{kind=link}

Which Yield Curve Foretells Growth the Best?

Which Yield Curve Foretells Growth Best?

The late summer inversion of the US Treasury yield curve raised concerns that the US economy might be heading towards a slowdown, or worse, in 2020. Investors should therefore be heartened to know that the US Treasury yield curve flipped back to a positive slope in mid-October.

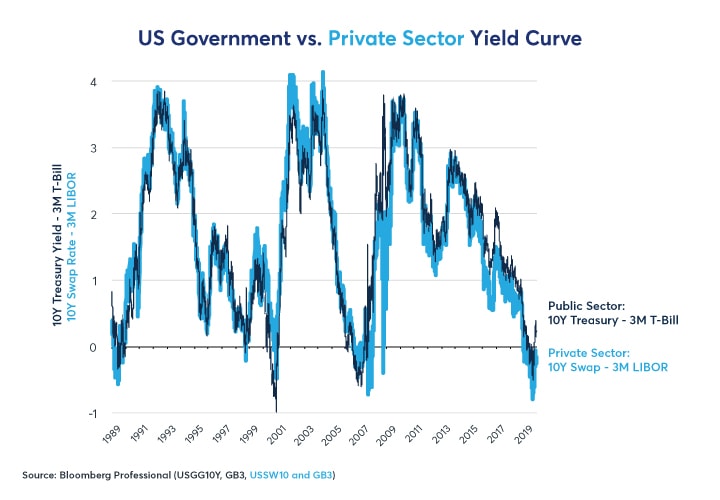

There is, however, a fly in the ointment. The public sector yield curve, which we measure by subtracting the rate on 3-month Treasury Bills from the yield on 10-year US Treasuries, isn’t the only, or even the best, yield curve available as an economic indicator. The shortfall with the public sector curve is that only the US government borrows at public sector rates and yields. The private sector has its own yield curve, which can be measured by the difference between 10-year swap rates and 3-month ICE LIBOR. Unlike the public curve, the private sector measure remains inverted (Figure 1). As of November 27, the 3M10Y public sector curve had a 15bps positive slope whereas the 3M10Y private sector curve remained inverted to the tune of 25bps.

Figure 1: Similar but not the same, the public and private sector yield curves occasionally diverge.

{kind=link}

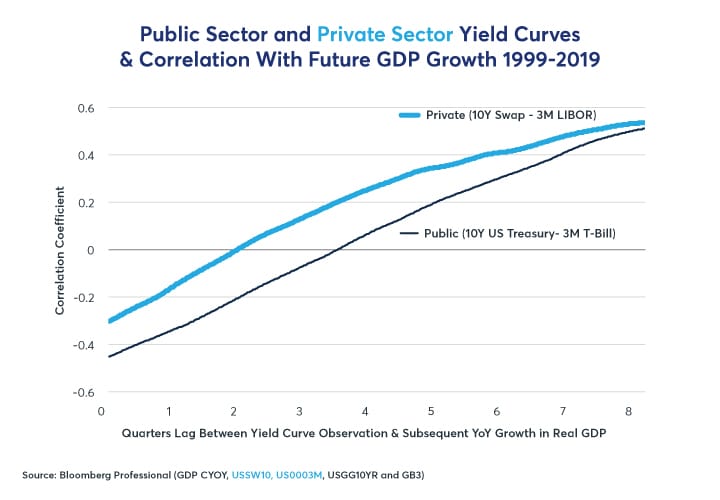

Over the past two decades, the private sector curve has correlated more positively with future economic growth than has the public sector version. Neither the private sector (10Y swap minus ICE LIBOR) nor the public sector (10Y Treasuries minus T-Bills) yield curve has much to say about what will happen to the GDP growth in the next couple of quarters. In fact, inverted yield curves usually occur during periods of strong growth while steep yield curves usually follow periods of weak growth. Both public and private sector curves, however, have positive correlations to growth further in the future.

