{kind=link}

Lessons from 2008 and 2020

The nature of the economic disruptions during the Great Recession of 2008-09 and the Pandemic of 2020 were entirely different, and so were the monetary and fiscal policy responses. 2008 was about a financial crisis and involved a rapid deleveraging of the financial system. The pandemic of 2020 was about a forced shutdown of key parts of the service economy. There are important lessons embedded inside the differences in causes of the two recessions and the policy responses.

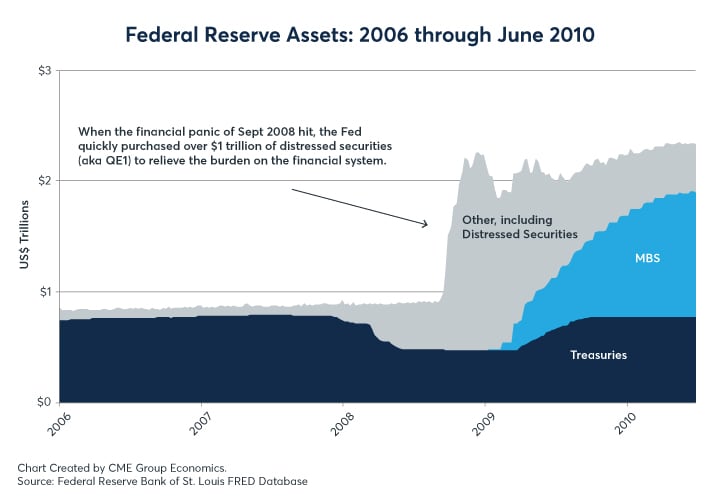

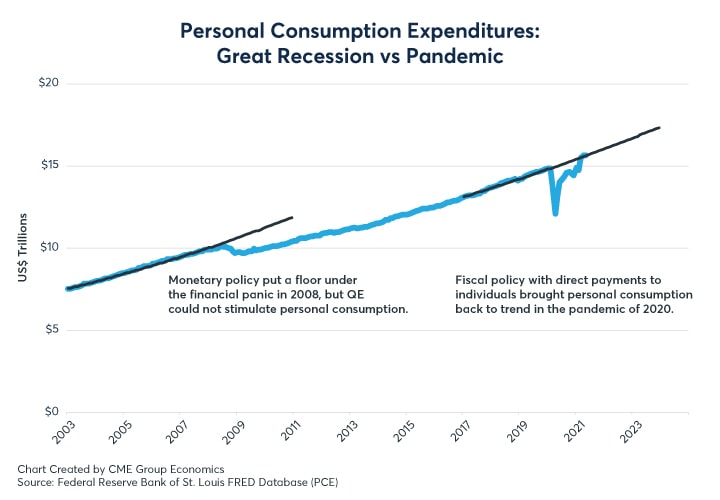

In the 2008 financial crisis, the U.S. Federal Reserve (Fed) moved quickly to purchase over $1 trillion in distressed debt securities in the first round of quantitative easing (QE) to relieve a critical burden from the financial system. Fiscal policy was expanded, too, with a large package for “shovel ready” projects, but the money went out very slowly and was not directed at individuals.

