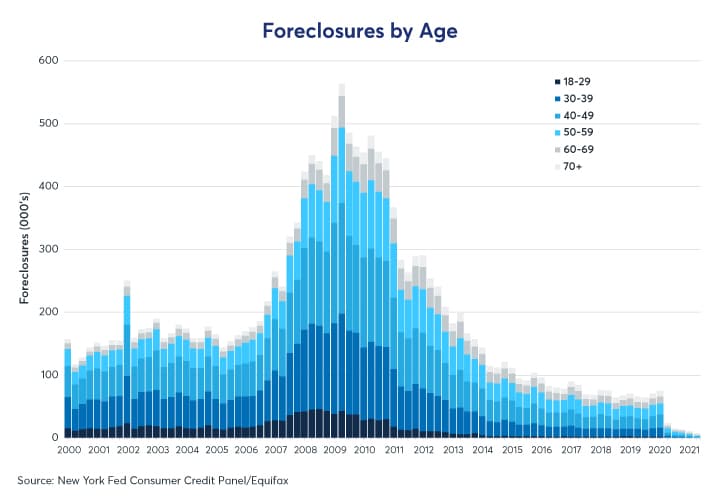

Our single factor model does not represent many of the complexities of the housing market. It does not consider, among other factors, vacancy rates, inflation expectations, and rental yields, all of which could play a role in determining market rents. There are also signs that the housing market is starting to cool. The federal moratorium on mortgage foreclosures ended on July 31st, and was responsible for pushing foreclosures to record lows (Figure 11). The mortgage forbearance program will end on September 30th, and as of July 11th, 1.75 million borrowers were still enrolled in the program. This is in comparison to the 1.37 million units currently available for sale. Should even a small fraction of these 1.75 million homeowners choose to sell instead of going back to repaying their mortgage, it may boost housing supply in a historically tight market. This may keep inflation at bay, especially if a growth in supply is coupled with Fed tapering.

Figure 11: The foreclosure moratorium has sent foreclosures tumbling to record

{kind=link}

Ayushman Mukherjee

Ayushman Mukherjee will be attending the University of Cambridge in October to study Economics.

Interest Rate Products

Explore the deepest centralized pool of liquidity, offering capital-efficient risk management solutions throughout the yield curve.