{kind=link}

Seven Factors that Drive the U.S. Dollar-British Pound Rate

AT-A-GLANCE

- GBPUSD tends to correlate positively with EURUSD

- Brexit-related politics played a significant role in influencing GBPUSD

- USD, EUR account for 80% of total foreign exchange reserves

- GBPUSD had a strong co-movement with oil benchmarks like WTI

- Investors expect BOE to hike rates at a slower pace than the Fed

In our recent article on the euro -U.S. dollar exchange rate (EURUSD), we identified four macroeconomic forces that influence the currency pair’s movements: 1) trade surpluses/deficits; 2) budget surpluses/deficits; 3) differences in economic growth rates and monetary policy, particularly with respect to investors’ expectations for future interest rate levels, and 4) the relative pace of economic growth. These factors also play a role in determining the exchange rate between the British pound and the U.S. dollar (GBPUSD), or “cable’ in trader jargon. However, GBPUSD also has three other key influences, which include:

- The EURUSD exchange rate, with which GBPUSD tends to be positively correlated

- The price of oil, which influences the trade deficits/surpluses of the U.K., U.S. and eurozone

- Brexit related politics, which may be fading in importance but played a large role in recent years.

GBP and its relationship with EUR

It’s difficult to understand the GBPUSD exchange rate without first understanding what is driving EURUSD (read our article here). The International Monetary Fund (IMF) estimates that as of Q1 2021, 59.5% of the world’s central bank currency reserves were held in USD and 20.6% in EUR. Together, the two currencies account for around 80% of total foreign exchange reserves. GBP was the fourth most widely held currency (behind the Japanese yen), accounting for 4.7% of global reserves (Figure 1). If one imagines the global currencies as a solar system, the USD is the star at the system’s center. EUR will be the system’s largest planet and the other European currencies, including GBP, are akin to moons that have eccentric orbits around EUR.

Figure 1: Forex reserves in GBP are a quarter of those in EUR and 1/15 those in USD

{kind=link}

Together, a moon and a planet have a common center of gravity, but being larger, the planet’s gravity has a greater influence on the behavior of the system. Within Europe, the eurozone’s GDP amounts to $11.8 trillion, compared with $3.1 trillion for the U.K. Their relative size is also reflected in trade flows: 44% of U.K. exports head to the eurozone, but only 16% of eurozone exports head to the U.K.

