{kind=link}

Is Oil-Indexation Still Relevant for Pricing Natural Gas?

The oil and gas markets have functioned over the years through megacycles that are driven by the balance between demand and supply. The trajectory of these oscillations is determined by the magnitude and the nature of the price shocks driven primarily from either the demand or the supply side. However, COVID-19 pandemic has created a new paradigm that combines both unprecedented demand destruction and a simultaneous supply shockwave that has reverberated throughout the fabric of the energy ecosystem.

Without a doubt, this global health crisis is having a profound impact on the economy as a whole and more specifically on the oil and gas markets. It is reasonable to anticipate that these developments may create new trends while accelerating some existing ones. It is also natural to be curious about the impact of these developments on oil-linked natural gas contracts that have already been losing their luster even before the pandemic. What are the structural challenges of oil indexation? Will it survive in the long run?

Broadly speaking, there are three main regimes for pricing natural gas, whether delivered by pipeline or via Liquefied Natural Gas (LNG) transport: (1) Hub pricing also known as gas-on-gas competition (“GOG”) or market-based pricing, which represents the framework by which natural gas is competitively priced based purely on the interplay between gas demand and supply; (2) oil-indexation, sometimes referred to as oil price escalation (“OPE”), which means contractually pricing natural gas using oil or other refined fuels prices; and (3) regulated prices set by governments.

Over the years, the gas industry has used oil-indexed long-term contracts that have usually been 20 to 25 years in most parts of the world. But oil-indexation is increasingly losing its economic attractiveness. Particularly with a gas glut, new arrangements that are more favorable to buyers are ever more in evidence (Grigas, 2018).

