{kind=link}

Oil: Could Iran Risk Reverse Options' Bearish Signal?

The removal of Secretary of State Rex Tillerson and replacing him with CIA Chief and former Congressman, Mike Pompeo, has implications for nearly all aspects of U.S. foreign policy, including Middle East relations. More specifically, Tillerson supported the Iran nuclear deal (Joint Comprehensive Plan of Action or JCPOA), whereas Pompeo was one of its fiercest opponents on Capitol Hill.

In addition to the recent changes at Foggy Bottom, there are also numerous press reports that White House Chief of Staff John Kelly might be paving the way for the return of National Security Advisor H.R. McMaster to the Pentagon with his elevation to the rank of four-star general. McMaster has been a supporter of the Iran nuclear deal, albeit a lukewarm one. Among his possible replacements is former UN Ambassador John Bolton, also a critic of the Iran nuclear deal.

Whatever one thinks of the recent (and rumored) personnel changes and the JCPOA itself, the negotiation of the deal in 2014 and its eventual adoption in July 2015 may have contributed to the collapse in oil prices by reducing the risk premiums embedded in WTI, Brent and other benchmarks. The easing of Middle East tensions that JCPOA came to symbolize may have led oil prices to catch up with economic reality on the downside.

For instance, WTI normally tracks vegetable oil prices, but in the wake of the 2011 Arab Spring and heightened tension between the U.S. and Iran, WTI futures remained elevated for years even as soybean oil and other vegetable oil prices declined. According to our research, movements in vegetable oil prices often lead movements in crude oil, but typically only by one to six months and not by one or two years as they did in 2013 and 2014 (Figure 1).

Figure 1: In 2013 and 2014 Middle East Tensions May Have Kept WTI Elevated.

{kind=link}

The proximate cause of the oil price collapse in the fall and winter of 2014-15 was OPEC’s failure to agree on production cuts and Saudi Arabia’s gambit to thwart U.S. production growth by allowing prices to fall. While that may be true, blaming shale oil frackers, Saudi Arabia and OPEC for oil’s abrupt collapse overlooks the question of why oil prices remained so high to begin with. How is it that oil levitated in the $90 to 110-per-barrel range for so long given the potential downside price risks from surging U.S. production? Fears of supply disruption from the conflicts in Libya, Syria and Yemen certainly contributed, as did instability in Egypt and tensions with respect to Iran and its nuclear program.

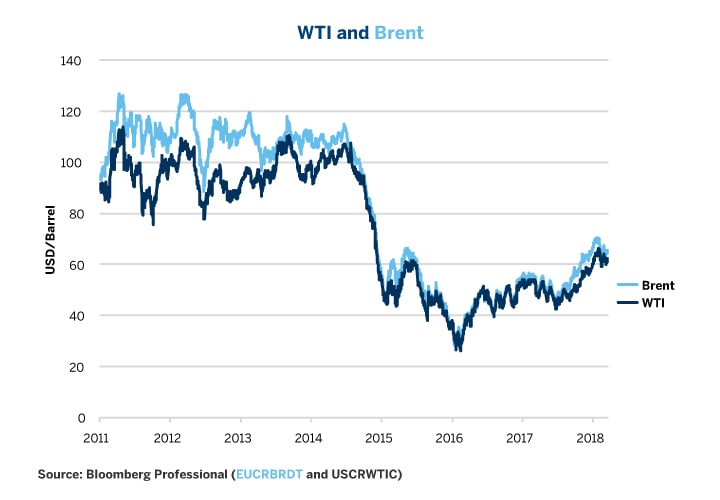

In addition to the gap between crude oil and vegetable oil prices, the other primary evidence of the impact of geopolitical tensions was the Brent-WTI spread, which blew out in 2011 as the Arab Spring began, and remained wide for years. As tensions eased, the Brent-WTI spread narrowed and eventually closed as the U.S. lifted its ban on oil exports in 2016 (Figure 2).

Figure 2: Post-Arab Spring, Brent Prices Exceeded WTI for 3 Years Until Iran Agreement Got Close.

{kind=link}

Changes in Washington D.C. are hardly the only reason to fear an upturn in geopolitical risk in the Middle East. The conflicts in Syria and Yemen are unresolved. The Syrian conflict is especially pernicious in that it involves so many different powers and groups: President Bashar al-Assad’s Syrian government, his Iranian, Russian and Hezbollah allies, ISIS, various rebel factions aligned with the Turks, the U.S., Saudi Arabia and Qatar, as well as the Kurds. Not one of the combatants appears to have an exit strategy. The conflict also risks spilling across the border into Lebanon and has, at times, crossed into Iraq. Outside of the hot conflicts, there is also the still unresolved diplomatic conflict between Saudi Arabia and the U.A.E. on the one hand and Qatar on the other.

