{kind=link}

Mexico's Peso Shines Even as Economy Wobbles

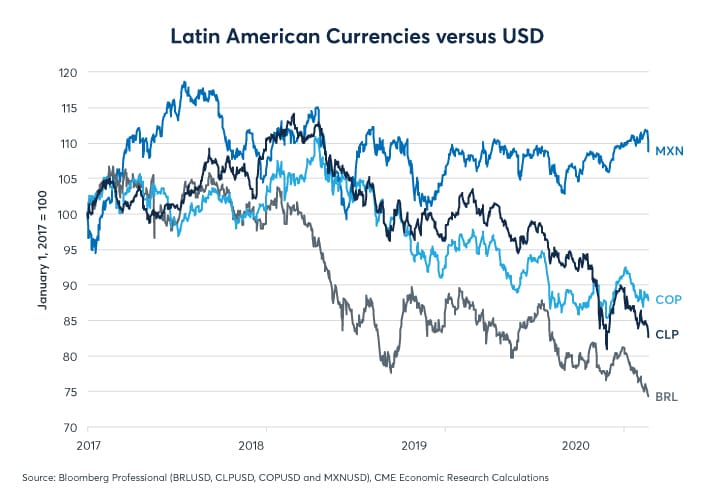

When Mexican President Andres Manuel Lopez Obrador (AMLO) took office in December 2018, his inauguration was accompanied by a great deal of hand-wringing about what it might portend for the country, the economy and the peso (MXN). After 14 months, the currency market has delivered a verdict, of sorts: MXN has spectacularly outperformed its Latin American peers (Figure 1). While the Brazilian real (BRL), Chilean peso (CLP) and Colombian peso (COP) have fallen substantially versus the US dollar (USD), MXN has gained in value.

Figure 1: MXN, leader of the pack

{kind=link}

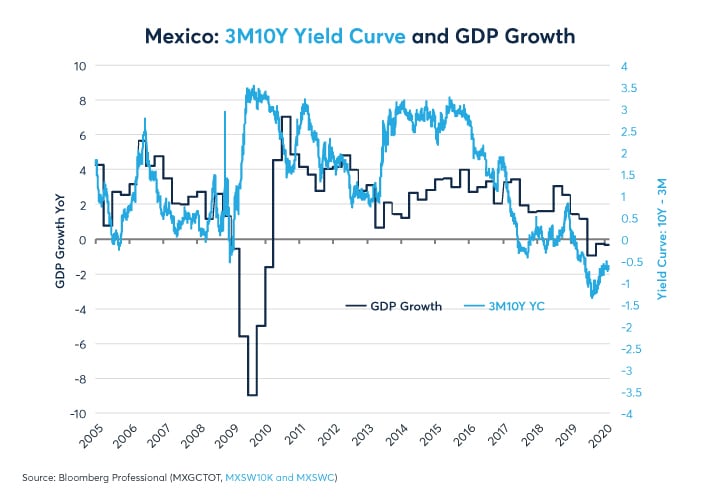

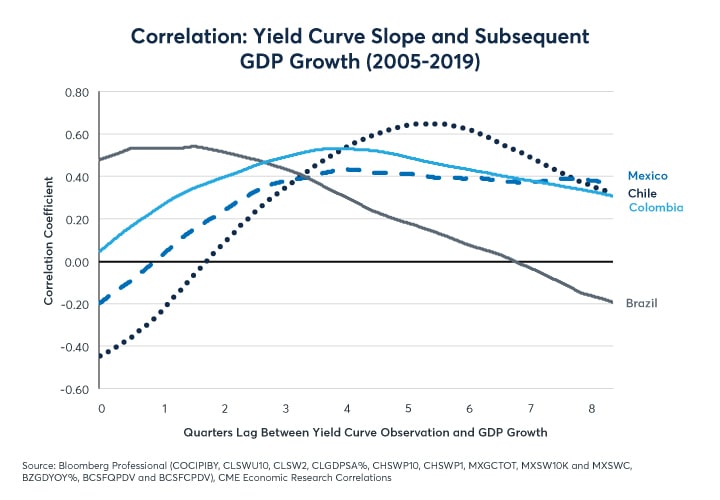

At first blush, the reasons for this overperformance are not overwhelmingly obvious. The Mexican economy contracted 0.1% in 2019 and the Mexican yield curve remains inverted, suggesting a likelihood of further weakness ahead (Figure 2). The yield curve slope is positively correlated with future growth in all four of Latin America’s Big Four currencies (Figure 3).

