{kind=link}

Black Sea Wheat futures spurs new spread trading opportunities

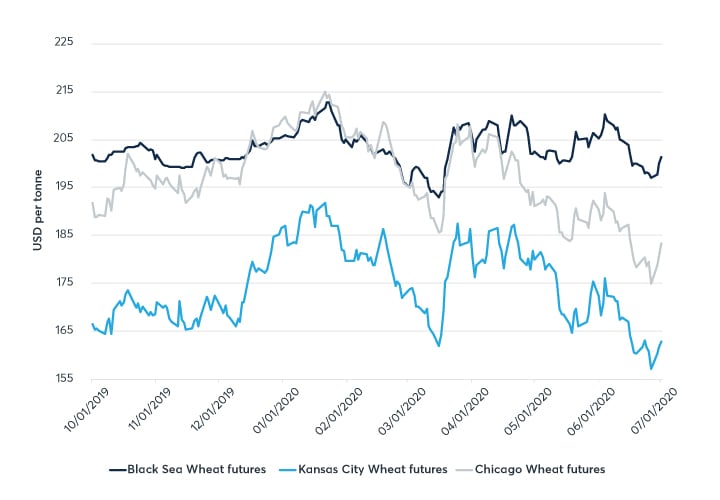

The Black Sea region has become the world’s largest wheat exporter, supplying high quality and competitively priced grain. The area has become the world’s price setter for milling wheat. Increased liquidity and participation in Black Sea Wheat futures has seen the contract gradually become the region’s pricing benchmark, sitting alongside the other CME Group benchmarks Chicago and Kansas City (KC) Wheat markets.

Chart 1: CME Group benchmark wheat futures prices

{kind=link}

Source: CME Group data

For US wheat 1 metric ton = 36.7437 bushels.

September 2020 contract month prices are shown

Global wheat spread volatility increases

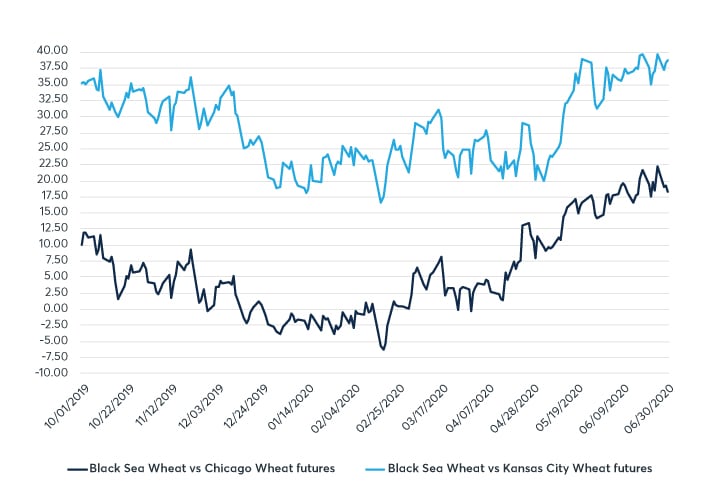

Wheat quality between the Black Sea and US hard red winter (HRW) wheat is broadly similar and they both compete on the world market. As such, firms are paying increasing attention to the futures arbitrage spread between the Black Sea and KC markets. As trading opportunities continue to expand along with the increasing liquidity in Black Sea Wheat futures, spread trading between Black Sea Wheat and KC Wheat and/or Chicago Wheat futures is expanding.

Black Sea Wheat futures September 2020 contract month premiums over KC Wheat futures have risen sharply in recent months, back to the highest levels seen since October 2019 of $37 per tonne. This is an increase of over 100% since February 2020. Similar price trends have been recorded against Chicago Wheat.

Chart 2: Black Sea Wheat premiums vs US wheat futures

{kind=link}

Source: CME Group data

For US wheat 1 metric ton = 36.7437 bushels.

September 2020 contract month prices shown

Trading the spread between Black Sea and KC Wheat

Firms who procure wheat from multiple origins can now trade the price spread between Black Sea and US wheat. When a firm believes that the spread is mispriced, the firm may choose to buy or sell the spread by taking a long or short position in the Black Sea and a corresponding opposite position in the KC and/or Chicago Wheat futures.

For example, a firm who is sourcing high quality wheat from multiple origins, including the Black Sea and the US. They closely watch the spread between both KC and Black Sea Wheat futures. They decide that the Black Sea Wheat September futures trading at close to $35 per tonne over KC represents an opportunity to sell the spread, believing that a more normalized value should be closer to $20 per tonne.

On the June 15, the trading house enters the futures spread trade and sells 100 lots (5,000 tonnes) of Black Sea Wheat futures for September delivery at a price of $200 per tonne and simultaneously buys 37 (~5,000 tonnes) lots of KC Wheat for September delivery at a price of $4.50 per bushel (equivalent to $165.35 per metric ton equivalent)1. Therefore, the firm has sold the spread at a price of $35 per ton ($200 - $165 per metric ton).

