{kind=link}

Abenomics: A Work in Progress After Five Years

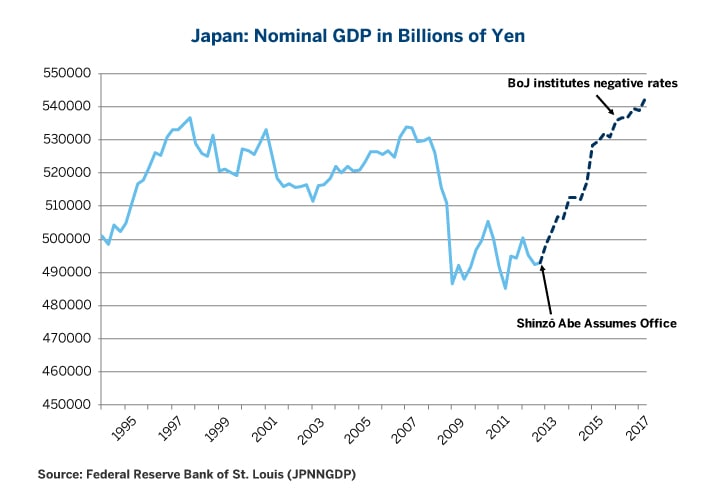

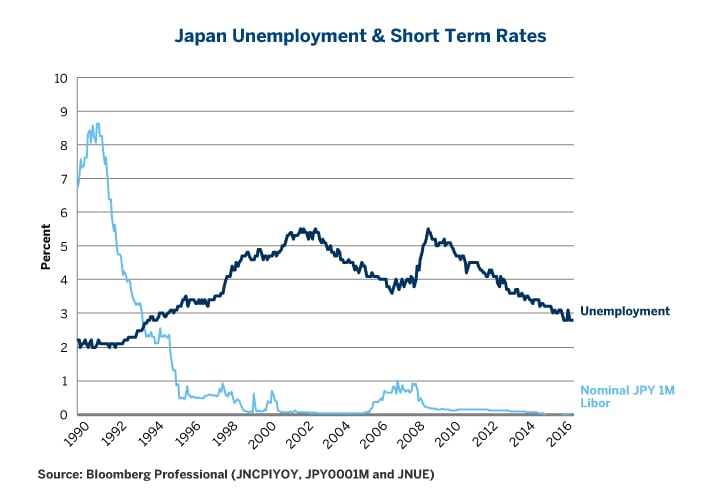

Japanese voters returned Prime Minister Shinzō Abe’s Liberal Democratic Party to power for a third term with over 60% of the seats in the lower house of parliament on Sunday October 22. The vote was an endorsement of Abe’s “three arrows” approach to reviving Japan’s economy though monetary policy, fiscal stimulus and structural reform. Over the past five years Abe’s policies have borne some fruit. Nominal GDP has had its first sustained period of growth since the mid-1990s (Figure 1) - its best performance since Japan’s financial crisis began in 1990; and unemployment rates have fallen to levels not seen since 1994 (Figure 2). Abe’s third mandate appears to be aimed more at constitutional reforms that will enable Japan, the world’s third largest economy, to rebuild its military and play a more active role in regional security matters, including standing up to China and North Korea. The nation appears set for economic-policy continuity, including continuing quantitative easing by the Bank of Japan (BoJ).

Figure 1: Nominal GDP Growth is Essential to Bringing Debt Under Control.

{kind=link}

Figure 2: Unemployment is at a 23-Year Low.

