{kind=link}

Taking the Pulse of Dr. Copper for 2019

Copper prices are often said to reflect the health of the global economy because of the metal’s use in every major facet of industry, hence the moniker “Dr. Copper.” Between January 2016 and the end of 2017, prices soared 72% as China’s pace of growth picked up and the rest of the world economy boomed. For 2018, however, copper prices had fallen 18% by late November amid concerns over trade wars, U.S. fiscal and monetary policy, Brexit, the Italian debt situation and a possible slowdown in China. Here’s a look at copper’s demand-and-supply conditions as we enter the last year of the decade.

China: Copper’s Most Important Source of Demand

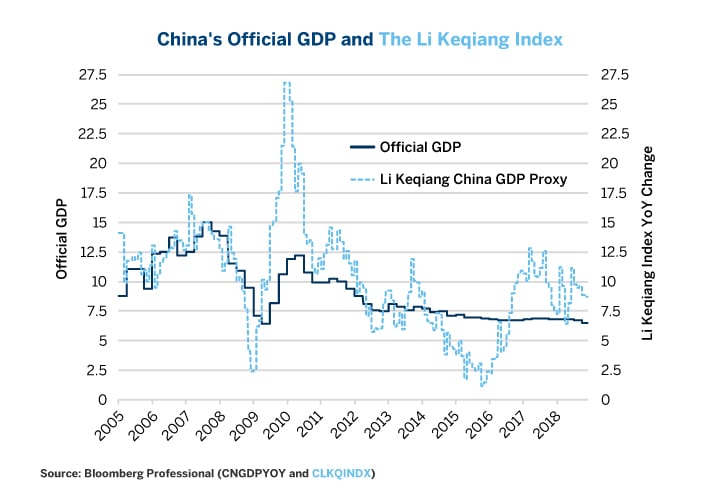

China consumes 40-50% of the world’s copper supply, making it by far the world’s dominant consumer. China’s economy did well in 2018: growing at 6.5%, according to official data, and even faster (around 9%) according to alternative measures of growth such as the Li Keqiang Index, which is based upon growth in electricity consumption, rail freight and bank loans (Figure 1). Even so, the strength of China’s current demand for copper is faced with concerns about the future. For starters, the trade dispute between the US and China might impact the Chinese economy, shaving a few tenths of one percent off the country’s growth going forward.

Figure 1: China’s Official Data Shows 6.5% Growth, But Other Measures Show Growth Closer to 9%.

