{kind=link}

Q1 Dairy Market Outlook

Feed Prices & Dairy Farm Margins

Summary: Feed prices have been stable, and the outlook is for improved margins for US dairy farms in 2019.

Grain futures prices have remained in a narrow range over the last month as is common in post-harvest trading following large crops. Corn futures prices are currently between $3.75-4.00/bushel while soybean meal is trading between $310-325/ton. The corn price is slightly higher than the last 5-year average while soybean meal is lower. So, the total feed cost for 2019, as reflected in the Margin Protection Program calculation, is very close to the 5-year average and below the 10-year average. Combine that with higher projected milk prices in 2019 and the result is a net margin that is $1/cwt or higher than 2018.

While a welcome improvement, the extra $1/cwt in the milk check will be insufficient for most US dairy farms to catch up from poor margins for most of 2018. Weekly dairy cow slaughter has been running well above year ago levels for the last few months reflecting the unprofitable economics on dairy farms. This should result in a continuation of the downtrend in overall cow numbers. In contrast to the US, dairy farmers in other regions are relatively profitable. In Europe, the average milk price moved up to €36 per 100 kg in November. In New Zealand, Fonterra lowered their projected payout to $6 per kg milk solids vs. an average breakeven near $5. Positive margins for farmers in both regions should be supportive to additional milk growth in 2019.

Milk Production

Summary: Milk production growth has slowed in three key regions – Europe, US, and New Zealand.

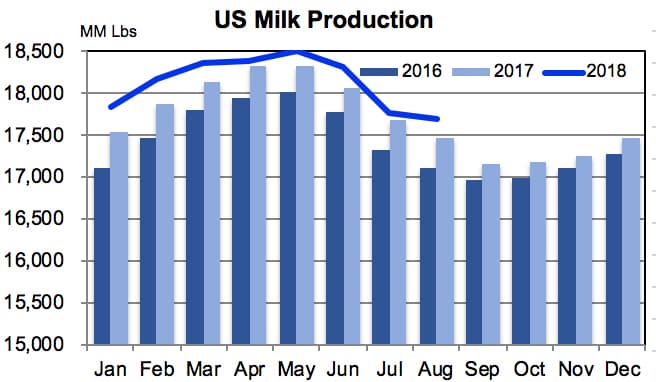

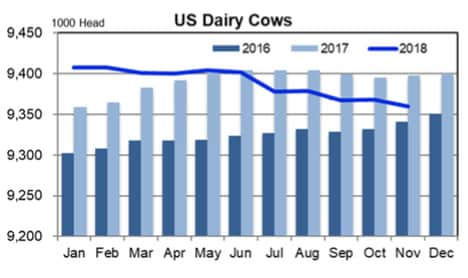

Milk production growth in the US in November was up only 0.6% vs. year ago. Eleven of the top 23 states posted declines vs. year ago with the largest losses coming from states in the eastern half of the country. However, growth in the West more than made up for weakness in the East. Cow numbers declined another 8,000 head and are at the lowest point since January 2017. With improving on-farm economics, the rate of culling and sell-outs should slow, but it might be spring before cow numbers level off. US milk production is forecast to grow around 1% this year. In the past, supply growth of 1% or less was not sufficient to meet domestic and export demand and prices moved higher. This is a watch-out for 2019 as the supply-demand balance is expected to be tighter than the last few years.

{kind=link}

{kind=link}

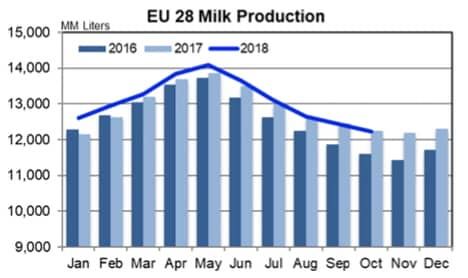

In Europe, milk production declined slightly for the second straight month. October production was down 0.2% vs. last year’s strong growth. The largest volume losses came from France (-4%) and the Netherlands (-5%), but were offset by growth in Ireland (+20%) and Poland (+3%). Germany, the largest milk producer in Europe, was down about 0.5%. Output continued to move lower in November with the Netherlands falling 7% below last year and weekly data pointing to 2% and 4% losses in Germany and France, respectively. The feed situation and lingering effects of last summer’s drought continues to be a watch-out in some areas. However, milk prices are mildly profitable for most farms, so year-over-year growth is expected to continue at around 1%, close to the long-term average.

{kind=link}

{kind=link}

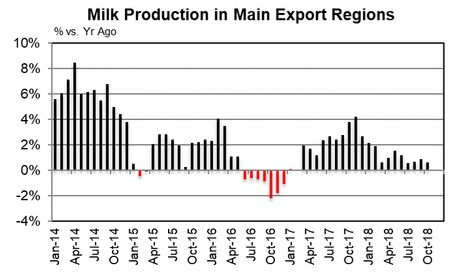

With milk production in both Europe and the US slowing, supplies from the three major export regions grew at only 0.7% over the last three months. New Zealand got off to a very good start vs. last year’s poor early season. However, the year-over-year comparison slipped from around 6% in September and October to only 1% in November. With Australia suffering through another drought, Oceania output is expected to post only modest increases vs. last season. This is likely not enough to offset weaker growth in Europe and the US and sustain the global demand as witnessed by the drawdown in stocks of major dairy products in recent months.

