{kind=link}

Is automotive demand for platinum increasing or decreasing?

Summary

Platinum has been used in autocatalysts for over forty years, with automotive demand the single largest demand segment for platinum, accounting for around 40% of annual platinum demand. As a result, investor sentiment towards platinum is heavily influenced by trends in the auto sector, which has had to overcome significant challenges, including the Dieselgate scandal, in recent times.

This year, automakers are feeling the negative impact of the COVID-19 pandemic; in the first half of 2020, global light vehicle sales contracted 28% year on year, with European sales down 43%. Yet behind the headline data, and against a background of tightening emissions legislation around the world, a more detailed examination reveals several automotive themes, including resurgent diesel demand and substitution by platinum for palladium, that point to a more positive outlook for platinum automotive demand than auto sales data alone might suggest.

Introduction

Automotive demand is the single largest demand segment for platinum. It is comprised of three main applications: autocatalysts; sensors; and spark plugs. Of these, platinum use in autocatalysts is predominant, accounting for over 95% of total automotive demand.

Figure 1: Sources of platinum demand

{kind=link}

Source: WPIC Platinum Quarterly. N.B. Platinum demand from the automotive sector could be viewed as an ‘industrial’ use of platinum, but it is considered as a separate category due to its size and the strategic nature of vehicle emissions control

This year, the auto sector has been significantly negatively impacted by COVID-19 and, in the first half of 2020, global light vehicle sales contracted 28% year on year, with European sales down 43%. Because automotive demand for platinum accounts for c.40% of total annual platinum demand, the fall in vehicle sales in 2020 has negatively impacted platinum investor sentiment. However, the aggregate data hides several positive platinum and diesel trends which, together with the background, trends and outlook for automotive platinum demand, are presented here.

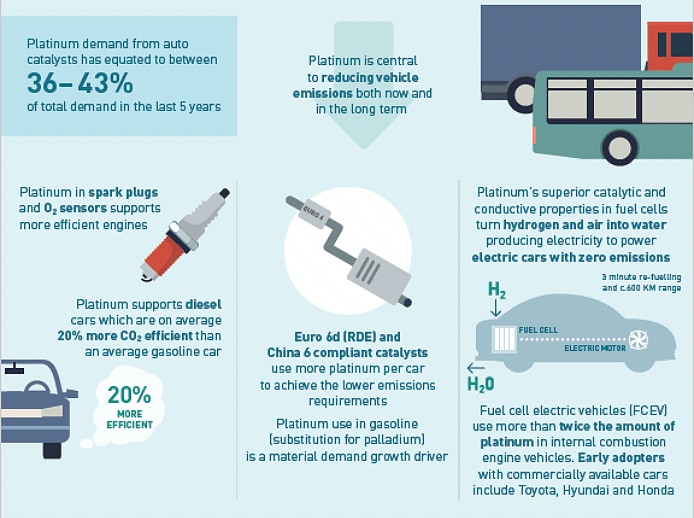

Figure 2: Infographic showing platinum automotive demand

{kind=link}

Source: WPIC

Emissions continue to be subject to increasingly strict regulations in most countries around the world and platinum – an excellent catalyst - is instrumental in reducing the three main emissions from internal combustion engines: unburned hydrocarbons (HC); carbon monoxide (CO) and oxides of nitrogen. Its sister Platinum Group Metals (PGMs) palladium and rhodium are also used in autocatalysts to control vehicle emissions. PGMs’ automotive demand is determined by the four main drivers detailed below:

- Vehicle numbers – The more vehicles on the road, the more autocatalysts are needed which increases the total PGMs required or demand. Vehicle production and sales are driven by economic growth, and consumer trends. Shared vehicle use, for example (Uber, Lyft) could reduce vehicle ownership in developed markets. The opposite is true in growing markets as vehicle ownership per capita grows. The negative impact of the COVID-19 pandemic will be material on vehicle sales although the exact impact is still being evaluated.