{kind=link}

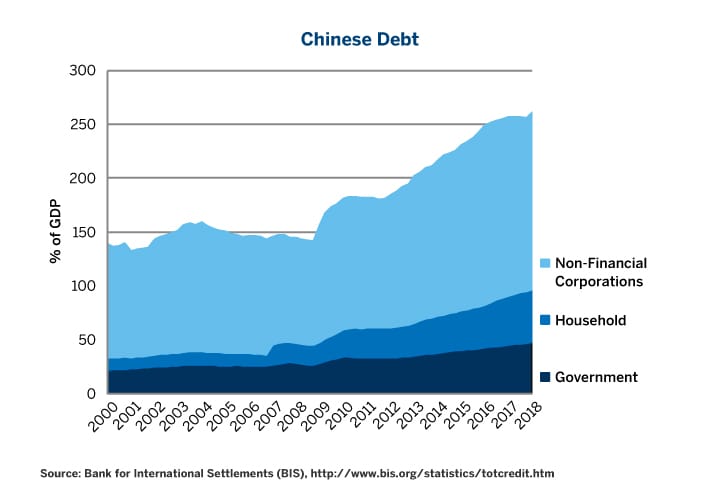

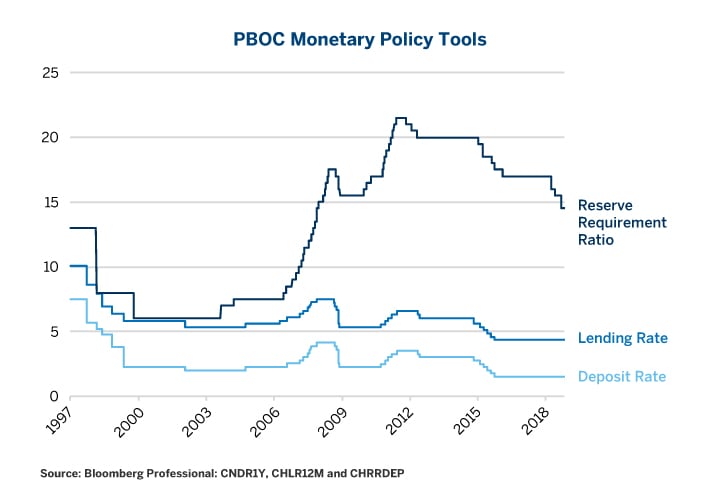

More importantly, China’s 2018 growth came largely from its continuing to lever-up the economy. Debt-to-GDP ratios, which stabilized in 2017, soared in Q1 2018 (Figure 2) and probably continued to rise through the year as the People’s Bank of China kept interest rates low and eased banks’ reserve requirement ratio (Figure 3). So long as China keeps monetary policy easy, a debt crisis is unlikely. Even so, as debt levels rise, monetary stimulus may become less effective as new borrowings will mainly serve to refinance the existing debt rather than support new investment and spending.

Figure 2: Chinese Debt Began Soaring Again in Q1 2018 and Tops European/U.S. Debt as a % of GDP.

{kind=link}

Figure 3: China May Not Experience a Debt Crisis Until After the Next Policy Tightening.

{kind=link}

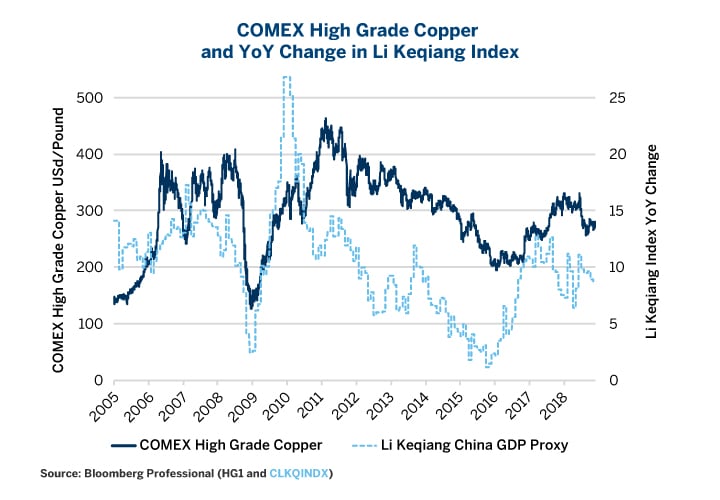

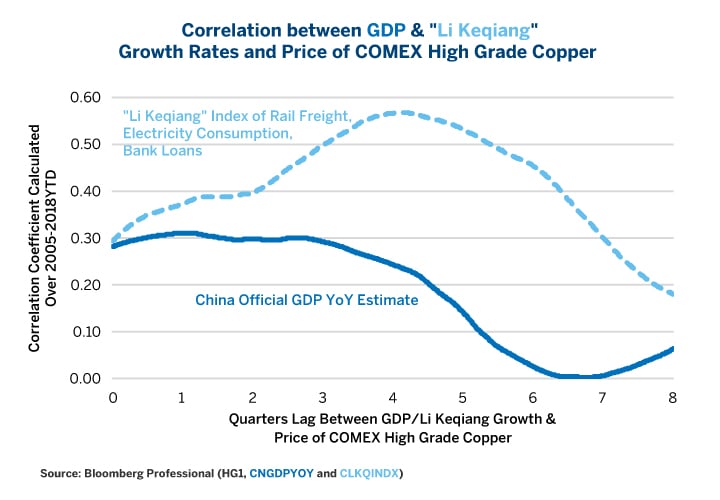

Copper prices correlate most closely with the Li Keqiang measure of GDP (Figures 4 and 5). So long as China’s growth remains strong, copper prices can probably remain near their current levels. But any signs of slowing in China, and copper prices would have a long way to fall. When China’s growth slowed dramatically between 2011 and 2015, copper prices fell from $4.50 per lb to as low as in the $1.90s. Copper’s average cost of production is probably around $1.90 per lb.

Figure 4: Changes in China’s Electricity Consumption, Rail Freight & Bank Loans Often Lead Copper Prices.

{kind=link}

Figure 5: Li Keqiang Shows a Strong Correlation with Copper Prices 3-5 Quarters in Advance.

