{kind=link}

U.S., China Corn Markets Converge Amid Surplus

Highly Liquid: CBOT and Dalian Corn Futures

Corn futures at CME Group’s Chicago Board of Trade (CBOT) and China’s Dalian Commodities Exchange (DCE) are highly liquid. The average daily volume (ADV) of CBOT corn is 350,000 contracts (44 million metric tons, or MT), and that of the DCE contract is 980,000 lots (4.9 million MT)1. There is a key difference - the CBOT contract is a global benchmark while the DCE contract is restricted to domestic Chinese trading firms.

As China, the world’s most populous country with a growing appetite for meat, produces corn domestically, and from time to time imports the grain from the United States, traders tend to monitor crop production in the world’s two largest economies for trading decisions, along with their bilateral trade flows.

China is largely self-sufficient in corn, but in 2009 the government began a stock-piling program to guarantee the supply of key commodities. Most of the imports were from the U.S. China currently has an estimated stockpile of 103 million MT of corn, an annual domestic production of about 218 million MT, and consumption of 226 million MT2.

Figure 1: China Corn Production vs. Imports from U.S.

{kind=link}

U.S.-China Corn Historical Correlation Very Low

There has been little correlation between CBOT and DCE corn futures prices3 in the past decade as they are two distinct and separate markets.

China is largely a closed market for corn, and the DCE contract generally reflects the domestic prices of roughly 200 million MT of annual domestic production.

On the other hand, the corn market in the United States, the world’s largest exporter of the grain that is largely used to feed livestock, is widely accessible. The CBOT contract reflects the 50 million MT that are exported from the U.S. annually, in addition to global supply and demand dynamics.

The ‘domestic versus international’ difference between the DCE and CBOT markets is the primary reason for the lack of correlation between their prices.

Figure 2: CBOT & DCE Corn Prices Uncorrelated

{kind=link}

Change in China Corn Stockpiling and Import Policy

However, this changed in April 2016 when China announced that it was ceasing its stockpiling program, and ending its subsidies that paid farmers high prices for their corn as a way to boost rural incomes. For the first time in almost a decade, farmers have to sell their corn crop without government price support.

China's surplus of corn has created a growing stockpile that appears to be unmanageable even as the country prepares to harvest a bumper crop in 2017.

This has led the Chinese government to permit two state-owned companies, Cofco and Beidahuang, to export 2 million MT of corn.

The DCE front-month contract fell to its lowest level in nearly seven years and is currently hovering around 1,450 yuan (CNY) per MT (about US$214).

Policy Change to Impact 2017 Contract Prices

DCE corn futures price movements in the Sep-2016 contract (reflecting the current crop) and Jan-2017 contract (the next harvest) have been divergent.

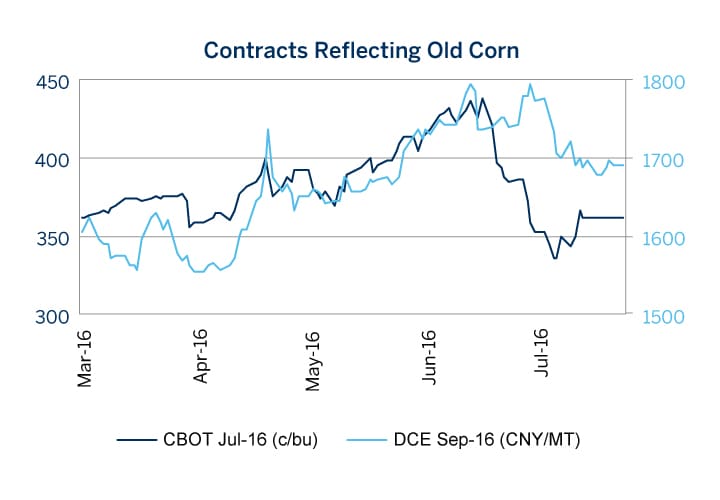

The government’s support for Chinese corn prices are maintained for the current crop, and the DCE Sep-16 contract continued to show a relatively poor 0.57 price correlation5 with CBOT’s corresponding Jul-16 corn prices (Figure 3).

However, price movements in the DCE Jan-17 contract representing the Chinese new crop were much more in step with CBOT corn. This is reflected in the much better 0.90 price correlation with CBOT (Figure 4). With the price floor removed, China’s new crop prices started to fall in line with supply and demand dynamics, which are impacted by international prices.

