{kind=link}

Investment Shift from Equities to Real Estate?

For many American investors, there are two main choices in terms of how to achieve returns: stocks and houses. In the past, one might have added bonds into the mix, or even gold. But with long-term bond yields below 2% and short-term rates stuck near zero, holding money in fixed-income accounts does not hold the same attraction that it did during the 1980s, when one could earn near double-digit returns just by parking money in a bank. Gold, meanwhile, has underperformed stocks, crypto assets and most other commodities since the beginning of the pandemic. As such, this might leave many investors a choice between home ownership and investing in equities.

Since the pandemic began, both U.S. home prices and the stock market have performed well. The median purchase price of new homes rose by 23% in June from a year ago, while home prices more broadly rose by 17% in the year to May 31, according to the S&P/Case-Shiller 20-City Composite Home Price Index. Meanwhile, the S&P 500® index has risen by over 30% from its pre-pandemic high in February 2020 (Figure 1).

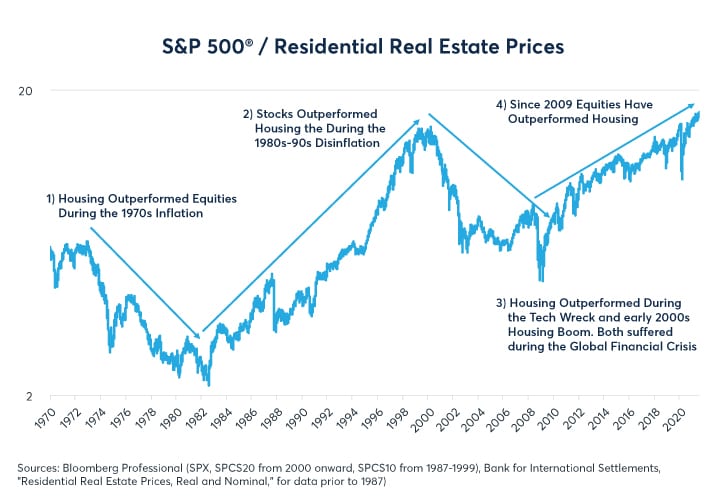

Figure 1: The ratio between stocks and real estate values has been given to strong long-term trends

{kind=link}

The recent outperformance of the stock market relative to housing continues a trend that has lasted since 2009. An investment of $100,000 in the S&P 500 when the market hit bottom in 2009 would have grown 3.51 times than a similar investment in a house, unlevered (i.e. with no mortgage) whose prices rose in line with the S&P/Case Shiller 20-city index.

But the stock market has not always done so well when compared to residential real estate. In fact, since 1970, there have been four distinctly different periods in the housing versus stock market relationship:

- Housing outperforms during great inflation (1972-82): During a period of high inflation in the 1970s and early 1980s housing prices outperformed equity prices. By 1982, an investment in housing in 1972 would have been worth, on average, 2.7x an investment in equites. Soaring bond yields weren’t good news for either stock or home prices. Both underperformed inflation. However, housing, being a physical asset and less dependent on the net present value of future cash flows like equities, resisted the rise in long-term rates better than stocks did.

- Stocks perform better during the great disinflation (1982 to 2000): By 2000, an equity investment in the S&P 500 made in 1982 would have been worth 6x the value of investment made in housing that same year, assuming that the housing investment tracked the average prices for U.S. homes over the period. In short, stock prices soared as inflation, interest rates and bond yields fell. Meanwhile, real estate prices were cyclical: rising in the 1980s, falling from 1989-94 and then slowly rising again.

- Housing rebounds versus stocks (2000 to 2009): An investment in housing in 2000 that performed according to the Case-Shiller 20-city index would have returned 3.16 times as much money by 2009 as an investment in the S&P 500. Housing prices soared from 2000 to 2006, and then began to slide. Although the collapse in the housing market triggered the global financial crisis, the stock market fell more than housing did from 2007 to early 2009 (-60% versus -35%).

- Stocks outperform from 2009 onward: continued low inflation and low bond yields boosted equities more than real estate as the economy recovered from the global financial crisis.

When it comes to the ratio of equity to home prices, economic narratives might influence the relative price trends. During the 1970s a narrative developed that home prices went up with inflation, whereas investors came to see the stock market as a poor investment. The August 13, 1979 edition of Business Week magazine proclaimed famously on its front page: “Equities are Dead: How inflation is destroying the stock market.” For the next three years Business Week appeared to be right: inflation peaked in 1980 and remained in the double digits in 1981 as the economy experienced a double-dip recession between early 1980 and the end of 1982. Stocks finally hit bottom in July 1982.

During the 1980s and 1990s, the narrative shifted. With inflation fading, the equity market soared 1,400%, leaving real estate prices in the dust. There was a real estate boom in the late 1980s but it was reversed during the Savings and Loan crisis, and real estate prices generally fell versus inflation from 1989 to 1994. While real estate prices did begin to rise again in the late 1990s, they were far outpaced by the 20%+ rise in equity prices between 1995 and 1999. A narrative developed that stocks were always the best investment over the long term.

The popping of the tech bubble burst this trend. Between 2000 and 2002 the S&P 500 fell by 50% while the Nasdaq 100 plunged by over 80%. During the stock market rout, the Federal Reserve (Fed) slashed rates from 6.5% and 1%. The result was a boom in housing construction and consumer spending that largely offset the “tech wreck” related decline in business investment. Some Americans began treating their homes as live-in credit cards, taking out second mortgages in order to finance current spending on the assumption that home prices were headed permanently higher.