{kind=link}

{kind=link}

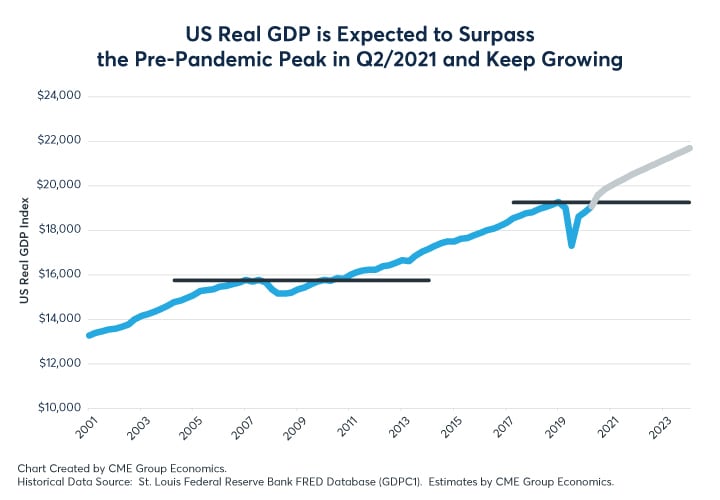

The crisis started in September 2008, triggered by the bankruptcy of Lehman Brothers and the bailout of AIG that severely disrupted the financial system from the U.S. to Europe and beyond. Equity markets abruptly fell as the economy entered a deep recession. Equity markets began a rapid recovery in March 2009. The economy began to grow again in Q4/2009. Personal consumption expenditures regained their previous peak in April 2010. The past peak of real GDP was reached in Q1/2011. However, the past peak of employment was not reached until May 2014. That is, equities recovered first, then real GDP, and jobs came last.

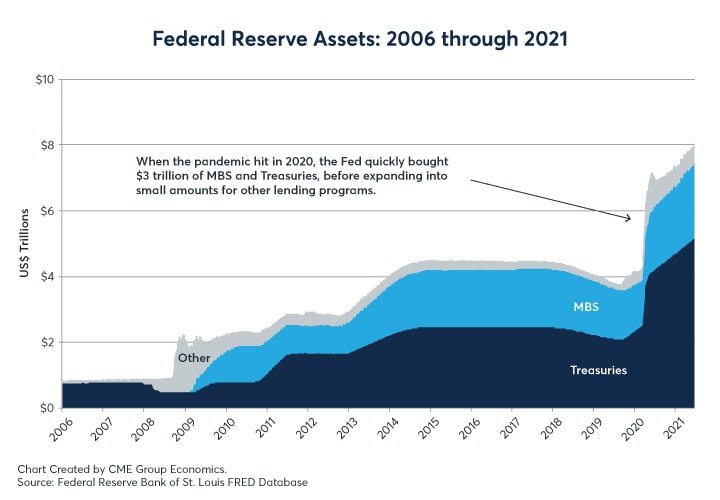

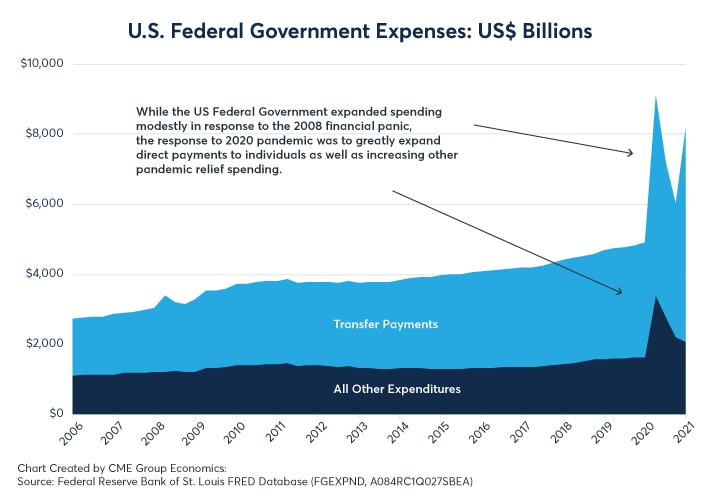

In the 2020 pandemic’s partial shutdown, the Fed responded quickly with purchases of $3 trillion in U.S. Treasury securities and mortgage-backed securities. This was not a financial deleveraging crisis, and the Fed did not purchase distressed debt. The fiscal response in 2020 was strikingly different from 2008. The U.S. federal government dramatically expanded direct assistance to individuals, while also increasing other expenditures to fast-forward the race for a vaccination and help states and local governments cope with the crisis.

{kind=link}

{kind=link}

As the pandemic spread globally, equity prices declined abruptly. The economic crisis in the U.S. hit hard in March 2020. Once the Fed’s actions were clear by mid-March, though, equity markets commenced their recovery, even as the economic situation was worsening. Personal consumption expenditures came back extremely rapidly with the direct transfer payments to individuals from the federal government. Real GDP appears on track to have reached or exceeded its previous peak by Q2/2021, although only 70% of the job losses have been recovered. As in the 2008 disruption, real GDP came returned to its previous peak much faster than jobs which have a long way to go yet in the case of the pandemic rebound.