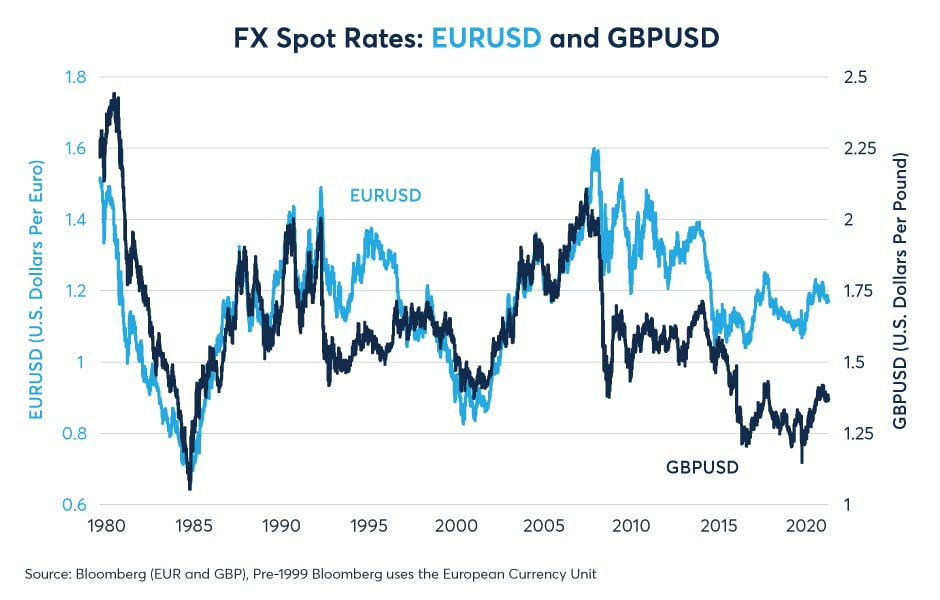

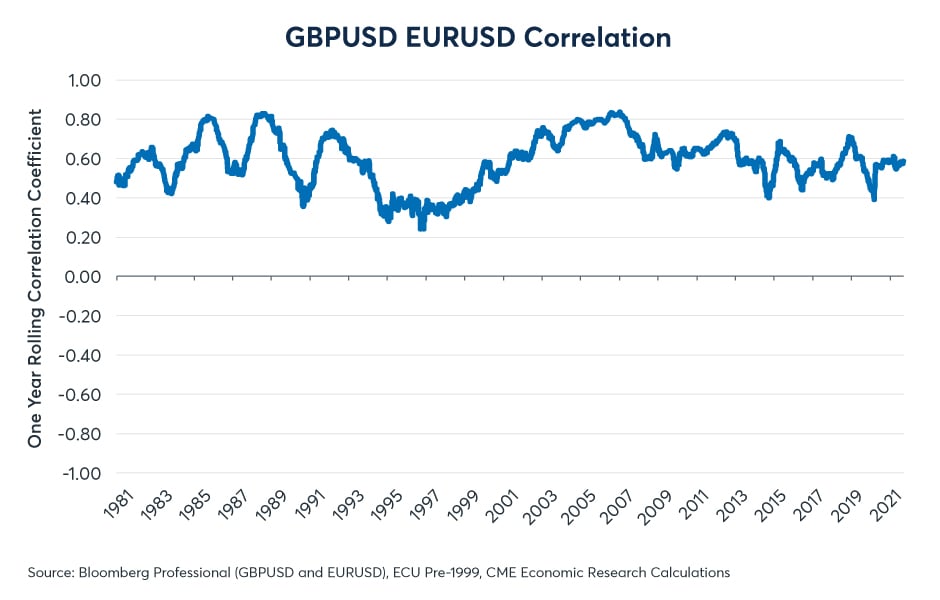

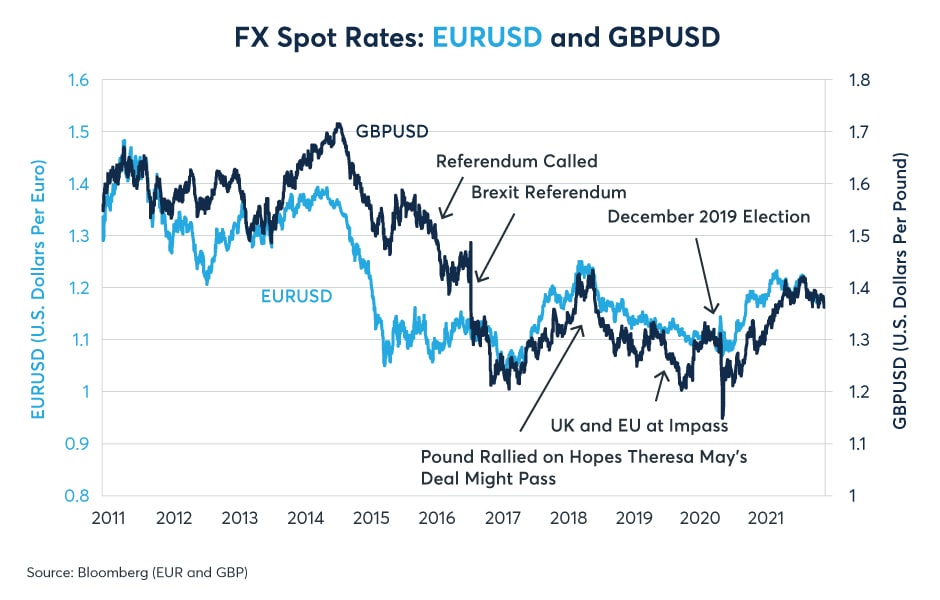

As such, perhaps its not surprising that EURUSD and GBPUSD exhibit both a strong co-movement (Figure 2), and have had a consistently positive one-year-rolling correlation since 1980 (Figure 3). When EUR rises or falls versus USD, it often pulls the pound along with it. The pound exerts some influence on EUR as well. However, the relative size of the two currency areas in terms of GDP, trade flows and central bank reserves is not equal, so GBP’s influence on EUR tends to be weaker than EUR’s influence on GBP. This much was evident in the aftermath of the 2016 Brexit referendum when the pound plunged 20% versus USD over a three-month period while EUR fell only a few percent.