Figure 3: CBOT vs DCE Old Corn Uncorrelated

{kind=link}

| CBOT N6 (Jul-16) vs DCE U6 (Sep-16) Prices4 | |

| Price correlation | 0.57 |

| Log Return Correlation | 0.25 |

Source: Bloomberg, CMEG market data & estimates

Figure 4: CBOT vs DCE New Corn Correlated

{kind=link}

| CBOT Z6 (Dec-16) vs DCE F7 (Jan-17) Prices | |

| Price correlation | 0.90 |

| Log Return Correlation | 0.36 |

Source: Bloomberg, CMEG market data

Factoring in FX, Freight, & Taxes to Prices

While the price correlations improved, the logarithmic return correlations have clearly not improved, remaining at a weak 0.36. There is a statistical theory behind this, which will be addressed shortly. First, a few explanations are included to make the above analysis more robust.

FX Improved the Correlation Slightly

When foreign exchange effects were taken into account, ( i.e., DCE corn prices were adjusted to U.S. dollar (USD) terms using prevailing USD/CNH FX rates), the price level return correlations were marginally better.

Figure 5: CBOT & DCE Corn Adjusted for FX Impact

| CBOT Z6 (Dec-16) vs DCE F7 (Jan-17) Prices | ||

| Adjusted for FX Impact? | No | Yes |

| Price correlation | 0.90 | 0.91 |

| Log Return Correlation | 0.36 | 0.37 |

Source: CMEG estimates

Including Tax and Freight Brought Prices Closer

Although the prices of DCE new-crop corn futures (CNY 1,446/MT or $214/MT) are moving closer to CBOT corn futures ($3.54/bu or $139/MT), there is a persistent price gap of around $70 to $100 per MT which has to be explained. This price differential is almost entirely due to freight costs and import tax imposed by the Chinese authorities. This is illustrated in the calculations in Figure 6.

Taking the price of U.S. corn delivered to Illinois River grain elevators as the starting point (as reflected in the CBOT Dec-16 futures price), a $0.50/bushel transport cost is added to price it basis free-on-board (FOB) at the U.S. Gulf Coast. $27/MT in freight costs and insurance fees are added to bring the price to a cost, insurance and freight (CIF) basis when shipped to China. And finally, a 13% value-added tax and 1% import duty is applied to arrive at the ‘landed cost’ of U.S. corn in China.

As Figure 6 showed, when the pertinent costs are included, the new crop prices of DCE corn futures do indeed appear to be converging with CBOT prices.

Figure 6: Difference in CBOT & DCE Prices Explained

| Date Selected: 17 October 2016 | ||

| USD/CNH Rate: 6.675 | CNY/MT | USD/MT |

| DCE Jan 2017 corn futures | 1,446 | 214.28 |

| US¢/bu | ||

| CBOT Dec 2016 corn futures | 354 | 139.37 |

| Basis FOB US Gulf Coast | 50 | 19.69 |

| Freight USGC to China | 25.00 | |

| Other Fees and Costs | 2.00 | |

| CIF China | 186.05 | |

| Import Duty and VAT | 14% | 26.05 |

| Landed Cost China | 212.10 | |

Source: CMEG estimates

Preliminary Take-Away – Trade the Right Contract

In agricultural commodities, futures contracts allow you to manage risk on the current as well as future harvests. Therefore, selection of the correct contract month is key to effective hedging when managing risk in old or new-crop exposures or in expressing a view on current or future price levels.

This has always been the case for trading corn futures, as with other grains, as the impact of factors such as global export demand and currency exchange rates primarily impact old crop values while weather impact on harvesting and planting affect new crop values.

The choice of contract month is even more pertinent in the current situation. The Chinese old crop corn still benefits from price support by the Chinese government. New crop corn, however, will not receive such support and price movements will likely be more volatile. Concurrently, price movements of DCE new crop futures will more closely follow global corn prices as represented by the CBOT corn market and can potentially be hedged with CBOT futures.

Good Case Study to Explain Correlation

As earlier mentioned, the current situation between CBOT and DCE corn futures provides a good case study to illustrate the differences between Price Level Correlation and Price Return Correlation6. Basically, if prices are from two separate and distinct markets, even though they reflect the same underlying asset (i.e., corn), their short term (daily) movements will be independent of each other. This means that one cannot predict the next day’s movement of DCE corn prices based on movements in CBOT corn prices the previous day.

Similar Price Patterns but No Causality

Even if CBOT and DCE prices appear to be moving in tandem, there is likely no cause-and-effect, and the percentage (i.e., return) movements as reflected by the log return correlation are not linked to each other. This is illustrated in Figure 7, where price level correlation is 0.91. The log return correlation of 0.37, however, tells us that the two prices were moving fairly independently of each other.

Figure 7: CBOT vs DCE Price Correlations

{kind=link}

| CBOT Z6 (Dec-16) vs DCE F7 (Jan-17) Prices in USD | |

| Price correlation | 0.91 |

| Log Return Correlation | 0.37 |

Source: CMEG estimates, adjusted for FX impact

DCE Corn Front Months Affect Back Months

Based on Figures 7 and 8, one is led to believe that the DCE Jan-17 (new crop) prices are correlated more to the movements of CBOT’s Dec-16 prices than to DCE’s own front-month prices. After all, DCE’s Sep-16 prices reflect the old crop supported by the government’s price-floor policy, whereas DCE’s Jan-17 prices are subjected more to global conditions.

The log return correlation of 0.59 indicates that DCE’s Jan-17 price movements are in fact more predictable7 using DCE’s Sep-16 prices than using CBOT’s Dec-16 prices, despite CBOT’s pattern looking more similar.

The CBOT and DCE prices follow ‘random walk,’ i.e., when the two prices may end up at the same place but the paths taken are different. On the other hand, within the same asset, DCE prices follow each other’s directional movement daily even if the prices do not end up in the same place.8

Figure 8: DCE Front vs. Back Month Correlations

{kind=link}

| DCE U6 (Sep-16) vs DCE F7 (Jan-17) Prices in USD | |

| Price correlation | 0.18 |

| Log Return Correlation | 0.59 |

Source: CMEG estimates

Conclusion

Due to the change in the Chinese government’s stockpiling policy, DCE corn futures prices are converging with CBOT prices, subject to differentials due to transportation costs and import taxes.

For traders holding their positions over the medium term, CBOT futures should become a reasonably good proxy tool for taking a trading view on China’s new crop corn harvest.

China's General Department of Taxation has resumed giving a 13% tax rebate for exporting 10 corn by-products, including ethanol and corn starch, since September 2016. The move is mainly aimed to clear the country’s huge corn stockpile.

At current price levels, China’s corn prices at around CNY 1,450/MT (equivalent to US$5.50 per bushel) do not appear to be internationally competitive. The United States has challenged China’s price supports, saying they exceeded limits Beijing committed to before joining the World Trade Organization in 2001 and could have an adverse impact on the incomes of U.S. farmers.9

Figure 9: Contract Specifications of CBOT Corn Futures and DCE Corn Futures

| CBOT Corn | DCE Corn | |

| Product Name | Corn | Corn |

| Product Description | Corn No. 2 Yellow | |

| Exchange Product Code | ZC | C |

| Bloomberg Product Code | C A Comdty | ACA Comdty |

| Contract Size | 5,000 bushels (» 127 MT) | 10 MT |

| Contract Months | Mar, May, Jul, Sep, Dec | Jan, Mar, May, Jul, Sep, Nov |

| Price Quotation | USD/bushel | CNY/metric ton |

| Minimum Price Fluctuation | ¼ cent/bu ($12.50 per contract) | 1 CNY/MT (CNY 10 per contract) |

| Contract Value (Nov 2016) | $17,725 | CNY 15,240 (» $2,250) |

| Contract Settlement | Physical | Physical |

| Delivery Quality | #2 Yellow at contract price #1 & #3 Yellow at premium/discount |

DCE FC/DCE D001-2009 |

| Delivery Locations | Approved regular warehouses for loading in Chicago and on the Illinois River. | Warehouses appointed by DCE |

| Termination of Trading | Day before 15th day of delivery month | 10th Day of delivery month |

References

1. DCE reports volumes by each-side traded, whereas CME Group reports by round-turns. To make them comparable in MT terms, the converted DCE volumes are halved.

2. Source: USDA GRAIN Report CH16027 dated 4/8/2016.

3. CBOT spot month contracts are compared with DCE next-month contracts as they are the more actively traded contracts.

4. For all comparisons between CBOT and DCE, DCE prices are with a day lag, e.g. CBOT 26 Oct price is compared with DCE 27 Oct price.

5. US Corn takes a month to arrive in China, so Sep-16 DCE price would be related to CBOT Jul-16 (CBOT has no Aug-16) price. And DCE Jan-17 price would correspond to CBOT Dec-16 price.

6. Log Return Correlation is used in practice when price range is big to prevent the big figures overwhelming the small figures. It is a variation within the family of Return Correlations.

7. Note we cannot conclude whether there is ‘causality’ here; to do so require other tests such as the Granger Causality Test.

8. Extracted from http://www.portfolioprobe.com/2011/01/12/the-number-1-novice-quant-mistake/

9. https://ustr.gov/about-us/policy-offices/press-office/press-releases/2016/september/united-states-challenges