{kind=link}

Q4 U.S. Dairy Market Key Drivers

Feed Prices & Dairy Farm Margins

Summary: Grain harvest is in full swing in the US with bumper crops expected for corn and soybeans. Futures prices for each are unchanged from last month and the relatively low feed costs mean an improving margin picture for dairy farms.

By September 30, 26% of the corn and soybeans were harvested, both above the 5-year average pace. Weather through October will be watched as rain could bring harvest delays. There is a big crop in the field, which was confirmed by the latest grain report on September 12. The forecasted yields, production, and ending stocks for both corn and soybeans were increased from the August estimate and were mostly above pre-report expectations. Grain prices immediately moved lower, but have recovered in the past few weeks as more positive trade news has surfaced. The old adage is “big crops tend to get bigger”, so the outlook for grain prices into 2019 is for continued cheap feed. The projected dairy farm (MPP) margin in 2019 is expected to improve vs. 2018, but will not get back to 2017 levels. As a result, most US dairy farms should return to modest profitability, but probably won’t generate enough extra profit to fill in the holes created over the last few years.

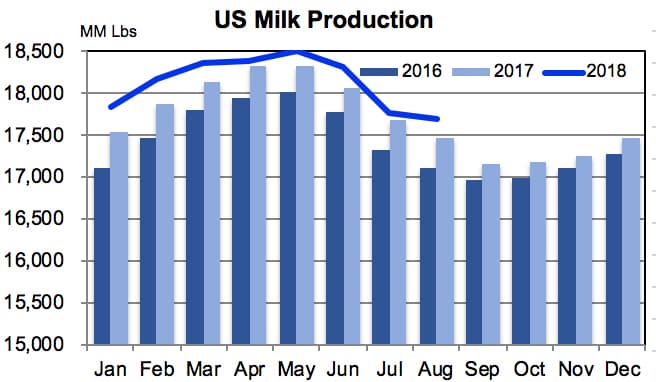

Milk Production

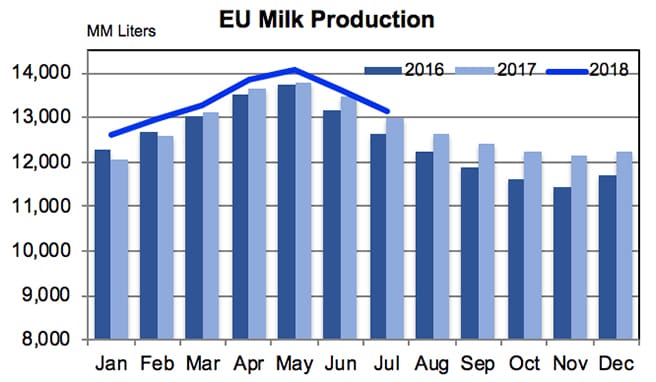

Summary: Prospects for milk production have improved from last month, casting a bit of a bearish pall over dairy markets. The impact from the summer drought in Europe will take months to fully develop, but milk production growth has slowed in several key countries. Overall, it appears global milk supply growth will slow in 2019 setting the stage for a recovery in prices.

What a difference a month makes. Following the small increase in July US milk production and drop in cow numbers, it appeared the long-awaited dairy herd contraction was starting. However, the August report showed milk production rebounding to 1.4% growth and cow numbers increasing 5,000 during the month despite a strong slaughter pace. While USDA can revise these numbers in the next report, for now, it looks like cow numbers will remain at historically high levels. One thing to watch is the large inventory of replacement heifers entering the herd. Another is that despite headlines of farm sellouts, there continues to be farm expansions in several parts of the country. In short, it doesn’t appear the US dairy herd is going into contraction mode following a dip in cow numbers in July.

{kind=link}

{kind=link}

In Europe, milk production was up 1.5% vs. year ago in July, but is expected to fall below year ago levels by Q4, in part due to strong year-over-year comparisons. Hot, dry weather has taken a toll on milk output in some countries, while others have bounced back. Preliminary data for August Irish milk supplies grew 4% vs. prior year, while the UK (-1%) and Netherlands (-3%) remained weak. In weekly data from mid-September, German milk production was about 1% below last year and output in France was down nearly 2%. In 2017, Q4 milk output grew a whopping 5.4%, so it should be no surprise when 2018 production falls short of that. Add in the uncertainty from the summer’s drought and lingering issues with feed price and availability and it points to lower production into 2019. However, dairy farmers are resilient and they often prove forecasts wrong. Milk prices are at a profitable level and Friesland Campina recently increased their payout 1 cent to €0.38/kg. Others could likely follow as it is in line with current spot prices for milk. In summary, higher milk prices will help offset higher feed costs, but the drought impacts are a wild card.

