{kind=link}

Natural Gas: Is Rally Over or Taking a Breather?

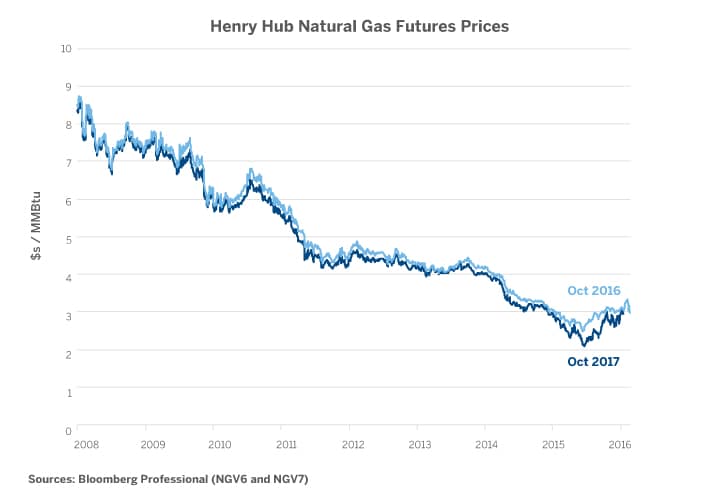

In the wake of a seven-year bear market in natural gas, we began publishing a series of reports in October 2015 warning that there was a preponderance of risk to prices rising: demand growth was steady, especially where electrical power generation was concerned, and there has been no growth in North American supply since the end of 2014. So far, Henry Hub natural gas price action has largely borne out these observations, with prices rallying from below $2 per MMBtu to around $3 (Figure 1). But prices have fallen back over the past few weeks. Is this a signal that the rally is over, or is it just a hiccup? We suspect it’s the latter for a variety of reasons.