Figure 2: EUR and GBP tend to track one another versus USD

{kind=link}

Figure 3: GBP and EUR have had a positive one-year rolling correlation for the past 40 years

{kind=link}

Oil and GBP

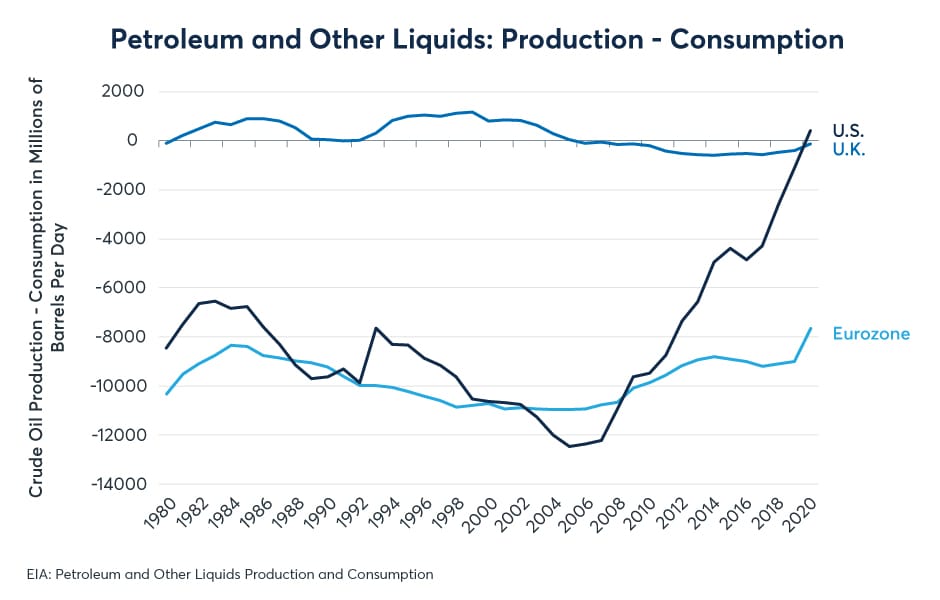

While GBPUSD may revolve around EUR to some extent, its orbit is an eccentric one that varies over time. Over the past several decades one British pound has bought anywhere from 1.7 euros (or at times more) on the high side to as little as 1.1 (or occasionally fewer) euros on the low side. Aside from having its own separate monetary and fiscal policy, the U.K. has one thing that the eurozone has never had: a significant quantity of domestically produced oil, thanks to the discovery and exploitation of North Sea crude.

When it comes to oil, the U.K. differs from the U.S. as well. Although the U.S. is also a large oil producer, before 2020 it was a net oil importer. And before the advent of large-scale fracking circa-2008, U.S. imported roughly as much crude oil as Europe.