Milk production in Oceania continues to be a mixed bag. Positive weather conditions have helped New Zealand to get off to a solid start with August production up 4.7% vs. year ago. However, the drought in Australia is worsening and the latest data show milk production was down 4% vs. year ago in July. The next watch-out is the potential El Nino in the region. However, only three of eight climate models are currently forecasting an El Nino event, and if it develops, the impacts wouldn’t be seen until late 2018. The stronger output from NZ should more than offset the weakness in Australia, so modest growth is currently expected from Oceania.

USMCA (aka NAFTA 2.0)

After a long wait, a renegotiated US-Mexico-Canada free trade agreement has been concluded and now moves to ratification by each country. It is important to note just signing a trade deal does not bring it into force. Each country’s legislative bodies need to ratify the new trade pact. For Mexico, the current President wants to sign it before he leaves office on November 30. In the US, Congress requires 60 days to study the bill before the Trump administration can sign it. However, Canada is saying they have no deadline, so their timeline is uncertain. For the EU-Canada trade agreement (CETA), it was signed on October 30, 2016, but did not go into force until September 21, 2017 after going through the legislative process. For TPP, Canada signed on March 8, 2018 and it could be before the Senate before the end of the year. One likely scenario for the USMCA is an order authorizing the signing could be in late November with a formal ratification by both chambers of Parliament by mid-2019.

So what does the new US-Mexico-Canada free trade agreement (USMCA) mean to US dairy markets? I believe it is directionally positive as it removes the uncertainty of trade prospects with two important export customers for US dairy products. The resumption of normal trade with cheese between the US and Mexico, assuming they drop their tariffs back to pre-July levels, will be positive for US cheese exports and prices. The reduction of Canadian SMP exports is positive for NFDM prices. The elimination of class 6 and 7 milk, along with the small increases in market access, are positive in that anything is better than nothing, but it will take time to sort out the details on what this really means to US exporters and markets.

Dairy Market Outlook

Summary: While milk supplies are tightening, ample stocks remain for most dairy products and prices are expected to remain near current levels in Q4. Less milk in 2019 should result in directionally higher prices for milk and dairy products, but hurdles remain.

