{kind=link}

Are Crude Oil & Natural Gas Prices Linked?

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Crude oil and natural gas are major fuels in the global energy mix. Their price linkage has been examined by many economists and industry observers due to its implications on broad swaths of the market including trading strategies, investment decisions, energy policy, and portfolio optimization.

Crude oil and natural gas prices have historically moved in tandem as a result of the linkage between the two commodities on the supply and demand sides. But their price relationship reached an inflection point after 2008 and they have since decoupled. The article discusses how the price relationship between crude oil and natural gas has evolved over time and the economic mechanisms behind their linkage from the supply and demand prospectives.

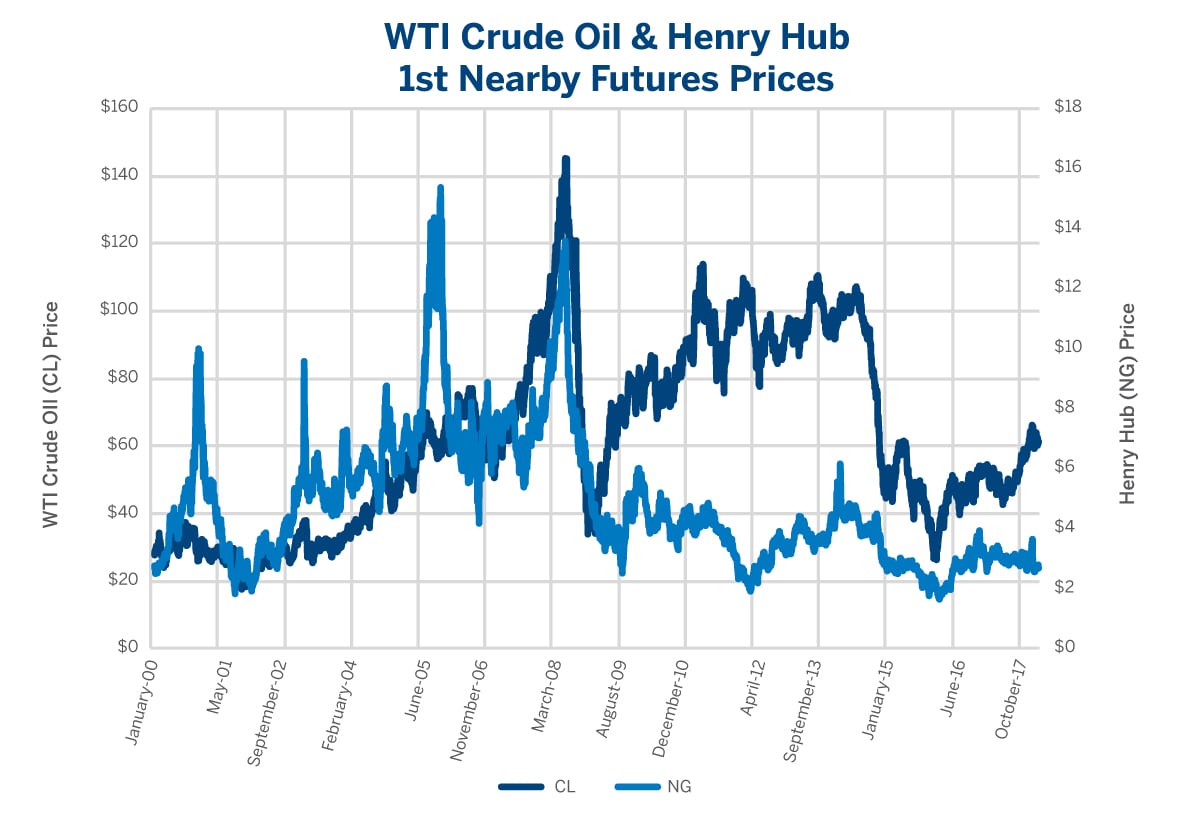

Figure 1

{kind=link}

Chart Source: CME Group

Resource Competition

From the supply side, the crude oil and natural gas price linkage is mainly driven by the direct competition for drilling resources at the wellhead. Natural gas can be produced from three types of wells: associated, non-associated, and condensate wells. The associated wells produce primarily oil with natural gas as a by-product. The non-associated wells refer to the wells that produce just natural gas, sometimes with just a small amount of oil. The condensate wells produce natural gas along with natural gas liquids (NGLs). The economics of non-associated gas fields are different from the economics of associated gas fields as the development of the latter depend on the dynamics of the oil market.

Since most Exploration & Production companies produce both natural gas and oil, they have to make a decision related the allocation of capital and resources to the exploration and development of either commodity based on the return on investment. With respect to natural gas extracted from an oil rig, an increase in crude oil prices may likely lead to an increase in associated gas production which would likely exert downward pressure on natural gas prices.

On the other hand, an increase in crude oil prices may lead to increase oil drilling which would decrease natural gas drilling, potentially leading to higher natural gas prices. The price signal between the two commodities is a catalyst that can prompt suppliers to produce one fuel source instead of the other in order to maximize profits. To some extent, the oil-natural gas price relationship depends on the source of the natural gas.

Fuel Substitution

Some refined fuels produced from crude oil are competitive substitutes to natural gas. Residual fuel oil competes directly with natural gas in the electric power generation and industrial sectors. An increase in crude oil prices would likely encourage the substitution of natural gas for petroleum products, which would increase natural gas demand and then prices. This substitution effect is sometimes referred to as “burner-tip parity”. This implies that natural gas prices converge with the price of the competing fuel at the burner tip or at the final destination on a BTU-equivalent basis. Any increase in crude oil prices motivates end-users to substitute natural gas for petroleum products in consumption where possible. This in turn increases natural gas demand and hence prices.

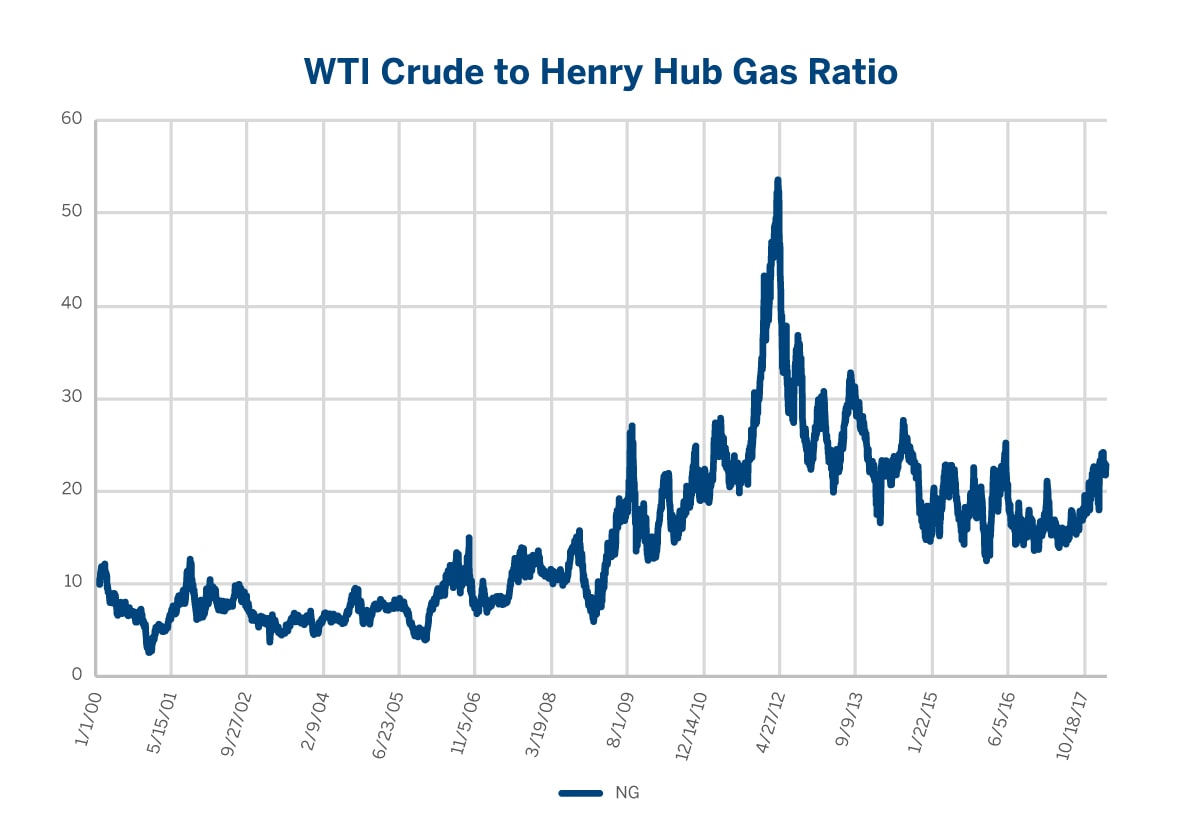

Figure 2

{kind=link}

Chart Source: CME Group

Crude-Gas Ratio

The industry has traditionally relied on the crude-gas ratio to measure the relative value of both commodities. Since 2000, this ratio has fluctuated between 3:1 and 54:1 which is different from the theoretical ratio of 6:1 based on the thermal parity also known as the Btu ratio. This ratio is derived from the fact that one barrel of oil is equivalent to 5.85 MMBtu. This implies that if the market prices of the two fuels were equal based on their energy content, the ratio of crude oil prices to natural gas prices would be approximately 6. As depicted in Figure 2, the ratio averaged 8 from 2000- 2007, then started to increase at the end of 2008 in response to the significant decline of crude oil prices during the recession. Afterwards, the ratio started to recover, reaching 27 in 2009, and continued to climb to reach a record 54 in 2012, due to the drastic increase in the oil price and decline in the natural gas price. During this period, the increase in the oil price was largely a result of the unstable political climate caused by the Arab Spring.

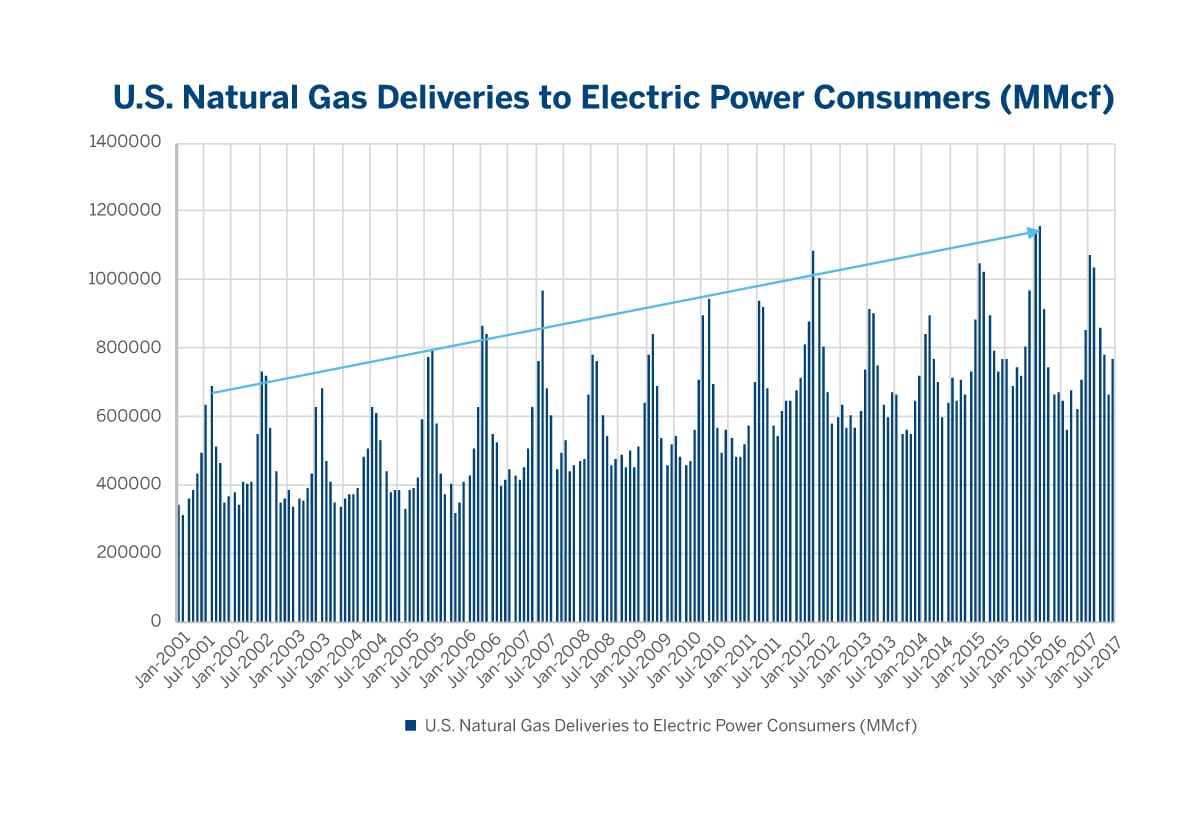

Meanwhile, natural gas prices weakened as production from the northeast Marcellus shale play started rising. The crude-gas ratio remained strong until 2014, which encouraged drilling for oil instead of natural gas. Concurrently, weak natural gas prices favorably impacted NGL economics by encouraging producers to switch to drilling more profitable NGL-rich wells. This led to the expansion of the processing industry which invested in infrastructure. From the demand side, end-users shifted their fuel preference to natural gas in order to cut costs. This shift in fuel preference is reflected through the growing trend of natural gas electricity consumption as illustrated in Figure 3.

Figure 3

{kind=link}

Chart Source: EIA

The economic factors linking natural gas and crude oil markets through substitution and competition effects would suggest they are connected through a long-run relationship. As shown in Figure 1, crude oil and natural gas prices predominantly moved in synchronization prior to 2008 except for some periods in which natural gas prices spiked and moved independently of crude oil.

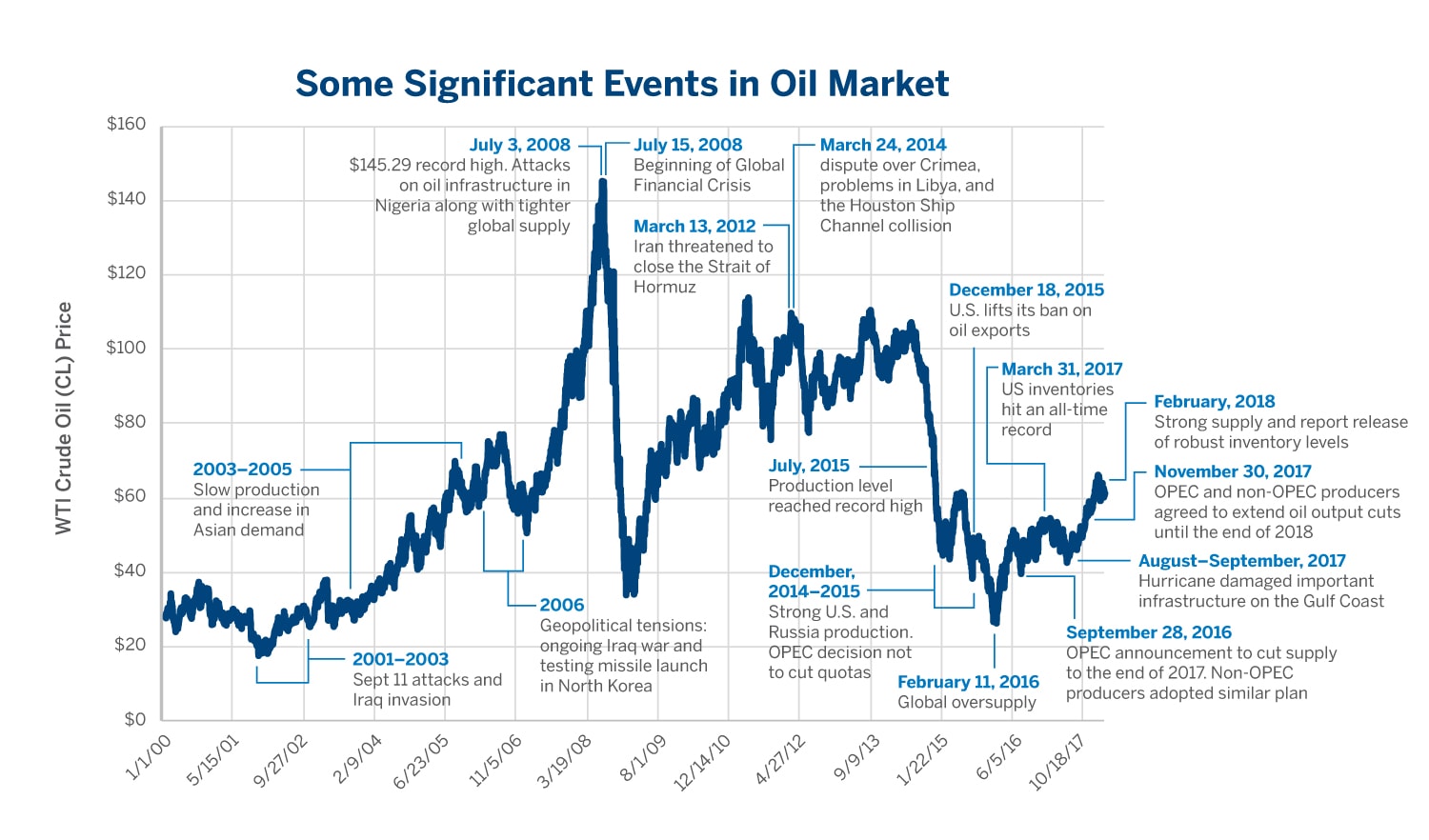

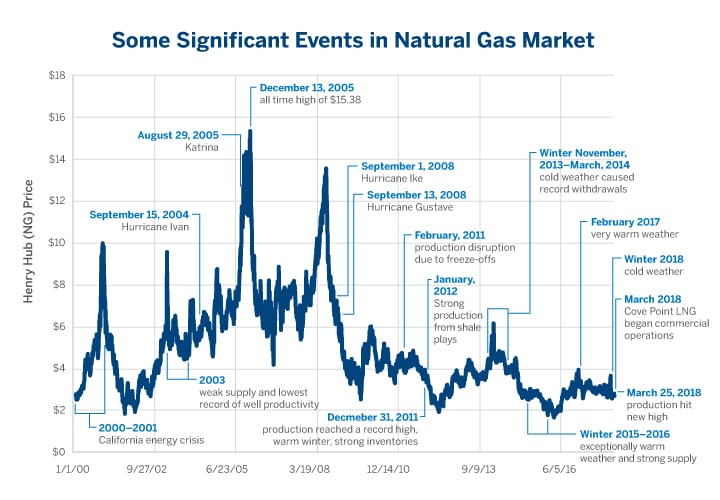

These price shocks were attributed to commodity-specific events as shown in Figure 4 & 5. In particular, natural gas is more prone to short-term price shocks and supply imbalances due to seasonality, storage dynamics, and weather-related events, which tend to increase the volatility and cause disequilibria to the short run oil and gas linkage. For example, in 2005 hurricanes Katrina and Rita caused a supply disruption that triggered a significant spike in natural gas prices, while the impact on oil prices was not significant. On the other hand, oil has a more geopolitical dimension and responds to global events. For example, following global economic expansion, oil prices rose to reach $145/bbl. In July 2008 then collapsed to below $40/bbl. because of the credit crunch and recession.

Figure 4

{kind=link}

Figure 5

{kind=link}

Chart Source: CME Group

The price relationship between natural gas and crude oil underwent a shift whereby natural gas prices strayed from oil prices following 2008. This apparent departure from the norm may have been attributed to the changes that affected the substitution and competition linkage between natural gas and crude oil.

For the past decade, the demand for residual oil for electricity production has contracted significantly for various reasons including: (1) the retirement of ageing petroleum generation assets, (2) the surge of new gas-fired combined cycle capacity turbines which have enhanced efficiency, (3) increased usage of natural gas in power generation due to low natural gas prices, and (4) environmental concerns which rise from high sulfur content of residual oil. These factors suggest that displacement due to gas-to-oil switching is a shrinking factor in determining the price relationship between natural gas and crude oil in terms of demand.

With respect to changes in the supply side, the Permian Basin in West Texas and New Mexico is at the center of the relationship between natural gas and oil production via associated gas. The production of both commodities has been experiencing soaring growth due to the lower breakeven costs and vast acreage that the basin offers. Permian associated gas is estimated at approximately 7 billion cubic feet (Bcf). Major players, including ExxonMobil, are spending billions of dollars to expand the infrastructure in the Permian because of its favorable drilling and production economics. The build-out in oil drilling and production is expected to stimulate an increase in associated gas. Although associated gas is an important component of US natural gas supply, the impact of this link has been relatively muted by strong supply from other shale plays specifically Marcellus/Utica, which has contributed to downward pressure and weak gas prices. Therefore, shale production has proved extremely important in the decoupling of oil and gas prices.

Conclusion

Natural gas and crude oil are both extremely important to the U.S. economy. The energy arbitrage between the two fuel sources was a significant determinant of their long-term price relationship, which in the past was relatively stable. The recent shale revolution has redefined the supply structure of the two fuel sources and has led to the decoupling of oil and gas prices. This fundamental shift is likely to prevail in the foreseeable future, unless the supply-induced downward pressure on gas prices is alleviated by a significant increase in exports of U.S. natural gas in the form of liquefied natural gas (LNG).

To read more economic research reports like this one or subscribe to the mailing list, visit cmegroup.com/research