{kind=link}

Treasury Options Skews: Investment Signals or Noise?

Nearly all options markets exhibit some kind of natural skewness. For example, out-of-the-money (OTM) put options on equity index futures are typically cost more than OTM call options as investors typically fear a sudden fall in stock prices more than a sudden rise and, hence, are willing to pay more for protection to the downside than upside. In agricultural markets, skew tends to work the opposite way. On corn, soy and wheat options, for example, OTM call options are usually more expensive than OTM puts. Food buyers fear a sudden spike in the price of these goods in the event of a bad harvest more than farmers fear a sudden price decline in the event of an exceptionally good harvest.

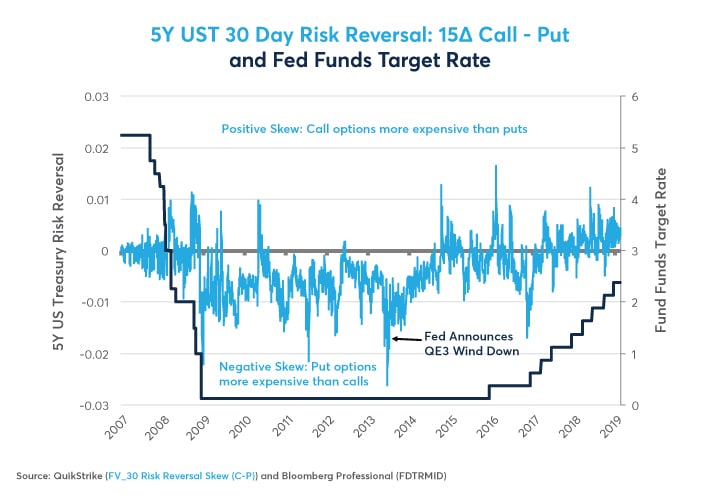

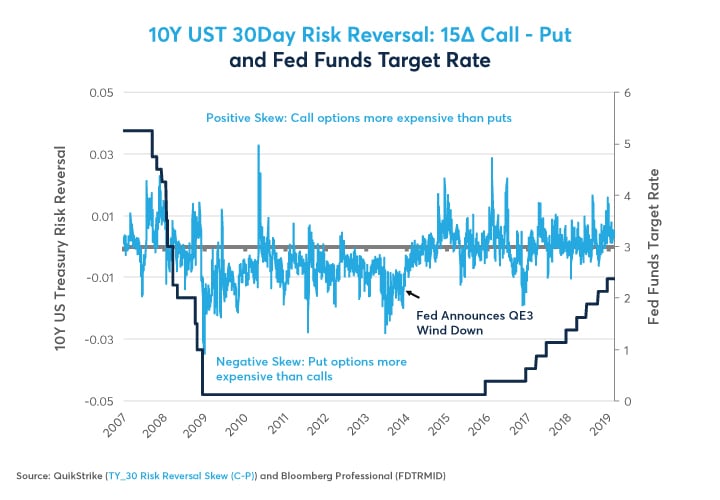

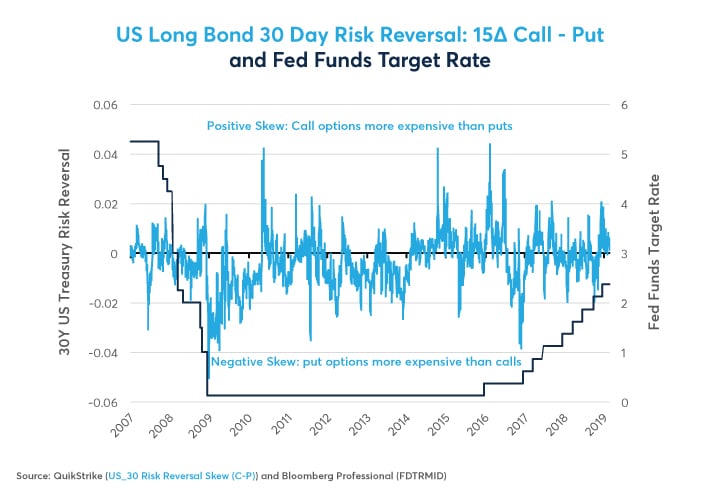

Treasury options markets are quirkier than equity or agricultural options markets. Generally, they are evenly balanced – at least when monetary policy is seen as having two-way risks. However, the combination of near-zero rates and the Federal Reserve’s (Fed) balance sheet expansion through quantitative easing (QE) caused five and 10-year U.S. Treasury options to skew sharply to the downside (OTM puts cost more than OTM calls) from 2009 through to 2013 when the Fed announced a tapering of its QE program. Since then, Treasury options traders have perceived upside and downside risks to be more balanced (Figures 1 and 2). This relationship has been weaker for options on long-dated U.S. Treasuries, which are less closely tethered to short-term interest rates and were not the primary focus of the QE program (Figure 3). Now that the Fed has normalized interest rate policy, or perhaps even significantly overtightened, risks may be building to the upside, especially if the Fed has to initiate an easing of monetary policy.

Figure 1: 5Y Treasury Options Skewness Tracked Fed Funds and QE.

{kind=link}