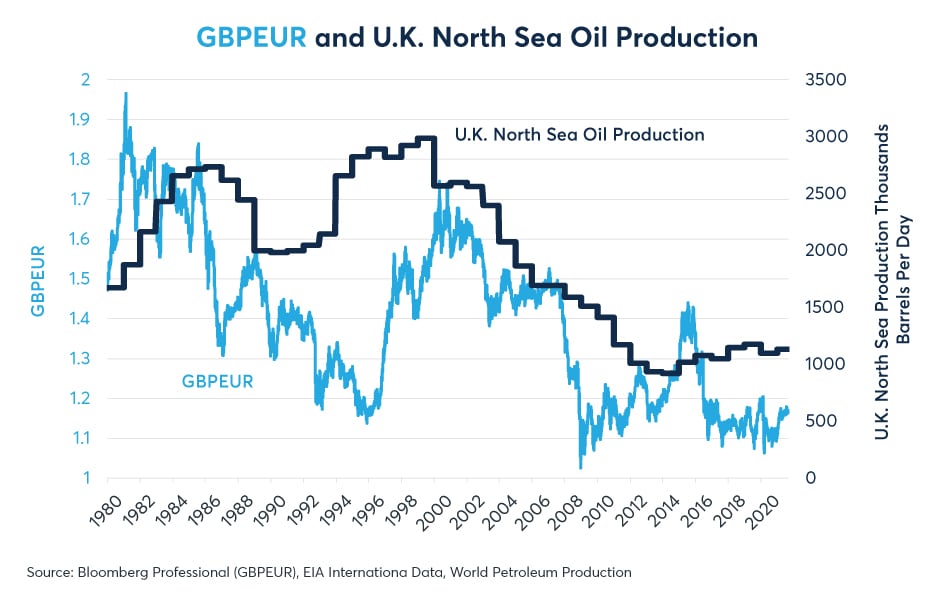

By contrast, from 1981 to 2005 the U.K. was a net oil exporter (Figure 4). Since 2006, the U.K. has been a net oil importer, but its oil imports are much smaller than those of the eurozone. The U.K.’s North Sea oil production peaked in 1999 and steadily shrank until 2015 before stabilizing and increasing slightly during the past six years. The shrinkage and subsequent stabilization of the oil production explains to some extent GBP’s decline versus EUR (Figure 5).

Figure 4: The U.K. has often been a net oil exporter in contrast to Europe

{kind=link}

Figure 5: Declining North Sea oil production may have weighed on the GBPEUR

{kind=link}

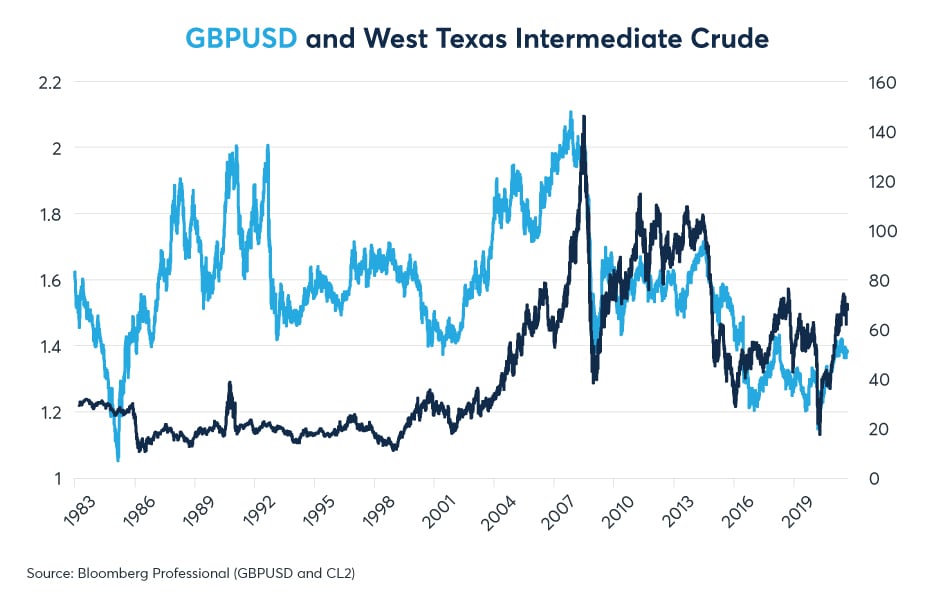

Since the early 2000s, and especially since 2008, GBPUSD had a significant degree of co-movement with oil benchmarks such as West Texas Intermediate (WTI) (Figure 6). GBP tended to strengthen versus USD when oil prices were high and fall when oil prices declined. Now that the U.S. is a net oil exporter (at least for the moment), it is not clear if GBPUSD’s correlation with oil prices will persist.

Figure 6: Since 2000s, and especially in 2008, GBPUSD often moved with WTI

{kind=link}

Brexit and GBP

During the past six years since the U.K. government called a referendum on its membership in the European Union (E.U.), it’s been difficult to ignore the role of politics in influencing the currency. GBP began selling off sharply versus USD and EUR in 2015 when the referendum was called, and then fell sharply against both currencies in the immediate aftermath of the June 2016 Brexit vote. It then recovered significantly in 2017 on the hopes that a deal would be reached, but then fell in 2018 and 2019 when the U.K. Parliament repeatedly voted down various U.K.-EU separation agreements. It fell sharply one last time when the results of the December 2019 elections made clear that Brexit was, in fact, going to happen. As the E.U. and the U.K. reached and implemented the separation agreement in 2020, GBP drifted higher (Figure 7).

