{kind=link}

Analysis of CME CF Bitcoin Reference Rate

1. Executive summary

Through the analysis that follows, it is possible to conclude that the BRR is representative of the underlying bitcoin spot market that it tracks, as by definition it represents the actual trades that have occurred within that market. By capturing the notional value of transactions, the BRR provides an accurate reference to the average spot price over the period.

The design choices within the methodology makes the BRR highly resistant against manipulation. The use of medians reduces the effect of outlier prices on one or more exchange. The volume-weighting of medians filters out high numbers of small trades that may otherwise dominate a non-volume weighted median. The use of 12 non-weighted partitions assures that price information is sourced equally over the entire observation period. Influencing the BRR would therefore require trading activity during multiple partitions on several exchanges over an extended period, which would prove a costly and an operationally intensive undertaking.

There is sufficiency of data inputs for the calculation, and the data is provided under licencing arrangements with each exchange, who in turn meet strict entry criteria. The exchanges that are included within the calculation represent the underlying spot market and the trading on these venues account on average for over 50% of total BTC:USD volume.

There is liquidity in the BRR, in the 1 year to March 2019, over USD 3 billion worth of bitcoin trades were executed, over 1.8 million trades were included in the BRR based on a total of 607,000 bitcoins traded, this shows credibility in the computation of the BRR. The BRR is replicable, as a trader can replicate the BRR by trading bitcoin on any of the constituent exchange(s) where the price is trading close to the median. The ability to replicate the BRR assures that the index appropriately tracks the price of bitcoin at the constituent exchanges.

To maintain its integrity, the index’s development relied on recognized best principles for financial benchmarks. Furthermore, an expert oversight committee is responsible for overseeing the scope of the index by approving and regularly reviewing the calculation methodology, practice, standards and definition of the reference rate to ensure it remains relevant and robust. A clear policy has also been established against which any hard fork can be evaluated to determine its significance, as well as a set of pre-defined criteria to govern the course of action to be taken should a hard fork occur.

1.1 Qualitative Factors in BRR Methodology Construction

The below factors have been addressed by the BRR methodology and associated frameworks:

- Number of Constituent Exchanges

- Coherent Inclusion Criteria

- Regular review and update of Exchanges

- Resistance to manipulation

- Type of Methodology used for calculation

- Transparency of methodology

- Replicability of methodology

- Adherence to on regulatory guidelines

- Expert oversight

- Independent back testing

- Practise Standards

- Conflicts of interests Policy

- Executed data licence agreements

2. Bitcoin Reference Rate

The CME CF Bitcoin Reference Rate (BRR) was introduced on November 14, 2016 to provide market participants with a reliable credible source for the price of bitcoin and intended to facilitate the creation of financial products based on bitcoin. The BRR is the underlying rate used to determine the final settlement of the CME Bitcoin Futures Contracts. It also serves as a reference rate in the settlement of financial derivatives based on the bitcoin price, and in the net asset value (NAV) calculation of funds. Several criteria can be assessed to satisfy whether it is a robust benchmark, including the 8 distinct tests of: Relevance, Manipulation resistance, Verifiability, Replicability, Timeliness, Stability and Parsimony. This paper will seek to address these tests.

3. BRR Methodology Overview

The CME CF Bitcoin Reference Rate (BRR) is a daily reference rate of the U.S. Dollar price of one bitcoin. It is the aggregation of executed trade flow of major bitcoin spot exchanges during a specific one-hour calculation window. All relevant transactions are added to a joint list, recording the trade price and size for each transaction. This one-hour window is then partitioned into twelve, five-minute intervals. For each partition, the volume-weighted median trade price is calculated from the trade prices and sizes of all relevant transactions, i.e. across all constituent exchanges. The BRR is then given by the equally-weighted average of the volume-weighted medians of all partitions. Calculation rules are geared toward a maximum of transparency and replicability in the underlying spot markets.

4. Digital Asset Landscape

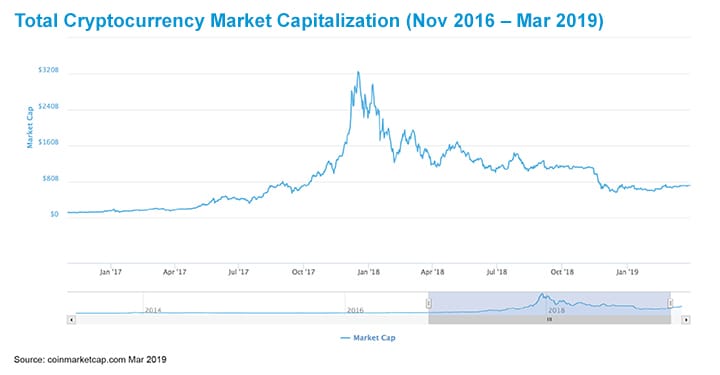

The digital asset market capitalization has grown substantially relative to 2016 and currently stands at c.$175B (Mar 2019). The number of cryptocurrencies is now a staggering 2100+. In 2016, when CME launched its first cryptocurrency products on bitcoin, the total cryptocurrency market capitalization was c.$11bn.

https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/analysis-of-cme-cf-bitcoin-reference-rate-fig04a.jpg https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/2019/analysis-of-cme-cf-bitcoin-reference-rate-fig04b.jpg

{kind=link}

{kind=link}

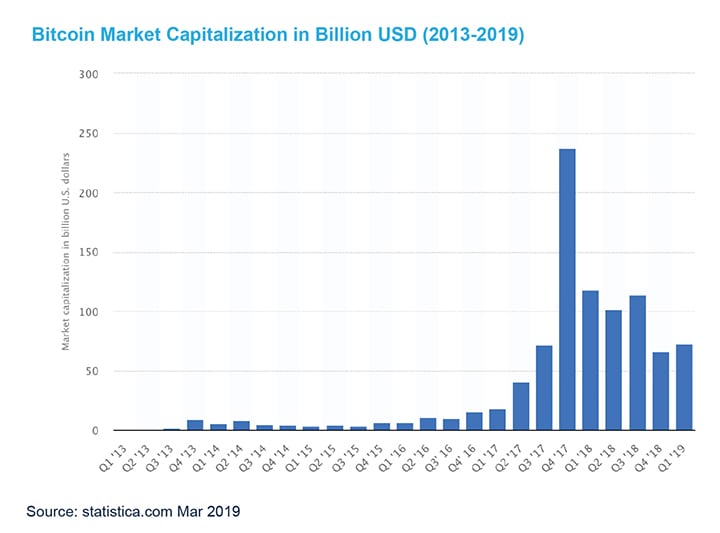

4.1 Bitcoin Market Capitalization

{kind=link}

The graph represents the market capitalization of Bitcoin, from Q1 2013 to Q1 2019.