{kind=link}

Mining Supply Continues to Rise

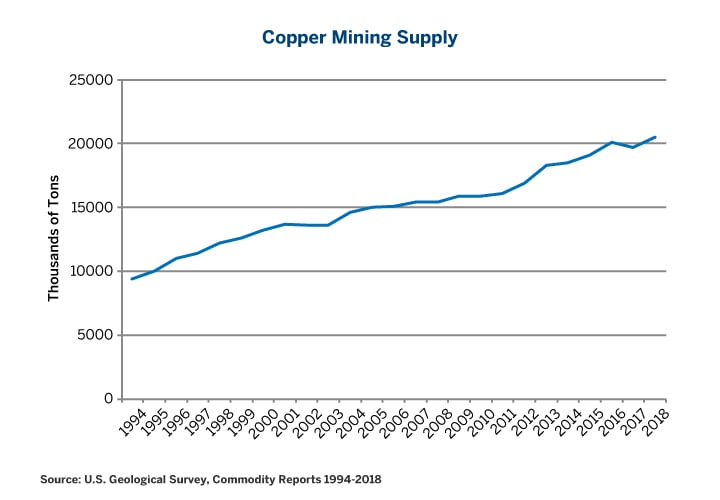

Mining supply of copper has more than doubled since 1994 (Figure 6), and with copper currently trading above its cost of production, supply probably continued to rise in 2018. Over the course of 2018, copper prices averaged around $2.90 per lb. This represents close to a 50% profit margin for the average copper mine. Even at the lowest price of the year, around $2.56 per lb, the average mine probably showed margins of around 34%. This should be enough to incentivize further production increases in 2019 and beyond. An increasing flow of copper emanating from the world’s mines makes copper especially sensitive to any slowdown in demand growth.

Figure 6: Copper Mining Supply Could Temper Prices if Demand Doesn’t Keep Pace.

{kind=link}

For copper, China is a particularly difficult source of demand to replace in the event of its slowdown. While India continues to grow at around 7-8%, its economy is only one-fifth the size of China’s. Meanwhile, the other BRICs (Brazil and Russia) are likely to struggle. The recent selloff in oil could be bad news for copper demand from Russia, Brazil and other oil producers. Additionally, Brazil’s incoming President has to deal with significant budget deficits and politically challenging pension reforms which could slow economic recovery.

Copper, the U.S. Dollar and Europe

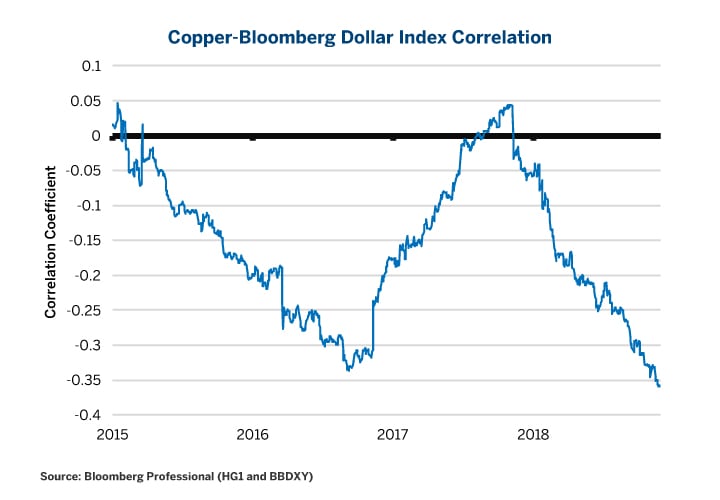

U.S. dollar (USD) strength was another reason why copper found itself under downward pressure in 2018 despite the strength in the U.S. economy. Copper typically has a negative correlation with USD (Figure 7). In 2018, USD strengthened as the Federal Reserve’s (Fed) rate hikes contributed to a sharp selloff in both developed and emerging market currencies.

Figure 7: Copper has Become Increasingly Negatively Correlated with US Dollar.

