{kind=link}

Introduction to Platinum

Precious metal with wide industrial uses

Platinum has a unique combination of physical and chemical properties; it is in demand as both a precious and industrial metal. Its high melting point, density, ultra-stability and extreme non-corrosiveness make it crucial to many industrial and manufacturing processes, yet it is also used to fabricate the finest jewellery in the world. Platinum is also an investment asset that reflects its value across the demand spectrum from industrial to precious metal. It is included in investment portfolios via physical bars and coins, on-line bullion accounts, physically-backed exchanged traded funds and through futures contracts.

One of platinum’s most important uses is as a catalyst – the presence of even a small molecule can speed up chemical reactions, reducing process energy needs and improving yields. Platinum enabled the first-ever autocatalysts in the 1970s and to this day it remains a key component in vehicle emissions control; predominately in diesel autocatalysts in both light and heavy-duty vehicles.

Biocompatible and well tolerated by the body, platinum is used in numerous established medical treatments and is at the forefront of many new ones. It is radiopaque due to its density, giving high x-ray visibility, especially important in stents and clot-retrieval devices used to treat cardiovascular disease. In addition, it is an excellent electrical conductor when used in pacemakers and cochlear implants. Compounds made from platinum are used in the treatment of many cancers.

Glass, petrochemicals, silicones and sensors are all produced using platinum. It is present in the hard disk drives that continue to enable the growth of cloud storage in the global computing industry. Fuel cell technology that made the moon landing possible uses a platinum catalyst to produce electricity from hydrogen; key in renewable power generation and transport. Today, platinum is more relevant than ever as emission-free platinum fuel cells unlock the nascent hydrogen economy.

Thirty times rarer than gold

Thirty times rarer than gold, platinum is found at very low concentrations in the Earth’s crust. Platinum extraction from mining is concentrated in only three geographical locations in the world, with 80 per cent of all production in Southern Africa. Around 6 moz (190 metric tons) of platinum is mined worldwide each year, compared to 108 moz (3,300 metric tons) of gold. Each year, a further 2 moz (60 metric tons) of platinum comes from recycling, predominantly from autocatalysts in end-of-life vehicles.

{kind=link}

Diverse demand drivers

Non-investment platinum demand is broadly split between three segments: automotive applications (mainly autocatalysts in diesel vehicles) at c.40 per cent of demand; jewellery, also at c.40 per cent; and industrial at c.20 per cent of demand.

Platinum has strong, long-standing associations with the luxury goods market, especially in western markets and Japan. Recent growth in demand for platinum jewellery has come from the US, China and India, which maintained double digit growth in 2018. Research has shown platinum to be the precious metal most associated with love and the expansion of platinum into global jewellery markets is rooted in buyer behaviour in the bridal sector, especially among millennials, although self-purchasing is becoming an increasing trend.

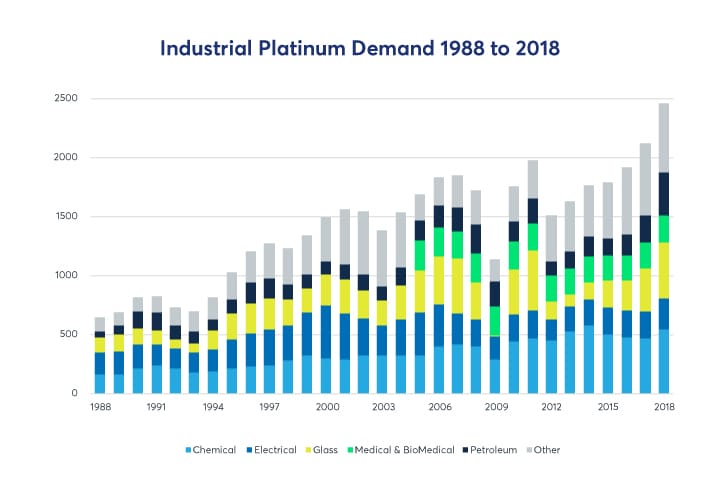

Industrial uses of platinum are myriad and industrial demand has quadrupled over the last thirty years. For example, its catalytic properties are used to make nitric acid for fertiliser and in the petrochemical industry to make higher octane fuels during the reforming process. Platinum’s high melting point, stability and non-corrosiveness are vital to the glass making industry, as it can withstand the high temperatures necessary without distortion or causing contamination. Light emitting diode screens and glass fibre are produced using platinum.