Market capitalization is calculated by multiplying the total number of bitcoins in circulation by the bitcoin price.

At its height, bitcoin’s market capitalization increased to approximately $238bn in the Q4 2017. For Q1 2019, bitcoin’s average market cap currently stands at approximately $80bn.

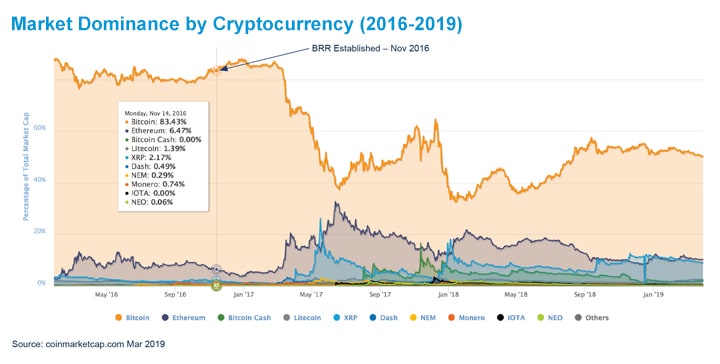

4.2 Bitcoin Dominance

Currently bitcoin’s dominance - the demand for bitcoin compared to other cryptocurrencies - stands between 50- 55%. Dominance was at its lowest during the bull run of January 2018, when most other cryptocurrency altcoins were booming. Bitcoin’s popularity usually rises during bearish times and there are a few explanations for this.

Firstly, it is the one high-profile cryptocurrency everyone has heard about and is therefore a natural choice for novices. There is high correlation between the price of bitcoin and altcoins; they have always been strongly coupled. Secondly, with its relatively low volatility compared to other cryptocurrencies, bitcoin can be considered a safe haven in bear markets. After all, it has only retracted 75%1 from its all-time high, whereas the majority of altcoins are down 80-95% from their peaks. Thirdly, a cryptocurrency’s price movement is primarily a function of its liquidity. Bitcoin has higher volume and market cap than any other coin and its thicker order books mean smaller movements. Traders who employ risk management techniques often move funds into bitcoin when they believe the market is going down and then back into altcoins when arrows point upwards again as alts seem to rise higher and fall harder. This also makes bitcoin a good option for risk averse investors who are uncomfortable holding positions in altcoins but don’t want to exit the markets. Adding to this, bitcoin is still the only universal on/off-ramp to the crypto world. Whichever coin or token you want to buy, the simplest first step is usually buying bitcoin with fiat and then trading the bitcoin for another crypto asset.

{kind=link}

So, with bitcoin involved in most of the market action, shouldn’t its dominance be even higher? We don’t have to go further back than to March 2017 to find it at 85%. Fast forward to June the same year and interest had shifted to ether and the other hot ICOs, and so bitcoins dominance drops to 40%. Back to present-day, the 2100 or so altcoins currently listed on CoinMarketCap, has heavily diluted bitcoin’s market share.

More than 1,600 of the altcoins have a market cap between $10 million and zero. But they have no liquidity, no trading volumes. There are hundreds of coins out there like these, taking share from bitcoin just by existing, even though they are in reality dead. This tells us there are now too many altcoins in the market for bitcoin’s dominance to rise much further. In 2016, when CME launched its first cryptocurrency products, bitcoin’s dominance stood at 83% of total market cap, followed by ether at 6%. Bitcoin remains the dominant cryptocurrency despite the addition of numerous altcoins since Nov 2016, given Bitcoin’s continued market dominance, the BRR remains an important index.

4.3 Bitcoin Trading

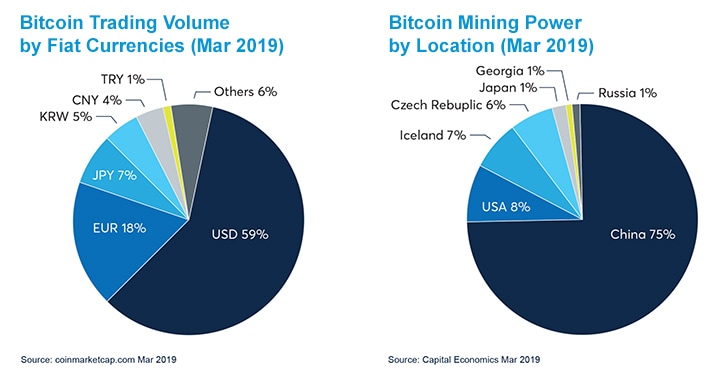

In terms of bitcoin trading against fiat currency, about 60% of bitcoin-to-fiat trading volume is currently against the U.S. Dollar. Euro to BTC trading takes second place with 18% and the Japanese Yen is in third with 7%. It is interesting to see countries with some political instability feature, albeit small, – such as BTC vs Turkish Lira or BTC vs Venezuelan Dollar, and other South American countries as well as some African currencies.

Generally, through 2018 we have seen a notable shift towards crypto-crypto trading through the use of stable coins and other crypto-pairs. Back in 2016, when the BRR was established, USD accounted for 54% of bitcoin trading, Yen came in 2nd place and accounted for over 12%, the Korean Won for approximately 11%, and smaller fiat pairs account for the remaining portion. This liquidity “location” by currency is in stark contrast to the location of mining (hashpower) where access to cheap electricity is paramount to the bitcoin “proof of work” function.