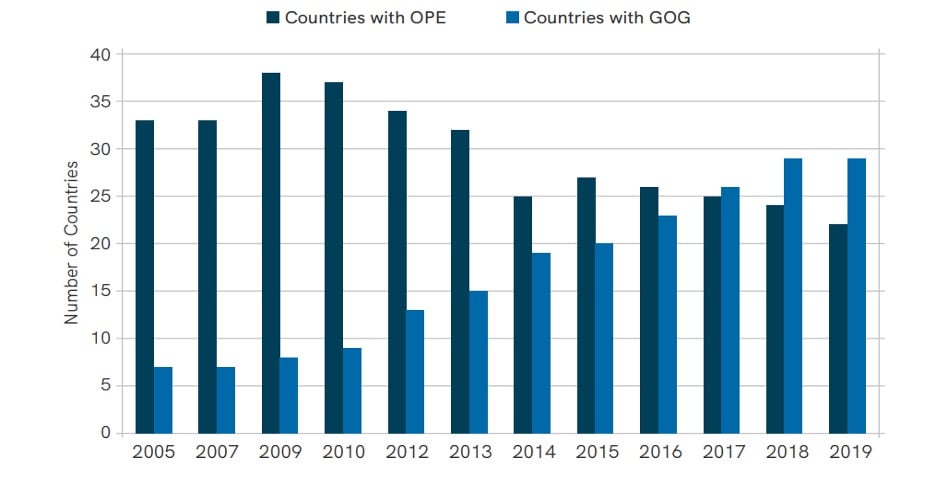

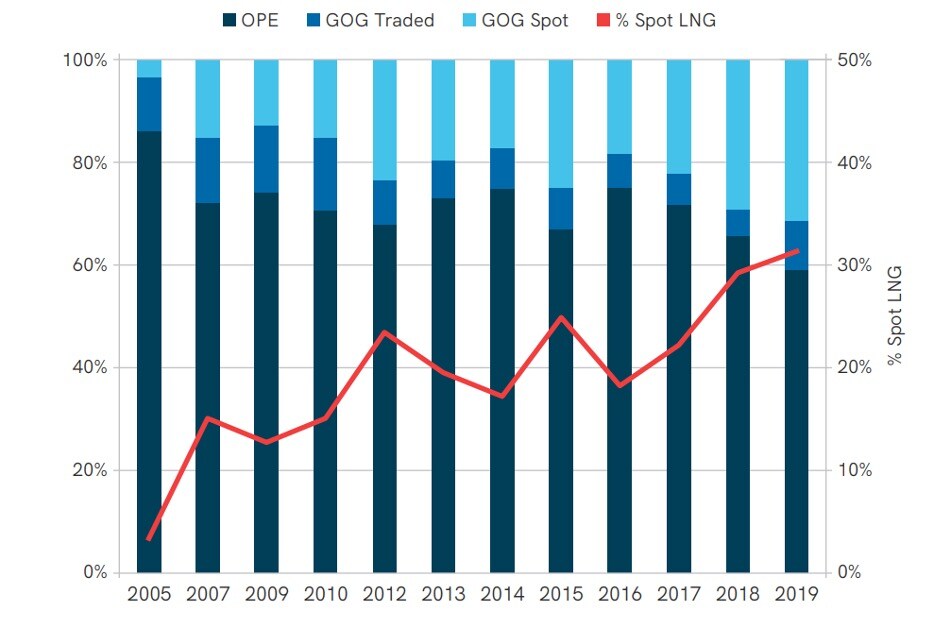

Figure 1 and Figure 2 illustrate how more countries are straying away from OPE as a pricing mechanism and adopting GOG instead. This explains the significant rise of the market share of GOG in LNG imports from 2005 to the most recent published data of 2019 while the share of OPE continues to decrease.

Figure 1 - Number of countries by price formation

{kind=link}

Source: International Gas Union (IGU) Wholesale Price Survey 2020

Figure 2 - World price formation- LNG imports

{kind=link}

Source: IGU Wholesale Price Survey 2020

Regional differences

The linkage of gas and oil prices is not uniform across the global market and should be analyzed in a regional context because natural gas is priced differently in the North America, Europe, and East Asia. Each regional market has historically followed a different evolutionary path and developed independently from the others due to various considerations including regulatory environment, contractual structuring, and economic conditions. Subsequently each regional market has gained its own distinctive attributes and idiosyncrasies. That said, these regional markets are becoming increasingly interconnected (Grigas, 2018).

The natural gas market in North America relies on a purely hub-based pricing or GOG mechanism whilst at the other end of the spectrum, the East Asian gas market is still heavily indexed to oil. Corbeau (2017) noted that “[c]reating a transparent and liquid hub … [can] take a decade.” The American experience is the most successful representation of the hub-based market structure. In essence, the U.S. has become home for the most mature, highly competitive, and fully liberalized gas market in the world after going through major milestones of deregulation and market liberalization, which in turn took 15 years of gradual policy changes (Till, 2018). The U.S. gas market is anchored around Henry Hub natural gas futures, which serve as a benchmark to all locations in the form of a differential or basis to account for regional market conditions, transportation costs, and available transmission capacity between locations.

The picture in Europe can be thought of as a mosaic since the level of transition from oil indexation to hub pricing varies across subregions. For example, Northwest Europe has the most advanced hubs followed by Central Europe. Southern Europe, in turn, is at an embryonic stage in hub pricing.

Contractual linkage versus economic linkage

It is important to differentiate between economic linkage versus contractual linkage with natural gas and oil. Oil indexation is a contractual linkage that is explicitly embedded in the contract while economic linkage refers to the direct relationship between the two fuels based on supply and demand factors. For instance, U.S. gas prices are established by the balance of gas demand and supply without any explicit reference to oil although natural gas and oil prices have moved in tandem in the long run due to their linkage through a substitution effect and resource competition (Mchich, 2018). This price relationship reached an inflection point after 2008, and they have since decoupled as the crude oil production surplus from the shale plays has redefined the relative supply structure of the two fuels.

Oil and gas are no longer competing fuels

In Asia, the genesis of linking gas prices to those of oil related products goes back to the 1960s when Japan enacted environmental regulations and started to offer financial assistance to power generation companies to incentivize them to switch to LNG/gas instead of burning crude oil and coal. In addition, Continental Europe independently adopted a similar strategy to promote switching from oil products to gas. This contractual linkage was founded on the hypothesis that oil and gas are close fuel substitutes in energy generation and industrial plants. Essentially, this makes their relative value to be equivalent to the difference in intrinsic heat contents in addition to any costs associated with transportation and production. Their relative value had historically kept both fuel prices from deviating significantly from each other. However, this hypothesis no longer holds as oil is becoming less a generation fuel and more of a transportation fuel that is still heavily influenced by geopolitical events. Regarding the latter factor, Putnam and Norland (2020) covered the plausible disruption scenarios unique to crude oil before the global health crisis hit this past spring. In comparison to crude oil, gas is now the de facto fuel of the stationary sectors, which includes the commercial, industrial, residential, and power generation sectors.

