https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/bnr-erik-norland.jpg

{kind=link}

Zinc-onomics: Preventing Portfolio Corrosion

Zinc, widely sought after for its anti-corrosive properties, in the making of alloys like brass, and for use in automobiles, electrical components and rubber products, has a strong appeal for portfolio managers in its unexpectedly low correlation to industrial metals such as steel and iron.

Nearly half of the zinc produced in the world is used to galvanize steel, a metal that is highly dependent on the Chinese economy, which has been decelerating after decades of double-digit growth. But there is growth potential for zinc in the United States, the eurozone, Japan, and India.

What is clear is that zinc, given its lack of correlation with iron ore and steel and its status as a leading indicator of aluminum and copper prices, could be a useful addition to any portfolio that includes other metals.Roughly one-sixth of zinc’s industrial use involves brass, an alloy of zinc and copper that is sometimes coated with a transparent layer of aluminum oxide to protect against saltwater corrosion. Brass is stronger than either copper or zinc and has a lower melting point, making it easier to cast. Owing to its shiny gold-like color, brass is often used as a less expensive substitute for precious metals. Additionally, its low-friction property makes it suitable for making locks, door knobs and zippers. Brass is also used in industrial processes where it is important not to generate sparks, such as in work environments where potentially explosive gasses are present. Finally, brass has widespread use in musical instruments. Zinc is also found in bronze, which is primarily made of copper and tin.

Zinc, which is fairly brittle, is also used to make a variety of alloys, including:

- Nickel silver -- typically 60% copper, 20% nickel and 20% zinc, and is sometimes plated with real silver.

- Solder -- a combination of aluminum and zinc; used for soldering electronics and plumbing.

- Die casts -- made primarily of zinc and small amounts of other metals such as aluminum, copper and magnesium. Some die casts can also be made with combinations of zinc, titanium and copper.

- Prestal -- an alloy of aluminum and zinc that is similar in strength to steel but is malleable like plastic.

- Cadmium-zinc alloys -- have semi-conductive properties and can be used in integrated circuits.

Zinc usage can also be found in construction-related materials (roofing and gutters) and in transportation, consumer goods and electrical products (Figure 1).

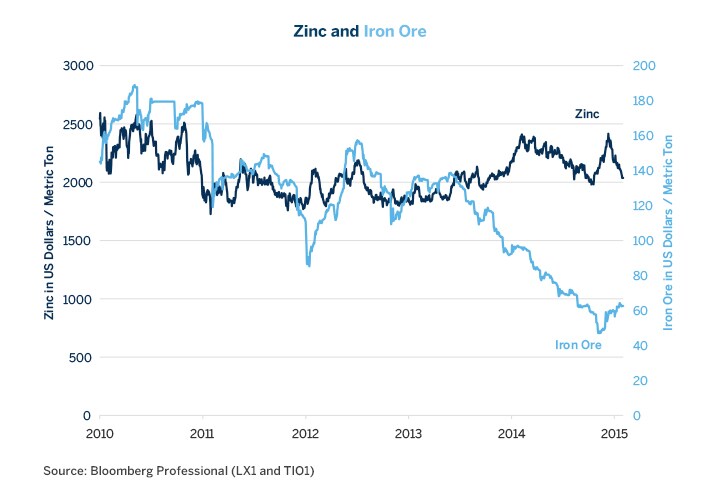

Given the diversity of zinc’s uses and its compatibility with other metals, one might expect it to respond to a broad variety of economic forces and to be highly correlated to other metals, particularly steel, iron and copper. In actuality, its correlation with steel and iron has been extremely low: typically close to zero with steel, and rarely more than +0.2 with iron ore (Figures 2 and 3).

Figure 1.

{kind=link}

Figure 2.

{kind=link}

Figure 3.

{kind=link}

This lack of correlation and the general price disconnect between zinc on one hand and steel and iron ore on the other can largely be explained by the supply side. Data from the U.S. Geological Survey, which tracks global mining production of both zinc and iron -- the primary component in steel -- show that between 1994 and 2014 the correlation of the growth rate in zinc and iron ore mining production was low, only +0.3. Moreover, iron production has been soaring while zinc production has been growing at a much more modest pace. In the ten years from 2004 to 2014, global zinc production grew by 3.3% per year on average. Iron ore production, by contrast, grew by 8.8% per annum. Between 2004 and 2014, global iron ore mining production grew faster than zinc mining production in eight of the ten years (Figure 4).

Figure 4.

{kind=link}

The fact that global iron production has grown 2.6x as much as global zinc production over the past ten years has contributed to a massive supply glut of iron ore and subsequent price collapse that zinc hasn’t experienced. Iron ore is also highly sensitive to changes in Chinese economic.