The BRR remains relevant as a measure of BTC:USD trading, given the majority of bitcoin fiat trading occurs against USD.

{kind=link}

5. Analysis of the BRR

5.1 Evolution of Price

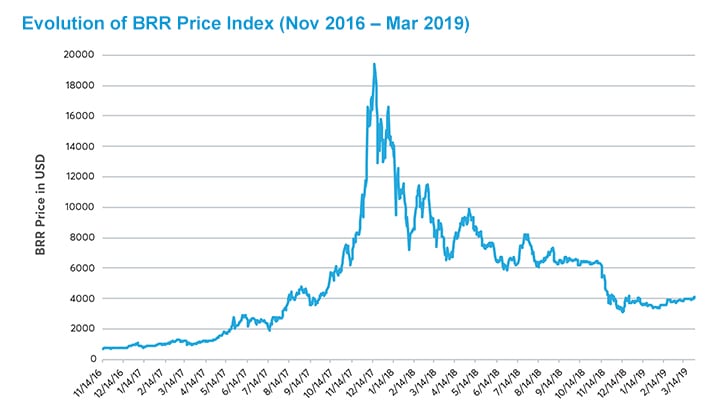

The chart below best represents the evolution of price over the period. At the inception of the BRR, the price of bitcoin was around $700. On January 1, 2017 the cryptocurrency’s value to crossed $1,000 for the first time. The year to follow would bring unprecedented interest – particularly from the finance industry – that some may not have imagined possible just 12 months prior. Some salient points of note for the evolution of the price over the year follow. Firstly, in January 2017, the Peoples Bank of China (PBOC), took a move to tighten its oversight of the country’s then-dominant bitcoin exchanges; and ultimately closed fiat trading.

{kind=link}

Investors Cameron and Tyler Winklevoss first filed to launch a bitcoin exchange-traded fund back in 2013, setting the stage for a multi-year journey that led to the March 2017 rejection by the U.S. Securities and Exchange Commission (SEC). On the news, the market dropped by nearly 30% that day. April saw Japan recognize bitcoin as a legal method of payment. The country’s legislature passed a law, after months of debate, that led bitcoin exchanges to comply with anti-money laundering rules/information about your client, and classified bitcoin as a kind of prepaid payment instrument. As May drew to a close, the price of bitcoin climbed above $2,000 for the first time and surpassed $3,000 just weeks later. At the same time, those price milestones were often accompanied by subsequent turbulence, including a drop of $300 within one hour.

It was then a summer of bulls for bitcoin, where between May and September new all-time highs were recorded almost weekly. The summer also saw significant activity around initial coin offerings. On August 1st, 2018 Bitcoin forked, leading to the creation of Bitcoin Cash (BCH). Wall Street analysts entered the bitcoin price-watching game. By the first week of September, the price of bitcoin exceeded $5,000 for the first time – only to drop by hundreds of dollars with a reversal of the late summer’s gains, with the cryptocurrency’s price falling past $3,500 on September 15th.

By mid-October, the September disorder had been forgotten and the price of bitcoin was once again above $5,000.

Despite a global crackdown on unregulated ICOs beginning to take shape, the price of bitcoin was largely buoyed by a bullish sentiment which would set the stage for some incredible moves in store for November and December.

For all the regulatory rumblings and forks away from the bitcoin network, the cryptocurrency’s price largely continued its upward trajectory, culminating with the BRR Price Index’s all-time high of $19,448.21 on Dec. 17, 2017. Some spot markets, in fact, reported that the $20k barrier was broken on that day. To date, Dec 17, 2017 was the all-time high price for bitcoin. December also saw the introduction of 2 bitcoin futures contracts, listed on CBOE and CME, 2 regulated exchanges, affording investors the ability to manage their bitcoin-related risk and/or to access exposure.

The close encounter with $20,000 was followed just days later by a 30% drop that shaved billions of dollars off of the total cryptocurrency market capitalization. It was one of the biggest market corrections seen to date, sending bitcoin’s price tumbling down to $16,000, then $11,000. On Feb. 5th, 2018, bitcoin price dropped 50% in 16 days, falling to below $7,000. From there it moved steadily down to the $4k mark. The price band for much of the 2nd half of 2018 was between the $6,000-8,000 mark.

Given the cost of mining bitcoin can be thought of as a function of price, many experts feel that the current levels seen in Q1 2019, of around the $3000-$4000 mark are both more realistic and sustainable. Regardless, the BRR has captured all market price action.

5.2 Price Volatility

In 2017, — the year that brought bitcoin close to $20,000 — the market was known for its intraday volatility. Late 2017 into early 2018 saw bitcoin volatility hit peak levels, with intraday price swings above 10% becoming normal. In addition, the price differences between exchanges trading crypto reached as high as $1,000 during this period.

Whilst intraday price movements have been significant, daily price volatility of the BRR has stabilized and reduced drastically and is comparable to some equity markets.

6. Exchange Selection

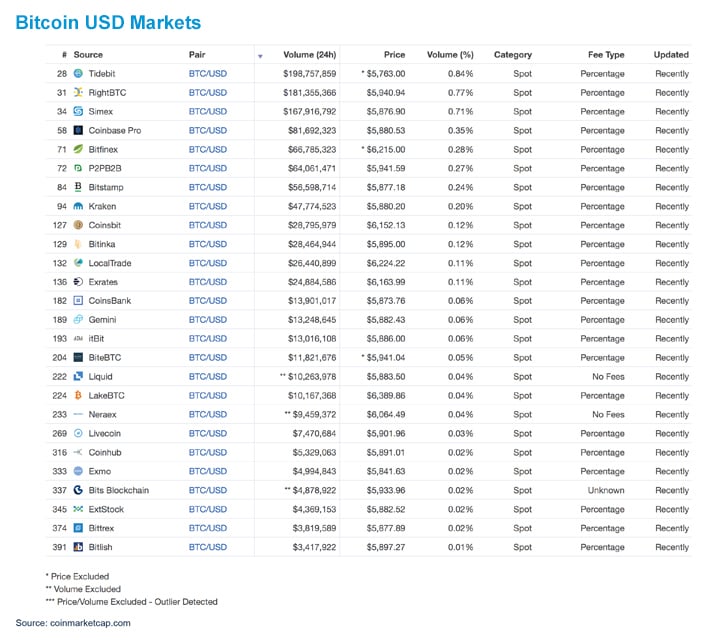

Looking at CoinMarketCap - the most widely cited source for bitcoin volume - more than 400 markets exist for bitcoin trading, offered by over 100 different exchanges based all around the world. If we narrow this universe down to those offering only BTC:USD, then we see the exchange universe shrink to around 30 global exchanges.