An Unusually Warm Fall Does Not Necessarily Mean an Unusually Warm Winter

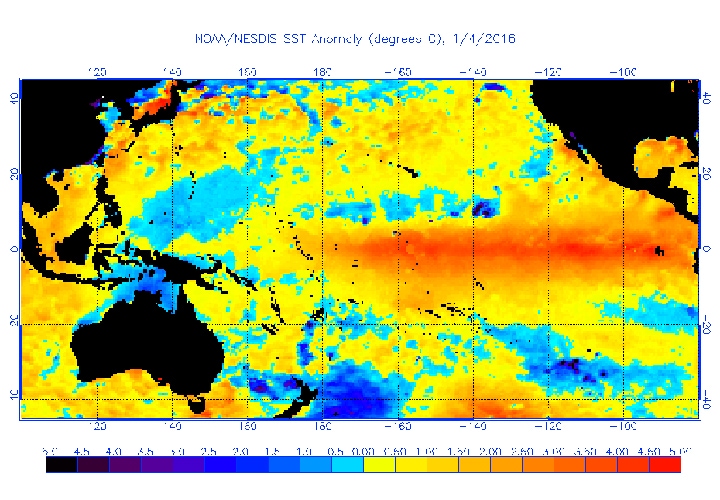

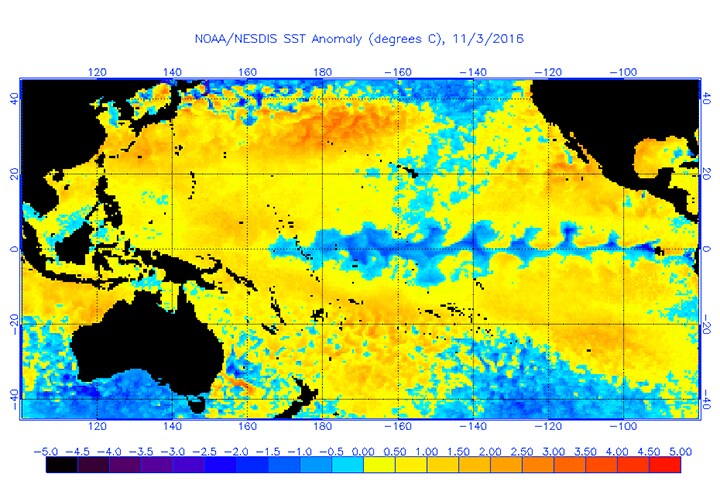

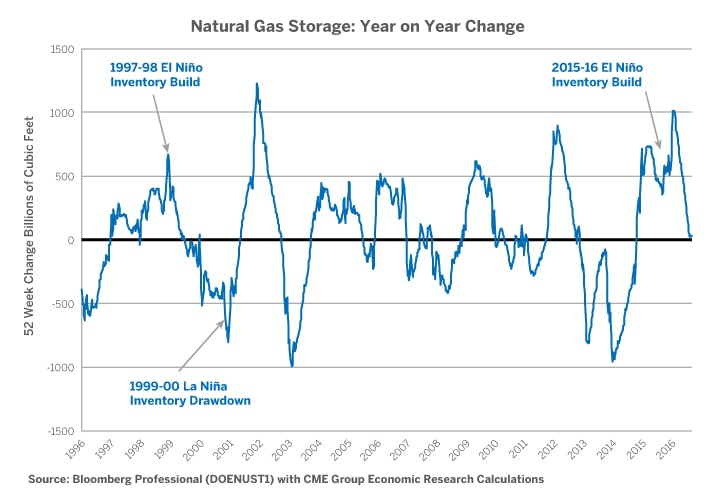

Natural gas prices have waned a bit after rebounding from March 2016 lows. This appears to be the result of an unusually warm start to fall in North America that has depressed electrical power and heating demand. Be warned: a warmer-than-usual fall does not necessarily mean a mild winter. Concern that January and February might be colder-than-usual in North America largely stems from the fact that we have gone from a strong El Niño earlier this year (Figure 2) to a mild La Niña (Figure 3).

Figure 1: A Rebound After a Big (and Long) Bear Market.

{kind=link}

Figure 2: January 4, 2016: Last Winter’s Strong El Niño Depressed Natural Gas Demand.

{kind=link}

Figure 3: November 2016: Waters off California are Still Warmer-Than-Usual but a La Niña is Forming.

{kind=link}

La Niña is, however, not the only concern. While North America has enjoyed a much warmer-than-normal fall so far, the opposite is true for Siberia, which has been much colder and snowier than usual. This could herald a brutal blast of Artic cold, and a strong and highly volatile polar vortex this winter. If January and February in North America turn out to be colder-than-normal as a result of La Niña and the early buildup of snow and cold air over Siberia, natural gas prices could soar as more fundamental factors like supply and long-term demand reassert themselves.

Supply: No Growth, at Least not for the Moment

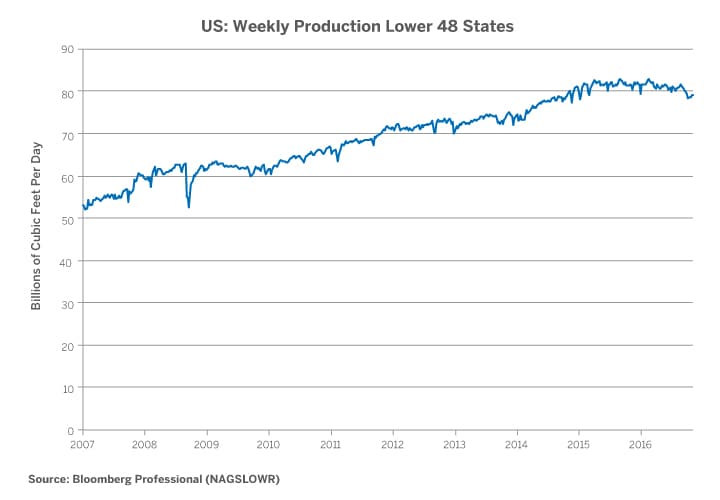

The single biggest upside risk to natural gas prices is the lack of supply growth. Supplies from the lower 48 states peaked in early 2015 and have since fallen by 3-4% (Figure 4). Such a drop might not sound like much but the inelastic nature of natural gas supply and demand means that small fluctuations in availability and end-use can give way to large percentage moves in prices.