When home prices began to fall in 2007, this storyline fell apart. Initially the popping of the housing bubble had an even more negative impact on the financial sector than it had on housing. The collapse of major banks severely unnerved equity investors. During the subsequent decade, however, corporate profits soared to a record share of GDP. Dividend payments rose by 155%. Meanwhile, housing struggled to shake off the reputation of being a substandard investment option. Stocks began rallying in 2009, whereas housing prices remained in the doldrums until 2012.

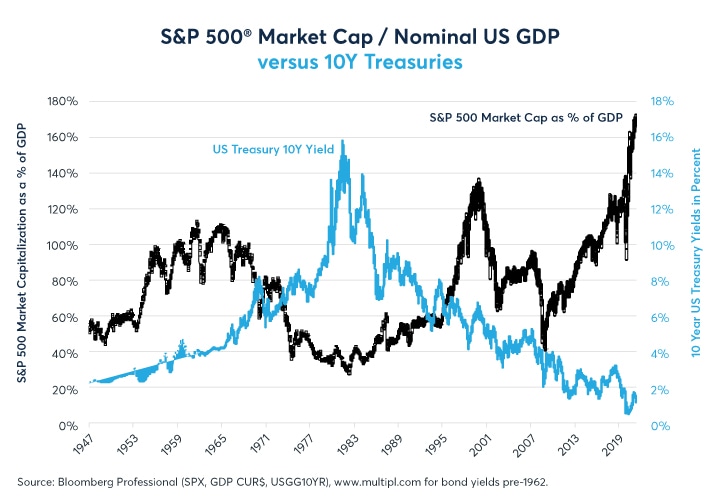

But will the tables begin to turn once again? So far equities have done quite well coming out of the pandemic. That said, equity valuations are at extremely high levels that appear to be predicated on the continuation of low long-term interest rates (Figure 2). The assumption of low long-term rates appears to be based on the idea that the recent rise in inflation will prove to be transitory. Moreover, $120 billion in Fed purchases each month may also be depressing Treasury yields.

Figure 2: S&P 500® market is 2x its 2007 peak even when adjusted for GDP growth

{kind=link}

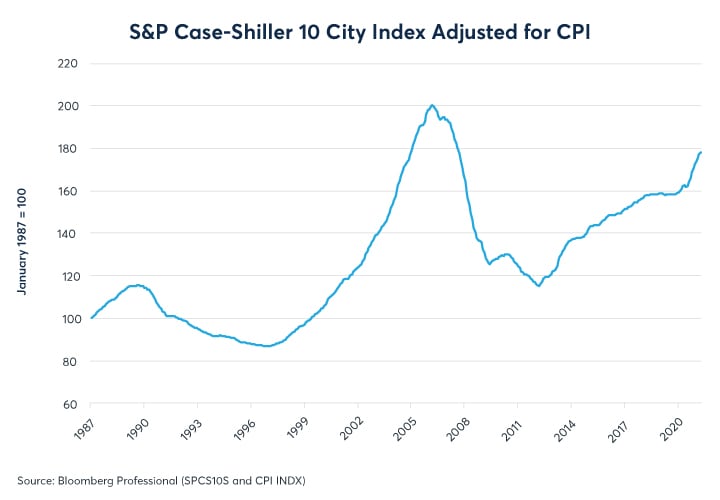

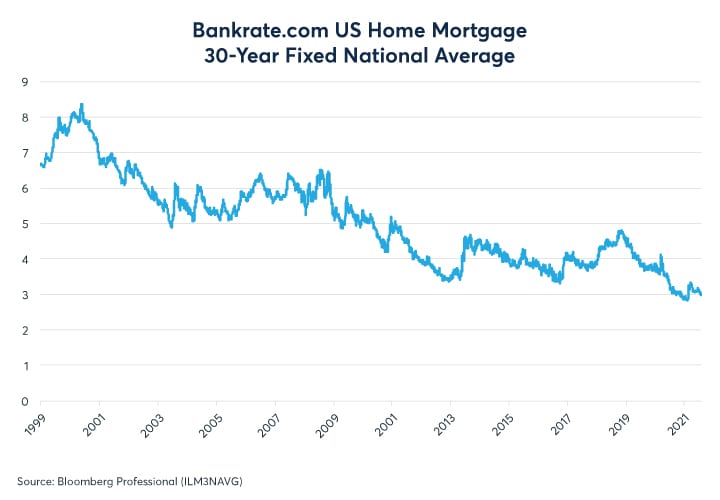

By contrast, if inflation does prove to be more persistent than most investors appear to expect, that could be good news for investors in residential real estate, at least on a relative basis. Unlike stocks, which are at record levels of valuation, housing prices are still about 10% below their 2006 peak, according to the S&P/Case-Shiller index (Figure 3). Moreover, this is despite mortgage rates being less than half the level today that they were at in 2006 (Figure 4). Given the relatively inexpensive cost of financing, it’s easy to imagine home prices continuing to rise.

Figure 3: Home prices are still 10% below their 2006 peak on an inflation adjusted basis

{kind=link}

Figure 4: Mortgage rates are less than half their 2006 levels

{kind=link}

Select Sector Index Futures

E-mini S&P Select Sector futures are liquid, cost-effective and capital-efficient products that track the same underlying indices as the most popular ETFs.