{kind=link}

Despite its widespread use, CoinMarketCap includes a large amount of fake and/or non-economic trading volume, thereby giving a fundamentally mistaken impression of the true size and nature of the bitcoin market. The first step in the creation of any pricing index needed to be the establishment of a universe of relevant exchanges that employ practices to mitigate concerns around market manipulation, liquidity, pricing, and arbitrage.

From the above we can see leading data aggregators show prices on different exchanges separated by hundreds of dollars. Trading frictions and differing KYC/AML practices at exchanges, the exchange’s banking relationships, and transaction costs have an impact on trading prices reported by each exchange. Traded volume also, could not be the only criteria for inclusion given the fast pace of the landscape.

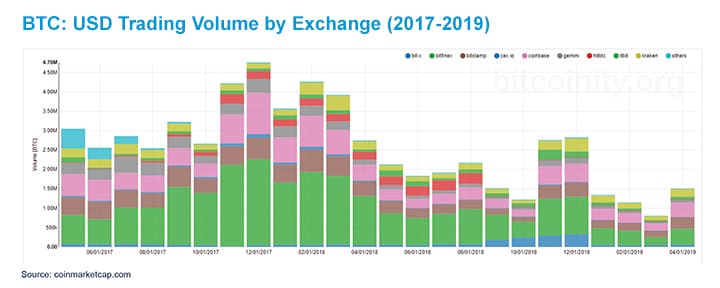

To understand the universe of exchanges that offer BTC:USD trading, it is necessary to see how different exchanges have grown, shrunk or even ceased to exist over time. The chart below shows this evolution.

{kind=link}

6.1 Eligibility Criteria

The BRR was designed to have limited susceptibility to temporary price swings and outlier prices. As such, the BRR has eligibility criteria for Constituent Exchanges (the exchanges from where trade flows are collated) which form the basis for participating in the reference rate calculation.

There is criteria for an exchange to charge a fee for trading, which eliminates wash trading to increase volumes. The BRR only includes trades executed between BTC and USD. It does not use alternate currency pairs or crypto to crypto trading, (in place of BTC:USD) and apply conversion calculations, nor does it include USDT or other stable coin transactions into the BTC:USD orderbook. The venue’s bitcoin vs. US dollar spot trading volume must meet the minimum thresholds as detailed in the methodology. Currently 3% relative contribution over 2 consecutive quarters.

The criteria provide that exchanges deliver transparent and consistent trade data and order data available via an API with sufficient reliability, detail and timeliness.

Furthermore, the venue are expected to maintain fair and transparent market conditions to impede illegal, unfair or manipulative trading practices, not place undue barriers to entry and comply with applicable law and regulation including, capital markets regulations, money transmission regulations, client money custody regulations, know-your-client (KYC) regulations and anti-money-laundering (AML) regulations.

There is also the criterion for the venue to cooperate with inquiries and investigations of regulators and the administrator and execute data sharing agreements.

Given that exchanges are third-party organizations operating in a volatile and competitive marketplace, the constituent exchange mix and index methodology for the BRR is regularly reviewed by the index administrator to ensure the quality and relevance of its indices. Establishing a clear eligibility framework makes the BRR clear and transparent.

6.2 Qualitative Factors in BRR Methodology Construction

Several entities provide a daily bitcoin price index. Some important points to note are some indices are based on ‘all of the available market’ from publicly available API’s without a data license. Whilst this may bring a holistic approach, it is fraught with challenges in that the exchanges may not be liquid by volume or order book depth, and they may be showing stale prices. Some may operate strict KYC and AML checks on their clients whereas others may not. This may in turn affect the bitcoin price shown on the respective exchange.

6.3 Exchange Universe

{kind=link}

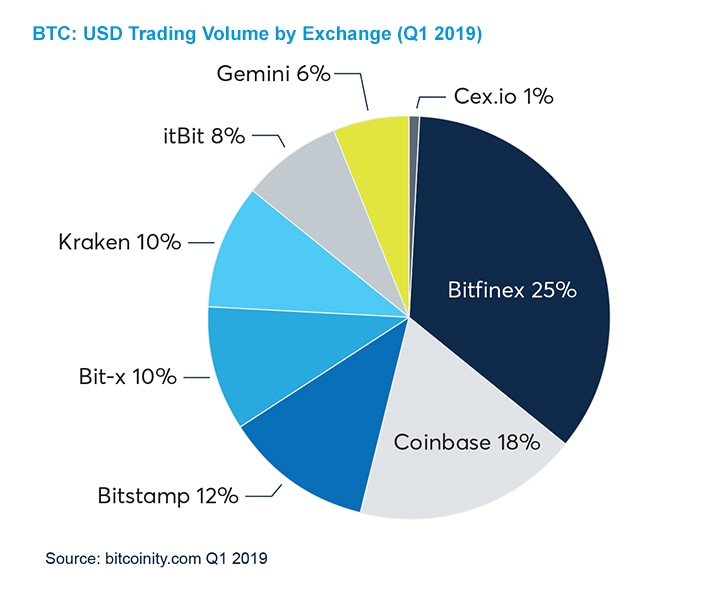

Taking guidance from the Eligibility Criteria only a few major exchanges dominate in BTC:USD trading, and liquidity is concentrated in a small number of exchanges.

