{kind=link}

Oil: Is Mideast Risk Premium Too Low?

This research article has been accepted for publication in the Spring 2020 issue of Global Commodity Applied Research Digest (GCARD at http://www.jpmcc-gcard.com/ [link-bold]).

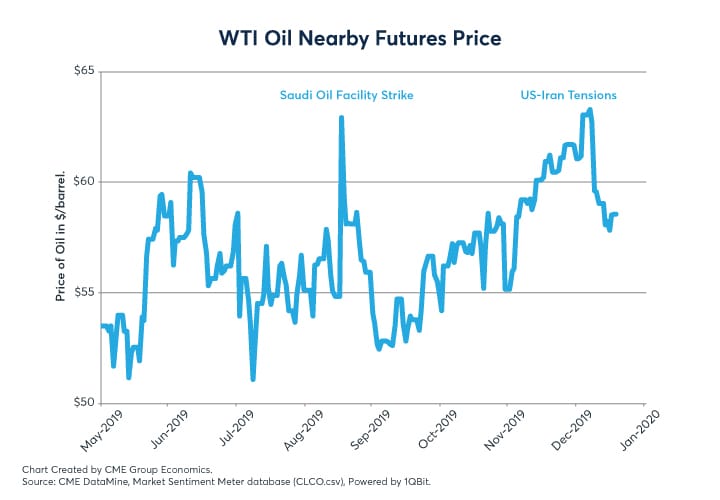

The mid-September attack on a Saudi Arabian oil processing facility that knocked out about 6% of the world’s oil supply caused a sharp $8-per-barrel surge in the price of oil before dissipating quickly. The early January 2020 US killing of an Iranian general in Iraq and the Iranian response with a missile strike on a US military base in Iraq also produced a similar outcome – a smaller abrupt quick price rise, then a rapid return back into previous oil price ranges.

{kind=link}

By our estimate, based in part on the degree of backwardation in the January 2020 futures maturity curve, the Mideast tension risk premium was only worth, maybe, $5 to $7/barrel, compared to $15 to $20/barrel before the US shale revolution reduced US oil imports and ramped up US petroleum (i.e., crude plus refined product) exports. The issue we want to frame is both why this risk premium did not respond more aggressively to the Mideast disruptions and what might cause the oil risk premium to rise down the road.

Factors resulting in the quick reversal of geo-political oil price spikes

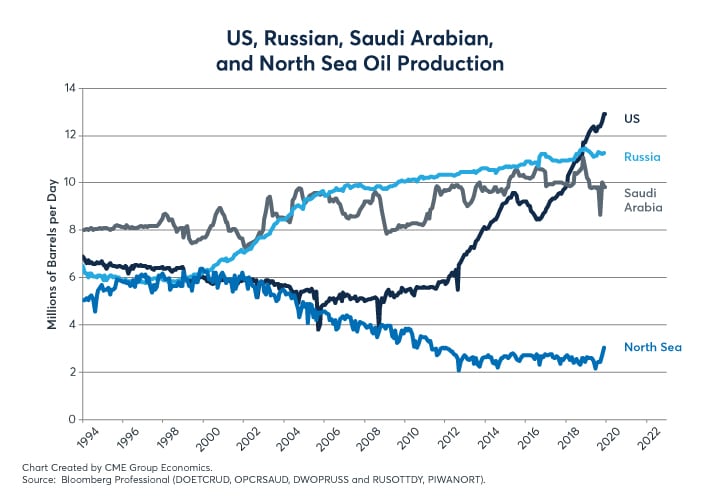

The US now dominates global oil production. It is the largest oil producer in the world, and the share of global oil production attributed to OPEC has been in decline. In the current environment, the Big Three primary oil suppliers, the US, Russia, and Saudi Arabia, effectively call the shots.

{kind=link}

Saudi Arabia is in a long-term adjustment as it transitions oil-production decisions from the King to Aramco, the state oil behemoth that became a public company in December. No big changes are expected quickly, yet over the long-term Aramco may evolve to become more focused on cash flow and revenue for dividend payments rather than serve as a buffer for global oil markets. Saudi oil has an extremely low marginal cost for adding production. If a focus on corporate valuation emerges, then keeping the oil and the cash flowing may rise as a priority.

