{kind=link}

Three reasons HDG Premium futures are a game-changer for steel risk management

CME Group launched HDG Premium futures in March 2020. The contract settles against the price difference between Hot-Dipped Galvanized (base) (HDG) and Hot-Rolled Coil (HRC), basis US Midwest, as assessed by CRU Group. The contract was launched after extensive market consultation. We highlight three reasons why this product can be a real game-changer for the ferrous industry:

Reason 1 – For service centers, it is a direct hedge for galvanized steel.

Let’s start with a brief example. In August, a steel service center receives an order to deliver processed steel to an OEM in October. The service center is not able to purchase galvanized steel in the spot markets today, due to Covid-19 disruptions and limited storage space. It will only be able to buy HDG in the spot market in October and needs to protect the business from an increase in prices in the interim. We assume that it agrees to a 100% fixed price today with the OEM, so it cannot pass through any potential increase in HDG prices.

“HRC-only” hedging

HRC futures for the October contract month trade at $530, and the current HDG premium is $150. The OEM and service center agree to a fixed price of $710, ostensibly generating a gross margin of $30 for the service center. Let’s first assume the customer uses HRC futures only.

The customer buys October HRC futures for hedging, thereby protecting the firm against an increase in HRC prices. However, the company is not hedged against a higher HDG premium. In the example below, the premium strengthens by $30, putting the entire service center margin at risk.

| "HRC only" hedge | |||||

| $/s.t. | HRC spot | HDG (base) spot | HDG premium | Financial hedge | |

| HRC futures (October maturity) | |||||

| August | 500 | 650 | 150 | 530 | Customer buys OCT futures at $530 |

| October | 550 | 730 | 180 | 550 | Final settlement price OCT HRC |

| Hedge performance | |||||

| Customer buys HDG at | 730 | spot price of HDG (base) in Oct | |||

| Futures performance | 20 | payoff of HRC hedge ($550-$530) | |||

| Net price for service center | 710 | $ Spot price minus hedge payoff | |||

| Agreed fixed sale price to OEM | 710 | $ | |||

| Gross margin | 0 | $ | |||

| *Note that example does not include exchange fees | |||||

HRC and HDG hedging

By including HDG Premium futures in the hedge transaction, the customer can protect their business from an increase in outright prices and from an increase in the galvanized steel premium. The customer locks in October prices for HRC ($530) and the HDG Premium ($150), resulting in a net purchasing price for HDG fixed at $680 today in August for October delivery. Now the service center’s margin is protected.

| HRC and HDG premium hedge | |||||||

| $/s.t. | HRC spot | HDG (base) spot | HDG premium spot | Financial hedge | |||

| HRC futures (OCT maturity) | HDG Premium futures (OCT maturity) | ||||||

| August | 500 | 650 | 150 | 530 | Customer buys OCT HRC | 150 | Customer buys OCT HDG |

| October | 550 | 730 | 180 | 550 | Final settlement price OCT HRC | 180 | Final settlement price OCT HDG |

| Hedge performance HRC | |||||||

| Customer buys HDG at | 730 | spot price of HDG (base) in Oct | |||||

| Hedge performance HRC | 20 | payoff of HRC hedge ($550-$530) | |||||

| Hedge performance HDG | 30 | payoff of HDG hedge ($170-$140) | |||||

| Net price for service center | 680 | $ Spot price minus hedge payoff | |||||

| Agreed fixed sale price to OEM | 710 | $ | |||||

| Gross margin | 30 | $ | |||||

| Note that example does not include exchange fees | |||||||

Prior to the introduction of HDG Premium futures, service centers with HDG price risk had to either: a) pass through the risk of a strengthening premium – meaning that OEMs would have to pay a variable component in addition to their fixed HRC price, or b) run the risk that a strengthening premium negatively impacts their business – as seen in the first scenario. HDG Premium futures present a potential solution to help service centers and other market participants mitigate risks around galvanized steel prices.

Reason 2 – Inventory protection

Firms active in the ferrous supply chain are able to use derivatives to protect their stock against a decrease in value. Let’s look at an intermediary storing galvanized steel. In April 2018, HRC was trading at $860 and the HDG premium was $155, meaning the galvanized steel price was $1015. Over the span of six months, HRC dropped to $830 – a $30 price move that could have been hedged by shorting HRC futures. At the same time, however, the premium dropped to $100 ‒ a loss in value against which the inventory holder was not protected. In fact, in this case, which uses real-world historical price data, the premium change of $55 was even higher than the $30 drop in HRC outright prices in the above scenario.

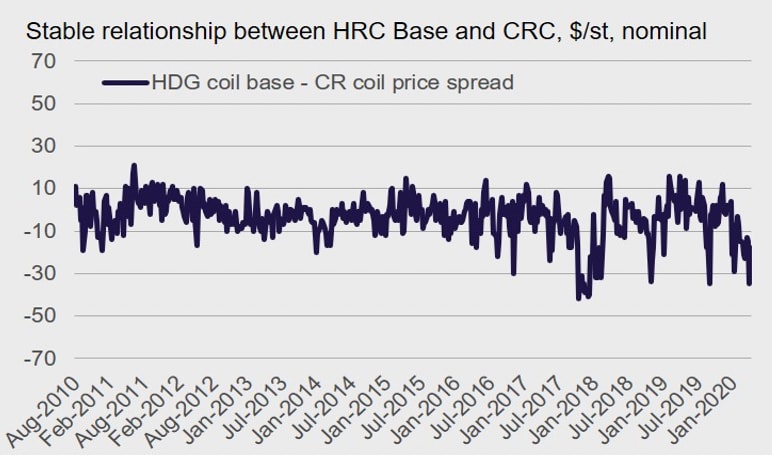

Reason 3 – HRC, HDG, and Cold-Rolled…

Most HDG steel is made using Cold-Rolled (CR) sheets. The prices for CR and HDG (base) are therefore very similar, historically trading within +/- 10$/s.t. of each other. This means that HDG Premium futures can be a useful tool for firms with exposure to the CR price. They can now use HDG Premium futures to manage CR price risk.

{kind=link}

Source: CRU Group

If you would like to speak about steel futures in more detail please contact us at metals@cmegroup.com.