{kind=link}

{kind=link}

What are our key take-aways from these two different economic disruptions?

First, monetary policy purchases of distressed debt were a key to putting a floor under the deleveraging financial crisis of 2008 and setting the stage for a recovery of the financial system. It matters what the central buys, and if the problem is with poor credit and an over-leveraged system, then purchases of distressed debt work much better than loans to the banking system or purchases of government debt securities.

Second, fiscal policy direct payments to individuals were key to sustaining personal consumption in the pandemic of 2020, leading to a more rapid return of real GDP to pre-pandemic levels than occurred after the Great Recession of 2008. The lesson here is that deficit spending is not sufficient, as it matters how the deficit is created. If the problem is demand, then putting cash into the hands of individuals can propel consumption expenditures back to old levels and will have a more immediate impact on bring the economy out of the recession than tax cuts or building projects.

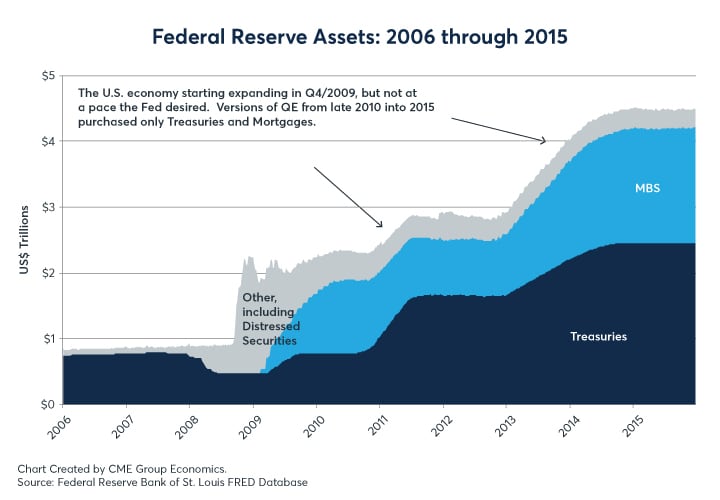

Third, in both cases, the Fed’s expansion of its balance sheet helped to engineer strong and rapid recoveries in equity markets, well ahead of the economic recovery. We also note that the Fed’s purchases of Treasuries and mortgage-backed securities after the U.S. economy was recovering, that is from late 2010 into 2015, did little or nothing to increase the pace of economic growth or encourage inflation, even though these later rounds of QE continued to support equity prices. That is, QE during the recovery from the Great Recession did not change the previous pattern of low inflation, did not induce higher inflation or additional economic growth. In the pandemic of 2020, with substantial supply chain disruptions, elevated inflation was being observed in the spring and summer of 2021. The lesson of 2010-2015 is that inflation is not necessarily elevated permanently by the pandemic burst of QE from the Fed.

The lessons from the financial crisis of 2008 and the pandemic of 2020 will be thoroughly studied by academics and policymakers for many years to come. Here are our preliminary bottom line conclusions:

- When an economic disruption is caused by a financial crisis, monetary policy assistance in removing distressed securities from the financial system can put a floor under the economy, even if it does not allow for a more rapid recovery.

- When the economic disruption is caused by a forced shutdown of part of the economy, direct fiscal policy assistance to individuals can support personal consumption expenditures and assist in a more rapid recovery of the economy.

- Monetary policy QE involving mostly government debt and not related to purchasing distressed debt to contain a financial crisis seems to support asset prices without helping create jobs or inflation.

- Regardless of the cause of the crisis and policy mix involved, real GDP recovers much faster than employment. That is, the economic disruption leads to changes in business models that encourage increases in labor productivity but do not accelerate the eventual recovery of employment back to previous pre-crisis levels.

{kind=link}

SOFR Futures and Options

Our SOFR futures and options offer unmatched capital efficiencies through margin offsets, as well as spread trading opportunities with futures for Fed Funds, Eurodollars, and Treasuries.