{kind=link}

Will Coronavirus Impact Industrial Metals Markets?

The global economy was weakening even before the coronavirus outbreak. Japan contracted at a 6.3% annualized pace in the fourth quarter of last year following a hike in the value added tax. Growth in France, Germany, Italy and UK ground to a halt. Mexico and South Africa’s economies contracted while Brazil and Russia barely grew. India decelerated to 4.3% year on year, its slowest in years. Even the strong performers, such as China and the US, showed a somewhat slower pace of growth.

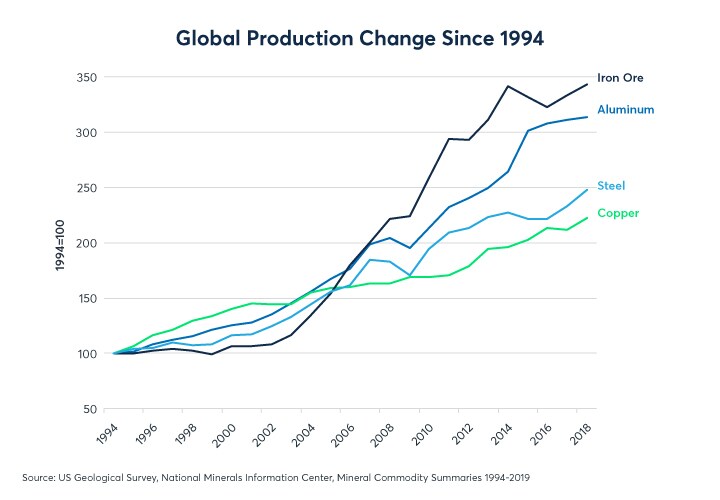

For industrial metals, weakness in the global economy comes at a time when the world is awash in aluminium, copper, iron ore and steel. In the past quarter century, copper mining supply has risen by 125%, while steel production is 150% higher. Those gains pale in comparison to the 225% rise in aluminium production and the 250% increase in iron ore mining supply (Figure 1).

Figure 1: A world awash in industrial metals

{kind=link}

Despite the crash in prices in the mid-2010s, aluminum, copper and steel production has continued to rise. This suggests that even at post-crash prices, it’s still profitable to invest in new production and to maintain existing facilities. The only exception appears to be iron ore, whose mining production dipped in 2015 and 2016 before recovering in 2017 and 2018. The increase in industrial metals supply has been predicated on continued strong global growth led by China.

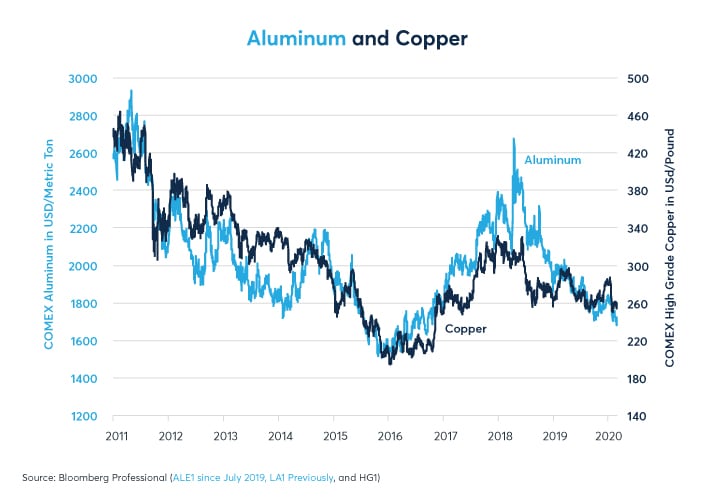

Despite the slowing global growth and surging supply, metals prices have remained remarkably stable. Copper sold off sharply at the end of January but showed only a mild reaction to the equity market’s late February plunge. Aluminum demonstrated a slightly more negative response. Other industrial metals have demonstrated similarly mild reactions (Figures 2 and 3).