- Vehicle sizes - Large vehicles typically have large or more powerful combustion engines and require higher amounts of PGMs per vehicle to achieve the regulated emissions levels. Historically, this relationship was broadly linear; i.e. a 1.5 litre vehicle needed about half as much PGM content as a 3 litre one did. So, a consumer trend for larger vehicles had a positive impact on PGM demand (and vice versa). This remains largely true although higher performance vehicles of similar engine size can have far higher loadings, and fear of missing regulatory compliance has resulted in ‘over engineering’. This is where more metal is used to ensure emissions regulation compliance under all conditions and is mainly due to fears after the ‘Dieselgate’ scandal in 2015 (cheating by automakers in the US) and the subsequent introduction of more stringent on-road tests that replaced in-laboratory ones.

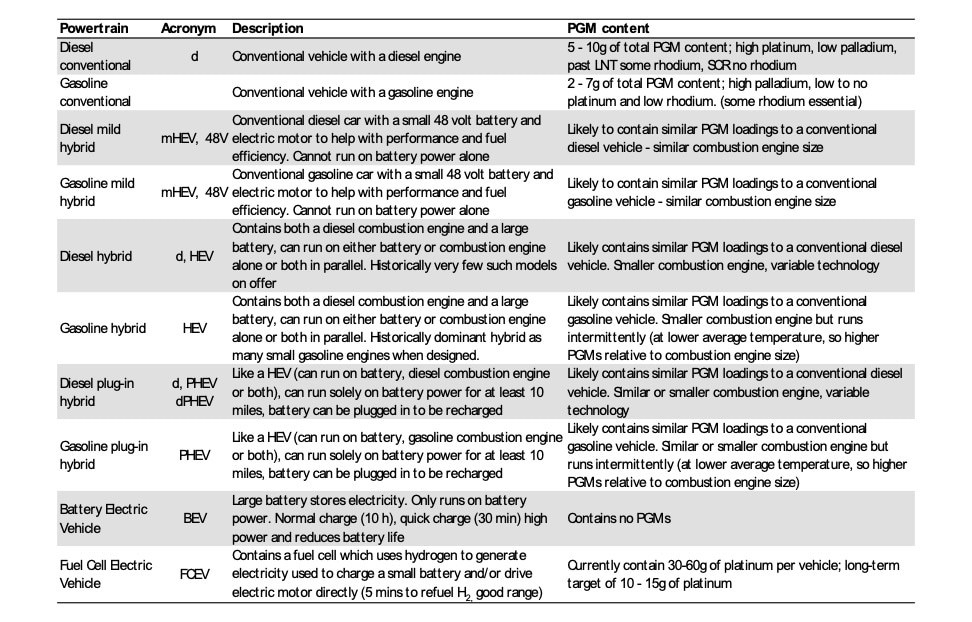

- Powertrain trends - Different powertrains (e.g. diesel, gasoline hybrid, battery electric and fuel cell electric) have significantly different loadings of platinum, palladium and rhodium. Only Battery Electric Vehicles do not contain any PGMs. Historically, diesel vehicles have the highest platinum loadings of internal combustion engine vehicles. A higher share of diesel vehicles on the road would increase platinum demand (and vice versa).

- Technological changes (including substitution) – The dominant driver of increased platinum automotive use has been to meet tightening emissions legislation. Countries and regions have applied progressively more stringent emission limits on HC, CO, CO 2 , NOx, NH 3 and particulates emitted from vehicles. Regulation is typically most stringent in developed countries, with developing countries following a similar trend. However, the China 6 emissions regulations being implemented for cars are more stringent than current EU and US regulations. The China VI regulations for trucks also require much heavier platinum loadings than average loadings in Western markets. This reverses historic developments where China lagged the west. All else being equal, to achieve lower emissions from a (non-battery) vehicle, a higher volume of PGM content is needed. Technological improvements can go some way to offset this; autocatalyst manufacturers have significantly improved the efficiency of catalysts in meeting emissions regulations and this has allowed them to ‘thrift’ PGM usage per catalyst. This has been achieved by, for example, advances in wash-coat formulations (the layer on the autocatalyst surface that holds PGM molecules in place), and the tailoring of catalysts to individual vehicle models, as well as the impact of reduced sulphur content in fuels. Patterns of use between platinum, palladium and rhodium in autocatalysts have varied over time, while emissions standards have grown ever more stringent. Usage is determined by multiple factors including the effectiveness, availability and price of each metal. The catalytic efficiency of each metal is influenced by engine temperature, fuel type, fuel quality and durability of the autocatalyst’s washcoat. Today, platinum is predominantly used in autocatalysts in diesel vehicles, with palladium principally in those in gasoline vehicles. However, this usage is shifting, with substitution of platinum for palladium occurring due to sustained palladium deficits and the high price of palladium, as of August 5, 2020, palladium is still over US$1,000/oz higher than platinum.