In addition to conflicts between nations, there are plenty of problems within nations. Iran has experienced significant domestic protests recently. Across the Gulf in Saudi Arabia, details are leaking out about the allegedly brutal treatment and continuing legal limbo of many (formerly?) wealthy and powerful individuals recently released from the makeshift Ritz Carlton prison in Riyadh. In addition to any potential domestic blowback if the new Crown Prince, Mohammed bin Salman, or MBS as he is known, fails to deliver on his promises of less corruption and more economic growth, there is also the question of the damage done to the initial public offering of state-owned oil behemoth Aramco from the perceived lack of due process and rule of law. With respect to the recent round of arrests, MBS may have violated two core principals of the world’s greatest political theorist, Niccolo Machiavelli:

- Crush your opponents completely. Do not merely humiliate them but then let them survive.

- People will sooner forgive a Prince for killing their relatives than they will for confiscating lands, assets or titles.

How would a rejection of the Iran nuclear deal impact these delicate internal and international balancing acts? Nobody can know for certain but we suspect that it would skew risk to the upside for WTI and other oil products. For the moment, however, the options skew is pointing decidedly in the other direction (Figure 3).

Figure 3: Options Traders Fear Downside Risk More Than Upside Risks.

{kind=link}

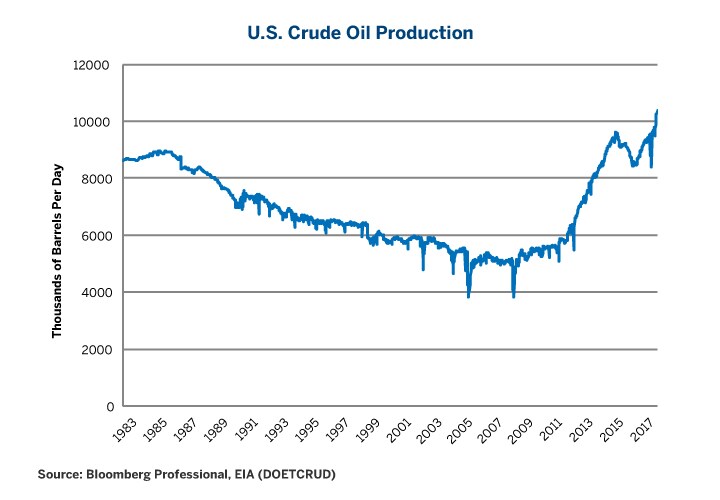

The reason why markets are so sanguine about upside risk is probably due to surging U.S. production (Figure 4) and still high levels of inventories (Figure 5). But one should be wary of such logic for two reasons. First, oil investment in the U.S. has stalled and, as such, it’s clear how much higher U.S. production can rise (Figure 6). Secondly, while inventories remain high they are falling quickly from their peak levels and as such their ability to absorb a demand shock may not be as great as some options traders might believe (Figure 7). The main downside risk to oil might be a collapse of OPEC’s production-cut agreement, although so far, remarkably, OPEC has largely stuck to it.

Figure 4: U.S. Production has Crossed 10 Million Barrels Per Day

{kind=link}

Figure 5: Oil Inventories Remain Abnormally High.

{kind=link}

Figure 6: Rig Counts Have Stagnated Despite $60+/Barrel. Can Production Continue to Rise?

{kind=link}

Figure 7: Inventories Might be High but YoY, they are Falling at the Fastest Pace on Record.

{kind=link}

Bottom line:

- Oil traders are pricing more downside than upside risk.

- That could change if the U.S. pursues a more muscular policy with respect to Iran.

- Options traders appear to fear downside related to possible OPEC cheating, surging U.S. production and still higher-than-normal inventories.

- The ability of U.S. production to keep growing is questionable given that rig counts have stalled.

- Inventories are high but are falling at the fastest pace on record.

New Canadian Crude Oil Options Coming Soon

Canada is among the world's top producers of crude oil, and in conjunction with this NYMEX will launch three new net energy Canadian crude oil options on March 25, 2018. The initial listing of Canadian Crude Oil Average Price Option Contracts will include Synthetic Sweet Oil, Light Sweet Oil and Canadian C5+.