By comparison, Russia’s economy needs the cash from oil and gas revenues. It can participate in oil production cuts, but only to a limited degree.

{kind=link}

The big changes are in the US. The growth rate of production from shale producers is slowing. Nevertheless, higher prices can elicit a powerful upward supply response about 8 months down the road. Moreover, US shale producers are more likely to be hedgers than their deep well onshore and offshore brethren. Deep oil wells produce for 25-30 years at a relatively steady rate. So, the producers often prefer to ride out the cyclical moves in oil prices and just let the long term take care of itself. Shale oil producers live on a much shorter time frame. Shale wells last about 18-24 months, and shale producers must drill new wells to keep the supply coming. As a result, shale producers are much more likely to hedge their future production (e.g., going short oil futures) compared to deep well producers. So, when there is an abrupt upward price move, shale producers are quick sellers of oil futures to hedge future production, including new wells not even drilled yet. This factor contributes to quick dissipation of any oil price shock.

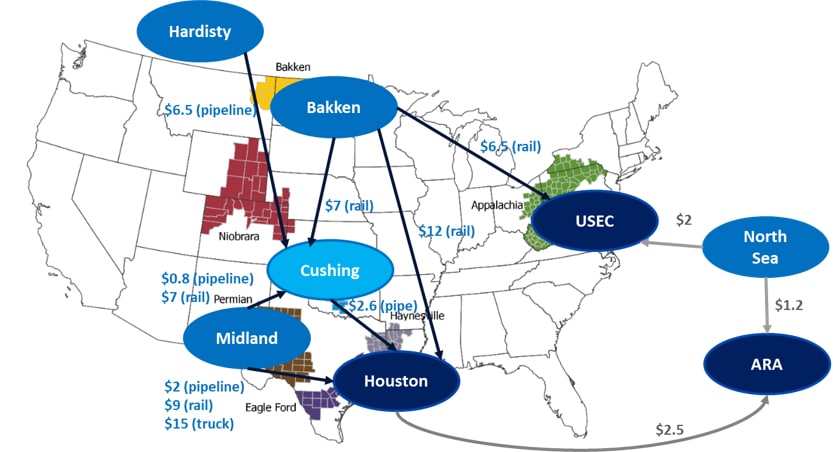

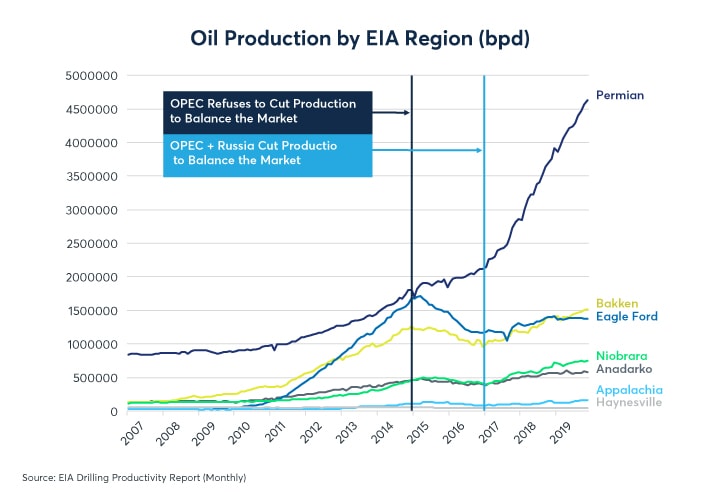

What also is striking and, perhaps under-appreciated, is how much capacity the US has to increase production further should prices rise to a level that would incentivize renewed investment in regions like Bakken, Eagle Ford and Niobrara. Those areas saw strong production growth prior to 2014 when oil was trading in the $80-$115 per barrel range. Since the 2014-16 oil price crash, production growth has concentrated in the Permian basin, which is better connected with pipelines than the other regions to the pricing center in Cushing and to the export terminals in the Houston area.

{kind=link}

Outside of the Permian, capital expenditure (capex) plunged with oil prices from late 2014 to early 2016 – and it never made anything close to a full recovery. Over the past year, capex has been falling across the board, including in the Permian as well as in other regions. This indicates that prices are currently too low to justify deploying additional equipment. However, should a disturbance in the Middle East or other factors push prices back above $70 per barrel, this trend could reverse. That would be especially true if prices rose back above $90 per barrel.

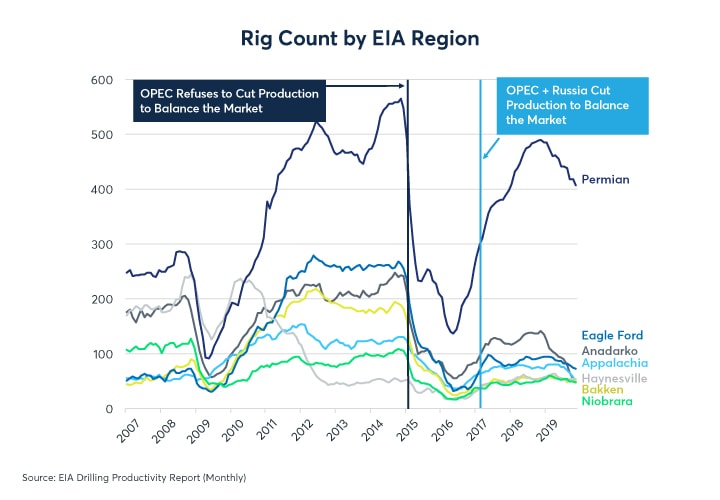

{kind=link}

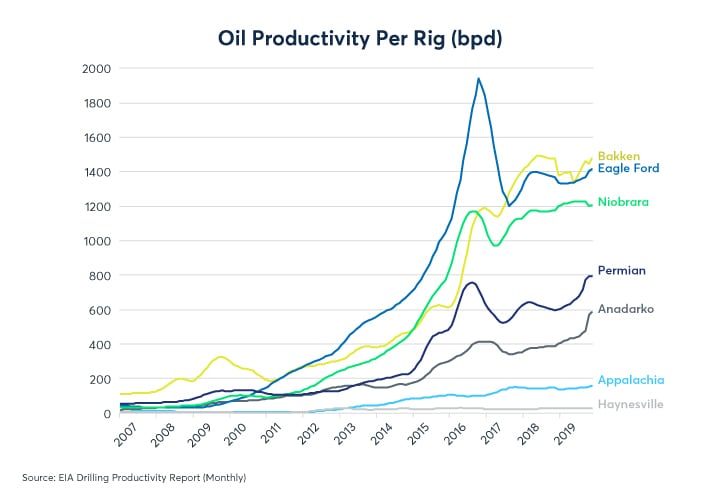

The collapse in rig counts, however, does not provide a complete picture. The amount of oil produced is equal to rig counts multiplied by productivity per rig. Since 2011 there has been a revolution in rig productivity. Some of the recent productivity gains may prove illusory, however. Falling rig counts indicate that there is less exploratory drilling and that firms are using their best equipment to exploit their most productive wells. Eventually, as these wells are exhausted, productivity and production will begin to decline. The lack of capex is likely to exacerbate the decline once it begins.

The news in 2020 is that declines in US production do not seem set to happen yet. The offsetting news is that production declines may become a risk later in the decade, giving rise to a complex dynamic in the oil markets. Falling US production would likely increase the oil market’s sensitivity to events in the Middle East, building back a greater risk premium into the markets. That greater risk premium –and especially any actual supply disruptions—could allow prices to rise in a manner that reignited investment and supply growth in the US. Hence, the US is likely to remain the primary swing producer through the 2020s.

{kind=link}

If the experience of the past decade is any guide, it will take about four months for the US rig count to respond to higher prices and a further four months before supply begins to increase. So, the lag time between a price spike and the beginnings of a sustained rise in US production are probably on the order of about eight months, on average.

The other factor to watch is inventories. Why oil did not respond more to the events in 2019 and early 2020 probably reflected inventories. Storage levels were highly elevated in the US and around the world at the time of the disruptions. This also limited the upside on refined gasoline prices at the time. Future disruptive events might not see such a quick dissipation of an abrupt price rise if storage levels were relatively diminished compared to the late 2019 and early 2020.

