Buying Futures for Protection Against Rising Livestock Prices

{kind=link}

Those involved in buying livestock and livestock products are aware of the risks they face from a potential price increase. Market participants, such as feedlot operators, meat packers, processors and importers, who are concerned about the impact an increase in price could have on their business, constantly seek ways to mitigate risk and protect their bottom line.

Fortunately, due to the availability of CME Group Livestock futures and options, there are many strategies that buyers can employ. This module will discuss buying futures as a hedge against rising prices, including how changes in the basis could affect the final outcome.

Example Trade

Say the buyer is a feedlot operator and it is September. He is planning to purchase feeder cattle for his operation, but is concerned about an increase in feeder cattle prices by the time he’s ready to make his purchase in February. The basis in his area in February is typically $2 over the March Feeder Cattle futures price, which is currently $140 per hundredweight.

The feedlot operator knows that his business will be profitable if he pays $142 for his animals, so he decides to hedge his upcoming feeder cattle purchase by buying, or going long, March Feeder Cattle futures.

By hedging with March Feeder Cattle futures, he locks in a purchase price level of $142 per hundredweight, which is the March futures price of $140 plus the expected basis.

Increasing Prices

Look at what happens to his long futures hedge if feeder cattle prices actually do increase, or if they in fact decline.

Assume the March Feeder Cattle futures price increases to $148. This means that the cash price for feeder cattle in February would be $150, which is $8 higher than the cash feeder cattle price the feedlot operator was anticipating back in September.

However, the $8 gain he makes when he offsets his long futures position by selling March feeder cattle futures will give him a net purchase price of $142 per hundredweight, which is the futures price of $148 plus the expected basis of 2 over minus the $8 gain on the futures position.

Note that this is $8 lower than the feeder cattle price in the cash market.

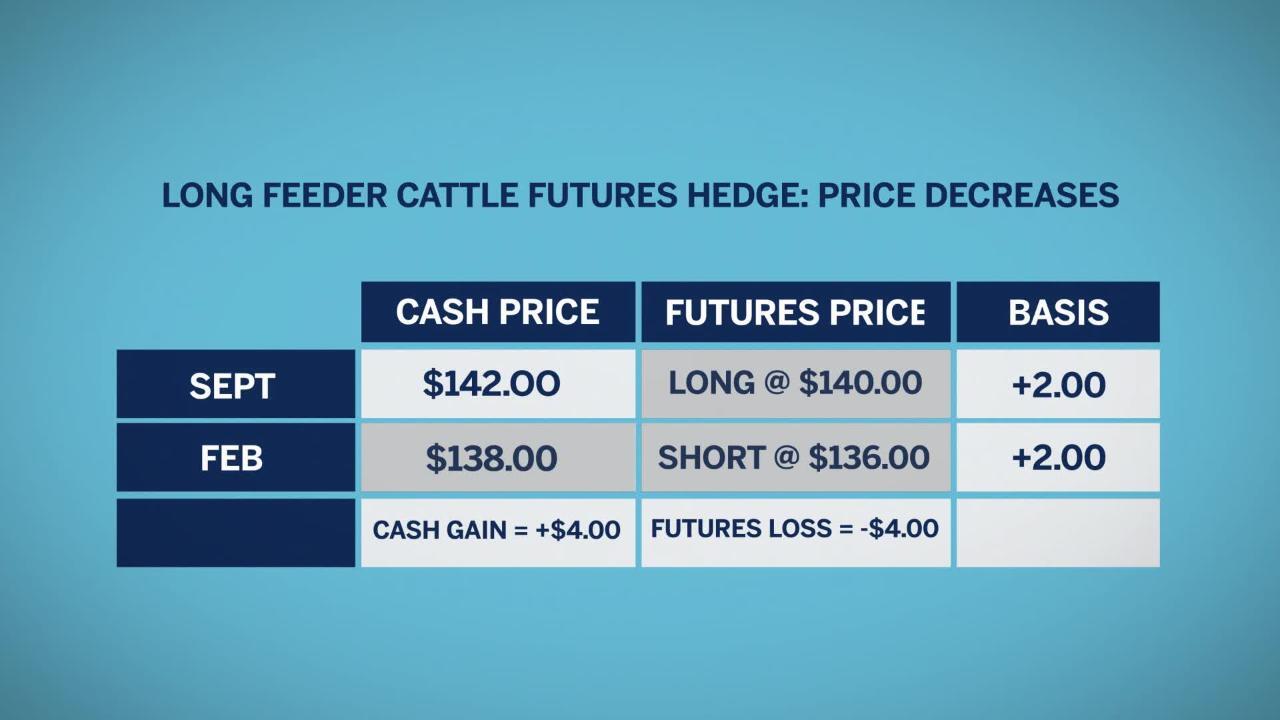

Declining Prices

If feeder cattle prices decline instead, the feedlot operator will still pay $142 per hundredweight for the animals he needs.

Suppose the March Feeder Cattle futures price falls from $140 to $136 by February. With the basis of two over, the feedlot operator would purchase feeder cattle locally at $138 and simultaneously offset his futures position by selling March Feeder Cattle futures at $136.

Even though he could purchase his animals at a lower price, the feedlot operator lost $4 on his futures position. This still equates to a net purchase price for feeder cattle of $142, which equals the cash price of $138 plus the $4 loss on the futures position.

In this scenario, where hedging with futures provided protection against rising prices, but did not allow him to take advantage of a lower price, it may appear on the surface that hedging was a losing proposition for the feedlot operator.

However, remember his original goal at the beginning of this process: to lock in a price of $142 per hundredweight for his cattle purchases. By hedging with futures, he accomplished what he intended when making the decision to hedge. Relinquishing the chance to pay a lower price in exchange for securing price protection, knowing that the price could just as easily have increased, is a trade-off a futures hedger is willing to make.

Basis

Of course, the feedlot operator’s actual purchase price will be affected by what happens to the basis between the time he initiates the hedge and when he makes his cattle purchase. Keep in mind that a long hedger will benefit from a weakening basis, or a basis that becomes less positive or more negative.

A basis that is weaker than expected could lower a long hedger’s net purchase price, even in the face of a price increase. For example, in the earlier scenario Feeder Cattle futures increased to $148 per hundredweight. If the basis weakens from two over to one under for example, his net purchase price would be $139, which is the March futures price of $148, minus the basis of one under, minus the futures gain of $8.

However, if the basis strengthens, in other words, becomes less negative or more positive, it could increase the final purchase price. If the basis strengthens from two over to four over, the result would be a net purchase price of $144 per hundredweight: the March futures price of $148, plus the basis of four over, minus the futures gain of $8.

No one can predict the future, but hedgers can take steps to manage it. Buying livestock futures allows those who need protection against rising prices to acquire the peace of mind of knowing that they took steps to manage the risk involved in purchasing these livestock and livestock products for their business.