In line with the eligibility criteria which takes into consideration quantitative and qualitative factors, 4 exchanges currently contribute data to the BRR; Bitstamp, Coinbase, Itbit and Kraken.

Given that these are the 4 exchanges have sizeable trading volume they make the BRR reflective of the underlying spot market.

The exchange universe is regularly reviewed by the administrator to ensure that the relevant exchanges contribute to the BRR index.

6.4 Trading Volume Represented by the BRR

Based on worldwide BTC:USD trading volume the BRR continues to be representative of the bitcoin exchange universe. For the Q1 2019, the exchanges that contribute to the BRR capture 57% of total BTC:USD traded volume.

{kind=link}

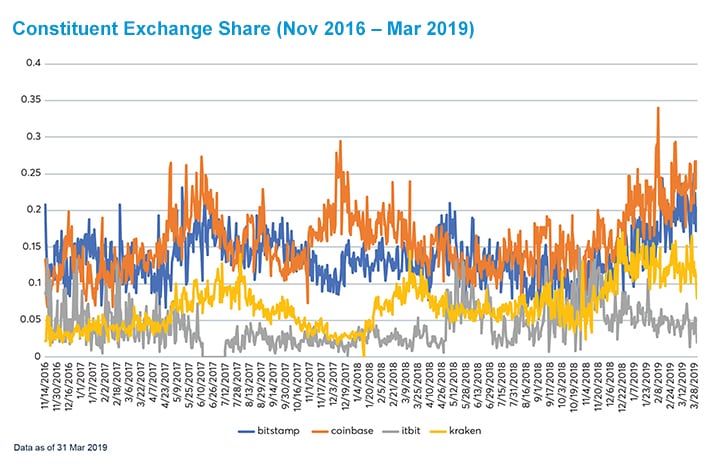

6.5 Constituent Exchange Contribution over Time

Over recent months, the dominance of any one exchange in the BRR calculation has reduced. Looking at the 4 exchanges currently included in the BRR for the timeframe of 14 Nov 2016 to 31 Mar 2019, we see a continual shift between the different exchanges volumes growing and shrinking in comparison to the others. This indicates that the exchanges that are included in the calculation are still very relevant. They all contribute a decent amount to overall bitcoin volume and there is no over dominance by any one exchange.

{kind=link}

6.6 Inclusion of Stable Coins and FX

One key area to note is that some bitcoin indices will include non-USD order books in their computed USD bitcoin prices, e.g. they take the non-USD trades and use an FX rate to convert to USD for inclusion. The BRR does not consider trading in other currency fiat pairs and apply an USD FX. Some indices view Tether (UDST) as a proxy for USD and combine both other books when calculating a price. The BRR also does not include coins that are pegged to a fiat currency, for example tether (USDT) or other crypto to BTC transactions, for example BTC:ETH.

6.7 Exclusion of Exchanges that Offer Trans-Fee Mining

Looking at the volumes reported by CoinMarketCap, some exchanges are achieving extraordinary trading results. A relatively new business model known as transaction fee, (trans-fee) mining has emerged in recent months. Whilst CoinMarketCap does a good job of collating data and determining the exchanges fee model, we find that some exchanges that engage in trans-fee mining are not categorised as such and can be included in the reported numbers.

With a conventional cryptocurrency exchange, a maker and taker fee is levied on each side of the trade. Ordinarily, this fee is deducted at the point of the trade being executed and collected by the exchange in the form of BTC or fiat.

Transaction fees are the primary way by which exchanges make their money, it also serves as a very important control mechanism. Charging a fee to trade, mitigates the risk of damaging market behaviour and manipulation. Transaction- fee mining exchanges take a markedly different approach, by handing all the fees back to traders in the form of a native token. In fact, during promotional periods – typically when launching the exchange – these platforms might even offer a rebate of greater than 100%. In other words, traders are technically profiting, in the form of native tokens, for each trade they made.

Cryptocurrency market aggregators such as CoinMarketCap have long excluded zero-fee exchanges, as their data skews the rankings. But because exchanges like Bitforex and Fcoin technically charge fees, albeit with all tokens collected from this disbursed to the community, they can leap to the top of the charts, and in doing so, gain inbound referrals, driving up volume with potential dubious trades. As such, exchanges exhibiting this behaviour are not included in the BRR calculation. By excluding these types of exchanges and those without a banking relationship, we are left with the list of exchanges as shown in Section 6.3

7. Choice of Reference Rate Observation Window

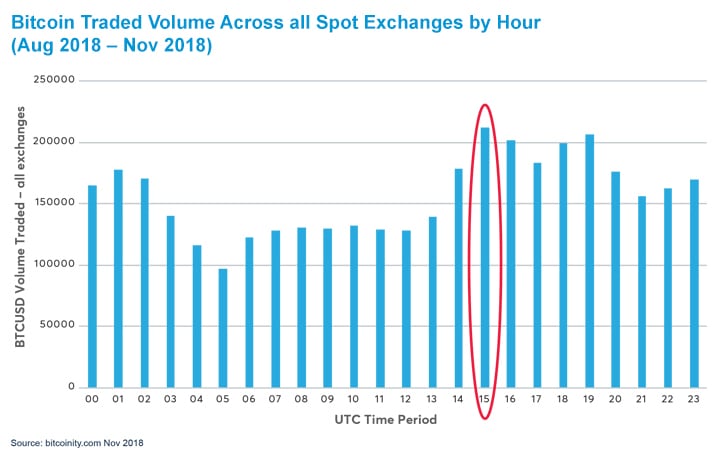

To determine the observation window, a timeframe needed to be identified where the most volume was traded on a global basis. This window needed to be wide enough to allow for a sufficient number of trades to be included but narrow enough such that the calculated rate is still relevant and representative of the market. Looking at the number and volume of transactions in the BTC:USD pair, on a global basis, including all spot exchanges, the 15:00 – 16:00 time period sees the greatest number of transactions.