{kind=link}

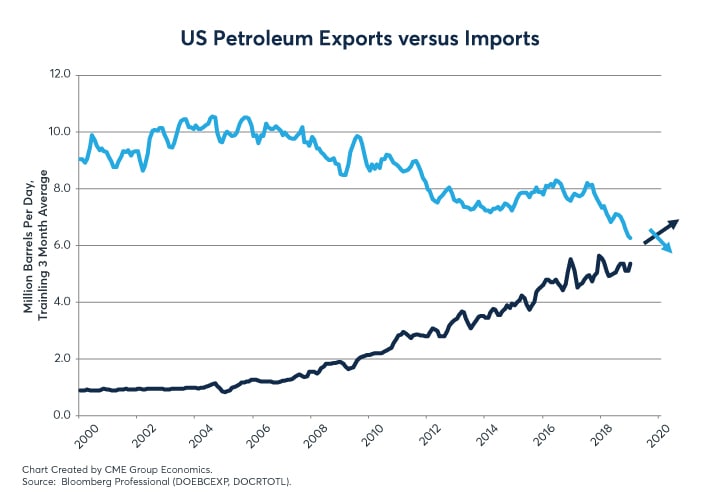

Also, with the US exporting both crude oil and refined products at a steadily increasing rate, US- produced oil is much more tightly connected with international oil demand. US exports have worked to stabilize the Brent/WTI oil price spread in a range that, more or less, reflects both the average and the volatility of shipping costs.

Rising risks in the Middle East

While the oil spikes from the geo-political tensions in September 2019 and January 2020 may have been short-lived, the probability of new disruptions may have risen. The US has set a precedent that it can target foreign military leaders it considers a threat to US assets. Iran has set a precedent that it can attack the US military in Iraq in retaliation. September 2019 taught the world that Saudi oil facilities could be targeted. Every strike and counter-strike tends to provide lessons for both sides that raise the stakes for the next round of any escalation.

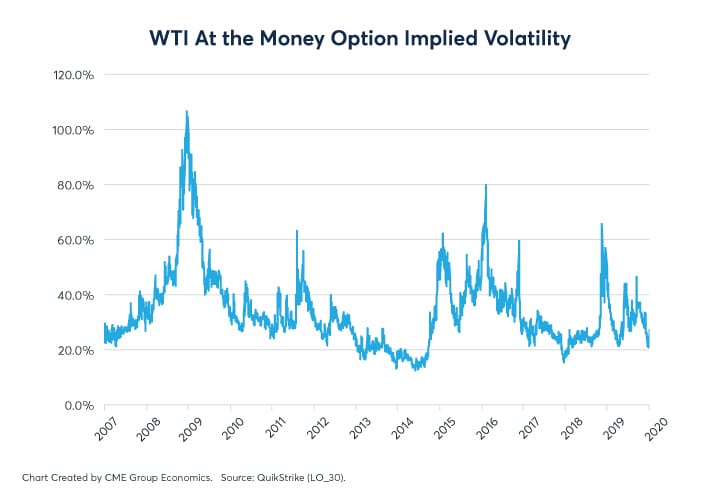

In our risk analysis, the probability of significant market-moving events has risen for 2020 compared to 2018 and 2019. This makes tail risks in the extremes of the risk distribution possibly under-estimated, and it makes shorter-term risk analysis from options-based implied volatility less useful. From our perspective, the risk premium looks relatively low, but it will take a series of low probability, high impact, disruptive events to change market risk pricing given the tendency of shale producers to quickly emerge as sellers into the rally as they hedge future production.

{kind=link}

We do note, however, even at the height of the US-Iran tensions in early 2020, implied volatility on 30-day NYMEX WTI crude oil options only made it to 29.4%, a relatively low level by historical standards. In the weeks after, implied volatility fell back modestly towards 26%. If oil inventories were relatively lower than in early 2020 and if US production were to reach a peak production level sometime later in the 2020s, implied volatility has the potential to rise significantly.

Energy options

Markets are pricing in a $5-$7 per barrel risk premium in WTI crude oil futures. Is that enough of a cushion against possible disruptions in the Middle East? Access the world’s benchmark options for crude oil, natural gas, and refined products around the clock.