{kind=link}

Equities: Are TOPIX and Nikkei Still Cheap?

Three months ago, we discussed the impact of Abenomics on Japan’s economy. Japan’s economy, generally speaking, has been doing well. While there is plenty to quibble about, since Prime Minister Shinzō Abe assumed power in late 2012 Japan has had its best sustained growth since the 1980s. Unemployment fell to its lowest level since the early 1990s and inflation turned slightly positive. Not everything is coming up roses: the government still runs a substantial deficit although its smaller than before, and while debt levels remain colossal, they have stabilized.

Not surprisingly, Japan’s two main equity indices, the TOPIX and the Nikkei, turned in a stellar performance. Since Abe took office in late 2012, the TOPIX returned 180% while the Nikkei returned 195%. By way of comparison, the S&P 500® returned 110% over the same period of time.

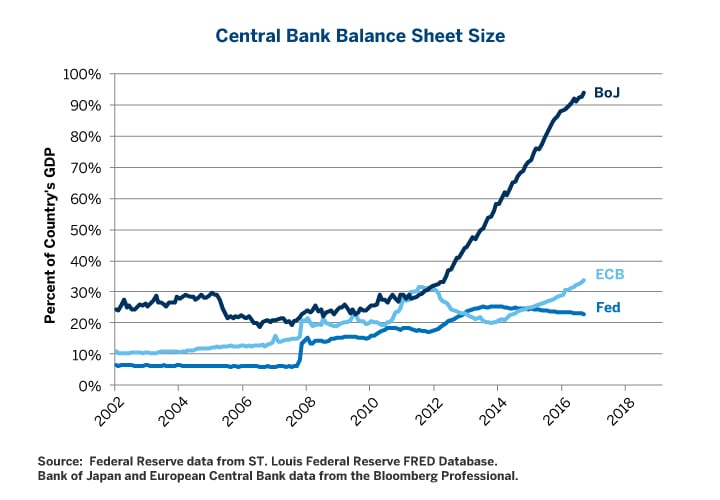

Part of what boosted Japanese stocks to even greater returns than their American counterparts, is aggressive quantitative easing (QE) by the Bank of Japan (BoJ). Not only does the BoJ’s QE program dwarf that of the U.S. Federal Reserve (Fed) and the European Central Bank (ECB), (Figure 1), it also involves buying over $50 billion of Japanese stocks via exchange traded funds (ETFs) each year. This differs substantially from the ECB and the Fed whose buying programs stuck purely to fixed income products.

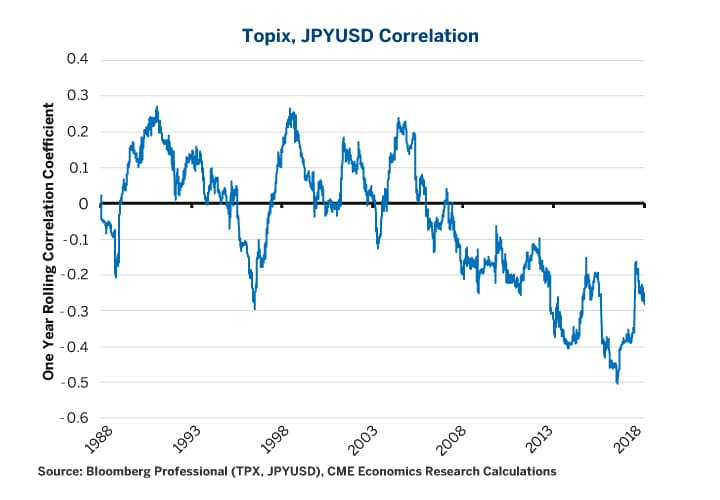

In addition to bidding up the equity market directly, the BoJ’s QE program also boosted the equity market indirectly by weakening the Japanese currency. Since Abe came to power, the yen has fallen 30% versus the U.S. dollar (JPYUSD), 25% versus the euro and 28% versus the renminbi. Not only has this helped to halt deflation and revive economic growth, it also made Japanese firms more competitive and increased the value of their foreign earnings and assets from a yen perspective. JPYUSD demonstrated a negative correlation with TOPIX for the past five years – Abe’s entire time in office. (Figure 2).