The below chart shows bitcoin volume across all spot exchanges, by hour, for the three-month period 1 Aug 2018 – 1 Nov 2018. The 3-4pm UTC time period continues to see the most volume and continues to be the calculation window for the BRR, with each rate being calculated at the end of the calculation period and published shortly after 4pm.

{kind=link}

8. BRR Methodology Deep-dive

8.1 Methodology: Partitions

The BRR is calculated as the equally-weighted average of the intermediate calculation steps for 12 5-minute partitions. Having 12 partitions of 5 minutes immunizes the reference rate to a high degree against price anomalies. A single large trade or cluster of trades occurring in any one partition will only have a limited effect on BRR. To have any effect, multiple, large, executed transactions will need to occur on all constituent exchanges, in all 12 partitions – a costly process to achieve.

8.2 Methodology: Volume Weighted Medians

A volume-weighted median differs from a standard median in that a weighting factor, in this case trade size, is factored into the calculation.

The BRR is designed to be representative of the underlying crypto spot market. To ensure it is undisturbed by the uptime and engine stability issues at spot exchanges, a median based index was a conscious design choice.

Many indexes use variants of volume weighted prices (VWAP) to compute an index. While VWAP is a reasonable choice for mature markets, it introduces instability in nascent markets, such as crypto.

The use of medians to calculate the weighted median trade price for each partition (as opposed to averages) greatly reduces the BRR susceptibility to price extremes on one or more Constituent Exchanges. A median automatically discards extremes by its very definition and any extreme behaviour or instability is automatically eliminated.

Trading is driven to some extent by automated algorithms that may execute a high number of small trades. The use of volume-weighted medians to calculate the weighted median trade price for each partition (as opposed to simple medians) assures that BRR appropriately reflect large trades and that whether an order is executed in parts or in full has no effect on calculation results.

8.3 Methodology: Exchange Failures

Within the crypto space, exchanges can go down for extended periods or be offline for maintenance without notice. Often exchanges with the heaviest volumes go down for some time and stay down. Spot prices have historically varied considerably across trading venues, particularly during times of high volatility. Exchanges can also have chaotic movements and bad prints which can cause a volume weighted index to swing wildly, with unnecessary instability in the resulting index price.

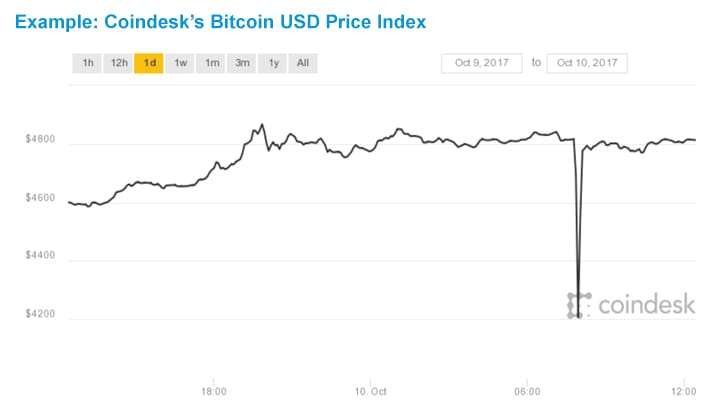

{kind=link}

As can be seen in the graph, CoinDesk’s Bitcoin index showed a sudden dip of more than $600 early Tuesday 10th October 2017. 10 minutes later, CoinDesk reported the currency rebounded. CoinDesk averages out its price index from 4 different exchanges – Bitstamp, Coinbase, itBit, OKCoin. However; none of the contributing exchanges showed a flash crash at the same time. The ‘crash’ was not reported by other bitcoin indexes.

A technical glitch may have occurred.

8.4 Methodology: Replication

Partitions are equally-weighted (as opposed to volume-weighted) to facilitate replication of BRR through trading on Constituent Exchanges. Assuming K partitions, a trader aiming to transact Y units of Bitcoin at the BRR can do so with little tracking error by transacting Y/K units of Bitcoin during each partition.

To test that the BRR is replicable to a small tracking error, we simulated the action to execute 10 BTC within the 60-minute BRR observation window by following the below method:

- Assume X (10) bitcoins need to be sold

- Divide 10 BTC by number of seconds (3600) within the calculation window, and execute trades to sell 0.002778 BTC each second

- The strategy trades on the same N (4) exchanges that are part of the index, during the 3600 seconds calculation period.

- The strategy sells X / N / 3600 bitcoins on each exchange every second- to estimate the strategy’s trade prices on each exchange

- If during a specific second, one or more trades have occurred on an exchange, the price of the first such trades is the executed price

- If there is no trade the most recent trade price that has occurred on that exchange would be the executed price up to max. 5 mins (partition length)

- If no last trade price is available within the 5-minute window the exchange is dropped and executions are from the remaining exchanges for that second.

We assume that:

- That the execution of 10 BTC divided up into 3600 orders of 0.002778 BTC will not move the market

- Average Daily Volume captured by CME CF BRR is circa 2000 BTC since November 16, 2017, 10 BTC = 0.5% of the average observed volume during the BRR 60-minute window

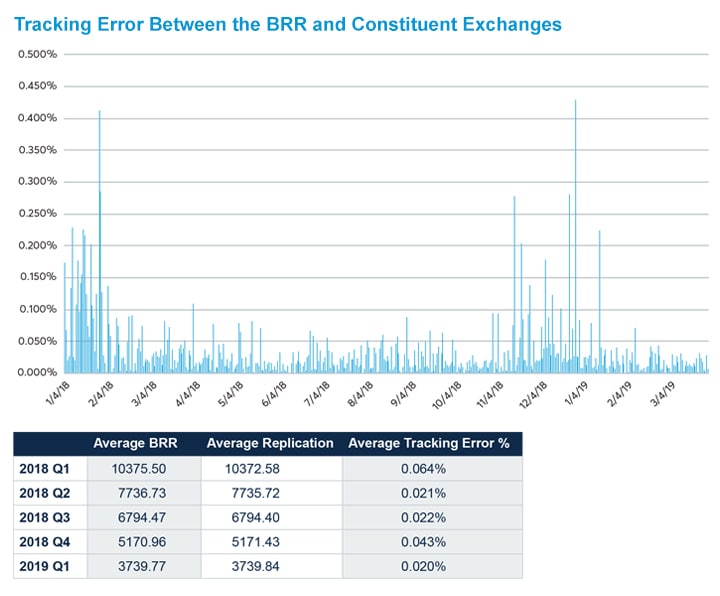

For the period Jan 2018 – Mar 2019, the average tracking error was 0.033%. Giving traders the confidence to use the BRR alongside their trading on constituent exchanges.