Figure 7: Brexit politics has played a major role in GBPUSD over the past six years

{kind=link}

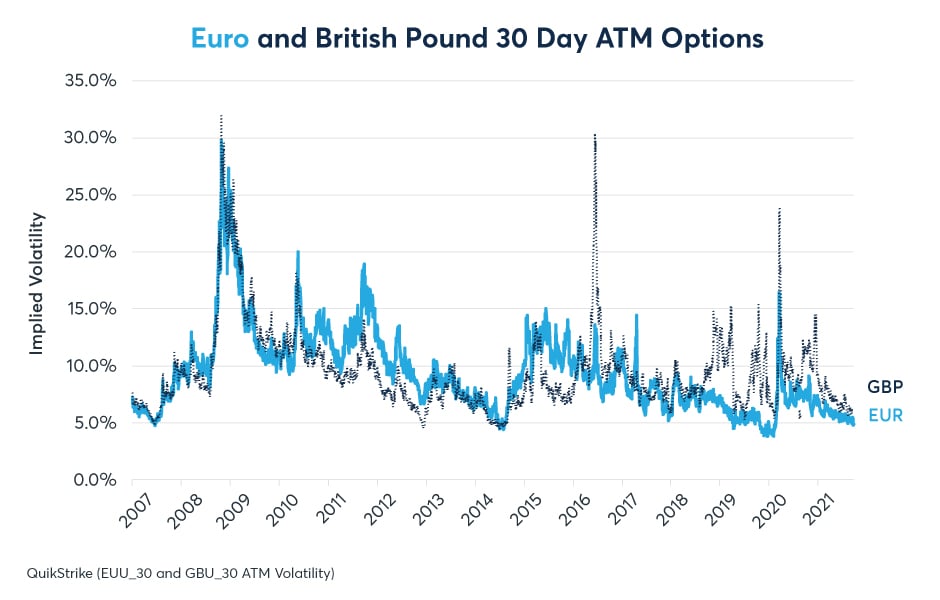

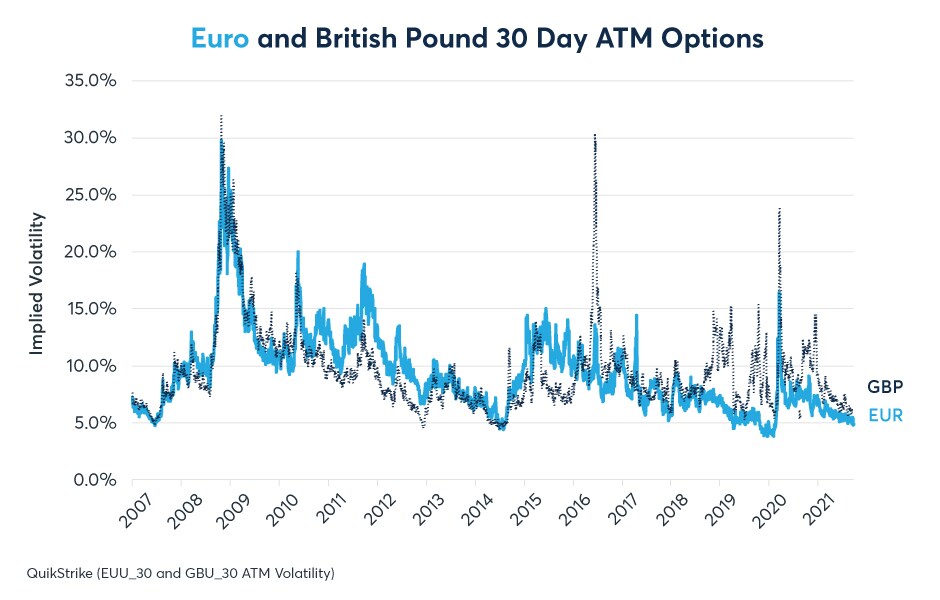

The various Brexit events and negotiations created repeated spikes in implied volatility for GBPUSD that were not reflected in EURUSD. Before the Brexit debate began, GBPUSD most often traded at lower implied volatilities than EURUSD. Since Brexit came into focus in 2015, GBPUSD options have most often traded at significant implied volatility premiums to EURUSD options (Figure 8). This continues to be the case today perhaps because there are many lingering, unresolved issues related to Brexit, including the ultimate resolution of the U.K. border and Northern Ireland, the possibility of a second Scottish independence referendum as well ongoing trade negotiations between the U.K. and the E.U.