Figure 1: The BoJ’s QE Programs Dwarf the Fed and ECB’s as a % of GDP

{kind=link}

Figure 2: Correlation Between the TOPIX and Yen Has Been Negative Since the Crisis.

{kind=link}

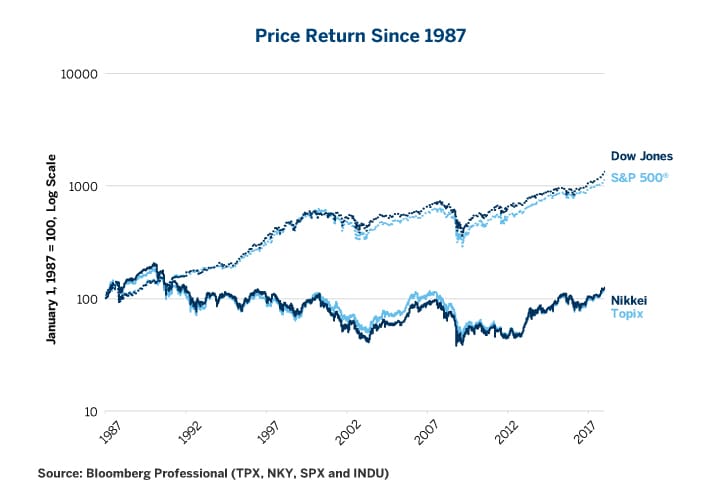

Despite their recent outperformance, it’s hard to argue that the TOPIX and Nikkei are overvalued. While they outperformed their U.S. counterparts during the past several years, they massively underperformed over the past few decades (Figure 3). This has taken Japanese stocks from a state of chronic overvaluation during the 1980s and 1990s to being relatively inexpensive today.

Figure 3: Three Decades of Underperformance Took Care of Japan’s Overvaluation Problem.