Figure 2: 10Y Treasury Options Skewness Also Follows Fed Funds and QE.

{kind=link}

This paper also addresses one additional question: is the degree of options skewness (also referred to as “risk reversal”) a useful indicator of whether U.S. Treasury prices are likely to rally or decline? For example, if OTM put options have become extremely expensive with respect to OTM call options, is that a sign that a Treasuries are likely to fall or is it a signal that they are oversold and likely to rebound? Likewise, if call options on Treasury futures become more expensive than normal vis-à-vis puts, is that typically a signal that Treasury prices are likely to rally or a warning sign that Treasuries are overbought and unusually susceptible to declines? As it turns out, more often than not over the past decade, it pays to listen to Treasury options traders.

Related article:

Figure 3: Fed Funds and QE Appear to Have Had a Weaker Influence on Long-Bond Options Skews.

{kind=link}

Looking at Skewness for Investment Decisions

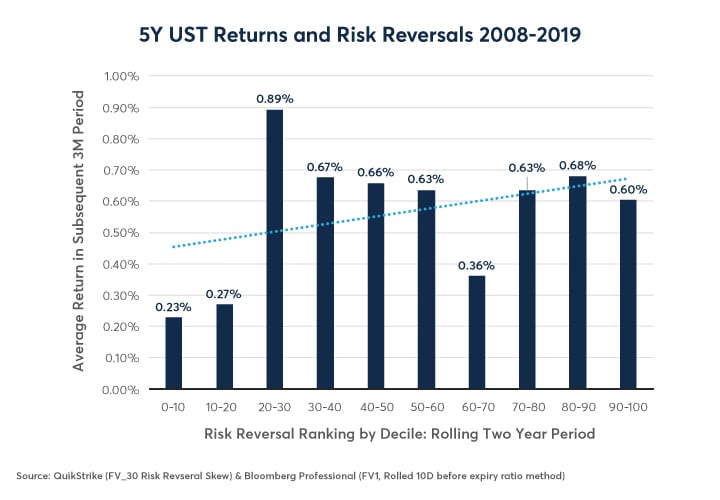

Do variations in skewness tell us anything about the future payoff of investing in U.S. Treasuries? Does extremely negative skewness send a buy or sell signal? What about extremely positive skewness?

To answer these questions, we indexed the skewness on a scale of 0-100 over rolling two-year periods and compared it to the return of the five-year, 10-year and long bonds versus the U.S. dollar (USD) in the subsequent three months (so there’s no look-ahead bias). For example, if the Treasury options skewness was the most skewed to the downside it had been during the previous two years, the index would have a reading of zero. If the Treasury options market was the most positively skewed that it had been during the past two years, the index would have a reading of 100. We then broke the results down into deciles and looked at the subsequent three-month performance of the reinvested Treasury futures rolled 10 days prior to expiry from 2008 until early 2019.