Figure 3: Vehicle powertrain breakdown

{kind=link}

Source: WPIC Research

What is an autocatalyst?

An autocatalyst is a device that reduces harmful emissions from internal combustion engine (ICE) vehicles by converting exhaust pollutants, including: carbon monoxide (CO); oxides of nitrogen (NOx); hydrocarbons (HC); and particulates into ‘atmospheric’ products, mainly CO2, nitrogen and water.

Also called ‘catalytic converters’, autocatalysts are made using a metal or ceramic substrate that is coated with a layer of PGM containing material (or washcoat) and canned in a metal housing. The placement of the autocatalyst (there can be more than one unit per vehicle) within a vehicle varies depending on the design of the vehicle and the vehicle’s powertrain (whether it is a diesel or gasoline powered vehicle, or a hybrid of either).

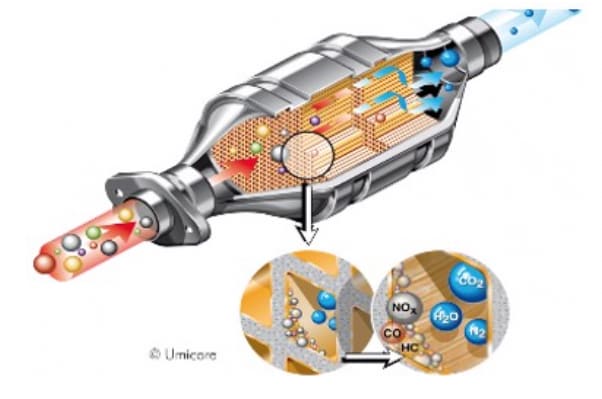

Figure 4: A typical autocatalyst

{kind=link}

Source: Umicore

Both heavy duty vehicles, for example trucks and buses, and light duty vehicles (passenger cars and vans), are fitted with autocatalysts; almost all vehicles sold worldwide each year have these devices. Patterns of use between platinum, palladium and rhodium in autocatalysts have varied over time, while emissions standards have grown ever more stringent. Usage is determined by multiple factors including the effectiveness, availability and price of each metal.

The catalytic efficiency of each metal is influenced by engine temperature, fuel type, fuel quality and durability of the autocatalyst’s washcoat. Today, platinum is predominantly used in autocatalysts in diesel vehicles, with palladium principally in those in gasoline vehicles. However, this usage is shifting, with substitution of palladium for platinum occurring due to sustained palladium deficits and the high price of palladium.

Systems to control emissions have become increasingly complex over the past decade as emissions limits have tightened, especially since 2015 when the scandal known as ‘Dieselgate’ heightened scrutiny of NOx emissions from diesel vehicles.

Dieselgate alerted consumers in Europe to the fact that diesel cars were emitting far more NOx on the road than they did in a laboratory-based test necessary for approval for sale. This meant that the level of harmful NOx emissions from nearly all diesel cars was excessive and causing poor city air quality, despite apparent compliance with prevailing European emissions regulations, known as Euro 5 and 6. In fact, at that time in Europe, millions of Euro 5 and 6 compliant vehicles, having passed an in-laboratory test demonstrating emissions below 180mgNOx/km or 80mgNOx/km respectively, were shown to actually emit over 500mg/km in on-road testing; some as high as 1,400mg/km.