{kind=link}

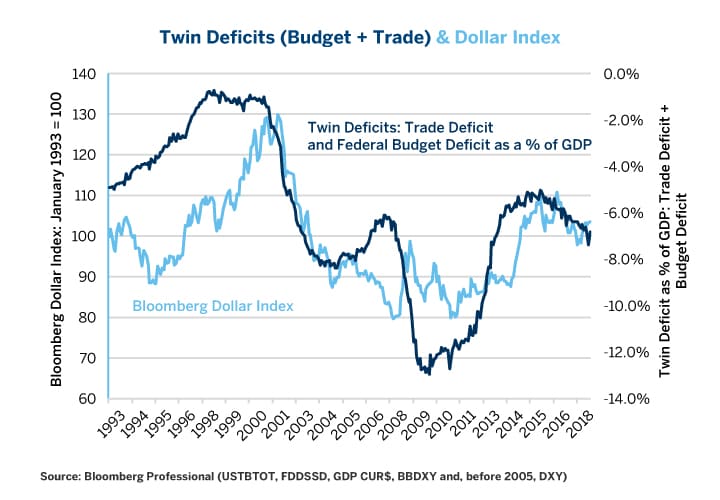

The dollar outlook for 2019 is more mixed. The Fed’s “dot plot” suggests that most members of the Federal Open Market Committee (FOMC) think that they will raise rates three or perhaps four more times next year. If the U.S. economy is sufficiently robust to support continued monetary tightening, USD might strengthen considerably to the probable detriment of copper prices. However, it is also possible, perhaps even likely, that the Fed will soon pause or significantly slow its tightening pace, depriving the dollar of the upward pull of rising short-term interest rates. Meanwhile, the U.S. budget deficit is growing, and this could weigh on the dollar (Figure 8) going forward. Any dollar weakness would most likely be bullish for copper prices.

Figure 8: Larger Deficits Often Weaken U.S. Dollar, To the Benefit of Commodity Prices.

{kind=link}

Investors should be particularly concerned about the possibility that the Fed could overtighten. If overtightening unintentionally produces an economic slowdown or recession, that could have unpredictable effects on copper. Weaker U.S. demand would be bearish, but a weaker USD could be bullish. We would guess that the overall impact of any severe U.S. slowdown would be negative for copper, at least in the short term, and that any benefits from the dollar’s weakness would be experienced later.

Lastly, Europe’s economy has been slowing in recent months, which isn’t particularly good news for copper. In late 2018 and early 2019, Europe will face two key tests that may influence copper prices: Brexit and the Italian debt situation. If Brexit turns out badly for the British pound (a no-deal exit), this could pull the euro down to the benefit of USD and to the likely detriment of copper. The same could happen if the Italian debt situation spirals out of control. The Italian debt situation is particularly worrisome given that the European Central Bank has bought European debt up to its legal limit and a second European debt crisis would be of much greater economic consequence than Brexit. So long as both situations reach an amicable resolution, which we think is likely, both the euro and pound could rebound, which would weigh on USD but might be positive for copper.

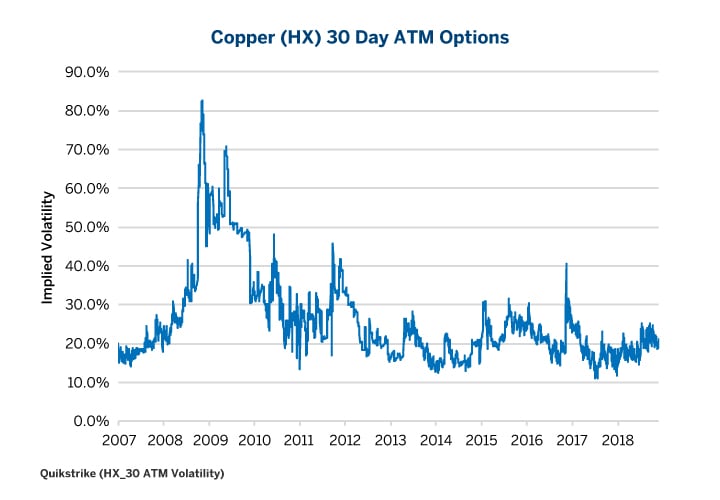

Copper options seem remarkably sanguine about the risks, with implied volatility trading much closer to record lows than record highs (Figure 9). 2019 could go either way – and indeed, the skew on copper options is about even at the moment— but the moves could be bigger than market participants anticipate.

Figure 9: Copper Options Implied Volatility is Relatively Low by Historical Standards.

{kind=link}

Bottom Line:

- Solid Chinese growth has prevented copper from falling further.

- China’s debt levels, however, should be a concern for copper traders.

- U.S. monetary tightening has been driving the dollar higher to the detriment of copper.

- Rising U.S. budget deficits could be bearish for the dollar and bullish for copper.

- Growth remains strong in India but not so for Russia or Brazil.

- Potential Fed overtightening could be a major risk for the U.S. economy and copper.

- Brexit and the Italian debt situation could also impact copper prices.

Copper 2019

How will copper prices trend in 2019? There are many factors to consider, including the pace of economic growth in top consumer China, the Fed's interest rate hikes next year and the strength of the U.S. dollar amid a widening budget deficit, among others. Hedge your portfolio with futures and options.