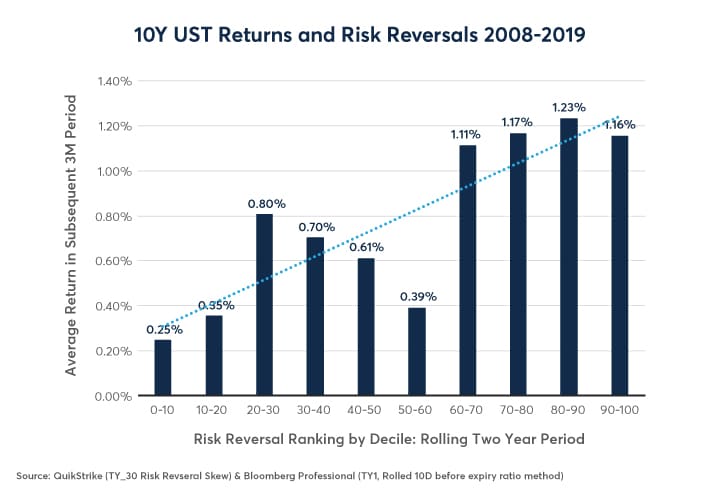

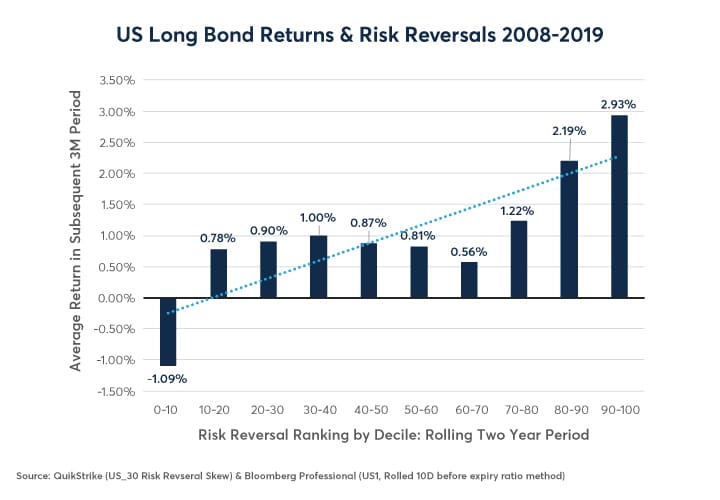

Over this 11-year period, the results are striking: Treasury options traders often provided useful warnings of coming periods of outperformance and underperformance in Treasuries. When Treasuries were unusually skewed to the downside, bonds often underperformed. This relationship was especially strong at the long end of the curve (Figures 4-6). When Treasury options were unusually skewed to the upside, bonds often outperformed. The above results should be taken with a large grain of salt. Like any such analysis, it’s time sensitive and past average relationships should not be expected to hold in the future. Nevertheless, options skewness might be something that Treasury traders, even those who only use futures, physical bonds or interest rate swaps, might want to be cognizant of as they manage their portfolios, especially when skewness has gone to extreme levels, one way or the other.

Figure 4: 5Ys Performed the Worst When Options Skewness Was Unusually Negative.

{kind=link}

Figure 5: 10Y Bonds Performed Best When Calls Were Abnormally Expensive Compared to Puts.

{kind=link}

Figure 6: U.S. Long Bonds had the Strongest Relationship to Options Skewness.

{kind=link}

Bottom Line

- Unlike equities or agricultural products, Treasury options don’t have a standard skewness.

- Treasury option skewness varies with QE and Fed Funds.

- Extremely positive skewness was often an indicator of better than average returns over the next three months.

- Extremely negative skewness often signaled an approaching period of underperformance.

U.S. Treasury Futures and Options

Take advantage of the liquidity, security and diversity of government bond markets with U.S. Treasury futures and options. Available on the 2-year, 5-year, 10-year, and 30-year tenors, U.S. Treasuries are standardized contracts on U.S. government notes or bonds that offer a variety of strategies to hedge or assume risk based on interest rate market exposure.