Diesel NOx emissions are mainly controlled using either Lean NOx Trap / NOx Storage Catalyst (LNT) systems or Selective Catalytic Reduction (SCR). Both LNT and SCR systems need PGMs to catalyse CO, HC and NOx.

In an LNT system, NOx removal uses cycles in the fuel/air ratio while the SCR system injects ammonia (as liquid urea / AdBlue ®) to react with NOx which has passed through the diesel oxidation catalyst (DOC). The SCR system may also need an Ammonia Slip Catalyst (ASC), that contains platinum, to prevent excess ammonia emissions.

SCR offers effective NOx reduction without compromising fuel efficiency in diesel engines. This is significant, as fuel efficiency is an important criterion in the quest to reduce CO2 emissions from both diesel and gasoline vehicles, although in this regard diesel vehicles have always had the advantage over gasoline vehicles, even today having 20 per cent lower CO2 emissions per kilometre than their gasoline equivalents.

PGMs in autocatalysts

Platinum, palladium and rhodium all have the necessary physical and chemical properties that make them well suited to autocatalysis. Their activity enables the reactions within the autocatalyst to occur at the low temperature-conditions that exist during cold starting of a vehicle, when emissions are at their highest. Durability is also important, since catalytic converters need to perform over the life of the vehicle. Without PGMs, the desired conversion reactions in the catalytic converter would not take place, resulting in the vehicle failing to meet emissions regulations. Other materials have been tried but have not met the long-term activity and durability requirements of modern-day emission control systems.

Although platinum has the longest track record as an autocatalyst of any PGM, with a history of use in both diesel and gasoline vehicles, today it is primarily used in diesel vehicles. The question of which PGM is best suited to a particular emissions-control system (and optimal loading) and the extent to which platinum, palladium and rhodium can be substituted for one another is complex, and dependent on several factors.

For example, diesel engines operate at lower temperatures than gasoline engines and run with a leaner gas stream containing lots of oxygen. Under these conditions, platinum is a more active catalyst for the conversion of CO and hydrocarbons to harmless emissions. However, the addition of some palladium to the platinum catalyst can improve its thermal stability. This is an advantage when reducing diesel particulate matter from the exhaust. This process involves trapping the particulate matter in a filter and then raising the temperature of the system to oxidise the matter to CO2. At these higher temperatures, palladium improves the thermal durability of the catalyst, helping it perform optimally for the lifetime of the vehicle.

Automotive demand trends

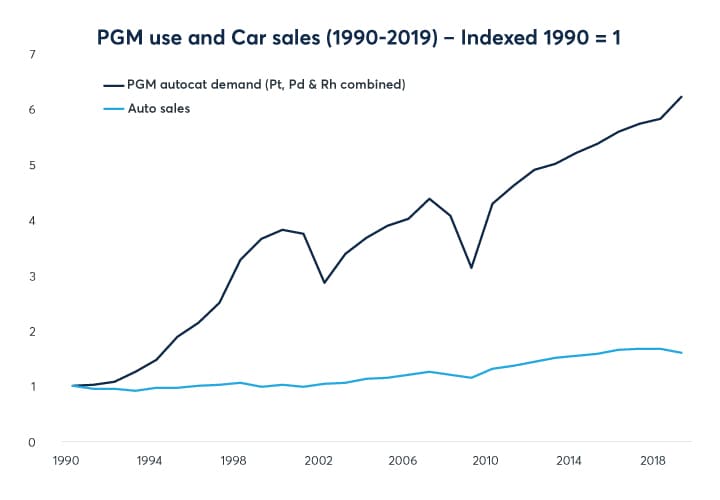

Historically, tightening emissions legislation, more than actual changes in volumes of auto sales, has driven platinum and PGM automotive demand growth. Between 1990 and 2019 annual car sales rose from c.54 m to c.92 m. but PGM use in autocatalysis rose from 2.2 moz per annum to 13.8 moz per annum.