Dairy Market Outlook

The tone of the global dairy market has become directionally more bullish to start 2019. For the first time since late 2015, the market soon won’t have the price suppressing SMP intervention stocks in Europe to deal with. At current pace, they will be depleted in February following the large sales in December and January. Milk supply growth has slowed in the major production regions and buyers have become more aggressive as prices start to tick higher. However, this isn’t 2013-14 by any means. The global economy is starting to feel wobbly and US stock market indices portend trouble ahead with economists talking more about a mild recession later in 2019 or 2020. Lower oil prices cut both ways – it can be a sign that economic growth is waning and oil exporting countries have less money to buy stuff with (bearish for dairy prices). However, it is bullish for dairy prices in more energy-dependent countries – people will have more money to buy things vs. paying for gas for the car or their utility bills. And trade wars are usually not helpful for economic growth. A resolution to US disputes with Mexico and China would be bullish for dairy markets.

China’s appetite for dairy, and the Chinese economy more broadly, will be a key driver for dairy markets in 2019. With reportedly declining stocks and lower domestic milk supplies, the pace of imports has been increasing in recent months. Imports of SMP in November increased 69% versus last year and were 56% higher than October. However, given higher tariffs, the US share of sales fell. Whole milk powder (WMP) imports were 29% higher than last year and were the largest for the month since the record-setting volume in 2013. As usual, New Zealand captured the majority of sales accounting for 87% of the total. While smaller volume than milk powder, China’s imports of cheese also moved higher. Imports were up 12% from last year with total purchases of 21 million pounds. Chinese whey imports dropped 3% from last year with total shipments just under 100 million pounds. The US share of imports fell dramatically – from 51% last year to 21% in 2018 – a direct result of higher tariffs. If Chinese imports continue to grow at double digits, it will be supportive to global dairy prices.

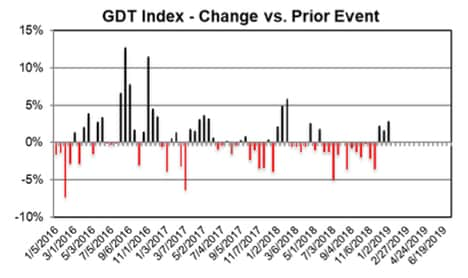

After sliding to the lowest level in over 2 years, the GDT index has increased in each of the last three events. On January 2, the index hit the highest point since mid-September. Volumes were lower for WMP and SMP, which likely contributed to some of the price strength. The uptrend in prices is expected to continue given tightening global supply and demand conditions and stepped up Chinese buying.

{kind=link}

{kind=link}

Cheese

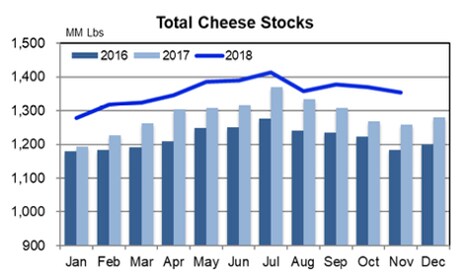

Summary: CME cheese prices appear to have stabilized after falling to the lowest level since May 2016 amid strong production and high stocks.

{kind=link}

{kind=link}

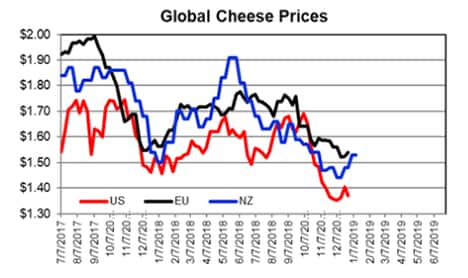

The US cheese market continues to languish under heavy stocks. Domestic demand has been decent, but not enough to make up for the slowdown in exports from earlier in the year. November 30 stocks were nearly 8% higher than year ago and the drawdown since July was 20MM lbs. less than average. In short, there is plenty of cheese around and stocks are expected to continue to exceed year ago levels. On its own fundamentals, CME block cheese prices are forecasted to trade in the $1.40’s and $1.50’s into Q2 and then the $1.60’s by May. Strength in the butter and NFDM markets will be supportive to cheese prices, so those markets bear watching. In addition, any increases in global cheese prices will be bullish for US prices as it would make US cheese more competitive in export markets.