{kind=link}

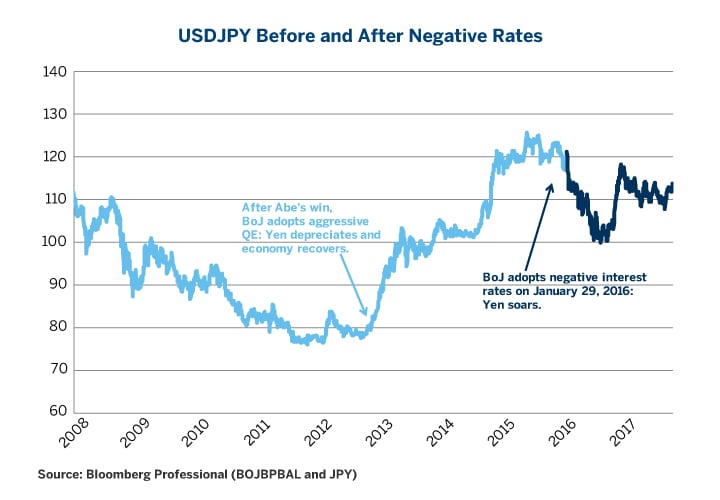

While Japan’s economy has improved since Abe assumed office, not everything has come up roses. For starters, Japan’s economy has slowed since early 2015 and the BoJ’s experiment with negative short-term interest rates does not appear to have been a success. If anything, the negative rates introduced in February 2016 serve as a tax on the banking system and might be slowing, rather than accelerating, economic growth. Moreover, instituting negative rates halted the depreciation of the yen in 2016 (Figure 3), which may have slowed economic progress by dampening export growth and delaying a return to positive rates of inflation. The currency weakened slightly after the election results became known on Sunday but it will take a sustained down trend to continue to boost Japan’s exports.

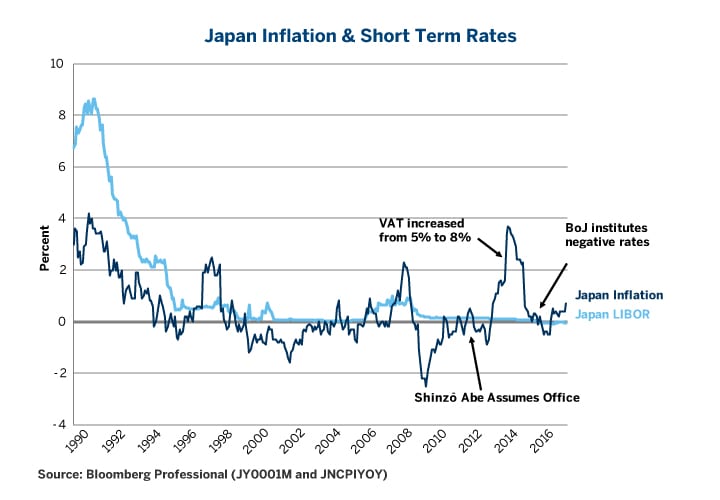

Negative rates not only stopped the decline in the yen, it halted Japan’s already faltering return to positive rates of inflation (Figure 4). Positive rates of inflation, along with solid real (inflation adjusted) economic growth, are critical for managing Japan’s massive public and private sector debt burdens.

Figure 3: USDJPY was Moving in the “Right” Direction Until Negative Rates.

{kind=link}

Figure 4: An Initial Post-2012 Abe Election Pop in Inflation Has Faded.

{kind=link}

Approximately half of the temporary 2013-2014 spike in inflation can be attributed to Abe’s increase in the value added tax (VAT) from 5% to 8%. This was policy was meant to offset the fiscal impact of supply-side reductions in income tax rates and to help close the size of Japan’s massive budget deficits. It proved to be politically unpopular and a second increase from 8% to 10% has been delayed, leaving the public sector still running deficits of 5.7% of GDP, albeit an improvement of the 8.7% deficit to GDP ratio that Abe inherited five years ago when he assumed office.

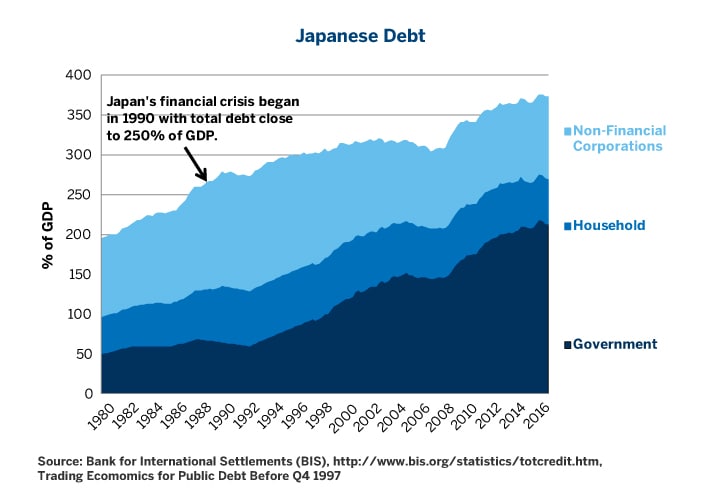

Despite the large budget deficits and the slowing in nominal GDP growth Japan has begun to stabilize its debt ratios. During the first four years of Abe’s administration, government debt-to-GDP ratio rose from 196% to 214%. Over the past year it has stabilized at 213% of GDP. Meanwhile, the household sector has de-levered slightly from 63% to 58% of GDP while corporate debt has remained near 100% of GDP (Figure 5).