Figure 2: Aluminium and copper prices have been relatively steady

{kind=link}

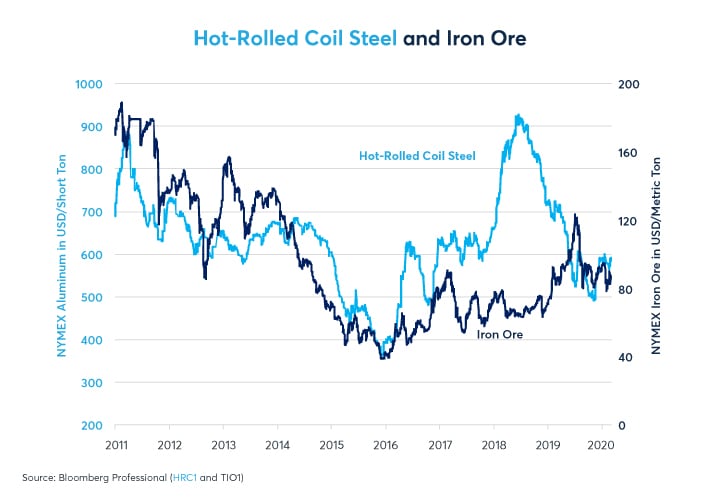

Figure 3: Iron ore and steel have largely been steady

{kind=link}

The metals markets reacted in sharp contrast to the oil market, where prices plunged by as much as 28% as the virus curtailed air, ground and water transportation in China and elsewhere. There are several possibilities for the metal markets’ behavior:

- Even if transportation is slow to recover, the consumer goods and building sectors could rebound quickly, stabilizing demand for metals sooner rather than later

- Lower interest rates and fiscal stimulus could be effective, generating a strong rebound in metals demand later in 2020

- Supply chain disruptions may require higher production in the future to catch up with demand

- Consumers, who are avoiding travel and curtailing spending today, could increase their savings rates, which may unleash pent up demand in the future

- Excess inventories can be held in storage while markets wait for demand to recover

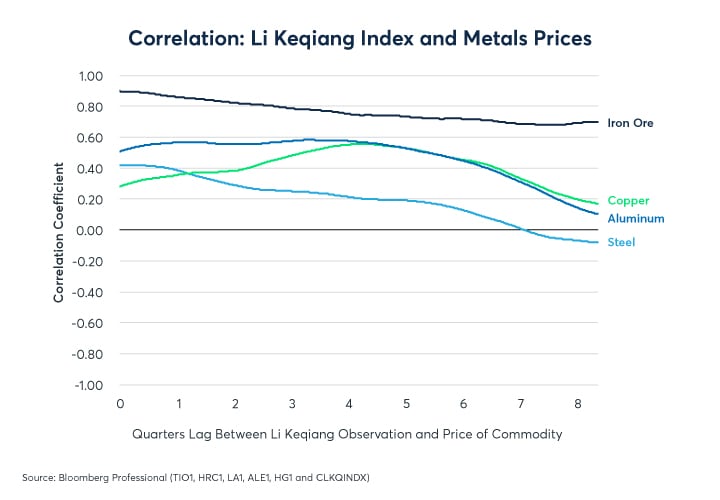

In addition to these optimistic interpretations, there is a less hopeful possibility. Over the past 15 years, industrial metals have shown a high correlation with Chinese growth – but often with a significant lag of up to 18 months (six quarters) (Figure 4). If experience is any guide, the true impact of the coronavirus on metals demand may not become apparent for six months to a year, or more. Moreover, the reason why metals prices haven’t shown a more negative reaction may have to do with the lagged effect of China’s solid growth in 2018 and 2019.

Figure 4: All industrial metals show a strong response to changes in the Li Keqiang Index

{kind=link}

To measure the relationship between Chinese growth and metals prices, we use the Li Keqiang Index, a narrow measure of China’s growth that focuses on electrical consumption, rail freight volumes and bank loans (Figure 5). The index assessment, which until December was indicating growth in China’s manufacturing sector of 9-10% year on year, will next be released in late March. In the meantime, China’s PMI data points to an extremely severe contraction in February after a relatively normal pace in January. The question for March and April is how quickly industrial production gets back on track. In addition to Chinese growth, the future path for metals prices will depend crucially on the impact of the coronavirus on demand for finished goods in the world and the success of fiscal and monetary authorities in boosting global growth.

Figure 5: Le Keqiang Index showed solid growth in December. Jan & Feb numbers out late March

{kind=link}

Bottom Line

- The global economy was weak even before the coronavirus

- Industrial metals prices have shown only a mild price response

- Metals traders may be banking on a rapid recovery in demand

- Metals markets often react with significant lags to changes in Chinese growth

Metals Options

We help market participants manage price risk with our comprehensive suite of COMEX and NYMEX Metals Options.