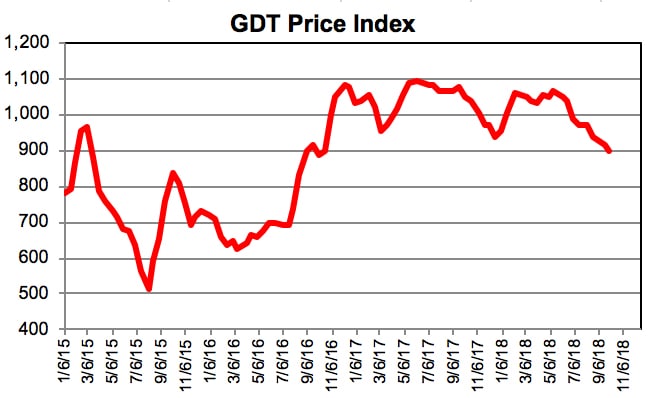

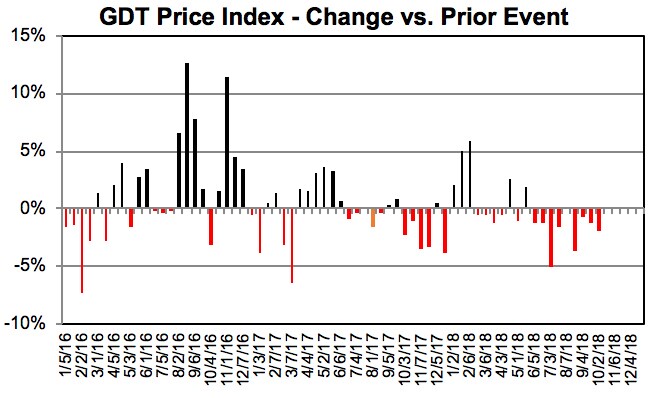

Lower milk supplies in the US and Europe are providing some bullish sentiment in the market, but abundant stocks (especially milk powder) provide a drag on prices. The net effect is continued range-bound prices for most products for Q4. A good start to New Zealand’s production season along with a lack of urgency from buyers has resulted in the GDT index sinking to the lowest point in two years this week. Looking to 2019, modest growth in milk supplies should support prices, but a key risk is the strong US dollar, which will reduce the purchasing power of key importers.

{kind=link}

{kind=link}

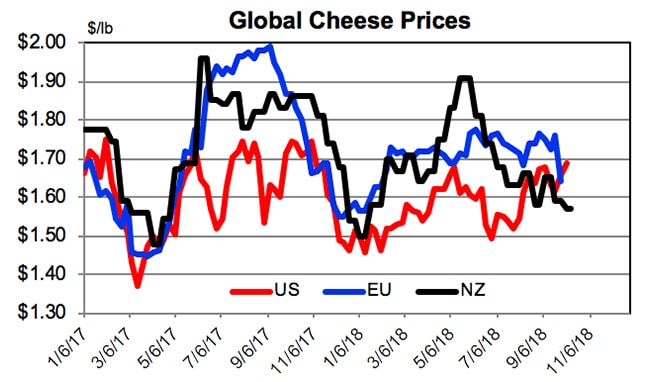

Cheese

Summary: Not much has changed in the cheese market over the last few months. Cheese prices remain range-bound in the $1.50-1.60’s, amid weakening global prices, with the potential for brief periods in the $1.70’s during the fourth quarter and a continued wide block-barrel spread.

The tendency for US cheese prices in Q4 is to move up rather than down given seasonal supply and demand conditions. CME block cheese made a 1-day run to the mid-$1.70’s to start October, but quickly fell back into the $1.60’s. Expect more of this in the next few months. In sharp contrast, barrel cheese has struggled to get out of the $1.30’s. Market fundamentals remain balanced. August cheese production was up 2.8% vs. prior year and August 31 stocks were 26 million lbs. (+1.9%) above year ago. Domestic demand is reportedly strong while exports have faded a bit due to the Mexican tariffs.

Global cheese prices have weakened over the last month. GDT prices have fallen in sympathy with other NZ products. European prices are also coming under pressure as a recent report showed cheese stocks at the end of July at a 7-year high due to higher production and stagnating exports. With European and New Zealand prices in the $1.50’s and $1.60’s, US prices won’t be able to trade above that for long lest they lose competitiveness in export markets.

{kind=link}

{kind=link}

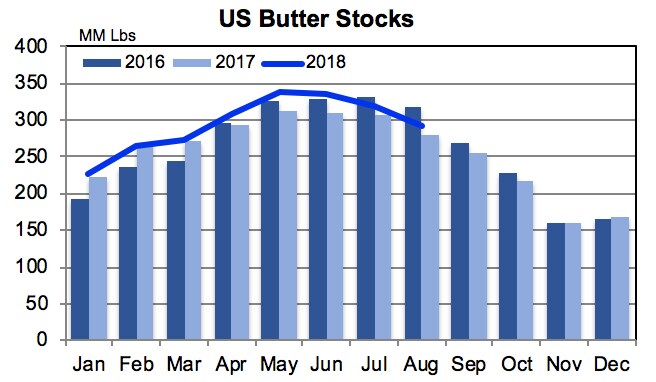

Butter

Summary: US butter prices have also been range-bound between the upper $2.10’s and mid-$2.30’s for the last several months. After holiday demand subsides by mid-November, lower NZ and falling European prices are expected to pressure the US prices lower by the end of the year.

CME butter prices are showing some seasonal strength heading into peak holiday demand. But stocks remain above year ago levels, and with an average draw-down, will be more than ample to finish the year. August butter production was up 2.1% vs. year ago after falling 0.8% in July. August exports were stronger, but amount to only a small portion of US production.