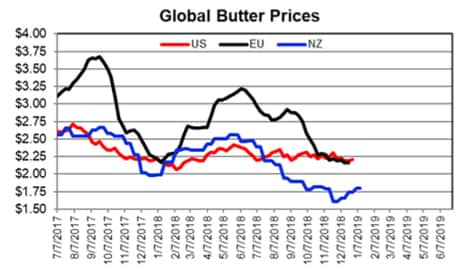

Butter

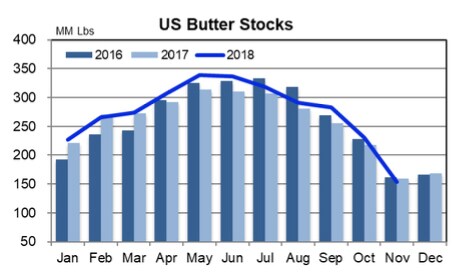

Summary: Global butter prices have diverged with US prices now trading at a premium to Europe and New Zealand. US butter stocks hit a 3-year low in November and cream supplies have tightened.

CME butter prices continue to trade in the $2.20-2.25 range following a bullish stocks report. Prices were just starting to weaken following the holiday demand period when the November 30 stocks report showed inventories had fallen to the lowest point since November 2015. Lower milk and cream supplies, particularly in the Eastern half of the country, drove cream multiples to their highest level in several years. Butter prices usually are seasonally weak to start the year, but lower cream supplies and end-user buying are expected to keep the CME butter price around $2.20 give or take 5 cents or so. The higher US price is attracting imports and making US exports less competitive. Unless global prices move higher, this dynamic offsets some of the bullishness in the market.

While the US fat market tightens up, the global market remains well supplied. Butter prices in New Zealand dropped to the lowest point since August 2016 before recovering to $4,076/MT – a 12% bounce off the low. European prices fell sharply from early summer highs and have stabilized near $2.20 or low-mid €4,000’s/MT.

{kind=link}

{kind=link}

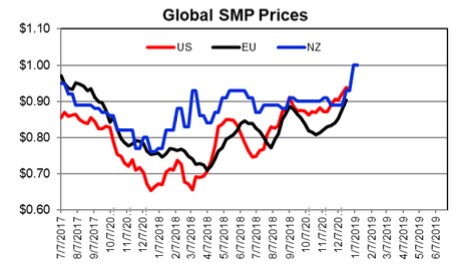

Milk Powders

Summary: The tone of the milk powder market has become more bullish in the last two months. The ingredients exist for more volatile, and higher, prices in 2019.

The fundamentals of the US milk powder market point to higher prices. US production has been below prior year levels for six of the last seven months. Exports over the last four months were 28% higher than the same period last year. And stocks have gradually moved lower and were 20% below year ago levels on October 31. Forecasted prices are now over $1.00/lb. for NFDM – the highest level in several years with a bias for higher prices than forecasted given the ingredients exist for more volatility. Looking back over time, the most explosive periods for the NFDM market was 2007 and 2013-14. Each time preceding these rallies, global stocks were low and demand was strong. While $1.00 sounds expensive given the last few years, those prior period highs were over $2.00, so there is a lot of room for prices to rally.

{kind=link}

{kind=link}

Global SMP prices are moving higher. The NZ/GDT price hit $1.00/lb. ($2,200/MT) on January 2 and the EU EEX price is up to $0.95 (€1,830/MT). The large sales from the SMP intervention program in recent tenders have been viewed as bullish. However, the production just moved from one place to another, so it will still be in the market for a while, just not visible. NZ production is expected to grow modestly and India has been exporting surplus powder. For now, the trend is higher, but not all the news is bullish.

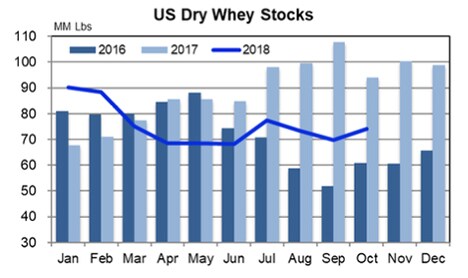

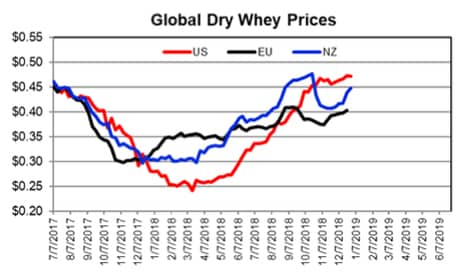

Whey Powder

Summary: Whey prices remain firm given lower stocks and solid demand.

While it looked like US dry whey prices were going to move lower last month, prices have been firm to higher in recent weeks. Global prices are also showing renewed signs of life as they edge up toward US price levels in the low-mid $0.40’s, depending on the index. Stocks have been below last year’s levels and production growth has been uneven as whey shifts to and from WPC production. Additional dry whey production is coming online, so prices are forecasted to remain near current levels and then decline slightly by spring.

{kind=link}

{kind=link}

Disclaimer: Information contained within is not guaranteed, is the opinion of the mccully group, llc, and is intended for informational purposes only. Commodities trading involves risk and is not suitable for everyone. Nothing contained within constitutes a solicitation to buy or sell derivative contracts. Trading futures/options contracts should be done with licensed professional brokers. The mccully group, llc is not a licensed commodity broker nor trades in commodity futures markets.