Figure 5: Total PGM autocatalyst demand growth is well above global auto sales growth over 29 years (6.2 times v 1.6 times)

{kind=link}

Source: OICA, LMC Automotive, Johnson Matthey. Indexed chart with 1990 = 1

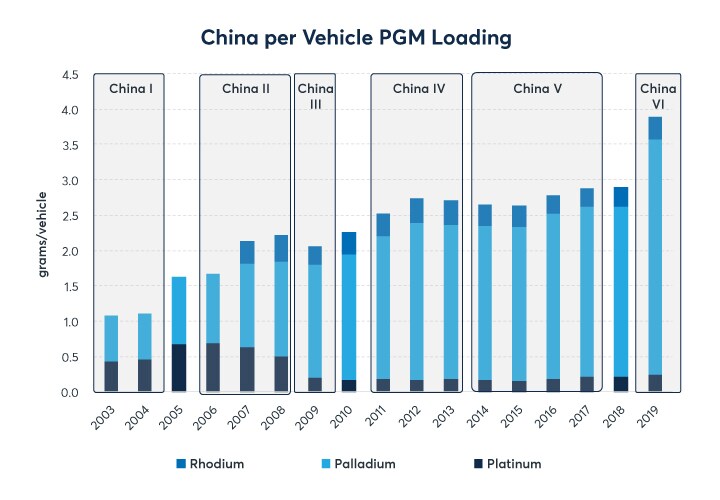

All major auto markets have introduced tighter vehicle emissions limits over time and significantly tighter light duty vehicle emissions legislation in recent years. The introduction that has had the biggest impact on PGM use is the China 6 standards which started being implemented in major cities in China from mid-2019. This implementation has resulted in a step change of c.40% in palladium loadings and between 50% and 100% more of rhodium. This increased demand for palladium in China and Europe has increased the likelihood of platinum substituting palladium in autocatalysts. This is where the highest demand growth in platinum is most likely to occur in the next three years. Only 5% substitution represents 450 koz.

Figure 6: China 6 implementation: step change in loadings

{kind=link}

Source: Johnson Matthey, WPIC Research

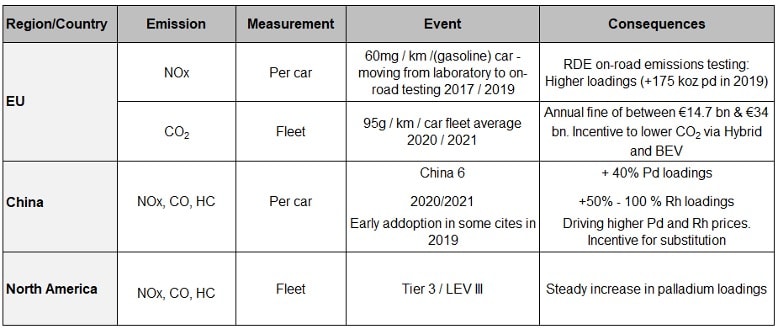

Figure 7: Key light duty auto emissions legislation recently implemented

{kind=link}

Source: WPIC Research

The combination of rapid auto sector driven palladium demand growth, combined with limited supply growth outlined above, suggests a re-balancing between platinum and palladium markets is highly likely.

Substitution of platinum for palladium in autocatalysts

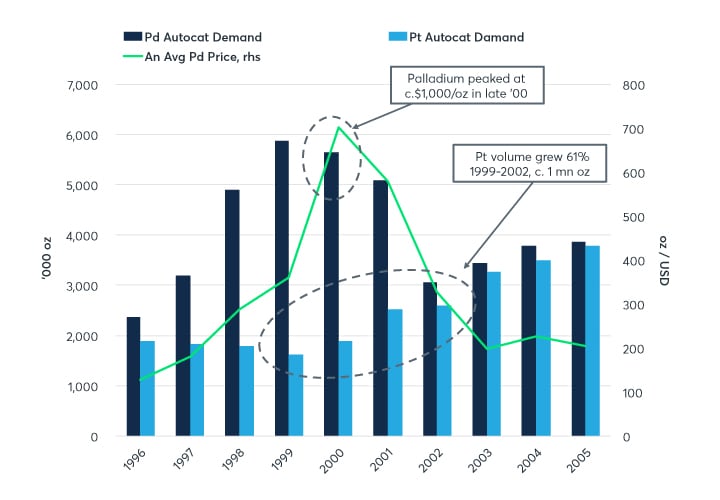

Substitution of platinum for palladium in response to price misalignment is not a new phenomenon. The US first introduced emissions standards in 1974 which required the use of auto catalysts. This led to the use of both platinum and palladium in internal combustion engine vehicle emissions control. By the late 1990s, palladium demand consistently outstripped supply. The annual shortfall was supplied from Russian state stocks. These stocks had built up as palladium was seen as having little value or application during the early years of production from the Russian Nickel-copper mines. Much of this stock had built up almost accidentally and had been transferred to state stocks. In 2000, an administrative failure in Russia coincided with a processing failure in South Africa that resulted in palladium increasing from around $200/oz to over $1,000/oz within a few months.

The consequence of this short-term price spike to levels well above the price of platinum was substitution of palladium by platinum with a significant demand increase for less expensive platinum. As illustrated in the figure below, gross palladium usage in auto catalysts contracted by 48% between 1999 and 2002. Palladium prices quickly reduced in line with reduced demand to $260/oz by January 2003. Platinum auto catalyst usage rose by 60% over this same period.

Figure 8: Palladium and Platinum auto demand vs Price, 1996 – 2005

{kind=link}

Source: Johnson Matthey, Bloomberg, WPIC Research

Until the early 2000s, twice as much palladium than platinum by mass was required to achieve similar levels of emissions reduction in gasoline engines. However, technological innovation, namely the improved stability of PGM molecules in the coating on catalysts and the significant reduction in sulphur content of gasoline, reduced this substitution ratio to the point where similar amounts of palladium or platinum can achieve the same level of emissions control. This 1:1 ratio was confirmed by Johnson Matthey in an academic paper publishing in 2013 (A Study of Platinum Group Metals in Three-Way Autocatalysts – Platinum Metals Rev., 2013).

Palladium is not solely used in gasoline autocatalysts. Around 700 koz of palladium per annum is used in diesel autocatalyst applications in key markets (Western Europe, North America and China). Platinum substituting palladium in diesel catalysis, the natural and long-standing home of platinum, has much lower emissions control risk than substitution in gasoline catalysis and should have a significantly shorter substitution implementation lead time. In May 2019, Johnson Matthey said it expected that the use of platinum in diesel autocatalysts to replace palladium could grow by tens of thousands of ounces in the short to medium term.

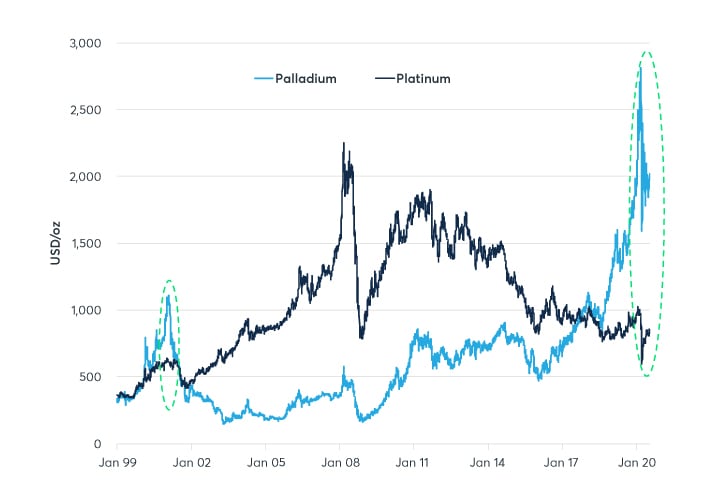

Figure 9: Palladium premium to platinum averaged $675/oz in 2019, and has averaged over $1,000/oz in 2020

{kind=link}

Source: Bloomberg, WPIC Research

The economic theory of substitution suggests that manufacturers will substitute a cheaper input for a more expensive one, up to a point where it is no longer economically logical to do so. That point can be price/cost driven, as rising demand for the initially cheaper alternative drives up prices of that input or related to the impact of substitution on the performance of the output product. A substitute good is also a good with a positive cross elasticity of demand i.e., an increase in the price of one good will (all things being equal) increase demand for its substitute. Theoretically, if the prices of the goods differed, there would be reduced demand for the more expensive good.