Figure 5: Debt Ratios are Stable for the Moment but Still Vulnerable to External Shocks.

{kind=link}

Although it was not a major theme of the campaign, one key thing to watch for will be another attempt to hike the VAT from 8% to 10%. If the government was to go ahead with such an increase it would probably have the same impact as in the past:

- A boost to economic activity before the hike as consumers move purchases forward.

- A drop in consumer spending after the hike that lasts six months or so but then fades.

- A reduction in budget deficits of about 0.5% for over 1% rise in the VAT.

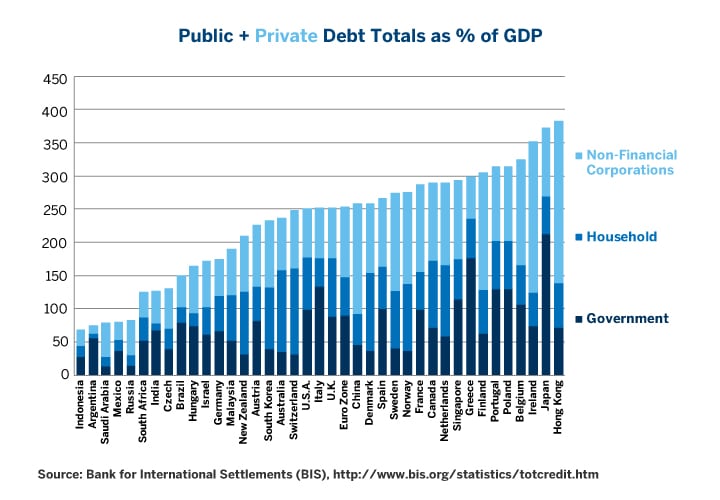

Even so, Japan’s debt levels remain excessive. They surpass their levels from 1990 when Japan’s financial crisis began, by over 100% of GDP. Moreover, they also exceed every other country in the world except for the region of Hong Kong (Figure 6). Finally, while stabilization of the debt ratio is good news, Japan has been here before. The levels stabilized from 1992 to 1994 and from 2000 to 2007. In both cases the debt levels rose again when exposed to external shocks (a rising yen in 1994-95, the Asian crisis in 1997-98 and the U.S. subprime crisis and European meltdown (2008-2012).

Figure 6: Only Hong Kong Surpasses Japan in Debt.

{kind=link}

The good news for Japan, at the moment, is that it benefits from a favorable international context with the first synchronized global growth since 2007. That said, China poses a major risk. 25% of Japan’s exports head to China or to Hong Kong and both places have run up massive debts. China also has a flat-to-inverted yield curve, which may signal a slowdown in 2018.

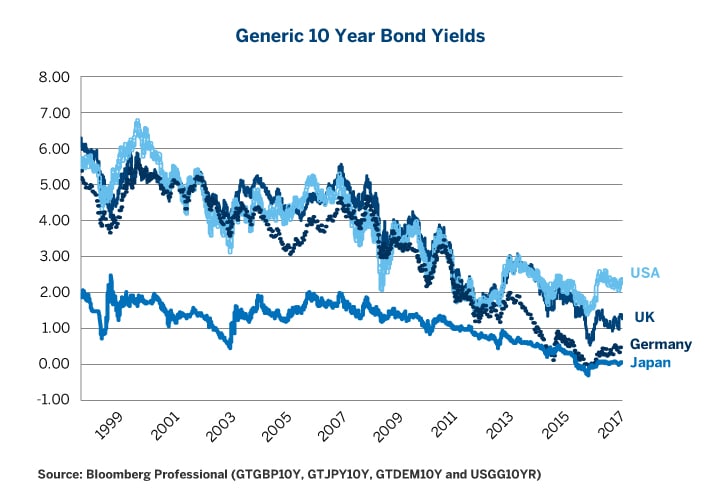

Japan’s high debt levels likely relegate the country to many more years of extremely low short-term interest rates even if the BoJ does eventually move to end its negative deposit-rate policy. This probably isn’t good news for holders of Japan’s long-term debt either. Currently the 10-year Japanese Government Bond (JGB) yields only about 6 basis points (bps), more than 230 bps below equivalent U.S. bonds and even below Germany and the U.K (Figure 7).