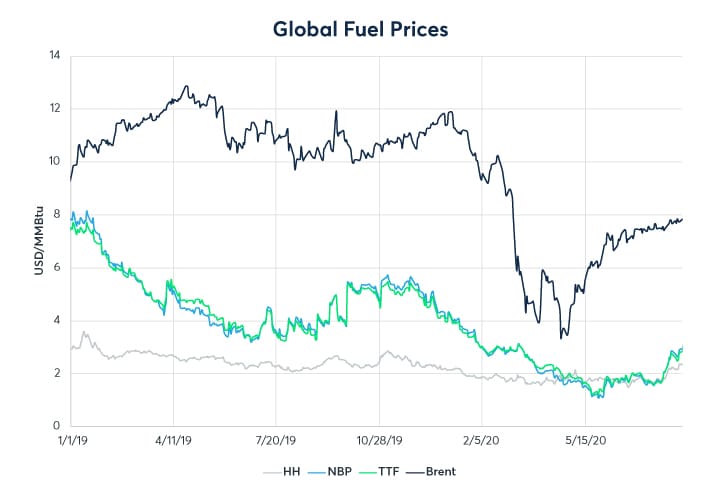

Figure 3 - Global fuel prices

{kind=link}

Source: CME Group

Note: HH stands for Henry Hub; TTF: Title Transfer Facility (in the Netherlands); NBP: National Balancing Point (in the U.K.); CSPI: Coal Switching Price Index (in Europe); and JKM: Platt’s Japan/Korea Marker. MmBtu stands for one million British Thermal Units.

LNG has traditionally relied on oil indexed long-term contracts to secure supply and finance capital intensive projects. Added Corbeau (2017): “Long-term commitments from buyers [were] … regarded as … [critical] for projects to move ahead, notably because banks [had] regard[ed] these elements as an essential part of project financing.” In the Asian markets, imported LNG has historically been priced based on the average of a basket of crude oil imports into Japan known as the Japanese Customs-cleared Crude (JCC) price. The JCC price usually has a one-month lag from the Brent oil price. The duration of the lag varies depending on the negotiated contract terms. Some contracts can be priced based on averaging JCC prices from one year to 5 years. This type of pricing is usually supplemented by spot transactions to balance the positions of importers in those markets. The spot transactions are usually priced using gas-on-gas competition-based markers such JKM or Henry Hub. The rationale behind averaging the Brent price is to smooth out any spikes or price shocks that are inherent to the oil market.

Oil indexation has been subject to criticism due to its structural flaws, which have prohibited a full-commoditization of LNG. Recently the COVID-19 pandemic and its drastic impact on energy prices seems to have exacerbated those flaws and magnified market inefficiencies.

This pricing system can create an economic disparity between the current market price when the gas is delivered (via cargo or pipeline) and the contracted price. The effect of the embedded lagged oil price is significantly amplified in an extreme volatile environment. As illustrated in Figure 3, oil prices suffered a severe price shock in March 2020 due to fundamentals that are intrinsic to the oil market. Yet, residuals of this shock will be carried and rolled several months forward to price gas that will delivered at a future date under very different market conditions.

Pirrong (2017) provided an apt historical analogy in understanding how problematic the oil-indexation approach has become:

“It would arguably be only slightly less efficient to put LNG on the gold standard than the oil standard. From 2009 to 2015, the correlation between the spot price of LNG, delivered to Japan and South Korea … and the price of Brent crude oil was -1.4%. During the same period, the correlation between the JKM LNG price and the price of gold was -2.4%. Thus, pace Keynes, oil benchmarking of LNG has become a ‘barbarous relic’ because oil-linked prices do not reflect the value of gas to purchasers, or the cost of producing it.”