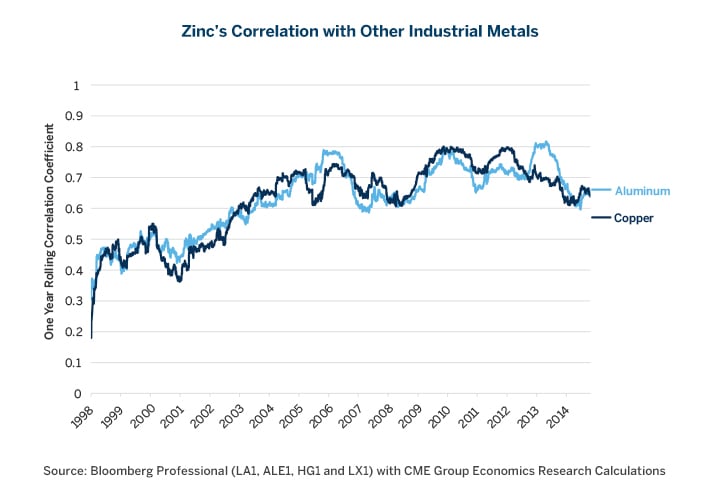

Zinc’s correlation with other industrial metals such as aluminum and copper has been much more robust than it has been with iron ore or steel. Since 2003, zinc has correlated at between +0.6 and +0.8 with both copper and aluminum on a one-year rolling basis. Prior to 2003 the correlation was much weaker, mainly between +0.2 and +0.6 (Figure 5). It appears that as the pace of growth in China and other emerging market countries quickened following the Asian financial crisis in 1997-1998, their hunger for industrial metals drove the prices of most metals higher from 2002 to 2008. Since then, fluctuations in demand from China and other emerging market countries have driven the prices of aluminum, copper and zinc more or less in unison (Figures 6 and 7).

Figure 5.

{kind=link}

Figure 6.

{kind=link}

Figure 7.

{kind=link}

Although zinc correlates quite highly on a day-to-day basis with copper and aluminum, the price patterns sometimes diverge. For example, zinc peaked late in 2006 and entered into a bear market in 2007 that presaged a collapse in aluminum and copper prices in 2008. Following the crisis, zinc prices rebounded, but not to the same extent as aluminum and copper. Zinc’s tepid reaction to the global recovery also appears to have signaled the eventual corrections in copper and aluminum prices that began in 2012. As such, one might wonder if zinc acts as a leading indicator of the health of other industrial metals.

Zinc’s correlation with precious metals hasn’t been as strong with aluminum or copper. Over the past 15 years, the correlation between zinc and silver, gold, platinum and palladium has averaged around 0.3. As such, for those holding portfolios of precious metals, zinc has the potential to be a good diversifier.

Economic Outlook for Zinc

Although zinc hasn’t been highly correlated with steel recently, in part because of the surging supply of iron ore, steel remains fundamental to zinc’s future. After all nearly half of zinc is used to galvanize steel. Steel itself remains highly dependent upon China, which according to the World Steel Association consumed 47.3% of the world’s steel in 2013. China’s economy has been slowing for a variety of reasons, which include:

- The Renminbi is strong, appreciating against almost every currency in the world during the past year except the US Dollar.

- China’s private sector debt is relatively high and a deleveraging is likely to hurt domestic consumption.

- President Xi Jinping has a launched a major crackdown on corruption. Whatever salutary effects this has in the long term, in the short term it risks slowing approvals for new construction projects, etc. that could hamper demand for steel and zinc.

Outside of China we see the potential for stronger growth in the US, the eurozone, Japan and India but generally weak growth in the Middle East and Latin America. In particular, housing demand in the US has the potential to grow strongly. For more information please see "Housing: Building Up to a Boom" as well as our outlook articles on China, Japan, the eurozone, the United States and Latin America.

The collapse in oil prices is unlikely to hurt zinc. It is not heavily used in drilling equipment but has a presence in refining operations. Oil refining is extremely profitable at the moment because crack spreads – the price difference between crude oil and petroleum products – are exceptionally wide. An expansion of oil refineries will likely increase demand marginally for brass, benefitting both zinc and copper.

Overall, we see a mixed economic environment with respect to zinc, with some risks to the downside for prices owing to the potential for weakness in steel demand. What is clear is that zinc, given its lack of correlation with iron ore and steel and its status as a leading indicator of aluminum and copper prices, could be a useful addition to any portfolio that includes other metals.

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Recommended For You

View this article in PDF format.