Selling an arbitrage spread Black Sea Wheat vs KC Wheat

| Timeline | Futures market (leg 1) | Futures market (leg 2) |

Spread value Black Sea Wheat – KC Wheat |

| June 15 | Sells 100 lots of September Black Sea Wheat futures at $200/mt | Buys 37 lots of September KC Wheat at a price of $4.50 per bushel ($160/mt) | +$35 |

| August 30 | Buys 100 lots of September Black Sea Wheat futures at $205/mt to close out the futures position | Sells September KC Wheat at a price of $5.03 per bushel ($185/mt) to close out the futures position | +$20 |

| Change | $5/mt loss | $0.53 per bushel ($20/mt) gain |

In this example, a trading firm has used the futures market to fix a spread value of $35 per tonne between Black Sea Wheat and KC HRW Wheat. In order to do this, the trader sold 100 lots of September 2020 Black Sea Wheat futures and bought 37 lots of KC HRW Wheat for September 2020, the resulting prices created the spread of $352. On closing out their futures position and after reflecting the changes in each of the contracts, the spread moved from $35 per tonne to $15 per tonne ‒ giving a gain on their futures position of $20 per tonne.

CME Group can offer potentially significant margin offsets for spread trades between Black Sea Wheat futures and both KC Wheat and Chicago Wheat futures. As of July 2, 2020, the margin offset between Black Sea Wheat futures and KC/Chicago Wheat futures is 50%3. To capture the growing trade interest in spread trades between the Black Sea and major US Wheat futures benchmarks, the exchange announced that effective July 13, 20204 block spread trades with new lower Chicago and KC Wheat minimum thresholds of 40 lots ‒ provided that each leg of the spread meets the minimum quantity.

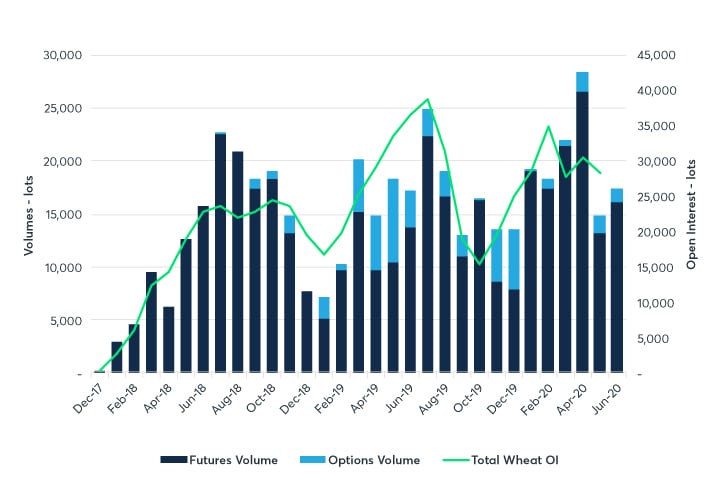

Black Sea Wheat futures and options liquidity

Launched in December 2017 as a price risk management tool for Black Sea Wheat, the futures and options contracts have seen quick adoption as a hedging tool and trading instrument by a wide range of physical market participants, including producers, exporters, trading houses, and processors in Europe, the U.S., Middle East, and Asia. The Black Sea futures settle to the price assessments provided by S&P Global Platts5.

Chart 3. shows the volume and open interest of the Black Sea Wheat futures and options by month since December 2017. Total contracts traded since launch through June 2020 is around 465,000 lots ‒ equivalent to 23.2 million tonnes of wheat.

Chart 3: Black Sea wheat futures and options volume by month

{kind=link}

Source: CME Group data

In the first six months of 2020, a total of 113,000 lots of Black Sea Wheat futures were traded ‒ a 78% increase from the same period a year earlier. This amounted to around 1,000 lots of Black Sea Wheat futures and options per day, or 50,000 metric tonnes (MT) of wheat traded daily. Open interest in Black Sea Wheat futures had increased to over 24,875 lots by end of May 2020 ‒ a rise of 40% from the same point a year ago.

For more information, please visit www.cmegroup.com/blacksea

Sources

- Conversion factor used is 1 metric ton = 36.7437 bushels https://grains.org/markets-tools-data/tools/converting-grain-units/

- The Black Sea wheat futures are financially settled whereas US wheat is physically settled therefore, exiting a futures position in US wheat ahead of expiry will avoid taking delivery against a futures position.

- CBOT Margin offsets (July 2 2020) https://www.cmegroup.com/clearing/margins/inters.html#exchange=CBT§or=AGRICULTURE&clearingCode=KCW&pageNumber=1

- CBOT Exchange notice – Block threshold changes effective July 2020 https://www.cmegroup.com/content/dam/cmegroup/notices/ser/2020/06/SER-8601.pdf

- S&P Global Platts Black Sea Wheat assessments https://www.spglobal.com/platts/en/our-methodology/price-assessments/agriculture/black-sea-grains-price-assessment