Automotive demand – traditionally the strongest demand sector for platinum - suffered as a result of the emissions testing scandal of 2015. However, the rate of decline is easing, and consumer confidence in diesel vehicles may return as new, more stringent emissions standards come into force globally.

Figure 1: Industrial Platinum Demand 1988 to 2018

{kind=link}

Source: Johnson Matthey PGM Market Report May 2019

The investment case for platinum

Introduction

For the past 50 years, platinum has traded at a premium to gold for over 80 per cent of the time as its supply/demand fundamentals added to its ‘precious’ value. However, in recent years, negative sentiment, rooted in concerns over the decline in demand for platinum in jewellery and autocatalysts, has seen this premium eroded.

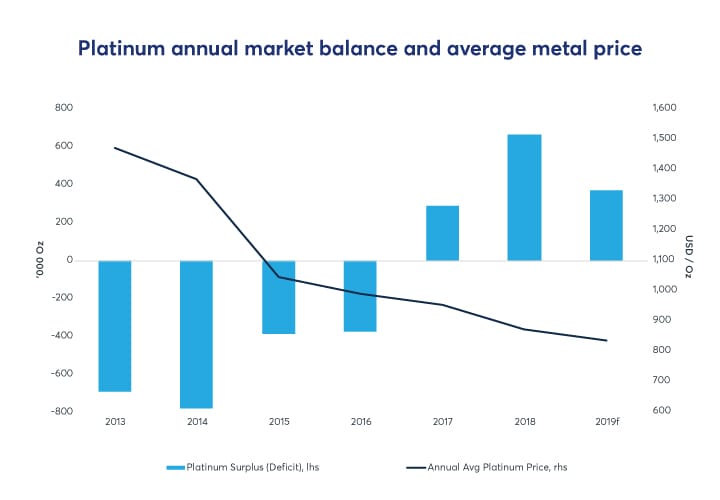

Today, platinum’s investment case is becoming more widely known. The reasons for past price weakness are better understood and supply/demand fundamentals are showing signs of strengthening (Figure 2), with demand growth signalling future deficits. On this basis, platinum looks undervalued relative to gold and silver, with its price still close to an all-time low, presenting a low-risk entry point for investors.

Figure 2: Platinum annual market balance and average metal price

{kind=link}

Source: Bloomberg, WPIC Research, as at 18 October 2019

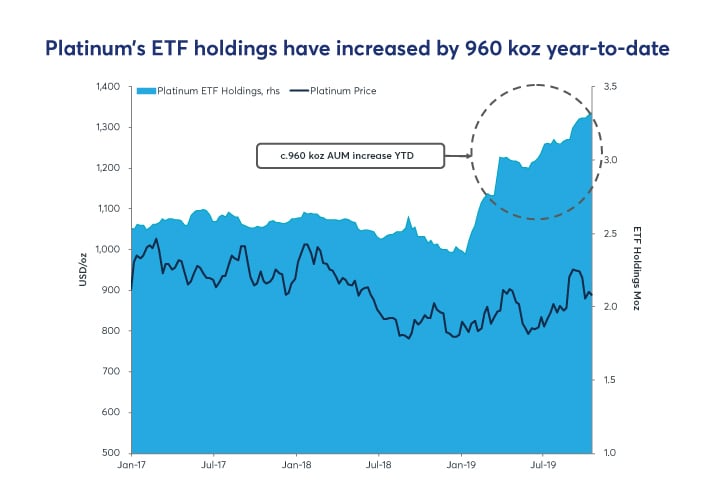

This re-reading of the platinum investment case and consequent shift in sentiment, recognising upside potential as well as inherent supply constraints, is reflected in 2019 year-to-date growth in ETF holdings, as shown in Figure 3.

Figure 3: Platinum’s ETF holdings have increased by 960 koz year-to-date

{kind=link}

Source: Bloomberg, WPIC Research, as at 18 October 2019

Upside potential, automotive recovery and fuel cell electric vehicle adoption

There is significant upside on the horizon for platinum automotive demand. In Western Europe, automakers are now required to comply with new European fleet CO2 emissions targets. As a result, automakers are likely to resume the active promotion of diesel cars (which was halted following the 2015 emissions scandal), because increasing the proportion of diesel cars sold will assist in meeting emissions targets and avoiding costly fines. The resultant increase in sales of diesel cars will have a positive impact on platinum demand – for example, a 4 per cent increase in diesel share equates to an extra 100 koz of platinum demand per annum. Outside of Europe, the high price of both palladium and rhodium, coupled with constrained supply, argues for substitution from palladium to platinum in gasoline autocatalysts, presenting further upside potential for platinum, especially as China 6 emissions regulations kick in, which are even more stringent than US and EU regulations.