Figure 2: Mexico is in a mild recession. An inverted yield curve suggests slower growth

{kind=link}

Figure 3: Yield curve slope at times correlates positively with subsequent GDP growth

{kind=link}

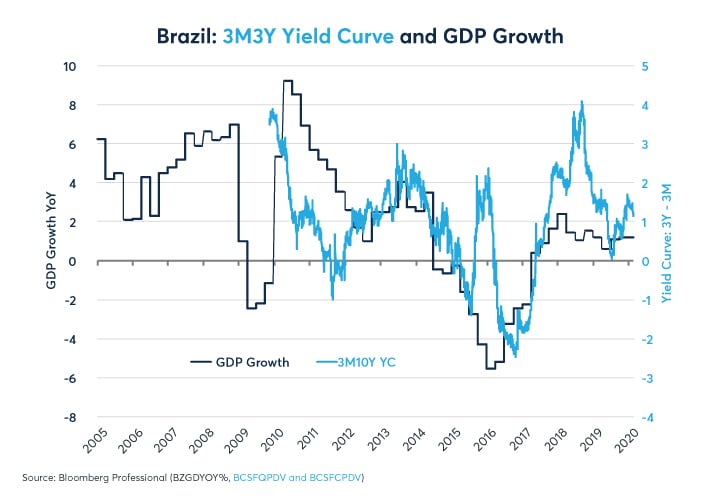

In this regard, Brazil, Chile and Colombia have a leg up on Mexico. While their economies all took a hit when commodity prices collapsed between 2014 and 2016, none of them are currently in a recession and all of them have at least somewhat positively sloped yield curves, suggesting a likelihood of slow-to-moderate growth ahead (Figures 4-6).

Figure 4: Brazil’s recession ended two years ago. Its yield curve suggests continued slow growth