{kind=link}

9. BRR Window Analysis

{kind=link}

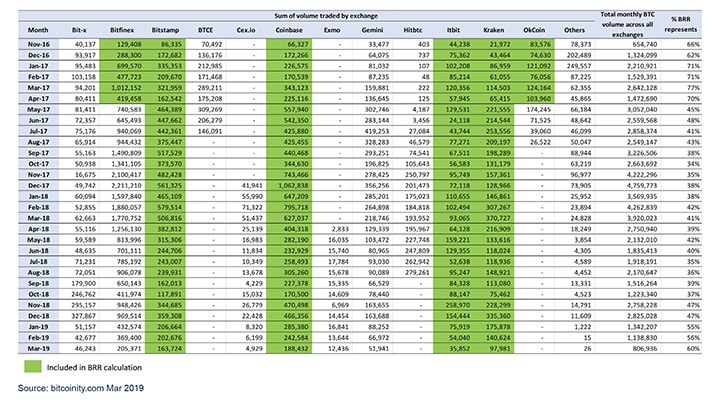

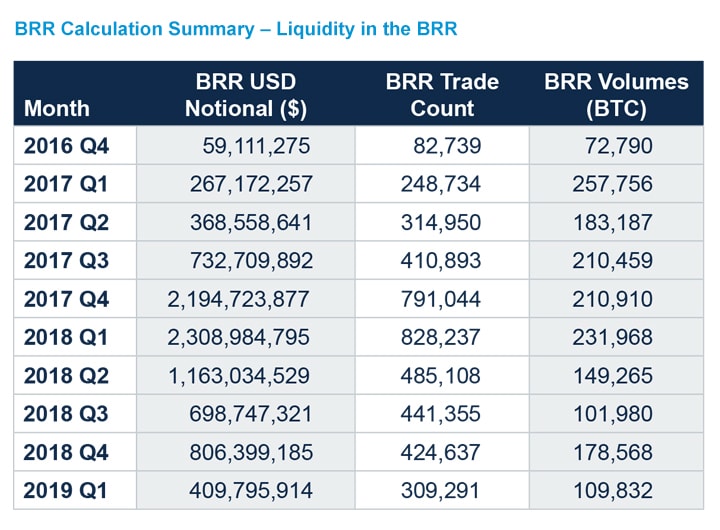

The table here shows the notional value and trade count of trades that were executed monthly on the Constituent Exchanges, within the 1-hour observation period and went into the calculation of the BRR.

In the 1 year to March 2019, over USD 3 billion of trades were executed, over 1.8 million trades were included in the BRR based on a total of 607,000 bitcoins traded, this shows robustness in the computation of the BRR.

The BRR has successfully been calculated every day since the 14th of November 2016, without any gaps, demonstrating the reliability of the BRR.

9.1 Window Analysis

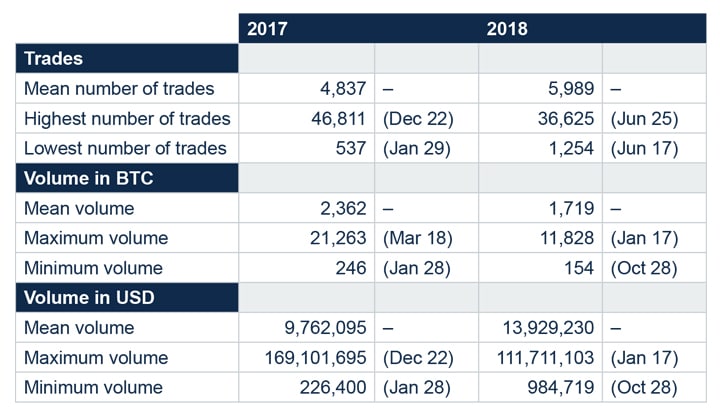

Here we see the number of trades and volume of transactions both in bitcoin, and USD that go through the BRR calculation window; 3-4pm London Time.

{kind=link}

9.2 Methodology: Exclusions Analysis

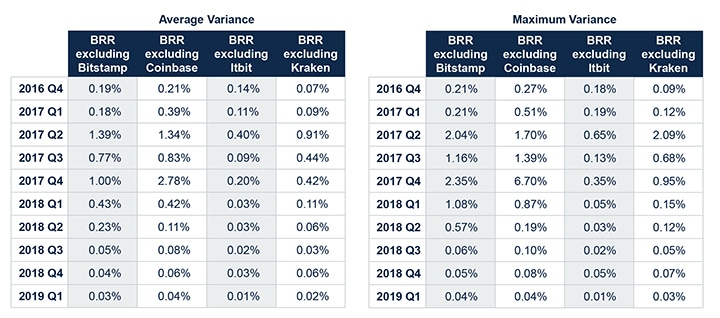

Currently the BRR has 4 constituent exchanges. The methodology was designed to remove the reliance on any single contributing exchange, where delayed or missing data from an exchange does not cause a calculation failure.

Based on the 2 years of data that is now available, analysis was carried out on the price effect on the BRR of excluding each of the constituent exchanges in the daily calculation. To achieve this, the deviation was calculated by computing the BRR but excluding each of the 4 exchanges in turn, to determine the effect that each exchange has on the overall price.

For the period 14 Nov 2016 – 31 Mar 2019, the below results were attained for the average and maximum variance per quarter.