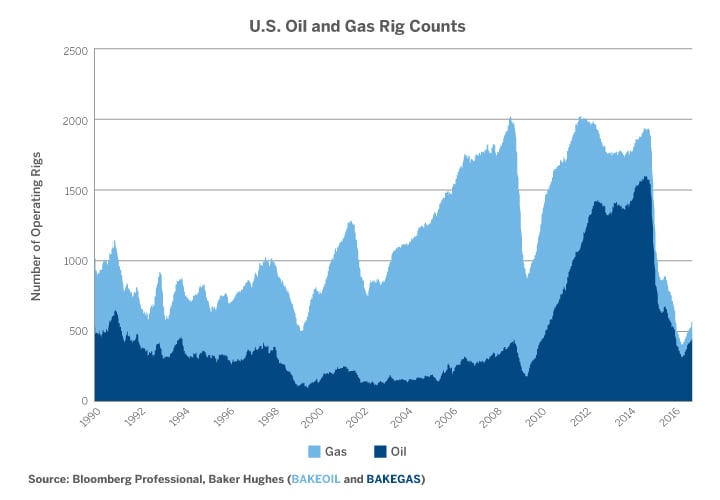

The news about U.S. supply is not all bullish for natural gas prices. Since we last wrote about natural gas in August, there has been a rebound in both oil and gas drilling, incentivized by the bounce in crude oil and natural gas prices. The number of gas rigs has risen from 81 on August 26, 2016, to 117 by early November this year, while the number of oil rigs increased from 406 to 450 over the same period. However, investment in the sector still remains depressed (Figure 5). That said, increased investment could eventually improve supply and limit the extent to which natural gas prices might rise. Finally, we would be remiss not to point out that the rig-count numbers do not take into account productivity. A small number of highly productive rigs could add more to production than one might imagine.

Figure 4: Production of Natural Gas Has Begun to Stagnate, Even Declining Slightly.

{kind=link}

Figure 5: Rig Counts are Rebounding But Investment Remains Depressed.

{kind=link}

Demand: Still Positioned For Growth

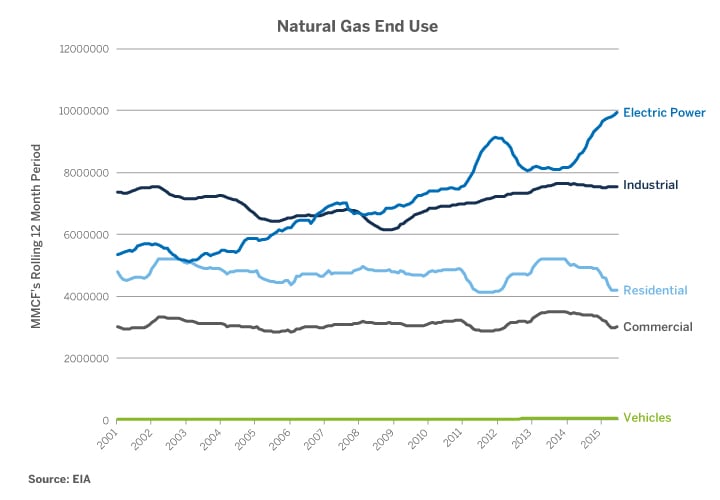

On the demand side of the equation, electrical power generation from natural gas continues to rise. Residential and commercial use dipped over the unusually mild 2015-16 winter but will probably recover later this year, especially if the coming winter turns out to be harsh (Figure 6).

Figure 6: Electrical Power Generation from Natural Gas Continues to Rise.

{kind=link}

Electrical power demand is likely to continue rising for two reasons:

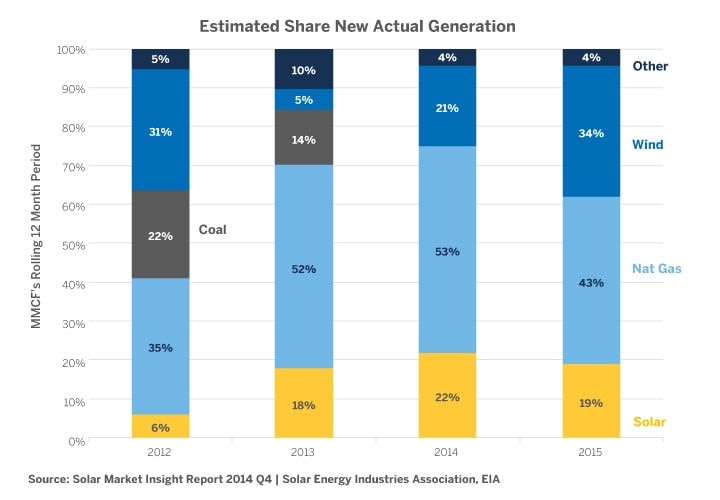

- There has been no new coal power generation facility brought on line since 2013, leaving natural gas, wind and solar as the primary replacements (Figure 7).