The public sector yield curve has a weak positive correlation with growth one year (four quarters) in the future and a rather strong correlation (+0.51) with growth two years (eight quarters) in the future when measured over the past 20 years. The private sector curve evidences an even stronger correlation with future growth. Its correlation to future GDP growth turns positive after just two quarters and achieves a very positive correlation (+0.54) with growth two years in the future (Figure 2).

Figure 2: The private sector curve does a better job of forecasting than the public sector curve.

{kind=link}

Causal or Coincidental?

Yield curves tend to invert towards the peak of economic expansions for two reasons. First, as the economic expansion wears on, the Federal Reserve (Fed) begins to worry that if labor and product markets become too tight, it will lead to inflation. To prevent the pace of inflation from quickening, the Fed raises short-term interest rates. Because of tighter monetary policy, investors in long-term bonds begin to worry about the possibility of an economic slowdown. Long-term bond prices rally and yields fall, thus further compressing the spread between long-term and short-term interest rates.

Whether yield curve slopes cause economic accelerations and slowdowns is more controversial. One could argue that banks and other lenders make money by borrowing short-term and lending long-term. As such, when long-term rates are higher than short-term rates, it incentivizes lenders to extend credit. Faster credit creation expands the economy.

By contrast, flat yield curves detract from the lending profitability. Eventually, under stress from flat yield curve environments, they will choke off the supply of credit, slowing economic growth and obliging the central bank to ease policy.

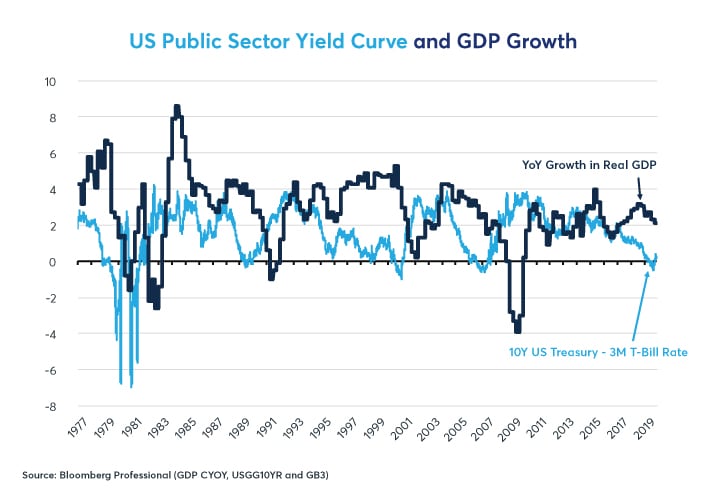

Irrespective of whether one thinks yield curves play a role in causing accelerations or slowdowns in the pace of economic growth, they have been useful indicators of where growth has been going over most of the past four decades. Prior to the tracking of swap rates in the early 1990s, the public sector yield curve was the only option for forecasters. Every single downturn in the past four decades has been preceded by a period of either extremely flat or inverted public sector yield curve. Every recovery has been led by a steep yield curve (Figure 3).

Figure 3: The yield curve has often been a good indicator of growth rates in 1-2 years’ time.

{kind=link}

Given the yield curves usefulness as a forward indicator of growth, it is particularly worrisome that even after three Fed rate cuts in 2019, the public sector curve has barely gone back to positive while the private sector version remains inverted. If past correlations are any guide, this may have little bearing on growth in early 2020 but could be indicative of a slowdown (or worse) in late 2020 or 2021. The fact remains that the Fed was the only central bank in the world that tightened policy so dramatically between 2015 and the end of 2018. Even after three rate cuts, the Fed has left six increases in place totaling 150bps of tightening and the fixed income markets continue to warn that US monetary policy remains very tight. In addition to raising interest rates, they also shrunk their balance sheet from 25% to 18% of GDP, which may have helped to trigger problems in the repo market in September.

All that said, there is also an optimistic case that the economy could defy the odds and continue to grow despite the warnings sent by flat or inverted yield curves.