{kind=link}

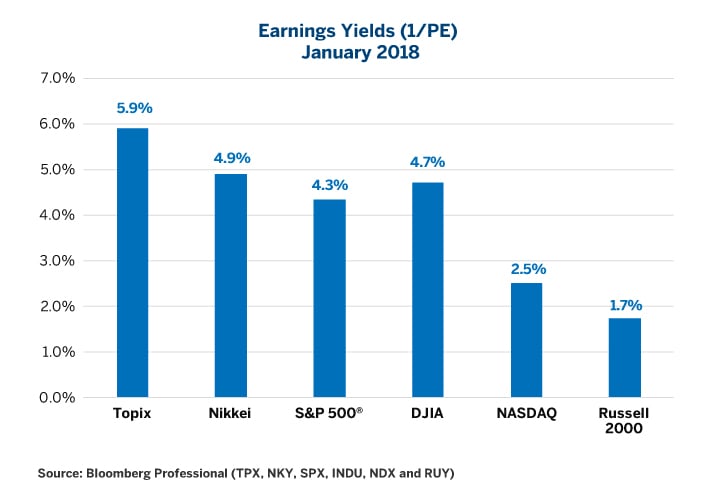

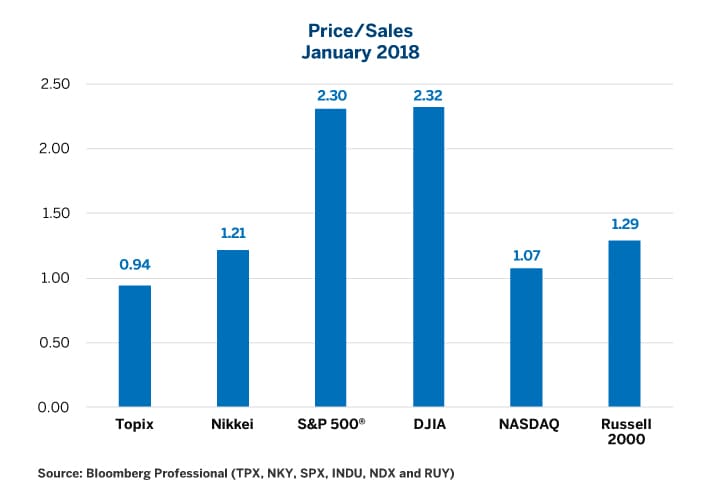

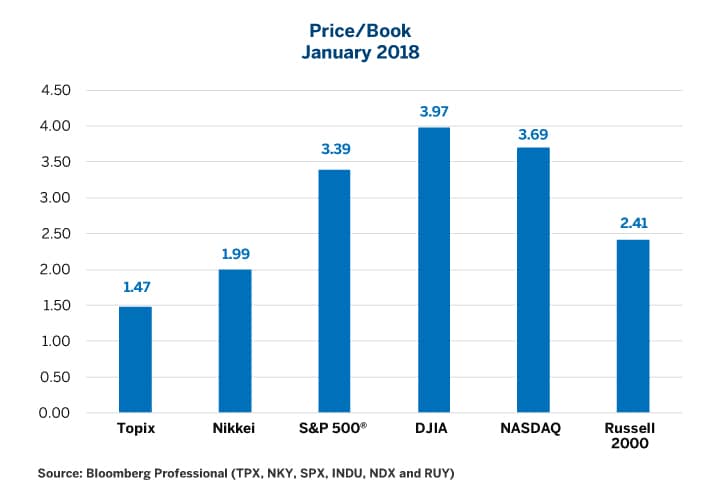

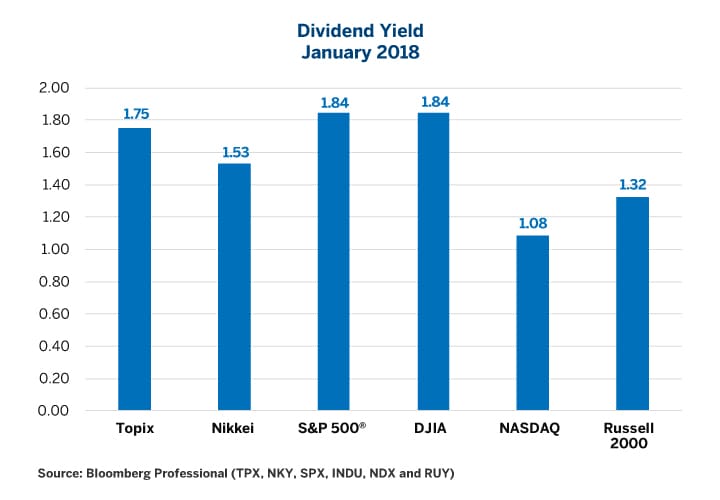

By almost every measure Japanese stocks are less expensive than their U.S. counterparts. The TOPIX and Nikkei have higher earnings yields (the reciprocal of the price/earnings ratio) than the S&P 500® and the Dow Jones Industrial Average (Figure 4). They also trade at much lower multiples to sales (Figure 5) and book values (Figure 6). Only the dividend yield makes them look more expensive than U.S. stocks and, even then, not by much (Figure 7).

Figure 4: Japanese Stocks Sport Higher Earnings Yields (Lower P/E) Than U.S. Stocks.

{kind=link}

Figure 5: Japanese Stocks Also Have Much Lower Price to Sales (Revenue) Ratios.

{kind=link}

Figure 6: Japanese Stocks Also Trade at Lower Price-to-Book Ratios.

{kind=link}

Figure 7: Only by Dividend Yield do Japanese Stocks Appear More Expensive Than U.S. Stocks.