{kind=link}

This demonstrates that there is no over dominance by any one of the 4 exchanges on the concluding BRR price. The effect of any single exchange on the BRR is minimal. It also demonstrates, no over reliance on any one exchange. Hence, should an exchange be excluded due to lack of data or any other reason, it will not have material effect on the calculated rate.

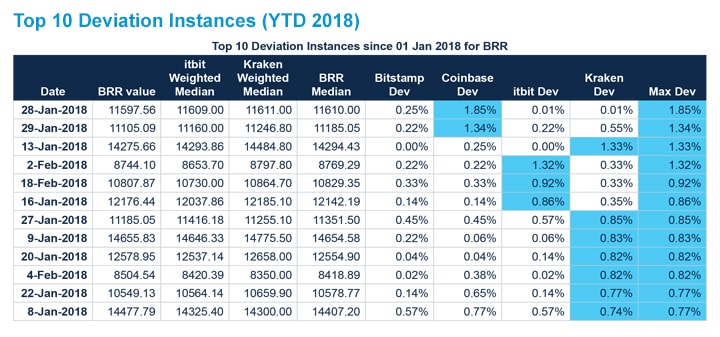

9.3 BRR Methodology: Deviation Analysis

In accordance with the BRR methodology, if for any constituent exchange the absolute percentage deviation of the volume- weighted median trade price, from the median of the volume-weighted median trade prices of all Constituent Exchanges exceeds 15%, all relevant transactions of that constituent exchange are flagged as potentially erroneous and are disregarded in the calculation of the BRR for that calculation day.

The below show the 10 days with the greatest deviation instances since 01 Jan 2018. The maximum deviation of any exchange has been 1.85%. The deviation test is certainly important in the robust calculation of the BRR. Given such low deviation of any one exchange to the other 3, demonstrates the quality of the exchanges chosen. Should any one exchange print a series of bad prices, the deviation between itself and the other exchanges would act as an indicator. The threshold is kept sufficiently wide to allow for movements in fast markets and regularly reviewed.

{kind=link}

10. BRR Methodology: Quality of Data Inputs

To ensure a robust index, the methodology has rules around:

- Delayed data and missing data

- Erroneous Data

- Potentially Erroneous Data

- Calculation failure

This includes automated screening for erroneous data for non-numeric or non-positive trade price or trade size and un-parseable data. The BRR calculations has never required the complete removal of an exchange for erroneous or potentially erroneous data.

Automated screening for each Constituent Exchange individually is carried out. Checks are made to ensure that the volume-weighted median trade price for one exchange does not deviate too widely from the median of the volume- weighted median trade prices of all Constituent Exchanges. If this deviation exceeds 15%, then all data from the particular exchange is discarded from the BRR calculation.

If the BRR cannot be calculated for a given Calculation Day, for instance because there are no Relevant Transaction on any Constituent Exchange or that the transactions cannot be retrieved by the Calculation Agent, or all Relevant Transactions are flagged as erroneous or potentially erroneous, or there is any other reason or circumstance that prevents the orderly calculation of the BRR, then the BRR for that Calculation Day is given by the BRR published on the previous Calculation Day. The occurrence of any BRR calculation failure is reported to the oversight committee. There has never been a calculation failure in the BRR.

The existence of a fully established validation framework as well as a back-up policy in case of calculation failure, makes this a robust reference point, suitable for use in a variety of derived financial products. Since its inception on 14 November 2016, the BRR has been calculated and published every day, including weekends and bank holidays just after 4pm London time.

11. Hard Fork Policy

Virtual currencies, including Bitcoin, are built upon widely agreed “consensus rules”, used to evaluate whether transactions on their respective blockchains are valid. Any change to these consensus rules must be implemented by all parties for the system to function.

When a group of entities make a change to the consensus rules, or resist making a change implemented by another group, a hard fork may occur, resulting in the creation of a new token. The BRR has a clear policy under which the administrator will evaluate any hard fork to determine its significance, as well as a set of pre-defined criteria to govern the course of action to be taken should a hard fork occur.

The BRR Hard Fork Policy defines that a hard fork has occurred if:

- two or more diverging blockchains are in existence post-fork that share the same pre-fork blockchain,

- the tokens on the post-fork chains are non-fungible across chains, and

- the respective blockchains are actively mined such that transactions can be processed at reasonable speed.

11.1 Hard Fork Determination Criteria

For the purpose of the BRR calculation, a new token will be deemed significant if it satisfies the following four market- based criteria for at least two of the Observation Period’s seven days: (a) The New Token Pair must be available to trade on at least 2 constituent exchanges, (b) There must be at least 100 trades in the New Token Pair across all constituent exchanges, (c) The New Token Pair trades at a price greater than or equal to 10% of the combined Price of both the Original Token Pair and the New Token Pair and (d) The Trading Volume of the New Token Pair must be greater than or equal to 10% of the combined Trading Volume of the Original Token Pair and the New Token Pair.

If a New Token is deemed significant, the BRR Administrator will initiate the calculation and dissemination of an index on the new token Pair. If a new token is not deemed significant, such step is at the Administrator’s discretion. The BRR will continue to track the Original Token Pair.

12. Data Licencing Arrangements

To ensure the continuous, uninterrupted publication of the BRR certain measures have been put in place:

- Crypto Facilities has licence agreements in place with each constituent exchange allowing the right to use the data in the creation of an index

- There is regular open dialogue with each of the constituent exchanges

This will be a comfort to the end-users of the BRR. The BRR is also made available for use in derived data works via the execution of a Derived Data Licence.

13. Governance

The BRR calculation ensures tradability and replicability in the underlying spot markets. To maintain its integrity, the index’s development relied on established best principles for financial benchmarks.

An expert oversight committee is responsible for overseeing the scope of the reference rates by approving and regularly reviewing the calculation methodology, practice, standards and definition of the reference rate to ensure it remains relevant and robust.

Please contact benchmarks@cmegroup.com with any inquiries.

Bitcoin Futures

Learn more about Bitcoin futures, including contract specs, launch date and the underlying CME CF Bitcoin Reference Rate (BRR).