The economic misalignment caused by oil indexation represents a major risk that can potentially erode the profitability of a commercial deal for either the buyer or the seller side depending on the direction of the price shock. The industry has traditionally relied on contractual provisions called “Price Review Clauses” or “Price Openers,” which allow the parties to make price adjustments if the market conditions change and the contract price does not adequately reflect current supply and demand dynamics. Since there is no standard language for those clauses, parties may find themselves in a situation where they have to negotiate and come to an agreement about the elements and circumstances that can trigger such stipulations. According to Christie and Ogut (2017), enforcing a Price Review provision is not an easy exercise because parties tend to have different interpretations of the terms which can subsequently become a fertile ground for debate that can often end up in arbitration or litigation.

Conclusion

Arguably, oil-indexation contracts have lost their relevance as oil and gas prices continue to decouple. The impact of the pandemic has provided further evidence of how this pricing framework has become ever more obsolete and an impediment to market competition and efficiency.

References

Christie, K. and E. Ogut, 2017, “The Interplay of Force Majeure and Change of Circumstances with Dispute Resolution Clauses in Modern Long-term LNG Contracts - What Role for A Price Review Clause?”, Oil, Gas & Energy Law Intelligence, Vol. 15, No. 4, November. Accessed via website:

https://www.lalive.law/wp-content/uploads/2019/10/ov15-4-article11.pdf on August 22, 2020.

Corbeau, A.-S., 2017, “LNG Markets in Transition,” Global Commodities Applied Research Digest, Industry Commentary, Vol. 2, No. 1, Spring, pp. 112-116.

Grigas, A., 2018, “The New Geopolitics of Natural Gas,” Global Commodities Applied Research Digest, Industry Commentaries, Vol. 3, No. 2, Winter, pp. 103-110.

Mchich, A., 2018, “Are Crude Oil & Natural Gas Prices Linked?”, CME Group Report, May 9. Accessed via website:

https://www.cmegroup.com/education/articles-and-reports/are-crude-oil-natural-gas-prices-linked.html on August 22, 2020.

Pirrong, C., 2017, “Liquefying a Market: The Transition of LNG to a Traded Commodity,” Journal of Applied Corporate Finance, Vol. 29, No. 1, Winter, pp. 86-92.

Putnam, B. and E. Norland, 2020, Global Commodities Applied Research Digest, Research Council Corner, The Economist’s Edge, January.

Till, H., 2018, “From Grain to Natural Gas: The Historical Circumstances That Led to the Need for Futures Contracts,” Global Commodities Applied Research Digest, Contributing Editor’s Collection, Vol. 3, No. 1, Summer, pp. 90-94.

About the Author

Hilary Till is the Solich Scholar at the J.P. Morgan Center for Commodities (JPMCC), University of Colorado Denver Business School and Contributing Editor of the JPMCC’s Global Commodities Applied Research Digest. Ms. Till is also a principal of Premia Research LLC. Prior to Premia, Ms. Till was the Chief of Derivatives Strategies at Putnam Investments where she oversaw the strategy development and execution of about $90 billion annually in derivatives strategies.

Ms. Till’s additional academic affiliations include her membership in the North American Advisory Board of the London School of Economics (LSE) and her position as a Research Associate at the EDHEC-Risk Institute in Nice, France. She has been a panel member at the U.S. Energy Information Administration’s (EIA’s) workshops on financial and physical energy market linkages, including the EIA’s workshop on the dynamics of oil, natural gas, and LNG markets. She has a B.A. with General Honors in Statistics from the University of Chicago and an M.Sc. degree in Statistics from the LSE where studied at the LSE under a private fellowship administered by the Fulbright Commission.

About the Author

Adila Mchich is a Director in Research and Product Development at the CME Group. She focuses on the fundamentals of energy markets. She has over 10 years of experience serving multiple roles in Market Research & Development, Risk Management, and Product Valuation at the CME Group. Ms. McHich, started her career as a Quantitative Analyst.

Ms. McHich, has also authored a series of articles on derivatives and energy markets. She is a member of the International Association for Energy Economics and the United States Association for Energy Economics. She received her M.S. degree in Financial Engineering from NYU Tandon School of Engineering.