Figure 8: Pre-Brexit GBP options often traded at lower implied volatilities than EUR options

{kind=link}

GBPUSD and the Four Major Macro Forces

The influence of EUR, oil and Brexit has sometimes obscured the importance of the other economic forces that might otherwise have played a larger role in influencing the currency pair:

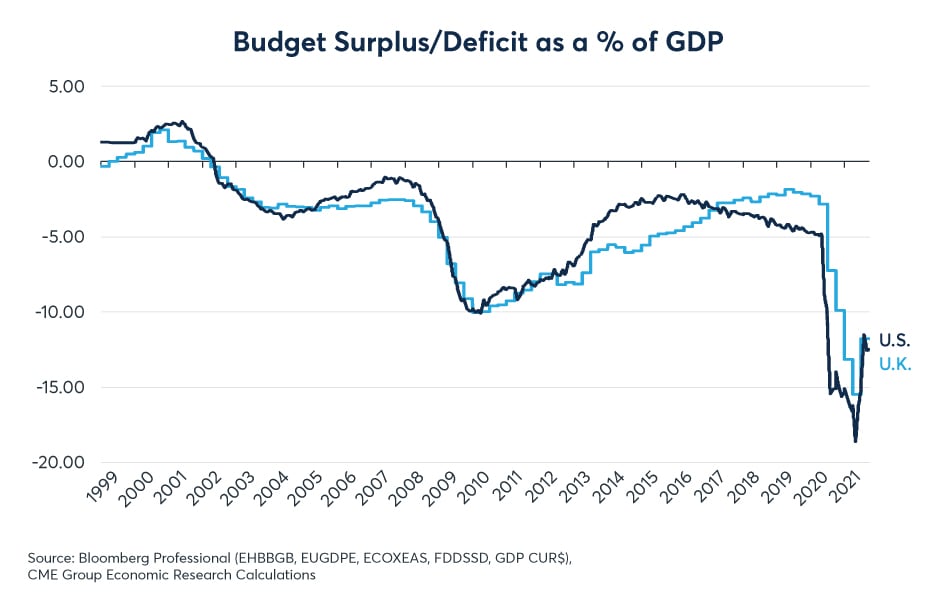

Relative fiscal positions: For starters, the U.K. and U.S. fiscal positions have most often been fairly similar (Figure 9) and their divergence hasn’t done an especially good job of explaining the variation in GBPUSD (Figure 10).

Figure 9: With exception to the 2015-19 period, U.K. and U.S. fiscal policy has moved in tandem

{kind=link}

Figure 10: U.K. versus U.S. fiscal policy has done a poor job of explaining GBPUSD variation