Goldilocks 2?

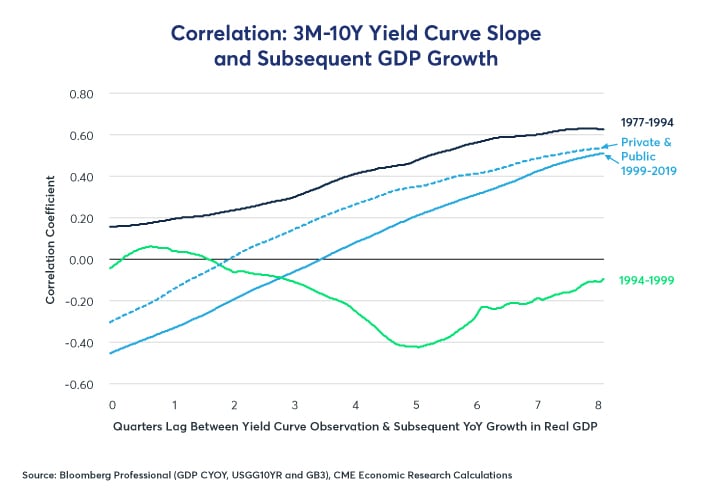

Since 1979, the yield curve has only misfired as an indicator once: in the second half of the 1990s. Following the Fed’s tightening cycle in 1994, the yield curve became quite flat but economic growth, after a brief slowdown in 1995 and 1996, accelerated in 1997 and remained robust until the middle of 2000. In the current so-called Goldilocks economy, inflation has remained low despite rapid growth. Whereas, the public sector yield curve correlated positively with future GDP growth both before and after this period, during the late 1990s, the correlation went negative for a five-year period (Figure 4).

Figure 4: Yield curve misfired in the late 1990s but worked well before and after.

{kind=link}

Can it happen again? Could economic growth defy the odds a second time despite flat/inverted yield curves? The current economy shares certain features with the late 1990s: low inflation and a powerful equity bull market. During the late 1990s and as is today, the relationship between the rate of unemployment and the level of inflation was weak. Even at 3.6% unemployment, we appear in 2019 to have even less inflationary pressure than we had during the late 1990s when unemployment last achieved similarly low levels.

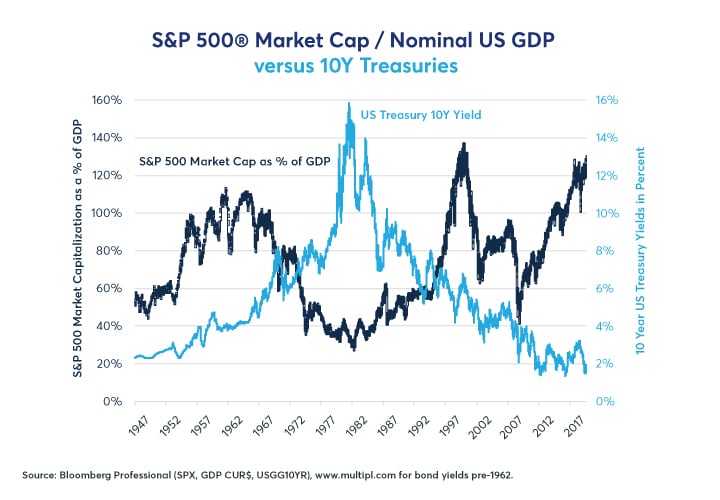

Also, in the late 1990s, the equity bull market provided the economy with an alternative source of financing. Initial public offerings (IPOs) raised capital that fueled an investment boom, defying otherwise rather tight credit conditions in the fixed income markets. Perhaps what is most striking is that while US equity market capitalization is at similar levels to those seen at the end of the 1990s, interest rates are only one quarter has high. Back then 10-year Treasuries yielded around 6-7%. Recently, they have traded in a range of 1.5-2.0% (Figure 5). Given lower bond yields, equities might be able to support much higher valuation ratios than they could in the past. If the equity market continues to soar, positive impacts from the wealth effect, and the ability to raise capital from IPOs, could overcome the drag of a tight Fed monetary policy and a flat yield curve.

Figure 5: Equity market cap is back to 2000 levels, but bond yields are only a quarter as high.

{kind=link}

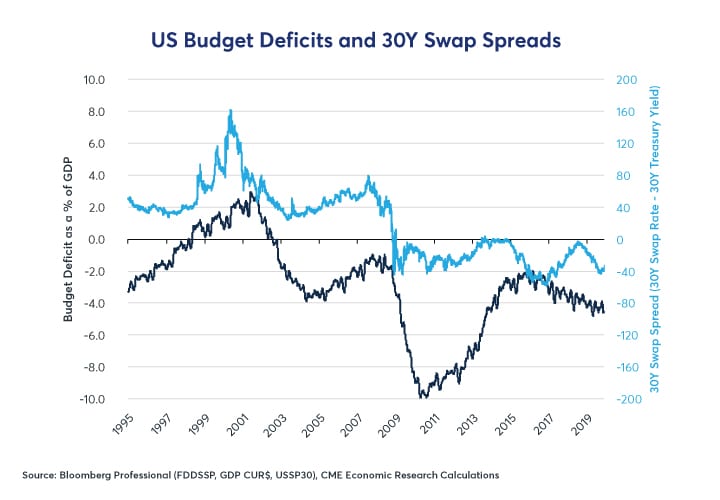

While the late 2010s in some ways look a great deal like the end of the 1990s (soaring equities with technology stocks in the lead, low inflation), there are differences as well. In the late 1990s, the US government was moving into a budget surplus. As such, it reduced its issuance of US Treasuries causing 30Y government bonds to trade as much as 160bps below 30Y swaps. Today, things are the opposite. Rather than a 2% of GDP budget surplus, the US government is running a 4.5% budget deficit. So many Treasury bonds are being issued that 30Y government yields are trading a 34bps over 30Y swap rates (Figure 6).

Figure 6: Bigger deficits have raised Treasury issuance and helped to push swaps spreads negative.

{kind=link}

And herein lies the rub. In the late 1990s, investors could be confident that if the economy went pear-shaped, the government had enormous borrowing capacity and could cut taxes and raise spending to save the day. Indeed, that’s exactly what the government did in 2001 and again in 2009. Today, with a budget deficit that is approaching 5% of GDP (10 years into an economic expansion), the potential for fiscal stimulus in the event of a downturn isn’t so great. Public sector debt has also climbed from 36% of GDP in 2000 to 100% of GDP today. Indeed, much of the reason why the public sector yield curve has gone back to a positive slope, while the private sector curve remains inverted (despite three Fed rate cuts), is because the US Treasury is issuing debt at a furious pace.

So far as we are aware, there is no recent precedent for such pro-cyclical fiscal policy this late into an economic expansion. Usually deficits shrink as expansions wear on. This time they are expanding. Moreover, if fiscal policy is pro-cyclical late in the expansion, it could be pro-cyclical during a slowdown as well, especially if Congress is unwilling to expand deficits further in the face of weaker growth or if expanding deficits further doesn’t achieve much in the way of boosting the economy.

Bottom line

- The private sector US yield curve remains inverted while the public sector curve flipped positive.

- Private sector yield curves have been better indicators of growth in the past 20 years.

- Yield curves misfired in the mid-1990s, predicting a slowdown that didn’t happen.

- Soaring equities could enable the economy to defy the yield curves’ suggestion of slower growth ahead.

- A larger budget deficit, however, could make it harder for the US government to fight off any slowdown.

Interest Rate products

Our Interest Rate products span the entire US dollar-denominated yield curve, including futures and options on the most widely followed US Interest Rate benchmarks: Eurodollars, US Treasury Securities, 30-Day Fed Funds, and Interest Rate swaps.