{kind=link}

Euro's Fate May Be In Italy's Hand

Euro’s Fate May Be in Italy’s Hands

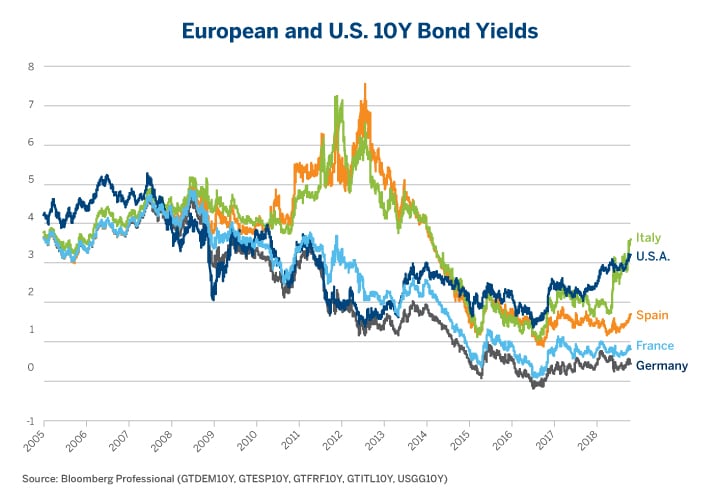

While the trials and tribulations of Brexit grab the headlines, the collapse in the Italian bond market may be of far greater consequence to the future of Europe than Britain’s departure from the European Union. The most recent selloff, which began in May, isn’t the first time that Italian debt has hit the skids. It’s last major price decline, between 2009 and 2012, sent yields soaring (Figure 1) and threatened to take the Eurozone down with it. What is remarkable is how little currency options appear to be responding to the potential threat on the horizon.

Figure 1: Italian Yields Are at a 4 ½-Year High and Far Above Most Other Eurozone Countries.

{kind=link}

In the summer of 2012, newly installed European Central Bank (ECB) President Mario Draghi promised to “do whatever it takes” to prevent Italy, Spain, Portugal and Ireland from defaulting on their debt. The market took him at his word. Over the next few years, yield spreads between Italy and Spain narrowed versus the core countries (Germany, France and Holland) as the ECB cut rates to zero and began a quantitative easing program that eventually bought almost one third of the outstanding debt of each Eurozone country (except Greece). The ECB’s ultra-loose monetary policy offset a persistent fiscal tightening across the Eurozone (Figure 2) and helped to produce a belated recovery from the Europe’s 2008-2012 double-dip recession.

This seemingly happy state of affairs wasn’t joyful for everyone. While Italian bond yields fell and fiscal deficits shrank, the Italian economy stagnated and unemployment persisted at high levels. Moreover, Italy’s public-sector debt remains at 134% of GDP, far higher than most of its eurozone peers. The fact that Italy has relatively low private sector debt doesn’t appear to reassure investors. In any case, voters lost patience and in March voted heavily in favor of the leftist (Five Star) and right-leaning (Northern League) populist movements. In May, they entered into a coalition government that almost immediately upset markets by threatening to increase welfare spending and cut taxes simultaneously.

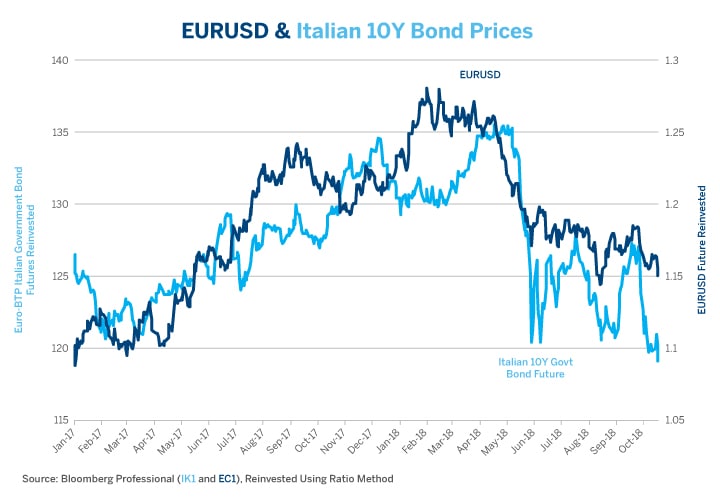

Since the election in March, the euro-U.S. dollar (EURUSD) exchange rate has been moving increasingly in lockstep with Italian government bond futures (and inversely with yields) (Figure 2). As such, the future direction of EURUSD might depend to a large extent on the fate of Italy’s debt market. If Italy’s coalition government persists in its fiscal loosening and investors continue to balk at financing widening deficits, EURUSD may be susceptible to a much deeper decline. If the government abandons plans for tax cuts and spending increases, Italian debt and the euro might rebound.

Figure 2: The Italian Government May Hold the Euro’s Fate in Its Hands.

