{kind=link}

Managing Climate Risk with CME Group Weather Futures and Options

An increasing focus on climate-related risks has become a major driver of the demand for financial products offering protection to adverse outcomes related to weather and climate change. As a result of the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), credit rating agencies, more firms, and other bodies are examining their exposure to climate-related risks.1 Recently released, a major report by the US Commodity Futures Trading Commission’s (CFTC) Climate-Related Market Risk Advisory Committee (MRAC) highlighted the growing need for utilization of derivative markets to manage climate-related risk resulting directly from the impacts of climate change.2

This recent heightened awareness of climate-related risk has contributed to increased activity in CME Group Weather futures and options trading volumes and the addition of new market participants in the space, including hedge funds and asset managers:

- In 2020, futures volumes have increased 60 percent year-to-date with a notional value of $750 million, while options volumes increased 143 percent year-to-date with a notional value of $480 million.

- September 2020 marked the highest volume month in over two years, with an average daily volume (ADV) of over 1,000 contracts.

- As of December 2020, open interest (OI) was over 29,000 contracts, a 175 percent increase year-over-year.

This resurgence in CME Group’s Weather futures and options complex coincides with the move by CME to list all weather products, including options, for trading on CME Globex, the Exchange’s electronic trading platform.

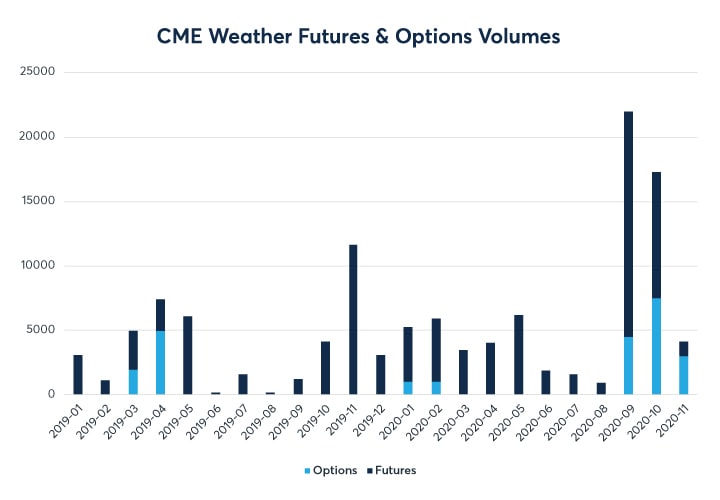

Figure 1. CME Weather futures and options monthly trading volume

{kind=link}

Source: CME Group

Reintroduction to CME Weather derivatives

The use of derivative markets for hedging climate-related risk has been around for over 25 years. These instruments traditionally include CME Group’s Weather and Power Market derivatives contracts, which are used by a wide variety of agricultural, energy, and financial-based entities from around the globe to help manage localized exposure to weather-related impact risk.