Figure 7: With 6 Bps Yields, How Will JGBs Benefit from a Flight-to-Quality?

{kind=link}

With little downward potential in rates and a flat yield curve, JGB holders are faced with little upside compared to bond holders in the U.S. where the risks are evenly balanced. As such, with little cost to being short JGBs, some hedge funds may be tempted to be short JGBs and long bonds elsewhere in the world. Additionally, some remaining domestic holders of JGBs might be tempted to search for higher yields abroad.

The campaign also largely sidestepped another burning issue: nuclear power. Following the Fukushima disaster in 2011, the Democratic Party government closed nearly all of the country’s nuclear power plants, which had been responsible for over 20% of electrical generation. This resulted in soaring imports of crude oil and natural gas at a time when prices of both were much higher than they are currently. Abe’s government has reversed course and has allowed for a progressive and partial return to nuclear energy. As such, his win should marginally reduce Japan’s demand for fossil fuels in the years to come which will be good for the country’s terms of trade but less positive for global oil and natural gas demand. Even so, the country remains a potential consumer of U.S. LNG exports.

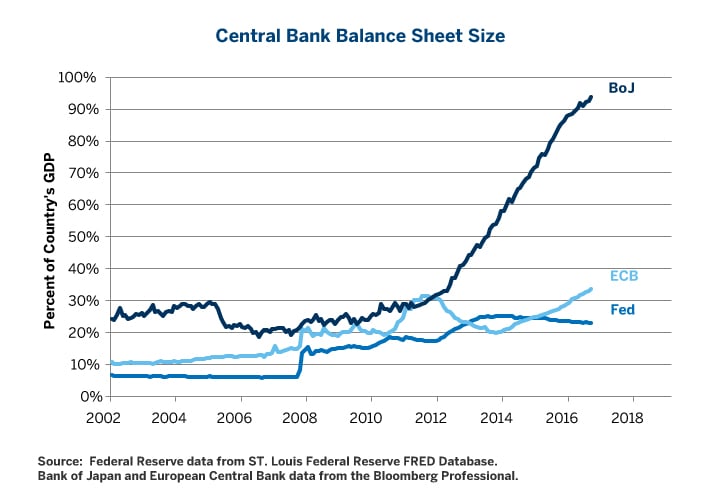

Finally, a closing note on monetary policy, even as the U.S. Federal Reserve (Fed) incrementally scales back its balance sheet and the European Central Bank (ECB) reduces its asset purchases; we expect aggressive BoJ economic support policies to continue. The BoJ will continue to anchor the 10-year JGB near a zero yield while regularly purchasing modest quantities of equity index Exchange Traded Funds to support the Japanese stock market directly. By end-2018, the BoJ’s balance sheet could hit 100% of nominal GDP. (Figure 8).

Figure 8. Bank of Japan’s Bloated Balance Sheet to Get Even Bigger.

{kind=link}

And, in an adjustment to previous policy, we expect the BoJ to pull back from negative rates on short-term deposits. Removal of negative rates, as discussed earlier, may work to weaken the yen, as will anchoring JGB’s near a zero yield, and policy comparisons with the Fed and ECB.

Bottom Line:

- Japan’s economy has improved significantly under Abe’s previous two terms.

- A VAT hike will boost increase pre-purchase activity but will temporarily slow the economy after the increase.

- Japan’s high debt levels will probably relegate the country to low short-term rates for many years to come, despite recently improved economic performance.

- If the BoJ puts deposit rates back to zero from negative levels, it might weaken the yen.

- The JGB has little upside and almost no carry rolldown, making it unattractive compared to bonds elsewhere in the world.

- A continued move back to nuclear energy should limit Japan’s budget deficit and soften demand growth for crude oil and natural gas while still leaving Japan an attractive market for LNG exports.

Wednesday Weekly FX Options on Futures

Weekly premium-quoted and volatility-quoted FX options on futures provide liquid, short-term expiration granularity that allows for more precise and capital-efficient FX risk management.

Available October 29: In Time for the FOMC Rate Announcement