{kind=link}

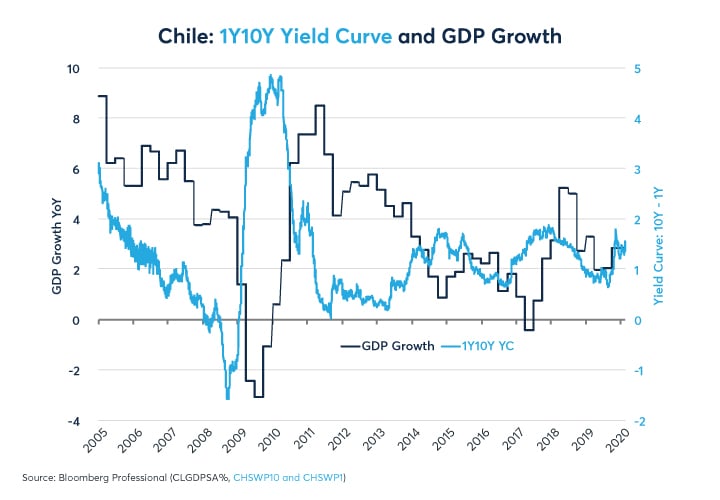

Figure 5: Chile’s yield curve suggests continued moderate growth

{kind=link}

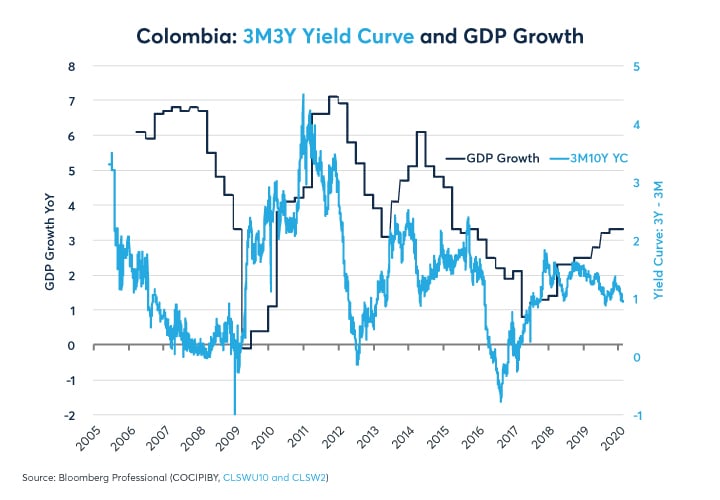

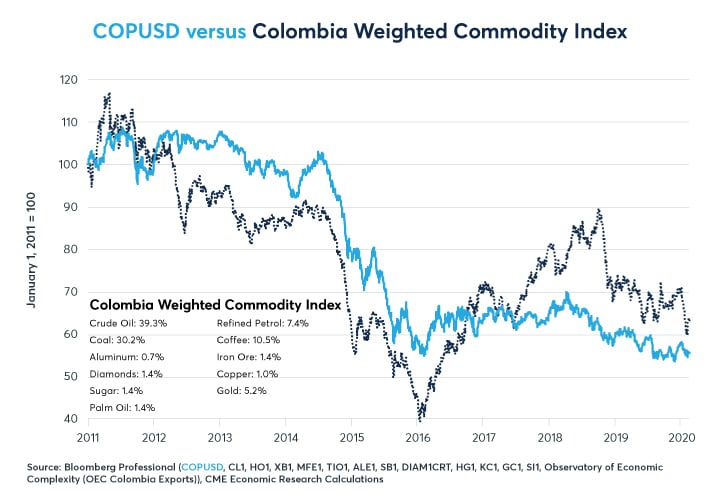

Figure 6: Colombia’s yield curve hints at a possible moderation in growth but no immediate downturn

{kind=link}

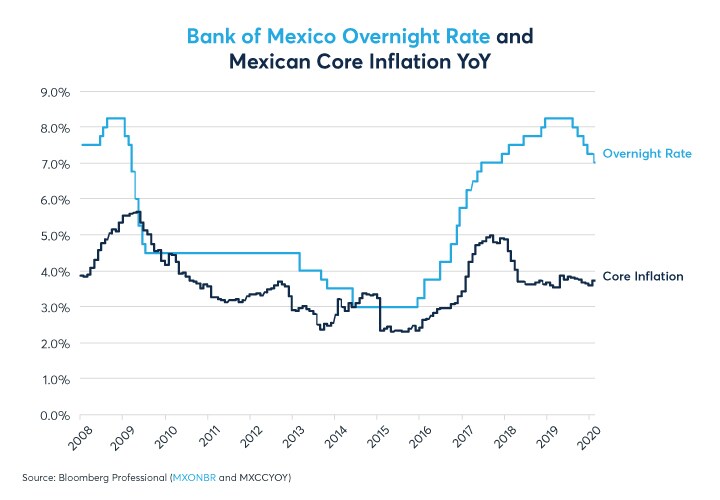

Moreover, the Mexican central bank has been slashing interest rates (Figure 7), which under normal circumstances is typically bearish for a currency. So, with Mexico’s economy underperforming its peers and likely to continue doing so in the near term, why is MXN outperforming its peers even amid easier Bank of Mexico monetary policy?

Figure 7: Bank of Mexico has been slashing rates, perhaps after overtightening

{kind=link}

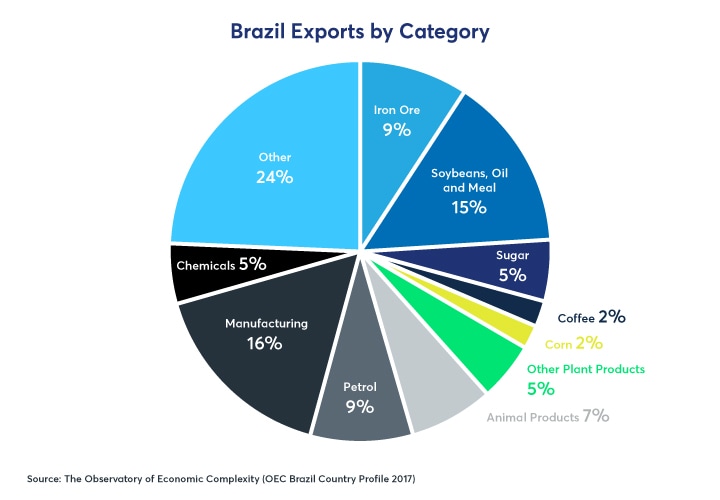

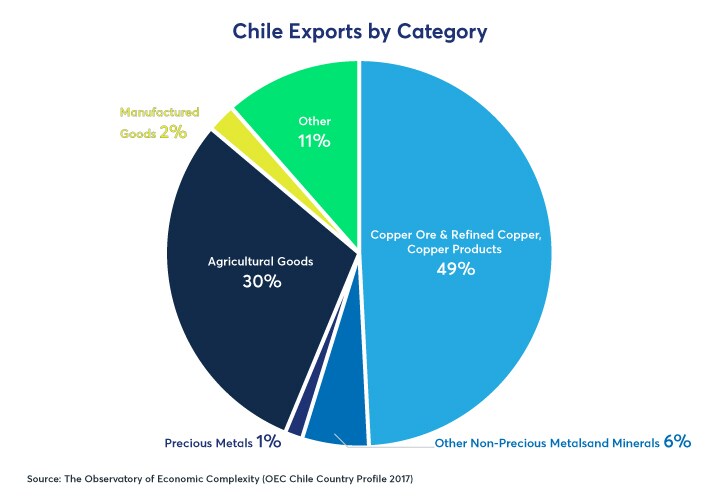

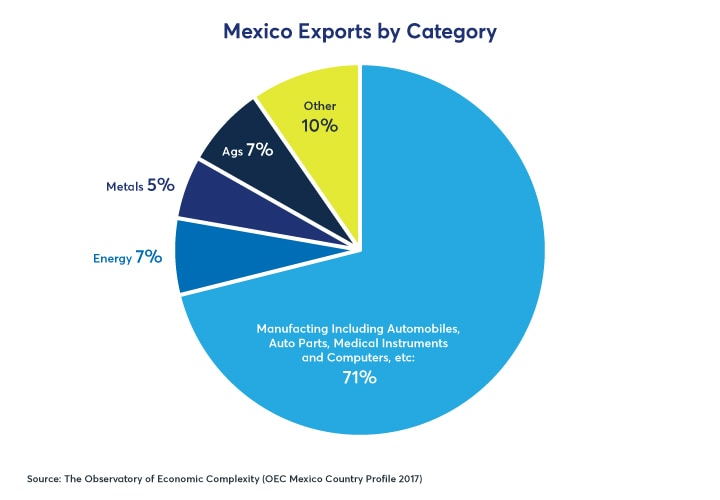

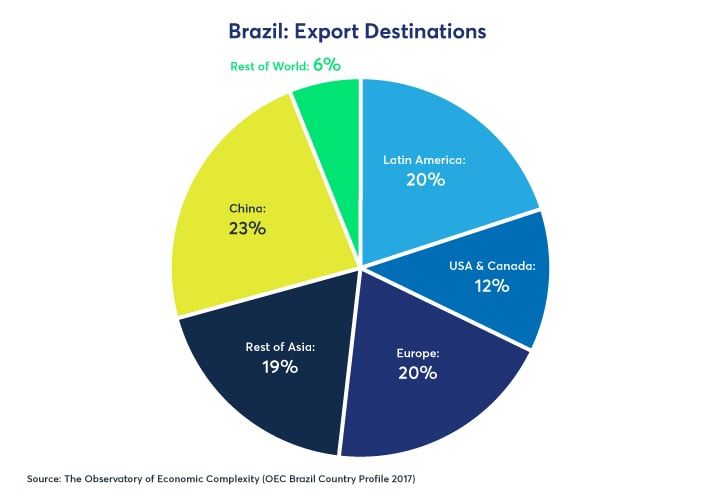

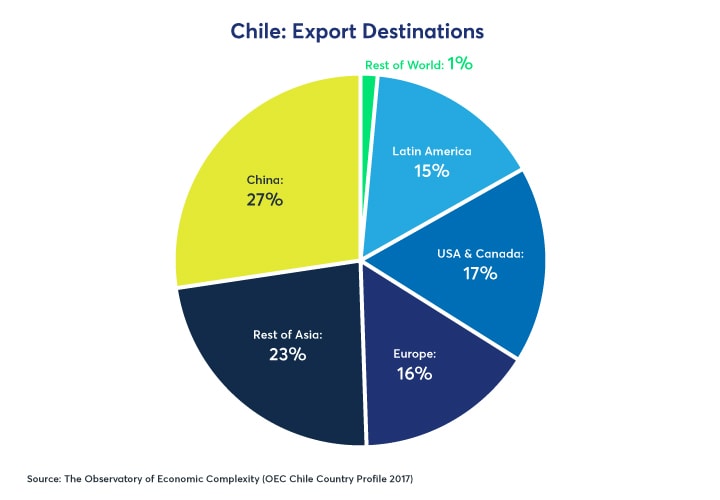

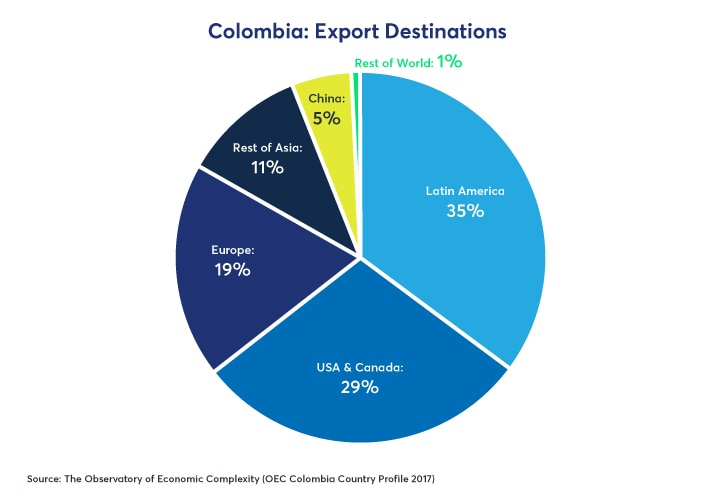

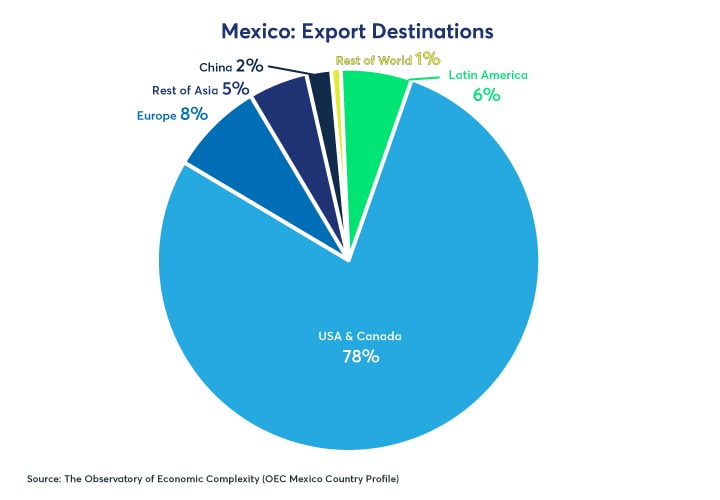

The answer lies in Mexico’s trade situation, which differs distinctly from its Latin American peers. Latin American nations typically rely on commodity exports. In Brazil, agricultural goods account for 37% of exports, with metals and energy adding another 9% each, bringing the total to 55% (Figure 8). In Chile, copper accounts for about half of all exports. Agricultural goods add another 30% while metals other than copper contribute 7%. Overall, commodities account for 83% of Chile’s exports (Figure 9). Commodities comprise 78% of Colombia’s exports, mostly energy and agricultural products (Figure 10). In Mexico, however, manufactured goods account for 71% of exports, while commodities contribute only 19% (Figure 11).

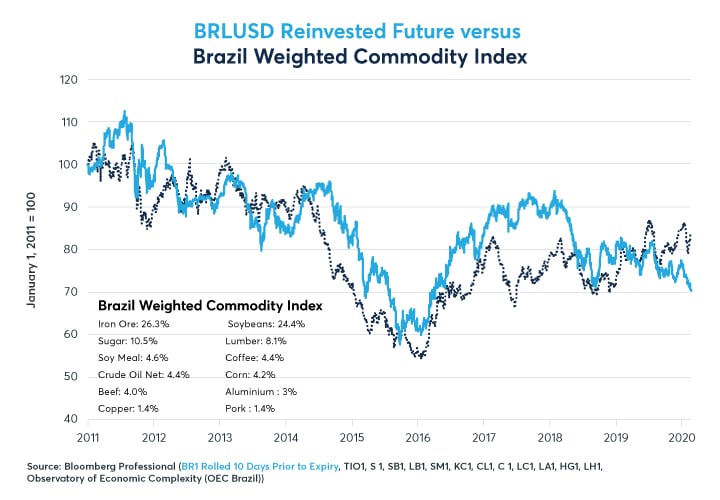

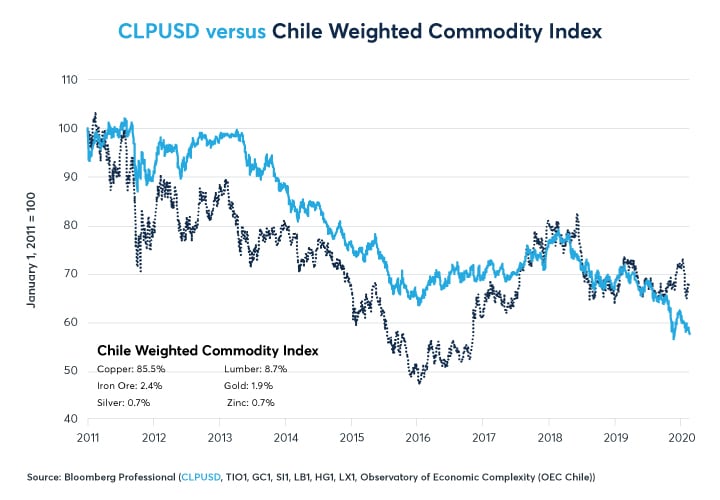

Not surprisingly, BRL, CLP and COP closely track locally weighted indices of commodity prices (Figures 12-14). By contrast, MXN marches to the beat of a different drummer. Mexico’s exports overwhelmingly go to one country: the United States. Canada is a distant second. Together they buy 78% of Mexico’s exports.

Remarkably, Mexico sends only 2% of its exports to China, compared to 23% for Brazil, 27% for Chile and 5% for Colombia. Mexico’s lack of dependence on commodities and China have immunized its economy from the impact of the coronavirus in a way that Brazil, Chile and Colombia are have not.

Figure 8: Commodities comprise 55% of Brazil’s exports

{kind=link}

Figure 9: Commodities comprise 83% of Chile’s exports

{kind=link}

Figure 10: Commodities account for 78% of Colombia’s exports

{kind=link}

Figure 11: Manufactured items are 71% of Mexico’s exports; commodities only 19%

{kind=link}

Figure 12: BRL tracks a Brazil-weighted commodity index with net crude imports & exports

{kind=link}

Figure 13: Chilean peso closely tracks its copper-heavy commodity index

{kind=link}

Figure 14: COP often moves in tandem with Colombia’s energy and ag-heavy commodity exports

{kind=link}

Commodities face short and long-term demand and supply issues. In the short term, the coronavirus is likely to be impactful on Chinese growth in the first quarter. Since China is the preeminent consumer of commodities, this is bad news for Brazil, Chile and Colombia. However, it is likely to have little impact on Mexico, whose manufacturers often compete with China rather than export to it.

Longer term, commodity markets face the issue of abundant supplies. Fracking has transformed the US from an energy importer into a net exporter and contributed to a global oversupply of petroleum, putting substantial downward pressure on prices. Metals production has also boomed: today’s mining supply of copper is double that of a quarter century ago while production of aluminium and iron ore has tripled over the same period. Brazil, Russia and Ukraine have led a surge in the production of key crops such as soybeans, corn and wheat. Booming supply makes markets highly sensitive to short-term fluctuations in demand. China’s demand for oil may have fallen by about 750,000 barrels per day in the first quarter of 2020 - equivalent to about 0.75% of global supply and enough to contribute to a more than 8% drop in prices since the outbreak of the coronavirus in China became known to the world in mid-January. Copper prices have also fallen by a similar percentage.

While BRL, CLP and COP suffer when Chinese demand for their goods declines, MXN is closely tethered to USD. The US economy is robust. Building permits are soaring, heralding a boom in housing starts. Credit spreads remain exceptionally tight, indicating that the labor market will continue to add jobs at a decent clip and a strong employment market is likely to underpin US consumer spending in the months ahead. Moreover, Mexico is no longer a net importer of oil and buys a substantial amount of natural gas from the US. As such, low prices for these two commodities is a net benefit to Mexico, even if it’s not great news for the Mexican energy giant PEMEX.

So, what could possibly turn the tables on MXN and cause a resurgence of its Latin peers? For starters, Chinese efforts to stimulate growth might succeed. Even before the coronavirus outbreak, the People’s Bank of China was already cutting its reserve requirement ratio to boost liquidity in the financial system. It is also cutting rates. Moreover, Chinese consumers may spend in Q2 2020 what they weren’t able to in Q1 due to the coronavirus. Finally, the impact of the virus may already be accounted for (or even over-accounted for) in current market prices for commodities. In short, if China rebounds more quickly than expected, that might be great news for commodities and the currencies associated with them, but not for Mexico.

Then there is the issue of Mexico’s dependence on the US. The US economy is currently experiencing steady growth, which is good news for Mexico’s exports. However, there might be some clouds on the horizon. The US Treasury yield curve remains rather flat and is still inverted on the 0 to 5-year section. The private sector curve remains inverted, as it has been for much of the past year. The private sector curve is the better of the two at forecasting future growth. If the US slows while China recovers later in 2020 – that’s a big if— that could turn the tables decisively in favour of BRL, CLP and COP, which are less reliant on the US as an export market (Figures 15-18). Lastly, there is the issue of the US budget deficit. Expanding the deficit from 2% to nearly 5% of GDP has contributed to the US boom since 2017. A large deficit could be a drag on US growth in the years ahead. If so, that might affect Mexico more than its peers further south.

Figure 15: Brazil sends 23% of exports to China and 12% to the USA and Canada

{kind=link}

Figure 16: Chile sends 27% of exports to China and 17% to the US

{kind=link}

Figure 17: Colombia sends 29% of exports to US and Canada

{kind=link}

Figure 18: Mexico has the least diversified & most US-dependent export mix in Latin America

{kind=link}

Bottom Line

- MXN has outperformed LATAM peers despite weak economic performance

- BRL, CLP and COP have suffered with declines in commodities

- Coronavirus affects Brazil, Chile & Colombia more than Mexico

- Mexico is highly dependent on the US economy

Emerging Market FX Products

Our suite of Emerging Market FX products provides investors with a highly liquid platform for international trade and risk management in a variety of currencies from the Mexican peso to Russian ruble to South African rand.