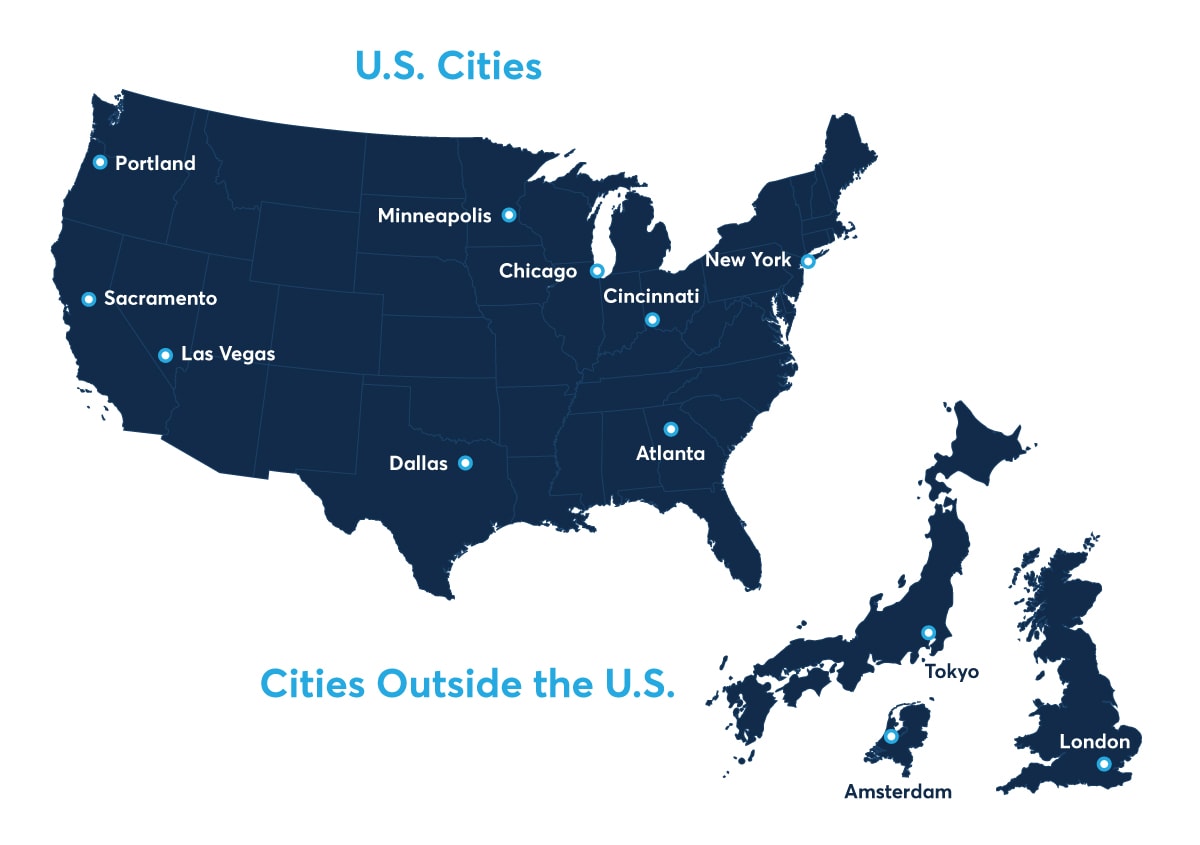

In 1999, the CME Group received approval from the CFTC to list the very first standardized weather futures contracts based on weather indexes of ten US cities. Subsequently, Amsterdam; London; and Tokyo, Japan were added for increased global coverage. Currently, there are nine US cities, two European cities, and one Japanese city listed at CME Group.3

Figure 2. CME Weather products

{kind=link}

Source: CME Group

HDD, CDD, and CAT Indexes

The CME Weather contracts for winter months in the US and Europe are based on heating degree days (HDDs), while the US summer month contracts are based on cooling degree days (CDDs). The concept of a heating degree day (HDD) index was developed by engineers who observed that commercial buildings were frequently heated to maintain an indoor temperature of 70° Fahrenheit whenever daily mean (average) outdoor temperatures fell below 65° Fahrenheit. Each degree of mean temperature below 65° Fahrenheit is counted as "one heating degree day." Conversely, air conditioning may be employed when temperature rises above the 65° Fahrenheit standard. Thus, each degree of mean temperature above 65° Fahrenheit is counted as "one cooling degree day." These concepts are expressed mathematically as follows:

HDD = Max (0, 65°F - daily average temperature)

CDD = Max (0, daily average temperature - 65°F)

To illustrate, if the average of a day’s maximum and minimum temperature on a midnight-to-midnight basis is 35° F, that day’s HDD is 30 (= 65°F - 35°F) and the CDD is zero (0). If the average of a day’s maximum and minimum temperature on a midnight-to-midnight basis is 45° F, that day’s HDD is 20 (= 65°F - 45°F). If the average daily temperature were in excess of 65°F, the HDD for that day would be zero.

Monthly HDD and CDD index values are simply the sum of each daily HDD or CDD value calculated according to how many degrees an average daily temperature rises above or below a baseline of 65° Fahrenheit in the US and 18° Celsius in Europe. Taking from the example used above, assume that the month had 31 days and the average daily temperature for all those days was 45°F. Accordingly, the cumulative monthly HDD would equal 620 (= 31 days x 20). The futures contract value would be identified by multiplying that figure by $20. In this example, the cash value of the contract would be $12,400 (= $20 x 620).

The European summer cooling month contracts are based on a cumulative average temperature (CAT). While in Tokyo, all listed months are based on CAT. Each monthly CAT index is simply the accumulation of daily average temperatures over a calendar month. These contracts further depart from the US standards in the sense that temperature readings are recorded in Celsius rather than Fahrenheit. Using Tokyo to illustrate, assume that the month had 30 days and the average daily temperature for each of the first 15 days was 10°C and the average daily temperature for each of the remaining 15 days was 20°C. Accordingly, the cumulative average temperature (CAT) would equal 450 (= (15 days x 10) + (15 days x 20)). The futures contract value would be identified by multiplying that figure by ¥2,500 (Japanese Yen). In this example, the cash value of the contract would be ¥1,125,000 (= ¥2,500 x 450).

