{kind=link}

Nikkei 225 Spread Opportunities

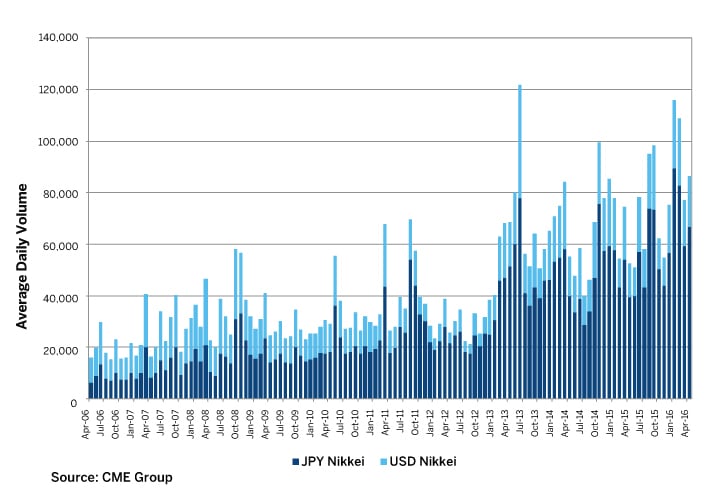

The pair of Japanese yen- and U.S. dollar-denominated Nikkei 225 Index futures is arguably the most liquid listed index quanto spread market. The volume traded in this market has grown five-fold since 2006, and average daily volume in the two products totaled over 100,000 contracts per day in the first quarter of 2016. A driving force behind this volume growth is the non-trivial nature of the spread between the futures with different currency denomination. Indeed, the correlation between the JPY/USD exchange rate movement and the performance of the equity market creates a unique trading opportunity in this set of products. This paper explains the dynamics behind this “quanto” or “correlation trade.”

Figure 1: Volume growth in JPY- and USD-denominated Nikkei 225 Index futures

{kind=link}

Contract Terms

A useful starting point is to review the contracts’ specifications, depicted in Figure 2. The most important difference between the two contracts is the currency denomination of the contract multipliers. The USD-Nikkei is sized at $5 x the Index, while the JPY-Nikkei is valued at ¥500 x the Index. The March quarterly expirations for both contracts trade continuously and with virtually around-the-clock liquidity on the CME Globex electronic trading platform. The serial months of the JPY-Nikkei are available for trading but have insignificant volume.

Both versions of the Nikkei 225 Index futures settle to the same final settlement value – the Special Opening Quotation of the Nikkei 225 Index – calculated based on the opening price of each constituent on the expiration day. As such, the prices of the two futures contracts of the same expiration will converge to the same price at their termination.

Figure 2: Nikkei 225 Index Futures Contract Features

| USD-Nikkei | JPY-Nikkei | |

| Contract Multiplier | $5 x Nikkei 225 Index | ¥500 x Nikkei 225 Index |

| Minimum Price Fluctuation | 5 index points | |

| Final Settlement | Cash-settled to the SOQ of the Nikkei 225 Index on 2nd Friday of the contract expiry month | |

| Last Trading Day | 4:00 p.m. CT on the day preceding final settlement | |

| Contract Months | 4 quarterly contracts | 5 quarterly and 3 serial contracts |

| Trading Venue and Hour | CME Globex: Monday – Friday, 5:00 p.m. previous day – 4:00 p.m. CT | |

| Position Limits | 20,000 contracts net long or short between Yen- and USD-denominated Nikkei 225 Index futures | |

Relative Pricing of the U.S. Dollar and Japanese Yen

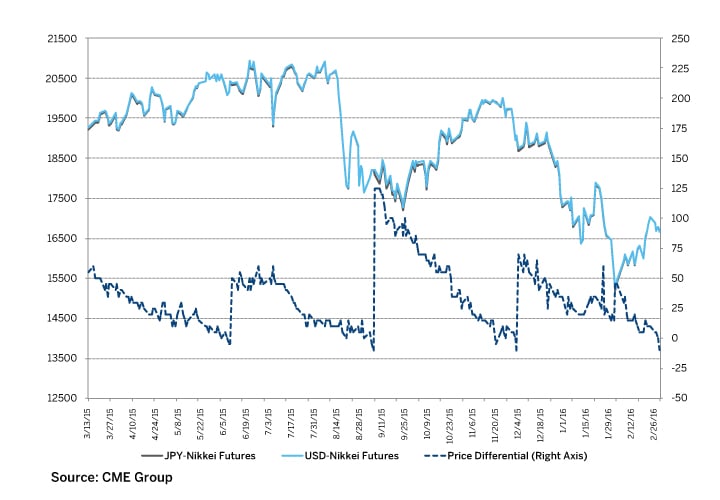

Figure 3 shows the price path of front quarterly JPY- and USD-denominated Nikkei 225 Index futures from March 2015 to March 2016, spanning four full quarterly cycles. As described under the contract terms, these two contracts will converge on expiration day to the same price. Generally speaking, they follow each other up-and-down, reflecting the valuation of the stock market they track. In examining the price differential (tracked against the right axis), it is readily apparent that the USD-denominated Nikkei futures price was generally higher. The price differential is unmistakably present and diminishes to zero as the expiry draws near. The persistence of the price differential suggests that it reflect something more fundamental than transitory order flow imbalances.

To understand, consider the following question: if the JPY/USD exchange rate and the Nikkei 225 Index stock were correlated, would market participants prefer to be paid in USD or in JPY?

Figure 3: Price Path of Front Quarterly JPY- and USD-denominated Nikkei 225 Index futures, March 2015 – March 2016

{kind=link}

USD-Nikkei 225 Index futures traded at a higher price than the JPY-Nikkei 225 Index Ifutures. The dotted line shows the differential, which diminishes over time.

Assume the JPY exchange rate is positively correlated with the Nikkei 225. As such, one might prefer to buy JPY-Nikkei futures vs. USD-Nikkei futures. This is intuitive to the extent that if the Nikkei 225 advances, profits on the long position would tend to be bolstered by an advancing JPY vs the USD. But if the Nikkei 225 should decline, losses are mitigated by a decline in the JPY vs. the USD. Thus, the JPY-Nikkei futures contract should trade at a premium vs. the USD-Nikkei futures contract.1

The reverse would apply if the JPY exchange rate was negatively correlated with the Nikkei 225. As such, one would prefer a long USD-Nikkei position over a long JPY-Nikkei position. This makes sense to the extent that if the Nikkei 225 advances, profits on a long position in JPY-Nikkei are compromised by a declining JPY. Or, if the Nikkei 225 should decline, losses on a long JPY-Nikkei futures position are magnified by an advancing JPY. Thus, USD-Nikkei futures should trade at a premium vs. JPY-Nikkei futures.

{kind=link}

This latter scenario is the commonly observed phenomenon, namely, JPY strengthening coincides with stock market falling. Thus, the USD-Nikkei is typically traded at a premium.

Anatomy of the Spread

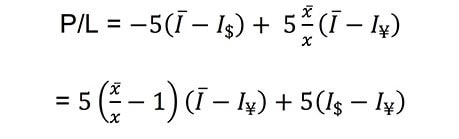

Consider the following trade: sell or short one USD-Nikkei futures at I$ and buy or go long Δ number of JPY denominated contracts at a price of I¥. Let Ī denote the Final Settlement Price of Nikkei 225 futures and x̄ denote the spot JPY-USD exchange rate on the expiration date of Nikkei 225 futures.2

At contract expiration, the position’s profit/loss (P/L), expressed in USD, may be denoted as follows.

{kind=link}

Picking the conveniently chosen the spread ratio Δ equals 1 / 100 x, where x is the spot JPY-USD exchange rate at the time the trade originally is executed,3 the P/L is now reduced as follows:

{kind=link}

If the futures were priced at “fair value”, the expected value of the P/L should be zero. In order for this to be the case, the relative prices between the two futures contract should be:

{kind=link}

Inspecting this equation, the left side is the percentage premium/discount of the JPY-Nikkei futures over USD-Nikkei. The right side represents the covariance between percentage changes of the JPY-USD exchange rate and that of the JPY-Nikkei futures. This quick-and-dirty calculation formalizes the earlier hypothesis – if the JPY-USD exchange rate and the Nikkei 225 Index are positively correlated, the JPY-Nikkei index futures contract should be valued at a premium over the USD-denominated contract.

Though this formula is already remarkably compact, it can be made yet more so by adopting the following notation. Let T denote the time to futures expiration, σᴇ and σI denote the annualized volatility of the exchange rate and the Nikkei index, respectively, and ρ denote the correlation between the exchange rate and the index. Then the premium of JPY vs. USD Nikkei futures – or the quanto spread – may be represented as follows.

{kind=link}

Determinants of the Premium

This equation reflects the three principal determinants of the price premium between the two index futures contracts and the relationship among these determinants.

- Correlation - If there is no systematic co-movement between exchange rate dynamics and stock index dynamics, then there is no reason to prefer one currency denomination to another.

- Historically, the strength of Yen is inversely related with the stock market. Based on the expectation of such correlation going forward, the USD-Nikkei futures almost always trade at a premium to the JPY-Nikkei futures. Figure 3 illustrates the premium of USD-Nikkei through four full quarterly cycles.

- Volatility – If the correlation effect is to exert any material impact upon pricing, there must be at least some actual movement in both the exchange rate and the index. Figure 3 illustrates the tendency. Significant drops in the Nikkei futures coincide with spikes in volatility. The magnitudes of the spread tend to be higher at the same time.

- Time – For either correlation or volatility to manifest themselves, it requires the passage of time. Figure 3 illustrates this time decay element.

It is perhaps easiest to look at the magnitude of the quanto spread during the quarterly roll period. Specifically, the calendar spreads for the JPY-Nikkei and USD-Nikkei futures provides a convenient comparison. Figure 4 tabulates the average quanto spreads during the last 15 roll periods.

Figure 4: Nikkei Index Futures Quanto Spread, based on calendar spreads of JPY- and USD-Nikkei futures during the roll period.

| Roll Period | Average Spread Differential | Averageg Spread as % of Expiring JPY-Nikkei | Average Implied Correlation | Average Implied 3-Month FX Volatility | Average Implied 3-Month Index Volatility |

| Mar-16 | 96.25 | 0.572% | 85.99 | 10.94 | 24.42 |

| Dec-15 | 74.18 | 0.380% | 105.41 | 7.64 | 18.97 |

| Sep-15 | 97.12 | 0.536% | 74.75 | 10.43 | 27.61 |

| Jun-15 | 57.66 | 0.284% | 76.51 | 8.79 | 17.02 |

| Mar-15 | 71.06 | 0.378% | 86.42 | 9.46 | 18.56 |

| Dec-14 | 117.50 | 0.670% | 99.84 | 11.76 | 23.12 |

| Sep-14 | 41.11 | 0.261% | 87.29 | 7.65 | 15.72 |

| Jun-14 | 44.06 | 0.293% | 104.30 | 6.08 | 18.51 |

| Mar-14 | 80.04 | 0.532% | 105.96 | 8.56 | 23.47 |

| Dec-13 | 95.35 | 0.613% | 89.16 | 10.24 | 26.88 |

| Sep-13 | 130.68 | 0.906% | 111.76 | 12.13 | 26.70 |

| Jun-13 | 163.58 | 1.253% | 115.28 | 14.10 | 31.05 |

| Mar-13 | 95.60 | 0.804% | 117.30 | 11.74 | 23.45 |

| Dec-12 | 24.00 | 0.250% | 65.38 | 8.58 | 17.75 |

| Sep-12 | 21.94 | 0.249% | 79.13 | 7.16 | 17.57 |

Source: Bloomberg, CME Group

The spread differential is the difference between the calendar spreads in term of index points of front and next quarterly months in JPY- and USD-Nikkei futures. As the USD-Nikkei had always traded at a premium to the JPY-Nikkei futures, the 96.25 index points for March 2016 was premium of USD-Nikkei over JPY-Nikkei futures for spanning the three-month period between the March 2016 and June 2016 expiries. This magnitude is 0.572% of the expiring (i.e. March 2016) of the JPY-Nikkei futures.

The two columns on the right show the three-month implied volatility of the exchange rate and the three-month implied Nikkei volatility. They are correlated with each other, as well as with the magnitude of the quanto spread, as expected.

The implied correlation is the ratio between the magnitude of the premium and the implied volatilities. It is interesting to see that the implied correlation between the FX and index can, and do, exceed 100% routinely. This is, perhaps, an indication that the end users in the USD-Nikkei futures value the dollar denomination so much that they are willing to pay beyond “fair-value” to get the feature.

Mechanics of the Spread Trade

Walking through an example of a spread trade, assume a spread trade was executed by purchasing 250 JPY-Nikkei futures; and, selling an appropriate number of USD-Nikkei futures. Assume there are three months until contract expiration and that USD-Nikkei futures are trading at a premium of 40 index points over JPY-Nikkei futures. Finally, the exchange rate is 107 JPY per USD, or 0.009345 in USD per JPY terms. The last of these assumptions implies that the appropriate spread ratio is 1:1.07. Thus, we might sell 234 USD-Nikkei futures.

One day later, both JPY- and USD-Nikkei futures rally 100 index points, while the spread remains unchanged at 40 index points. The marks to market are as follows.

{kind=link}

If, over the same one-day interval, JPY has strengthened, then the JPY margin inflow is worth more than the USD margin payout. One may lock in this gain via a currency trade, e.g., by selling JPY inflows for USD, covering the USD margin payout, and retaining the residual.

Subsequently, the spread ratio needs to be rebalanced to account for exchange rate movement, but this adjustment will tend to be small. For example, a 1% move in the exchange rate would require a 1% change in the spread ratio, which amounts to 2 or 3 contracts in the present instance.

Now recall the spread formula above. It suggests that the cumulative profit or loss on the JPY-USD index spread is simply the accumulation of the daily products of exchange rate and index movements. Against this backdrop, the example above dramatizes that the profitability of the spread trade essentially reflects the outcome of a race between this daily accumulation process on one hand; and, the convergence of the spread to expiration on the other.

Exchange Rate Gains and Losses

For many market participants, it may be impractical or infeasible to perform daily currency transactions to crystallize gains and losses on exchange rate movements, per the example above. In such instances, one might be forced to carry one’s P/L in two different currencies until futures expiration, at which time a single currency trade will occur.

If so, then a slight adjustment to the spread ratio may be desirable. To see why, one can revisit the mathematics of daily P/L.

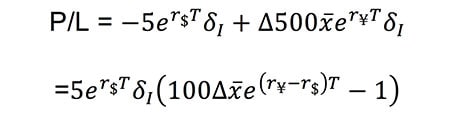

Denote the day’s change in Nikkei index futures as δ1. Let r$ and r¥ denote continuously compounding interest rates for USD and JPY, respectively. Finally, assume no change in the price spread between the JPY- and USD-Nikkei futures. Now suppose that, instead of instantaneously translating our profit on mark-to-market into dollars, we choose instead to carry the profit until futures expiration. The P/L for the day, as realized at contract expiry, may be represented as follows:

{kind=link}

A close look reveals that this requires an adjustment to the spread ratio to account for relative interest rates,

{kind=link}

where x denotes the current JPY/USD exchange rate. Conveniently, this complicated denominator term xe(r¥ - r$)T can be well approximated by the CME Japanese Yen FX futures price. Currency futures generally expire on the Monday prior to the third Wednesday of the contract month, a few days following expiration of Nikkei 225 futures. These few trailing days allows ample time to consummate the spot foreign exchange transaction entailed in booking the final P/L on the spread trade.

Per the example above, a 100-point move for a 250-lot Nikkei futures position generates a mark-to-market variation of ¥12.5 million. This is a convenient number as a standard sized CME Group Japanese Yen futures has a notional size of exactly ¥12.5 million. A 100 point movement in the Nikkei 225 is not uncommon over the course of a single day. Thus, one may conveniently hedge the exposure using currency futures as an alternative to a spot or cash currency transaction.

Visit cmegroup.com/nikkei to learn more about our Nikkei 225 Index futures complex.

1 It is important to recognize that one may establish a long or short futures position on a leveraged basis by posting collateral as the initial margin. That collateral may be held in the form of USD-denominated cash or securities; JPY-denominated cash or securities; or, in other currencies. Thus, a USD-domiciled trader may establish a long in JPY-Nikkei futures without actually holding or posting any Japanese yen. Subsequently, however, any profits or losses which accrue in the JPY-Nikkei futures position are denominated in JPY.

2 The Japanese yen vs. U.S. dollar exchange rate is typically quoted in terms of yen per 1 dollar and this is commonly referred to as the USD-JPY rate. For the convenience of USD based traders, however, we quote in “American terms” of U.S. dollars per 1 Japanese yen. This is referred to as the JPY-USD rate. This further sets the stage for a discussion of how one might use CME JPY-USD futures, quoted in dollars per yen, as a hedge. The conclusion would be identical had we gone with the interbank convention of USD-JPY.

3 This spread ratio is designed to ensure that the value of the contract multipliers of the two index futures contracts are identical.

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.