{kind=link}

That said, comparing equity valuation across borders can be tricky for two reasons: sector make-up differences and interest rate differentials. For starters, the equity sector make-up differs a great deal between the Japanese and the U.S. indices (Table 1). TOPIX attaches much higher weightings to industrial, consumer discretionary and telecom stocks than the S&P 500 does. By contrast, the S&P 500 has much greater concentration in information technology (IT) stocks and health care. The greater concentration in the fast-growing tech and health care sectors explains in large part why the S&P 500® commands higher earnings, sales and book-to-price multiples.

Table 1: Industry Weights

| Sector | Topix | Nikkei | S&P 500 | Dow Jones |

| Industrials | 22.8% | 22.9% | 10.3% | 23.6% |

| Cons. Disc. | 19.5% | 19.7% | 12.3% | 14.7% |

| Financials | 12.4% | 2.9% | 14.6% | 16.1% |

| IT | 12.3% | 17.3% | 24.2% | 17.2% |

| Cons. Staples | 8.5% | 9.2% | 8.0% | 6.5% |

| Materials | 7.6% | 8.3% | 3.0% | 2.1% |

| Health Care | 6.6% | 9.5% | 13.8% | 12.5% |

| Telecom | 4.6% | 7.2% | 2.0% | 1.4% |

| Real Estate | 3.0% | 2.3% | 2.8% | 0.0% |

| Utilities | 1.5% | 0.2% | 2.8% | 0,0% |

| Energy | 1.1% | 0.5% | 6.2% | 5.9% |

Source: Bloomberg Professional IMAP (TPX, NKY, SPX, INDU)

Lastly, there is the question of interest rates. In theory, Japanese stocks should trade at much higher multiples than U.S. stocks, given that long-term (30Y) yields in Japan are 0.85%, less than one third the level of U.S. 30Y yields (nearly 3%). That said, QE distorted fixed income markets beyond recognition on both sides of the Pacific, making it difficult to know what sort of rate to use when discounting future earnings for investors worldwide. What is clear in Japan is that if there is a bubble, it’s probably in government bonds and not in Japanese stocks.

To the extent that the market-cap weighted TOPIX index and the price-weighted Nikkei index don’t track each other perfectly, different industry weights explain those discrepancies, especially the very different allocation to financial shares. The Nikkei and the TOPIX have a very high correlation. Usually > 0.95.

The BoJ’s exit strategy from QE (if there is one) poses downside risks to Japanese stocks. Can Japanese stocks continue to rally as the central bank curtails its purchases of equities? Another big downside risk to Japanese stocks and economic growth would be a sudden, sharp rise in the value of the yen versus the Renminbi, the dollar and the euro. A slowdown in China, which is a possibility given their debt levels and flat yield curve, could also hamper Japan’s growth, especially if China were to devalue its currency. Lastly, a global correction in equity values could also cause Japanese stocks to suffer and it’s not clear how the BoJ could ease policy further in the event of a global downturn given that they already have an enormous balance sheet and short-term interest rates below zero.

That said, there are upside risks for Japanese stocks too. As we have pointed out in our other research, the U.S. is unlikely to fall into a recession in 2018 and 2019, which is good news for Japan. Equity markets may also continue head higher globally, given the lack of other obvious investment alternative for institutional investors given the low level of bond yields around the developed world.

Bottom line

- Japan’s stocks benefitted both directly and indirectly from QE.

- Curtailing QE poses significant risk for Japanese equities, especially if its accompanied by a rally in the yen

- A possible slowdown in China also poses risks for Japanese equities.

- Japanese stocks don’t look expensive versus their American counterparts by most measures

- Significant differences in industry composition make the comparison to U.S. equities difficult.

Recommended For You

TOPIX Futures

Raise your exposure to Japanese stocks through CME Group's TOPIX Futures, which will be launched on Feb 5, 2018.