{kind=link}

{kind=link}

While US prices remain range-bound, global prices are retreating. GDT prices for NZ butter have fallen 16% since early August and hit $1.82 on October 2 – the lowest price in 2 years. Stronger milk output in NZ to start the season has put downward pressure on butter and AMF prices on GDT. In Europe, the recent Milk Market Observatory report showed butter stocks at the end of July remained relatively low, but above prior year levels. The EEX price has dropped to $2.62 (€5058/MT) – the lowest price since early April. Further weakness is expected with futures currently trading in the mid-€4000’s ($2.30-2.40’s) through next September. While the outlook is bearish, the impact of the recent European drought could be felt by the butter market more acutely than others. Assuming butter-powder plants get shorted when milk tightens up, less butter production would result in fewer butter stocks, and therefore, higher prices.

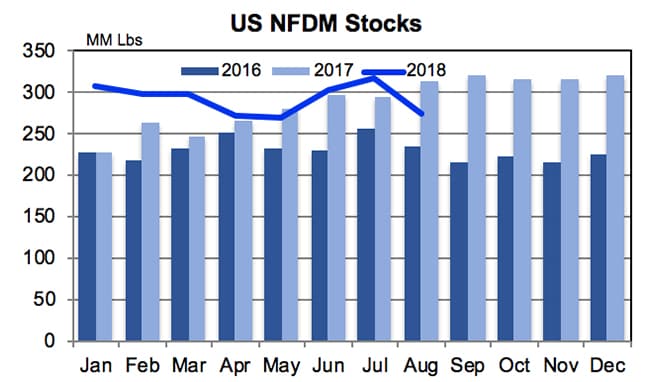

Milk Powders

Summary: Prices for SMP/NFDM from the 3 main exporting regions have converged and are forecasted to trade sideways in Q4. While some fundamentals point to a market swinging towards balance, stocks remain heavy and the EU intervention stocks look to hang around for another year.

In the US, CME NFDM prices rallied above $0.90/lb. briefly before falling back into the mid-upper $0.80’s. August production was down 6.1%, which was the largest % drop since January 2016. NFDM production was 10% below last year while SMP output increased 6%, indicating strong export demand. Stocks declined 42 million lbs. during the month of August and stood 12% below last year on August 31, the biggest gap since June 2016. This helps explain the rally from late July to early September. With that said, stocks remained well above 2016 levels. August exports were strong and domestic demand is reportedly solid. But, the elephant in the room continues to be the aging mountain of SMP stocks in the EU intervention program. The 2 most recent tenders were disappointing as the volume was much lower than earlier sales and the minimum price was unchanged around $0.65/lb. The EU Commission has additional tender offers planned in Q4, but it remains to be seen if there is enough demand to make a significant dent in the roughly 275,000 MT of SMP left in intervention. More than likely, these stocks will continue to overhang the market through 2019. At some point, they become irrelevant, but that’s been said for the past year.

{kind=link}

{kind=link}

Whey Products

Summary: Despite Chinese tariffs on US whey exports, prices in the whey complex continue to move higher on strong demand and tight stocks.

Tariffs? What tariffs. On the surface, US whey products had the most to lose from the retaliatory tariffs from China, but dry whey prices have steadily marched higher. The loss of a Midwest plant tightened supply in August along with a shift to higher protein products. Total US dry whey production during August was down 15% vs. prior year. Stocks were 27% below last August, but fell only 4.5 million lbs. vs. a nearly 13 million lb. drop in production. This implies demand might not have been strong as initially thought. Reported prices in the US are in the low-mid $0.40’s, yet the CME price is in the mid-$0.50’s with more gains possible. A headwind for US prices is the recent drop in European prices and steady NZ prices in the mid-$0.40’s. The rally in dry whey prices has surprised most people, so further gains cannot be ruled out.

{kind=link}

{kind=link}

Disclaimer: Information contained within is not guaranteed, is the opinion of the mccully group, llc, and is intended for informational purposes only. Commodities trading involves risk and is not suitable for everyone. Nothing contained within constitutes a solicitation to buy or sell derivative contracts. Trading futures/options contracts should be done with licensed professional brokers. The mccully group, llc is not a licensed commodity broker nor trades in commodity futures markets.