{kind=link}

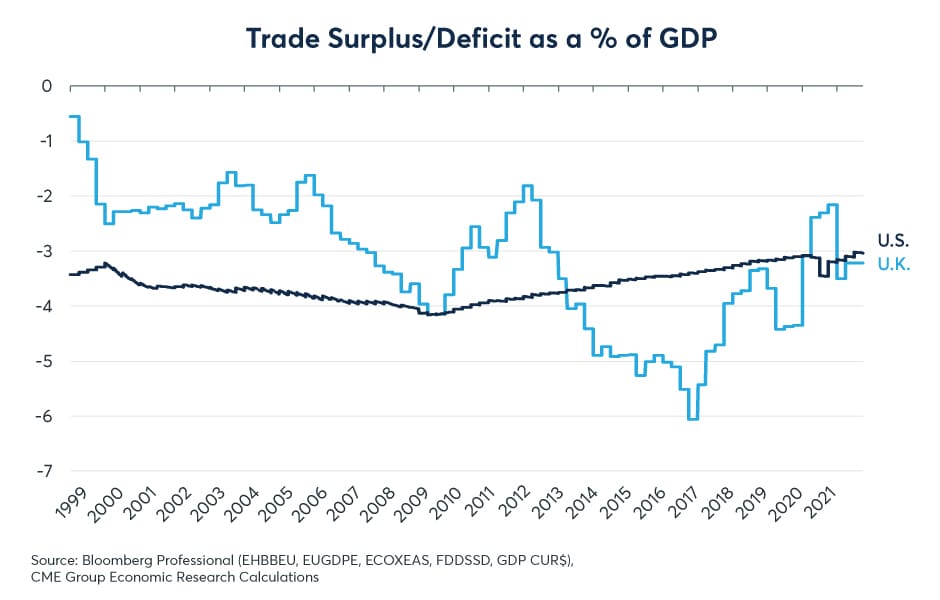

Relative trade picture: That said, the relative trade picture between the U.S. and the U.K. has varied significantly over time and does explain to some extent the variation in GBPUSD: the country with the bigger current account deficit usually has the weaker currency (Figure 11).

Figure 11: Size of U.K. trade deficit has varied more than that of the U.S.

{kind=link}

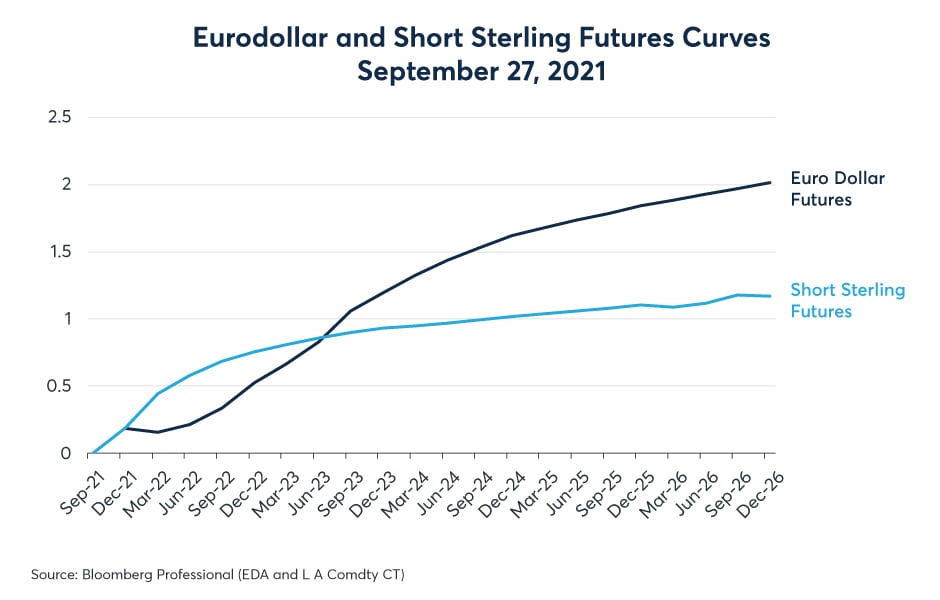

Monetary Policy: One year forward anticipated interest rate differentials have done a pretty good job of explaining the variation in the currency pair (Figure 12). Judging from Eurodollar and Short Sterling futures, investors expect the Bank of England to get off zero rates a bit more quickly than the Fed, but to then pursue a slower pace of rate increases than its American counterpart (Figures 13 and 14).

