Adjusted Interest Rate (AIR) Total Return futures ‒ product overview

{kind=link}

CME Group’s Equity Index futures offer several products designed for better risk management and improved capital efficiency, when trading total return exposures on global equity benchmarks. Adjusted Interest Rate (AIR) Total Return futures are now added to that list.

AIR Total Return futures are designed to provide total return exposure with an overnight floating rate built in – more closely replicating the economics of an equity index swap.

As a futures contract, not a bilateral negotiated OTC total return swap, AIR Total Return futures are traded and cleared at CME ‒ providing the standardization, efficiency, and security of listed, centrally-cleared futures contracts.

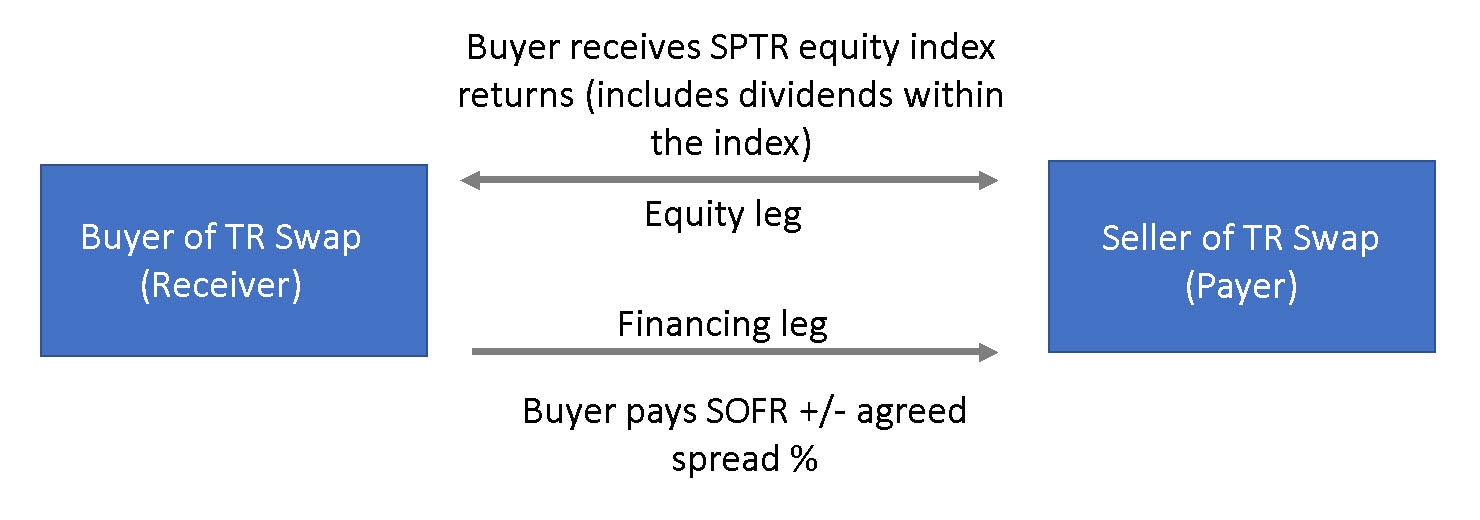

Equity index swaps

As a refresher, in an equity index swap, one counterparty agrees to periodically pay the other party index performance in exchange for an agreed upon financing payment.

{kind=link}

The financing payment for the period is based upon the swap’s notional value and an agreed to reference rate that aligns to the period length, plus or minus an agreed to swap spread. The counterparty that is long the equity performance, known as the receiver, will also receive any dividend income from the counterparty who is short the index performance, known as the payer.

In exchange for receiving the equity index performance, the receiver will make financing payments to the payer to compensate the payer for the financing costs associated with funding the underlying equity index position. If the underlying index is a total return index, this means the dividends are reinvested in the underlying index as part of the index methodology and an explicit adjustment for dividends need not be made.

AIR Total Return futures

Let’s now look at AIR Total Return futures on the S&P 500, which are comprised of three components:

- The S&P Total Return Index performance

- The daily accrued financing

- The financing spread adjustment

The Equity Index component is based on the S&P 500 Total Return Index (SPTR Index). The index levels are calculated by Standard & Poor’s. The second component, accrued financing, is calculated daily based upon the benchmark Effective Federal Funds Rate (EFFR). The ongoing accumulation of financing is incorporated into the daily settlement of the product.

The final component of AIR Total Return futures is the financing spread adjustment. When trading an AIR Total Return futures contract, the counterparties will agree to a trade price in terms of an annualized spread plus or minus to the reference rate. This is known as the Total Return Futures (TRF) Spread.

The financing spread adjustment in index point terms will be determined by multiplying that day’s closing index value by the traded TRF Spread, multiplied by the time to maturity expressed in actual days over 360.

How to trade AIR Total Return futures

AIR Total Return futures are only tradeable through the Basis Trade at Index Close (BTIC) mechanism on Globex or via a BTIC block trade.

The BTIC trade price of the contracts will represent the TRF Spread and is quoted in basis points. It is important to note that unlike other BTIC contracts, the AIR Total Return futures spread is quoted and traded in basis points, not index points.

For example, when a buyer and seller of an AIR Total Return futures contract agree to a BTIC price of twenty, that equates to a TRF spread of 20 basis points. That is the traded price of the BTIC transaction. Once the TRF spread is consummated via the BTIC transaction, it will be converted into an AIR Total Return futures price by the exchange at the end of the day ‒ once the index close price is established. The resultant cleared price of the AIR Total Return futures contract is computational and occurs on a trade-by-trade basis.

The AIR Total Return futures contract notional value is determined by the contract’s fixed multiplier, $25.00, times the futures settlement value. For example, the daily change in the futures index value, expressed in index points, times $25.00 would determine the change in profit or loss per contract.

As with most Equity Index products, AIR Total Return futures are a financially-settled product and are block eligible. Final settlement of a contract will be the third Friday of the contract month. The final settlement value is determined by Special Opening Quotation (SOQ).

Because AIR TRFs can only be executed via BTIC, the last trading day is the business day preceding the third Friday of a contract month. Contracts will be listed for 13 quarterly contracts, plus four additional December annual contracts. AIR Total Return futures replicate a total return swap, but as a listed and cleared futures contract are not subject to the uncleared margin rules that can adversely impact OTC equity swaps.

AIR Total Return futures offer an effective and cost-efficient vehicle for total return exposure. For additional information, please visit the Equity Index home page.