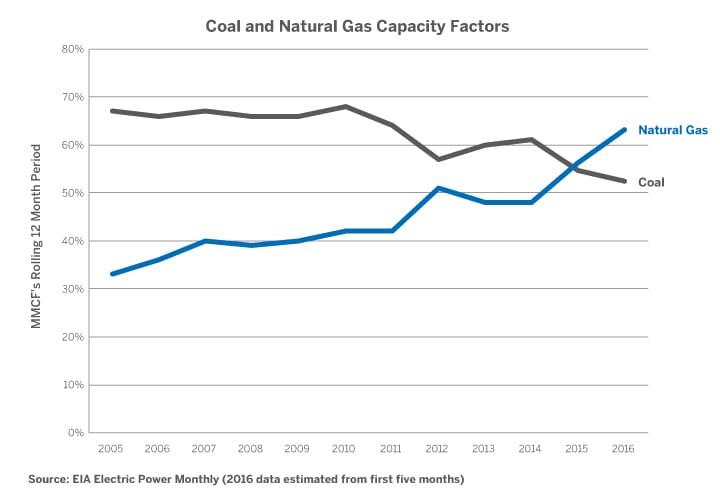

- Natural gas capacity factors have been increasing while coal capacity factors have been declining. Essentially this means that natural gas power plants are operating more of the time than coal power plants for the first time (Figure 8).

Basically, not only is natural gas increasing its share of the generating capacity, a greater share of the natural gas generating capacity is actually in use at any given time.

Figure 7: Natural Gas has Displaced Coal to be the Largest Share of New Generating Capacity.

{kind=link}

Figure 8: Natural Gas Power Plants Now Operate at Higher Capacity than Coal.

{kind=link}

Export Demand:

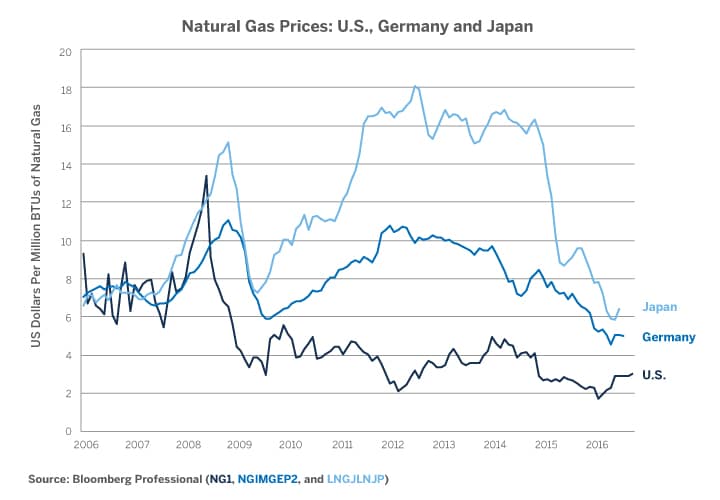

While domestic demand for natural gas has been robust, mainly thanks to electrical power generation, export demand is not likely to be of much help. Exports to Canada and Mexico could remain robust but hopes for a significant price boost from LNG exports have largely been dashed by the global convergence of prices, and Asian and European prices falling back towards the U.S. price (Figure 9).

Figure 9: Natural Gas Spreads Have Collapsed.

{kind=link}

Storage Levels Are Going To Be Less Of A Buffer

Despite rising electrical power demand, storage levels have soared over the past few years as supply outpaced demand. El Niño played a large role in the storage boom, but the good news for natural gas bulls is that inventories have apparently peaked and appear set to come down. Bulls should be warned, however, that the stored supply remains extremely large by historical standards and could limit potential upside until they come down substantially. An unusually cold winter could, however, reduce storage levels significantly, as was the case in 1999 and 2000.

Figure 10: Storage Levels Continue to Rise but at a Diminishing Pace.

{kind=link}

Bottom line

- An unusually warm start to the fall has interrupted the natural gas bull market, but an unusually cold winter could kick it back into gear.

- La Niña and heavy snowfalls in Siberia could trigger an Arctic blast in January and February.

- Supply continues to stagnate but investment is picking up again, and rigs are coming back on line.

- Electrical power demand appears set for further growth given the lack of alternatives to natural gas.

- Natural gas storage levels are record large and could limit upside moves, but storage levels are probably close to peaking and once they begin to decline could help sustain buying interest in natural gas markets.

- Once a natural gas bull market gets going, the potential price upside could be substantial. In the early part of the last decade, prices spiked to as high as $10 per MMBtu. That said, natural gas storage costs impose a significant negative carry for those who are structurally long.