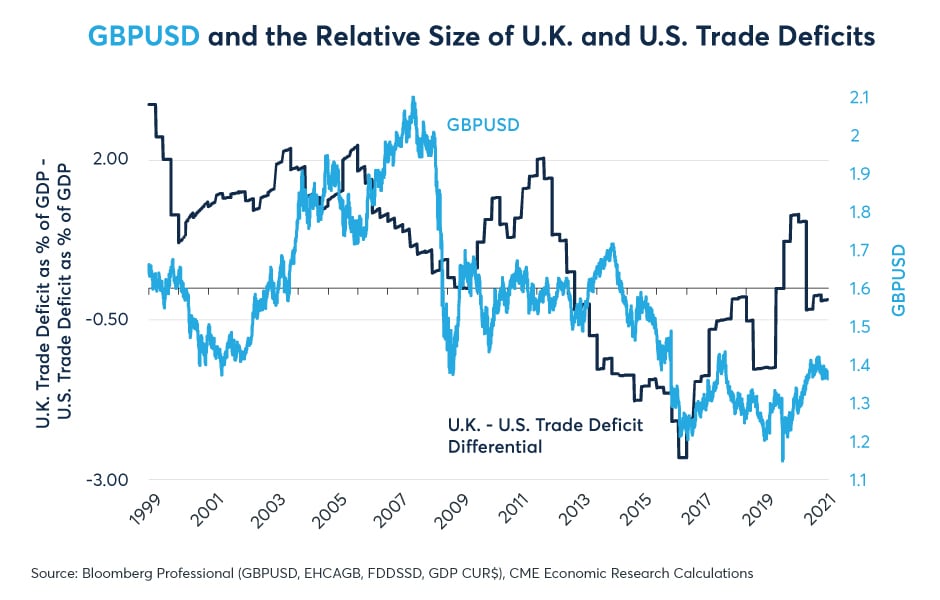

Figure 12: Relative trade picture explains some of the variation in GBPUSD

{kind=link}

Figure 13: Anticipated future interest rate differentials correlate strongly with GBPUSD

{kind=link}

Figure 14: Investors anticipate a faster lift off of U.K. rates than in the U.S.

{kind=link}

Gap in Pace of Economic Growth: Finally, since the Brexit vote, the U.K. economy has had the weakest growth of any European economy and has underperformed growth in the U.S. well. This may explain why the GBP has thus far failed to recover towards higher levels versus both currencies.

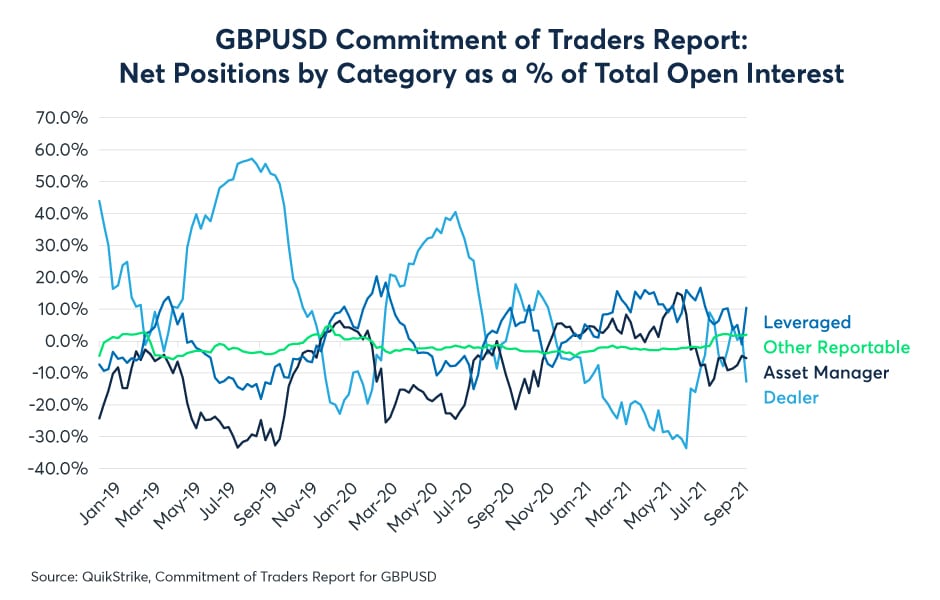

What the Commitment of Traders (COT) Report Tell Us About Positioning

For the moment, investors of all stripes appear to have relatively neutral positioning on GBPUSD (Figure 15). This may reflect the lack of a recent trend in the currency pair and the uncertainty as to how the pandemic, Brexit and the other forces that act on it will eventually turn out.

{kind=link}