So far this year, the palladium price has traded, on average, US$595/oz higher than platinum. This is well beyond the level that autocatalyst manufacturers have suggested as being the point of substitution on cost grounds alone. Johnson Matthey expects palladium’s eighth consecutive deficit in 2019 to be over 800 koz, with significant palladium demand growth expected as China 6 is implemented. Significantly, over 80 per cent of palladium is produced as a by-product, to nickel in Russia and platinum in South Africa, so meaningful short-term palladium supply growth is not possible. A very limited amount of palladium substitution by platinum would be material for platinum demand; only 5 per cent substitution would increase annual platinum demand by 400 koz.

Demand for platinum fuel cell electric vehicles (FCEVs) is on the rise, with growing acceptance that FCEVs will sit alongside battery electric vehicles as part of a multi-drivetrain solution to achieve zero on-road emissions. In the near term, platinum demand from FCEVs will come from heavy duty applications.

Constrained supply

Platinum is rare, concentrated in one location with underground reserves requiring significant capital investment to extract and refine. Platinum mining output from South Africa has fallen steadily since 2006, despite ten years of rises in the price of the basket of metals sold by platinum mining companies. New mining projects coming on stream will not compensate for the expected reduction in yield from mature, high-cost operations in the near term and the outlook is pointing to a reducing surplus with potential for a deficit as latent demand growth takes off.

Platinum in a portfolio

Platinum is suited to many more private and institutional portfolios than currently include it and there are several ways to include platinum as an investment: physical bars and coins (typically 99.95 per cent fine bullion); online bullion accounts; physically-backed exchanged traded funds; and through futures contracts.

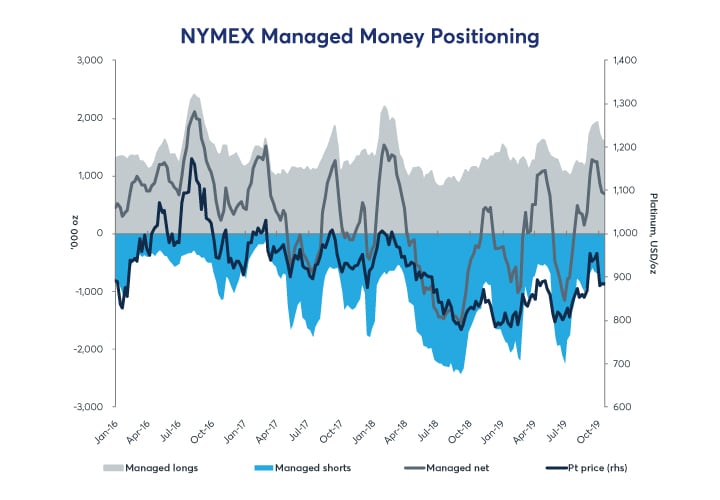

With the high correlation between the prices of platinum and gold (even after removing the effects of the USD), platinum performs much of gold’s diversification role and offers upside potential should it revert to a position where its price reflects supply/demand fundamentals that recognise upside from demand growth and its industrial value-in-use. Recent NYMEX positioning supports the view that this is beginning to happen, with recent short-term prices being positively affected by net investor positioning on Nymex (Figure 4).

Figure 4: NYMEX positioning shows stable short and long positioning

{kind=link}

Source: Bloomberg, WPIC Research, as at 18 October 2019

Important Notice and Disclaimer

This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need. No part of this publication may be reproduced or distributed in any manner without attribution to the authors. Unless otherwise specified in this document all material is © World Platinum Investment Council 2017. Material sourced from third parties may be copyright material of such third parties and their rights are reserved. Content within the publication that has been provided by SFA, one of our third party providers, is © SFA Copyright reserved. All copyright and other intellectual property rights in such content contained in this publication remain the property of SFA, and no person other than SFA shall be entitled to register any intellectual property rights in the information, or data herein. The analysis, data and other information attributed to SFA reflect SFA’s judgment as of the date of the document and are subject to change without notice. No part of the content provided by SFA shall be used for the specific purpose of accessing capital markets (fundraising) without the written permission of SFA.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, neither the publisher nor SFA intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Neither the publisher nor SFA is, or purports to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, neither the publisher nor any third party can guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results and neither the publisher nor any third party accepts any liability whatsoever for any loss or damage suffered by any person in reliance on the information in the publication.

The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks.