{kind=link}

CME FX Swap Rate Monitor User Guide

Overview

The CME FX Swap Rate Monitor calculates an implied interest rate differential based on pricing data from CME Group FX futures and the FX Link central limit order book. The interest rate differential implied by the OTC FX spot and FX futures markets is a useful measure when comparing the impact of interest rates to highlight potential areas of underperformance or potential investment opportunities.

Use the instructions below to maximize the value of this tool for your FX exposures.

Select your view

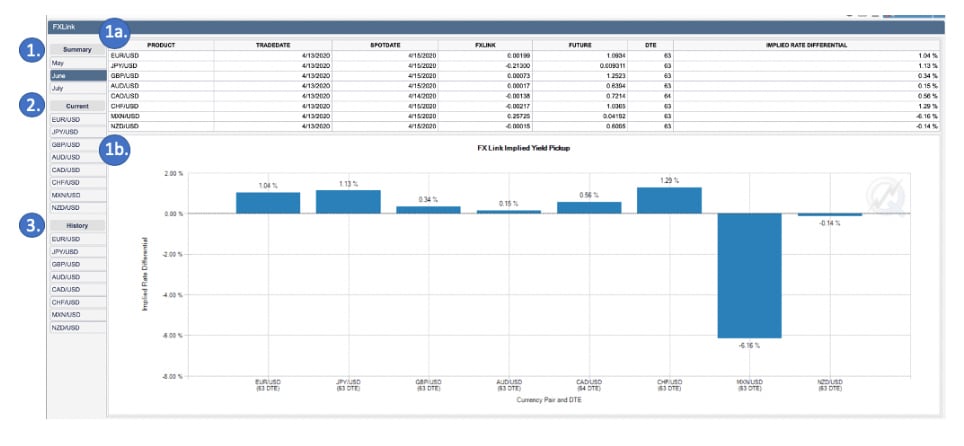

1. Summary view:

The summary view allows users to evaluate the current implied interest rate differential and corresponding FX Link and FX futures data for the first three available expiries, for all available pairs.

In this view, data can be selected and is depicted by contract expiry (see Figure 1).

- 1a. This table depicts the implied rate differential currently reflected in the market across all pairs in FX Link, and includes the relevant FX Link and FX futures market data.

- Product: The currency pair associated with the data depicted in a given row

- Tradedate: The business day associated with the market data presented in a given row

- Spotdate: The day when the FX Spot transaction is settled

- FX Link: The FX Link swap points; the basis between OTC FX spot and FX Futures for the specified Trade Date

- Future: The price of the outright FX Future

- DTE: T he number of days until the FX future expires

- Implied Rate Differential: The annualised implied rate of interest for US Dollars over the counter currency

- 1b. This bar chart illustrates the implied rate differential currently reflected in the market across all pairs in FX Link.

Figure 1: Summary view.

{kind=link}

2. Current Term Points:

The current view allows users to evaluate the current implied interest rate differential and a history of the rate differential at the point in time when the FX Link spread was approximately equivalent to a 3M, 2M, 1M swap, for the first 3 available expiries.

In this view, data can be selected and is depicted by currency pair (see Figure 2):

- 2a. This table depicts the current implied interest rate differential and history of the rate differential at standard OTC term points:

- i. The implied rate differential at the point in time when the FX Link spread was approximately equivalent to a 3M, 2M, 1M swap by expiry. Data will only be populated if the time to expiration has reached a 90, 60, or 30-day threshold.

- Term: Standard durations of OTC FX Swaps to provide anchor points of comparison to an FX Link Spread of a similar duration at a point in time

- Current: The most recent trade date associated with the market data presented in a given row

- Date: The day associated with the market data presented in a given row that corresponds to a standard term point or the most recent trade date

- DTE: The number of days until the FX future expires

- Rate: Is the implied interest rate differential - The implied rate of interest for US Dollars over the counter currency (non-US dollar currency for a given pair)

- ii. The implied rate differential currently reflected in the market by expiry.

- i. The implied rate differential at the point in time when the FX Link spread was approximately equivalent to a 3M, 2M, 1M swap by expiry. Data will only be populated if the time to expiration has reached a 90, 60, or 30-day threshold.

- 2b. This bar chart represents the available expires and the implied rate differential currently reflected in the market.

Figure 2: Current view.

{kind=link}

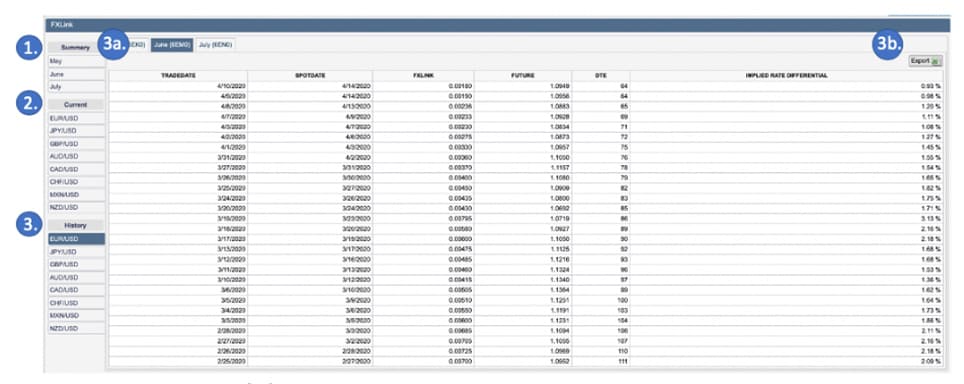

3. Historical Data:

The historical data view allows users to evaluate the progression of the implied interest rate differential and corresponding FX Link and FX Futures data for a given currency pair and the first three available expiries (see Figure 3):

- a. Selecting a given expiry will populate the table with the implied rate differential historically reflected in the market across all pairs in FX Link, including the relevant FX Link and FX Futures market data for the period of time when the contract was available.

- Product: The currency pair associated with the data depicted in a given row

- Tradedate: The business day associated with the market data presented in a given row

- Spotdate: The day when the FX Spot transaction is settled

- FX Link: The FX Link swap points; the basis between OTC FX spot and FX Futures for the specified Trade Date

- Future: The price of the outright FX Future

- DTE: T he number of days until the FX future expires

- Implied Rate Differential: The annualised implied rate of interest for US Dollars over the counter currency

- b. The export button allows users to extract this data into an excel file.

Figure 3: Historical data view.

{kind=link}

For more information

Visit The CME FX Swap Rate Monitor to start using the tool.

For questions about this tool, contact FXteam@cmegroup.com.