A seasonal strip contract is based on the cumulative HDD or CDD values during a five-month period within the season. Similarly, a CAT seasonal strip is based on the cumulative average during the five-month period within the season. The traditional heating season runs from November through March while the traditional cooling season runs from May through September:

- HDD/CAT Seasonal Strips (Nov-Mar & Dec-Feb)

- CDD/CAT Seasonal Strips (May-Sep & Jul-Aug)

Seasonal strip contracts provide the same type of risk exposure as monthly HDD, CDD, and CAT contracts but offer the convenience of being able to trade a bundled package of months during the heating or cooling season.

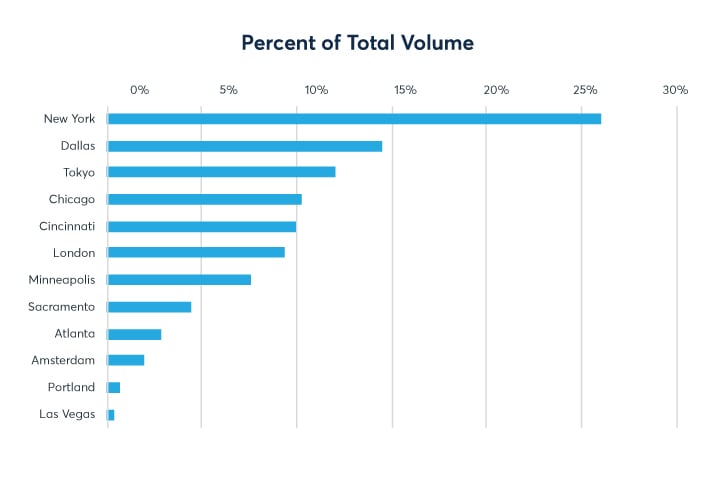

By indexing CME Weather futures and options, it makes it possible to trade weather in a way comparable to trading other index products such as stock indexes. However, unlike stock indexes, Weather products quantify weather in terms of how much the temperature deviates from the monthly or seasonal average in a particular city/region. The variations are geared to specific indexes/locations, with a dollar amount attached to each index point. In 2020 year-to-date, over 75,000 weather futures and options contracts have traded at CME. Figure 3 shows the listed cities ranked in order from largest to smallest in terms of proportional trading volumes.

Figure 3. Listed cities percent of total weather trading volume 2020

{kind=link}

Applications in risk management

HDD/CDD and CAT contracts are employed by a wide variety of enterprises, ranging from energy and agriculture, to breweries, and amusement parks. CME Weather derivatives offer a useful tool for hedging volumetric risks related to adverse temperature and climatic conditions.

Energy companies, for example, have been known to sell HDD or CDD contracts to manage the risk of diminished revenues under mild weather conditions, noting that the quantity of energy sold is heavily contingent upon consumer demand driven by temperatures. Large scale energy consumers including automobile manufacturers and large residential building operators may buy HDD or CDD contracts to hedge against the risk of rising utility costs under extreme weather conditions.

Retailers whose sales are sensitive to weather conditions might control inventory costs more effectively through the use of HDD or CDD contracts. Beer consumption reaches a seasonal peak in the summer and cool weather can put a dent in beer sales. From the 2000 Preliminary Report for SABMiller, “History shows that on a summer day with the temperature over 25 degrees Celsius, sales can be more than 50% greater than on a day where the temperature is under 20 degrees...”.

Amusement parks rely on favorable weather noting that people stay home if conditions are too hot or cold. It is a simple matter for parks to correlate temperatures to attendance and construct a “collar” to hedge revenues should temperatures fall outside a preferred range.

Agricultural production has a well-known sensitivity to weather, with adverse conditions impacting both the quality and quantity of crops yields. Authors of “Effectiveness of weather derivatives as a hedge against weather risk in agriculture” demonstrate the application and effectiveness of weather derivatives has been studied and proven in production of a wide variety of crops including grapes, corn, wheat, barley, soybeans, and cotton.4

Examining the use of temperature contracts on the part of utility companies, utilities may utilize HDD or CDD contracts to guard against so-called “volumetric risks.” These volumetric risks are based upon the quantity of energy that might be expected to be marketed throughout the course of a heating or cooling season. These transactions rely upon the intuitive and well-documented relationship between power consumption and temperature extremes.

Thus, if the daily average temperatures during a winter season were abnormally high, utility firms might face depressed demand for heating. Utilities have traditionally increased consumer prices to offset lower retail consumption volume. However, intensifying competition caused by ongoing deregulation has made it increasingly difficult for utilities to raise prices arbitrarily. Therefore, it becomes necessary for utility firms to address volumetric risks using other means such as HDD or CDD contracts.

A simple numerical example is presented here to illustrate the hedging application of HDD futures. Let us assume that ABC Utility Co. sells electricity in the Chicago area at $0.08/Kilowatt hour. Under normal winter weather conditions, ABC may forecast sales of 1 billion Kilowatt-hours (kWh) with a projected revenue of $80 million. However, ABC is concerned about the possibility of Ĕl Nino weather effects and would like to utilize HDD futures to hedge against the possibility of warmer than expected winter conditions.

In order to construct a hedging strategy, it will become necessary to quantify the relationship between economic outcomes (such as sales revenues) and weather conditions (as implied in weather futures prices). In particular, one wants to find an appropriate hedge ratio (HR) that might balance the anticipated change in revenues (denoted as ∆ Revenues) with the changing value of the subject derivatives contracts (∆ Value of Futures). A statistical regression between revenues and weather conditions is frequently useful in assessing these quantitative relationships.

Assume that, based on historical regressions, ABC finds that its sales are positively correlated with the CME Group Chicago HDD Index with a sensitivity ratio of 0.80. I.e., a 1 percent change in HDD may give drive a 0.8 percent change in ABC’s anticipated $80 million in revenues. Assuming futures are trading at 1,250.00, an effective hedge ratio may be calculated as follows.

| Hedge ratio (HR) | = | ∆Revenues ÷ ∆Value of Futures |

| = | ($80,000,000 x 0.8%) ÷ (1,250 x $20 x 1%) | |

| = | 2,560 futures contracts |

This suggests that ABC might sell 2,560 futures to hedge the risks of higher than expected temperatures and lower than expected revenues. Assume that temperatures are mild and that the HDD Index settles at 1,150. This decline of 100 HDDs (8 percent of original value of 1,250) implies that sales may decline from one billion to 936 million kWh for sales of $74,880,000 ($0.08/kWh x 936,000,000 kWh). This implies a revenue shortfall of $5.12 million. But this shortfall is offset by a corresponding $5.12 million profit in futures.5

| Revenues | Futures | |

| Now | Expected revenues of $80 million or 1 billion kWh @ $0.08/kWh | Sell 2,560 futures @ 1,250 |

| Later | Realized revenues of $74,880,000 | Futures settled @ 1,150 |

| Revenue shortfall of $5,120,000 | Profit of 100 HDDs or $5,120,000 (= 2,560 x 100 x $20) |

Proper use of temperature related contracts not only enables utility firms to stabilize revenue streams but may also be used to provide at least a partial hedge to the cost side of the equation. Note that most utility firms operate under inherent capacity limitations. Electricity represents a non-storable commodity. If temperatures suddenly rise or decline dramatically, utility firms may need to deploy less efficient generators to meet the sudden jump in demand or may be compelled to purchase electricity from the power grid in the face of soaring demands and rising prices. This implies that energy prices may increase and transmission costs may grow simultaneously. In this case, utility firms may find both weather derivatives and energy contracts useful to stabilize its economic outcomes, i.e., to hedge both volumetric and cost-based risks.

CME Group Weather markets reflect climate change

A recent paper by Wolfram Schlenker and Charles Taylor of Columbia University studying the mathematical relationship between CME Group’s Weather derivatives markets and the leading consensus climate models shows the Weather markets fully incorporate the climate model projections.6 In other words, the markets accurately price in in climate change and provide market participants with relevant information related to future weather and climate trends and the ability to hedge against related revenue loss. Observing futures prices since the early 2000s, their studies and analysis demonstrate that Weather futures market indexes across the US agree that climate is warming. As the authors state, “When money is on the line, it is hard to find parties willing to bet against the scientific consensus”.

Conclusions

As the awareness of the impacts and risks associated with adverse weather and climate change grow, reports such as MRAC’s “Managing Climate Risk in the US Financial System” suggest there will be a greater need for utilization of instruments such as those offered by the CME Group’s Weather complex. The 2020 trading volumes and entrance of new market participants in the space suggest future growth in the sector is well anticipated and underway.

While the associated risks each business and industry face are unique, standardized futures and options backed by CME Group’s market integrity, price transparency and liquidity can offer market users cost effective, flexible and transparent structures to manage their risk. To learn more, visit CME Group Weather.

References

- Task Force on Climate-related Financial Disclosures

- Managing Climate Risk in the US Financial System

- CME Group Weather products

- Effectiveness of weather derivatives as a hedge against weather risk in agriculture

- Note that this analysis is based upon an assumption that the relationship between sales and temperatures is linear when, in fact, it is more likely that a non-linear relationship exists such that energy demands will increase (decrease) exponentially as a function of rising (falling) HDDs. In other words, the hedge ratio becomes rather dynamic and may therefore require active adjustment in response to changing conditions.

- Market Expectations About Climate Change