In the case of the palladium price above the platinum price, theory suggests that where viable, more platinum should be used in automotive catalysts instead of palladium. The 1:1 substitution ratio further suggests that platinum and palladium can be viewed as almost perfect substitutes.

At the current palladium premium to platinum, and with a 1:1 substitution ratio between the two metals, there is a very strong economic argument for auto producers to substitute more platinum on future models. Palladium’s current elevated price is an availability signal that also argues for PGM diversification to maintain supply chain security. Historically, sustained relative premiums (e.g., Pd over Pt) of at least 18 months or more were needed to see significant auto catalyst loadings change among the 3 PGMs (i.e., the ratios used of Pt, Pd and Rh). With no short to medium term palladium supply growth likely, the only adjustment can be via demand. The concerns of unavailability of palladium were known by OEMs and fabricators some years ago, which suggests substitution has happened on models recently launched or about to be launched. In principle, the substitutability of platinum and palladium suggests that their diverging prices should converge over the medium-term (3-5 years) as demand substitution adjusts the relative demand-supply balances.

The platinum versus palladium price chart (Figure 9) above shows palladium’s overshoot in 2000 and currently as well as the change in price to reflect the change in substitution ratio from 2:1 to 1:1 between 2014 and 2017.

Automotive demand and the platinum investment case

A combination of factors, including the likelihood of substitution and regulatory changes, means that upside remains on the horizon for platinum automotive demand, despite the challenges to the automotive industry posed by the COVID pandemic. In addition, the picture that is emerging for 2020 global vehicle sales requires a more nuanced reading than headline figures would suggest, with several strands showing positive developments for diesel and better than expected performance, especially as far as heavy-duty vehicles in China and mild hybrid diesel vehicles in Western Europe are concerned.

The unavailability of palladium remains a serious consideration for automakers. While the palladium market looks likely to be balanced for 2020 (pre-COVID, deficits of between 1.2 moz and 1.9 moz for 2020 were forecast by competent participants in the market), it remains a fact that palladium supply remains constrained. This is because over 80% of palladium is produced as a by-product, to nickel in Russia and platinum in South Africa. The Russian nickel orebody is particularly high grade and is run at full capacity but has very long lead times on output increases due to high capital investment and seasonal weather complexity. South African platinum producers typically make long-term investment decisions based on the fundamental supply-demand outlook. The current palladium price is unable to stimulate investment in growth as these producers know platinum is a far more likely mechanism to re-balance the market than additional palladium supply.

The palladium price remains significantly above that of platinum and above the level at which autocatalyst manufacturers have indicated is the point of substitution in gasoline engines on cost grounds alone. Indeed, despite sales of gasoline vehicles falling more in 2020 than those of diesel vehicles, palladium’s large premium to platinum increased, averaging $1,300/oz in H1’20 ($755/oz in H2’19). In 2018, substitution efforts focussed on the low temperature gasoline V6 and V8 engines in the US typically found in the Ford F150, Dodge Ram and similar vehicles. Annually this segment accounts for nearly 3 million vehicles. If 40% of palladium were substituted by platinum in models launched in 2019 and 2020 (c.30% of annual sales in 2020), this would increase automotive platinum demand in 2020 by 93 koz, saving $142 per vehicle.

The high price, sustained demand growth and limited supply growth of palladium makes material platinum demand growth due to substitution of some palladium in gasoline cars extremely likely. Details of this substitution remain proprietary and highly confidential. Many market participants and investors are unable/unwilling to act until this confidential information is known. Fortunately, autocatalyst fabricators, including Johnson Matthey, are acknowledging that substitution can be done and is happening. This is still described as ‘some years off’ rather than explained as proprietary and confidential. The recent announcement from BASF, the German chemicals company, that it has successfully developed and tested new autocatalyst technology that enables the partial substitution of high-priced palladium with the relatively lower-priced platinum in light duty gasoline vehicles, without compromising emissions standards, supports this view further.

The magnitude of substitution is also becoming more widely considered. Some 9.7 moz of palladium are used annually in vehicle emissions control while only 3 moz of platinum are used in vehicles. Replacing only 5% of the palladium with platinum at a 1 to 1 ratio (also now more widely known) would require over 450 koz more of platinum and less of palladium; this will do little to ameliorate the palladium deficit yet creates a significant demand increase in platinum.

Regulatory drivers are a further upside factor that should not be overlooked, with diesel/diesel hybrid powertrains offering considerable CO2 emissions benefits over and above their gasoline counterparts, and some encouraging dataflow that shows promise with regard to sales of diesel heavy duty vehicles and mild-hybrid diesel vehicles.

Over the first 5 months of 2020 there has been an unexpectedly quick recovery in Chinese heavy-duty vehicle (HDV) production; 90% of which have diesel engines. COVID-19 driven factory shutdowns in China reduced HDV production in February by 51% year on year and led to auto market commentators forecasting double digit contractions for 2020. However, cumulative Chinese HDV production from January to May 2020 is almost 8% higher than in 2019. Should HD vehicle production from June to December 2020 remain at the same level as in 2019, this together with actual sales will increase platinum demand in 2020 by between 14 koz and 85 koz, depending on the portion of China VI emissions compliant vehicles automakers choose to produce over the remainder of the year.

Further, sales of mild-hybrid diesel cars in Europe have bucked the down trend in overall European light vehicle sales so far this year. In the UK, diesel mild-hybrid sales surged by 211% year on year in the first half of 2020, double the rate of growth in gasoline hybrids. Similarly, in Spain H1 diesel-hybrid sales were up 44% with gasoline hybrid sales down -9%. Total hybrid sales in H1 in Germany were up by 55%, helped by German automakers such as Audi, BMW and Mercedes offering diesel-hybrids across more of their model ranges. Growing diesel-hybrid sales have helped stabilise Europe’s diesel market share at c.30% this year, with new model launches likely to reverse its downtrend in recent years.

If you would like to speak with CME Group about our Platinum products please email metals@cmegroup.com [link-bold]

IMPORTANT NOTICE AND DISCLAIMER

This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development, providing investors with the information to support informed decisions regarding platinum and working with financial institutions and market participants to develop products and channels that investors need. No part of this report may be reproduced or distributed in any manner without attribution to the authors. The research for the period 2019 and 2020 attributed to Metals Focus in the publication is © Metals Focus Copyright reserved. All copyright and other intellectual property rights in the data and commentary contained in this report and attributed to Metals Focus, remain the property of Metals Focus, one of our third party content providers, and no person other than Metals Focus shall be entitled to register any intellectual property rights in that information, or data herein. The analysis, data and other information attributed to Metals Focus reflect Metal Focus’ judgment as of the date of the document and are subject to change without notice. No part of the Metals Focus data or commentary shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of Metals Focus.

Any research for the period 2013 to 2018 attributed to SFA in the publication is © SFA Copyright reserved. All copyright and other intellectual property rights in the data for the period 2013-2018 contained in this report remain the property of SFA, one of our third party content providers, and no person other than SFA shall be entitled to register any intellectual property rights in the information, or data herein. The analysis, data and other information attributed to SFA reflect SFA’s judgment as of the date of the document. No part of the data or other information shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of SFA.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, neither the publisher nor its content providers intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Neither the publisher nor its content providers is, or purports to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, neither the publisher nor its content providers can guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher and Metals Focus note that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results and neither the publisher nor its content providers accepts any liability whatsoever for any loss or damage suffered by any person in reliance on the information in the publication.

The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks.