{kind=link}

Uneven Debt Levels Complicate Eurozone Monetary Policy

Former British Prime Minister Winston Churchill once remarked that Americans could always be counted on to do the right thing after having tried everything else. The same could be said of the European Central Bank (ECB) for what it did over the past decade in the aftermath of the financial crisis.

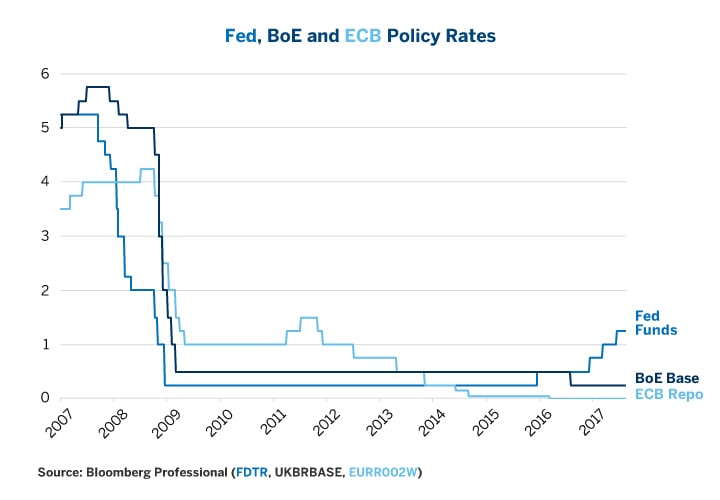

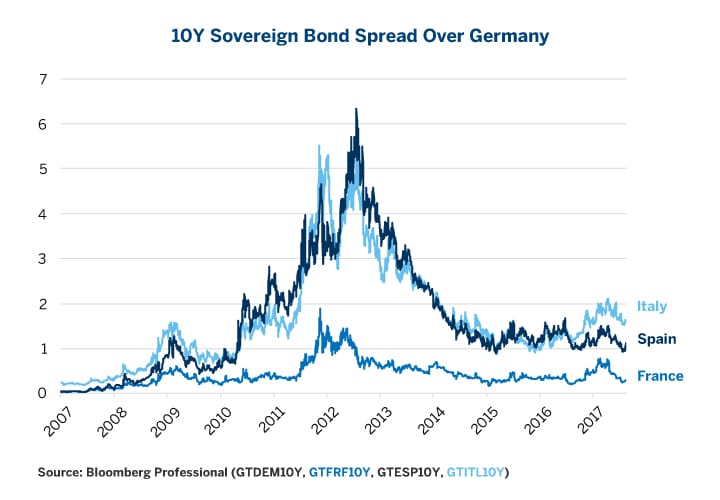

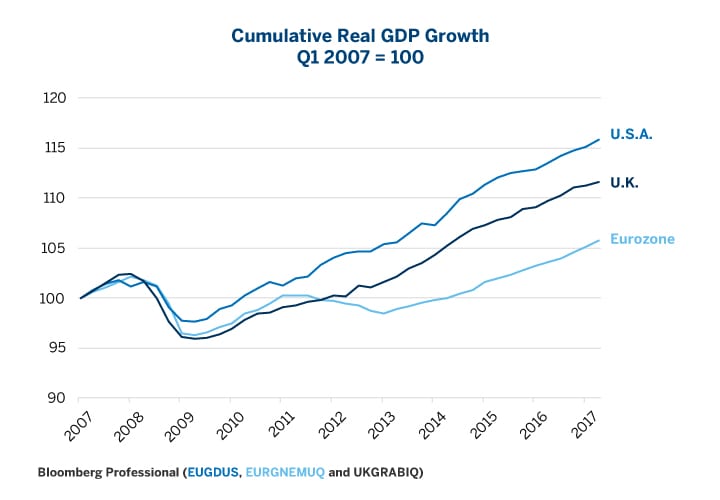

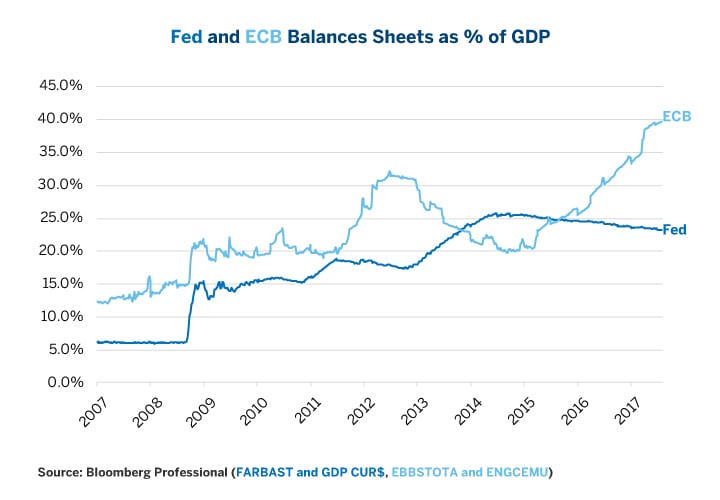

While the U.S. Federal Reserve (Fed) and the Bank of England (BOE) swiftly lowered interest rates to near zero in late 2008 as the crisis unfolded and initiated quantitative easing (QE) in early 2009, the ECB took a different approach. It didn’t lower its refinancing rate all the way to zero in 2009, and was tightening monetary policy by 2011 (Figure 1). The result was a disaster. Yields on non-German debt soared (Figure 2), bringing Greece, Ireland, Italy, Portugal and Spain to the brink of financial collapse while the eurozone experienced a double-dip recession that the U.K. and U.S. avoided (Figure 3). After 2012, when ECB President Mario Draghi indicated that the ECB will backstop eurozone sovereign debt markets and began cutting rates in earnest, yield-spreads narrowed and the eurozone economy recovered (Figure 4).

Figure 1: ECB Didn’t Cut Rates Quickly Enough in 2009. Its 2011 Rate Hikes Were a Disaster.

{kind=link}

Figure 2: The Sovereign Debt Crisis Nearly Bankrupted Five Eurozone Nations.

{kind=link}

Figure 3: After Draghi Backstopped Bond Markets and Cut Rates, Eurozone Growth Resumed.

{kind=link}

Figure 4: ECB Began QE in 2014, Five Years After the Fed Did.

{kind=link}

The European and U.S. financial crisis essentially had the same underlying cause. By the middle of the last decade, total debt levels (public + private) on both sides of the Atlantic climbed to levels that were unsustainable, with central bank policy rates in the 4-5% zone. There are numerous other superficial similarities between the U.S., U.K. and eurozone debt crises and their subsequent developments:

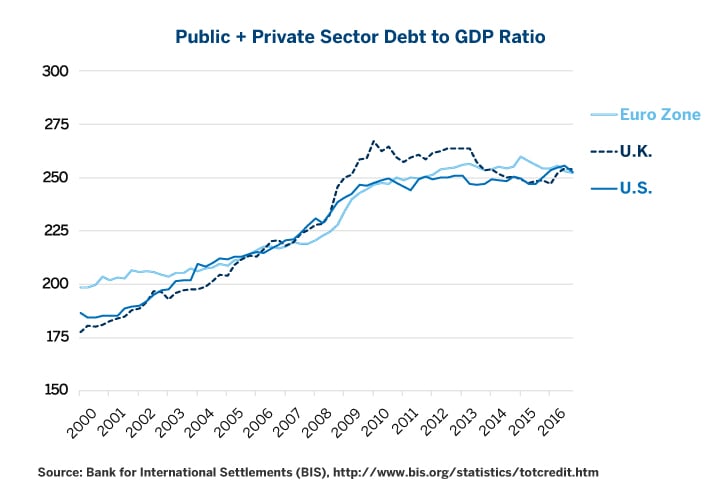

- All three crises began with total debt levels near 225% of GDP.

- Total debt levels soared in 2009 and 2010, and public sector deficits exploded.

- Fiscal tightening and crackdown on private-sector leverage allowed debt levels to stabilize after 2010 at around 250% of GDP but no overall deleveraging has occurred since (Figure 5).

Figure 5: The U.S., U.K. and Eurozone debt crises are superficially similar

{kind=link}

What differentiates the eurozone from the U.S. and U.K. isn’t the overall level of debt but rather their highly varied levels, trajectories and composition of debt within the 19-nation currency bloc. Essentially, the eurozone’s major economies fall into four categories:

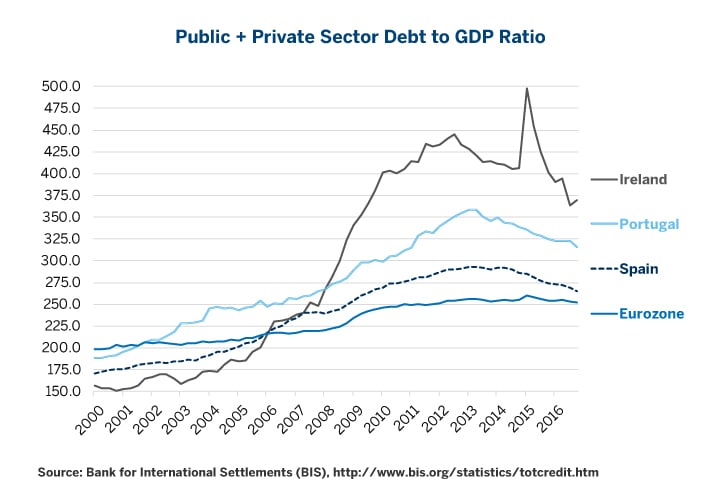

- Those with high levels of debt who are deleveraging (Ireland, Portugal and Spain – Figure 6).

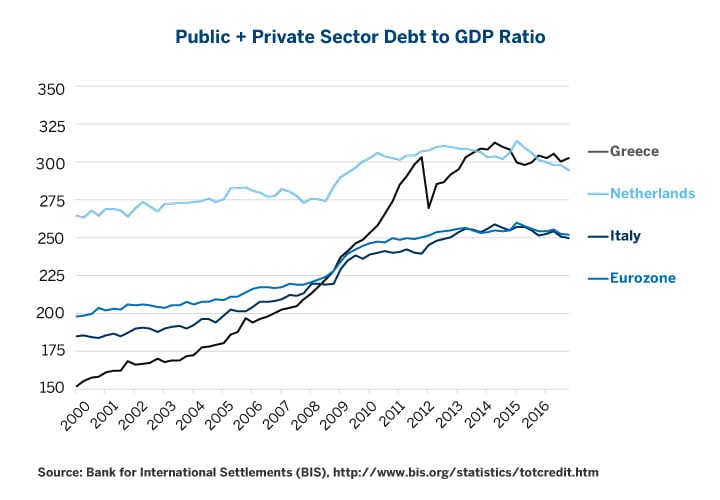

- Those with high levels of debt who are not deleveraging (Greece, Italy & the Netherlands – Figure 7).

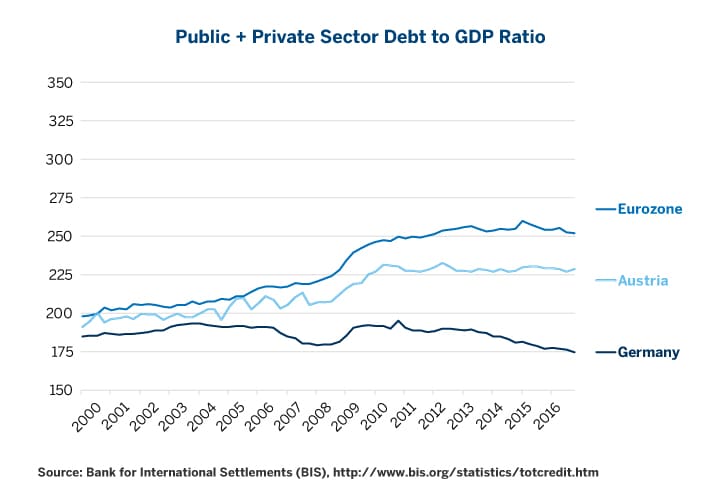

- Those who have low levels of debt that are stable and falling (Austria and Germany – Figure 8).

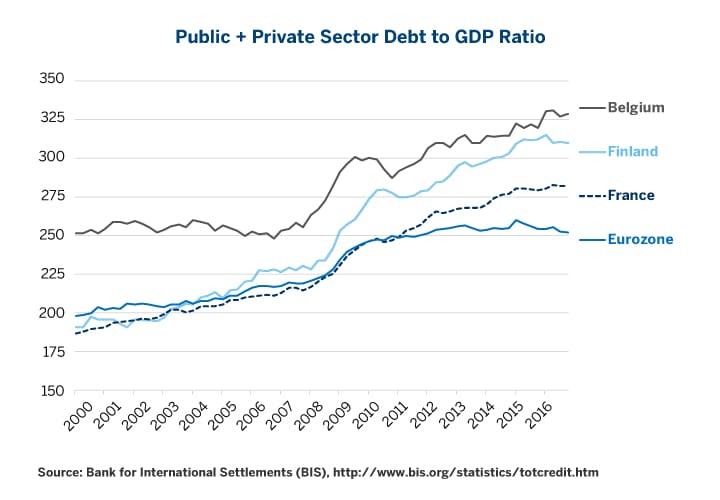

- Those who continue to ramp up their levels of debt (Belgium, Finland and France – Figure 9).

Figure 6: Ireland, Portugal and Spain are Using QE and Low Rates to De-lever.

{kind=link}

Figure 7: Greece and Italy are Using the Easy Monetary Environment as Life Support.

{kind=link}

Figure 8: Austria and Germany Remain the Savers and Lenders to the Rest of Europe.

{kind=link}

Figure 9: Belgium, Finland and France are Using Low Rates and QE to Party.

{kind=link}

For all the new regulations and relentless press coverage, the financial crisis failed to change the eurozone’s fundamental financial dynamics. Since its inception, Germany has been the lender to the rest of Europe. The reason is simple: prior to the creation of the eurozone, Germany was the wealthiest nation on a per capita basis and had the lowest borrowing costs. Germans borrowed at rates slightly below those in Austria, Belgium, France and the Netherlands, and at rates only one-third to one-half as high as the borrowing costs in countries like Greece, Ireland, Italy, Spain and Portugal (collectively referred to by the acronym PIIGS during the financial crisis). As the currencies converged into the euro, it was profitable for lenders in Europe’s core countries such as Germany to lend money to higher-yielding peripheral nations like Greece, Portugal and Ireland. This set off a decade-long virtuous spiral where growth in PIIGS exceeded that of Germany as they levered themselves to the hilt.

In 2008, that virtuous spiral turned vicious as rising yields in the peripheral countries pushed them towards insolvency while German bond yields plunged. Since then, Germany has continued to de-lever and it is alone among eurozone countries with a lower debt-to-GDP ratio today than before the crisis.

Ireland, Portugal and Spain have used the low-rate environment to begin de-leveraging. However, their debt ratios still exceed pre-crisis levels and their continued recovery relies upon cheap financing from the ECB. Each of them has also been helped by the past weakness in the euro and would be threatened by a continued rally in the common currency.

Greece, despite a series of bailouts and brutally austere budgets, has made no progress at all towards deleveraging. Italy, which was never bailed out by the government, also remains reliant on cheap financing from the ECB. Italy’s overall debt levels are about the eurozone average but its government debt is the second highest in the bloc, and bond markets continue to punish the country by making it one of the higher-yielding debt markets, making it expensive for Italy to borrow. Italy is also widely seen as having an undercapitalized banking system.

France, Belgium and Finland continued to lever up through early 2016, preventing Europe’s overall debt ratios from falling. This might bode poorly for their growth going forward; it also heightens their dependency on low borrowing costs.

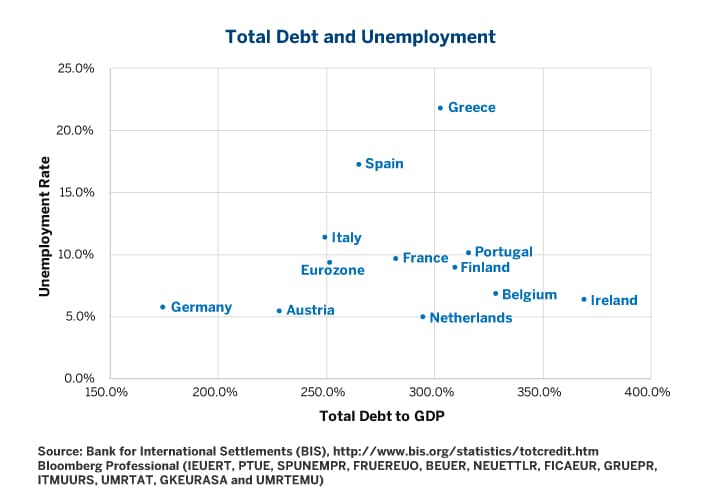

Europe’s highly varied debt levels make it hard for the ECB to implement an appropriate monetary policy for all its 19 members. Some nations, like Germany and Austria, have low levels of debt and unemployment and could probably have tighter monetary policy. The rest of the bloc still needs for interest rates to remain low for a long period. This is especially true for Europe’s most indebted nations, including Ireland, Belgium and Portugal, as well as the nations which suffer from the highest unemployment rates (Greece, Spain and Italy) (Figure 10).

Figure 10: Nations with High Debt, High Unemployment Require Low Rates for Longer.

{kind=link}

What is interesting is that QE doesn’t appear to have done much to narrow intra-European bond spreads or to boost the pace of Europe’s recovery. Spreads between Italian and German debt, for example, have changed little since the ECB began to ramp up its QE program in late 2014. Likewise, it Is not apparent that QE has given much of a pop to economic growth or to inflation. While economic growth remains solid, at least by Europe’s moribund standards, it does not appear to have accelerated much in response to QE. The same is true in the U.S., where the recovery that began in 2010 did not appear to get much of a boost from the second and third rounds of Fed QE.

As such, the ECB can probably wind down its QE program with relatively minimal risk. A QE unwinding might send rates higher in Europe and, by extension, elsewhere in the world as happened with the Fed’s 2013 ‘taper tantrum’ when then Fed Chairman Ben Bernanke signaled a slowing in the pace of QE. The corollary to the Fed’s QE2 and QE3 not having been particularly helpful to the economy is that the taper tantrum and the subsequent QE wind down have done nothing thus far to derail the U.S. recovery.

Higher bond yields will be welcome news for pension managers and others required to buy long-term debt. When a financial crisis occurs, somebody has to pay the price for it and that somebody is usually the lender. In Europe’s case, it was unacceptable for PIIGS to default since the banks, bondholders, ECB and International Monetary Fund didn’t want to write down the value of their loans. As such, Europe’s savers and pensioners, many of the them in Germany, are picking up the tab through extremely low interest rates. And low interest rates will probably persist for a while, especially because inflation remains mired at 1.3%, well below the ECB’s 2% target, despite years of low rates, QE and a tepid economic recovery.

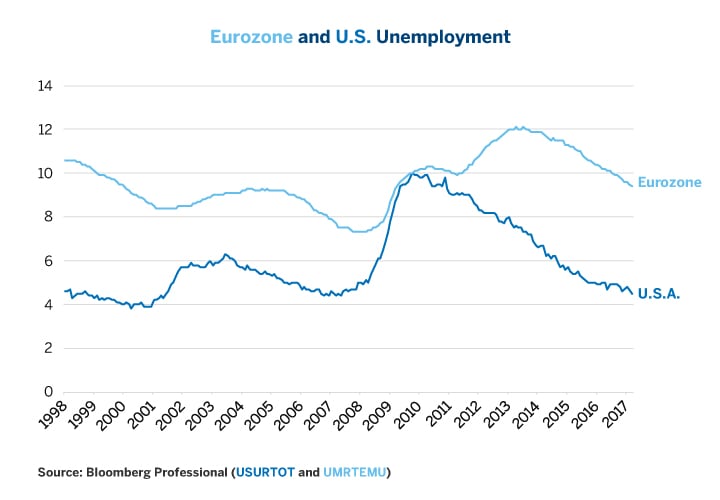

In the U.S., the Fed did not begin raising rates until unemployment fell to 5%, around its pre-crisis level. Europe’s pre-crisis unemployment rate was around 7.5%. Currently, eurozone unemployment is at 9.3% and falling by about 0.7-0.9% per year. If the recovery continues at its present pace without a major upswing in inflation, and if the ECB reacts to unemployment in a similar manner to the Fed, this implies that the ECB won’t be in a position to raise rates until sometime in 2019 (Figure 11).

Figure 11: Eurozone Unemployment Remains Well Above Pre-Crisis Levels.

{kind=link}

Given the distant prospect of any ECB policy tightening, the recent rally in the euro back to 1.17 to the dollar may have gotten a bit ahead of itself. The euro is vulnerable, both to a faster-than-priced tightening of U.S. monetary policy as well as a slower-than-priced normalization of ECB policy.

Bottom line:

- Divergences in debt levels within the eurozone create another impediment to the eventual normalization of ECB interest policy, but not necessarily to the tapering of QE.

- QE does not appear to have boosted the eurozone recovery, and while the tapering of ECB might boost bond yields around the world and the euro, it is unlikely to dent Europe’s recovery.

- Eurozone unemployment is falling at a pace that suggests that the ECB might take its first steps towards raising rates in 2019 or 2020.

- The essential debt dynamic in Europe has not changed: Germany still lends to a heavily-indebted periphery.

- Outside of Germany and Austria, debt levels are generally too high to sustain a significant tightening of interest rate policy.

Recommended For You

Interest Rate Products

Optimize your portfolio with Interest Rate futures and options at CME Group.