{kind=link}

This Time It’s Different (and Not in a Good Way)

The last time that Italy found itself in financial trouble, it found a savior in one of its very own, Mario Draghi. This time, with the ECB near its limit in terms of what it can buy and Draghi on his way out, it’s not so clear who will rescue Italy if its debt market fails to rebound. In 2012, the ECB had ample room to buy sovereign debt from every issuer in Europe. Over the next several years, ECB bought €1.8 trillion of public debt, including €341 billion of Italian bonds. The ECB cannot purchase more than a third of the outstanding debt of any public issuer and must purchase the debt of all countries roughly in proportion to the size of their respective economies. The ECB is currently near that limit. This is among the reasons why the ECB has downshifted its buying program from €60-80 billion per month from 2015-2017 to €30 billion per month for the first nine months of 2018. It plans to buy only €15 billion per month in Q4 2018. As such, if investors lose confidence in Italian debt on the scale of the period from 2009-12, it’s not obvious that the ECB could or would bail Italy out a second time.

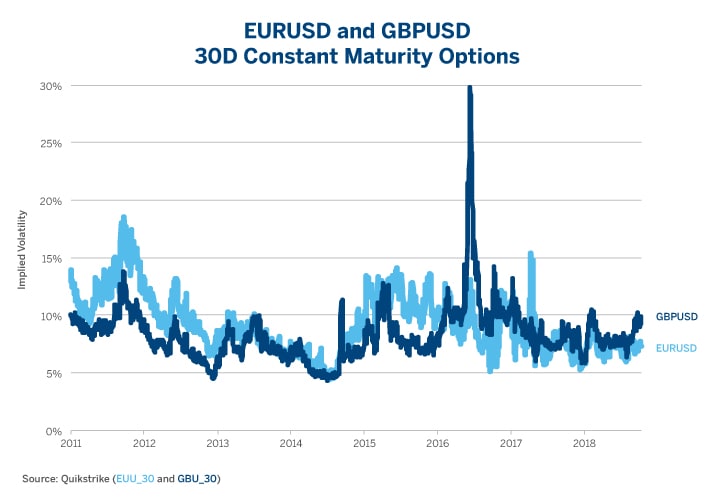

What is clear is that any further tensions in the Italian debt market will most likely be negative for the euro. That said, it’s remarkable how unconcerned the EURUSD option market appears to be. EURUSD options have rarely been much cheaper than they are today. British pound (GBPUSD) options have become slightly more expensive in response to the most recent breakdown in Brexit talks but EURUSD options have barely budged in response to Italy (Figure 3). Perhaps options traders are right to be nonchalant about Italy’s rising bond yields. Maybe Italy will get its house in order or perhaps investors will get on board with supporting a looser Italian fiscal policy. That said, conditions may be ripening for a spike in EURUSD volatility.

Figure 3: Yawn. EURUSD Options Traders Largely Unmoved by the Selloff in Italy’s Debt Market.

{kind=link}

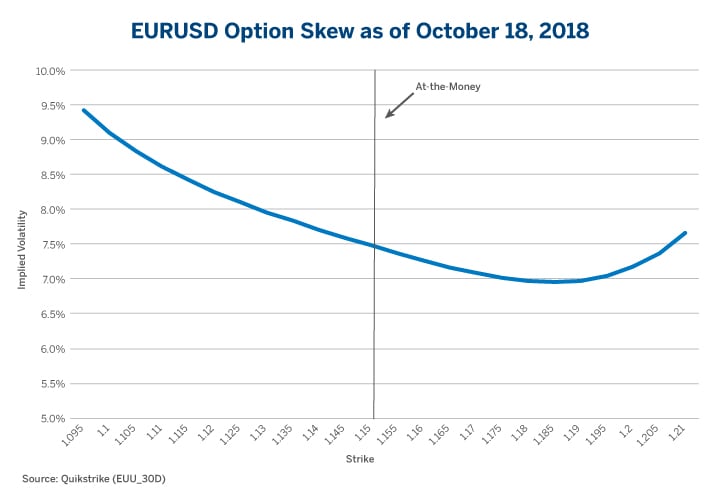

While the overall level of options volatility is low, the skewness of the EURUSD options implied volatility curve reveals the direction of investors’ worries. Not too many are worried about a sudden rise in EURUSD. Out-of-the-money call options are actually cheaper than at-the-money options until one gets to strikes 3% or more above the current market price. By contrast, put options become steadily more expensive (Figure 4). This suggest that options traders are, to some extent, bracing for EURUSD’s downside.

Figure 4: EURUSD Risks Skewed to the Downside, According to Options.

{kind=link}

Bottom Line

- EURUSD options remain historically cheap in the face of elevated political and market risks.

- Italian government debt markets are increasingly driving swings in the exchange rate.

- EURUSD puts are generally more expensive than calls, indicating that options traders fear downside more than upside for the euro.

- The ECB may no longer be in a position to help Italy if debt markets continue to sell off.

Hedging the Euro

The euro's value against the U.S. dollar has been increasingly moving in lockstep with Italy's bond futures (inversely with yields) since the election of a new government in Italy last March. But the coalition government has plans to cut taxes and increase spending, which could widen the deficit and impact the euro. Protect your investment portfolio with FX futures and options.