{kind=link}

Italy, Germany Sunday Event Risk: Market Impact

Euro-U.S. dollar (EURUSD) options traders are nervous ahead of the national elections in Italy on Sunday March 4th, and the German Social Democratic Party’s (SPD) internal vote on whether to enter into another grand coalition with Chancellor Angela Merkel. The outcome of these two events in Europe risks reverberating through numerous markets. They will also determine how easy or difficult it will be for French President Emmanuel Macron to achieve a deepening of the European Union integration with a banking union and fiscal transfers that could help the eurozone weather the next economic crisis. It could also influence the outcome of the Brexit negotiations. The results will also impact Europe’s fiscal orientation and might nudge it towards the U.S. path of greater fiscal, and less monetary, stimulus.

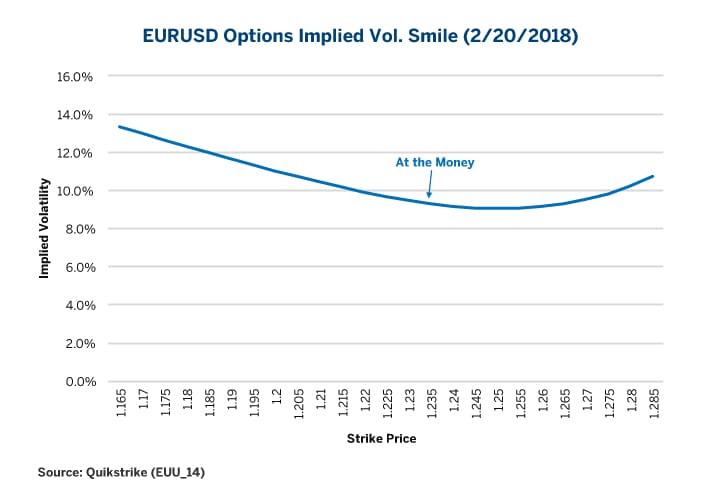

Options traders see mostly downside risk to the euro stemming from the elections in Italy and the announcement of the SPD’s coalition decision, both on Sunday. Out-of-the-money (OTM) puts on EURUSD currently cost a great deal more than OTM calls (Figure 1).

Figure 1: ‘Smiling’ but not Happily: Downside Risks on EURUSD over Next Two Weeks.

{kind=link}

That said, those hoping for a higher euro might do well if two things happen: 1) the center-right wins an outright majority in the Italian elections, and 2) the SPD votes to join Merkel’s proposed grand coalition – the third in the past dozen years. The first outcome, an outright majority for the Italian center-right, looks like a dim, but not impossible, prospect. The second outcome is highly uncertain.

Italy’s Election

For the 2018 elections, Italy will use a proportional representation system, with a 3% threshold to allocate seats, and some additional seats for the first-place winner. This method is unlikely to secure a majority for any coalition.

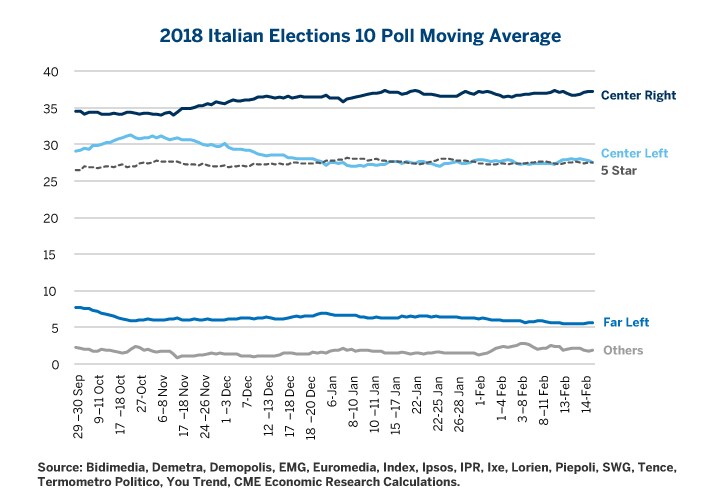

The Euroskeptic 5-Star Movement is currently the strongest individual party, with around 27% of the vote. It, however, lacks coalition partners. The four parties of the center-right coalition, which includes former Prime Minister Silvio Berlusconi’s Forza Italia and the Northern League, has been polling around a combined 37% of the vote, while the governing center-left coalition has been running around 28% – about the same as the 5-Star Movement (Figure 2). Polling in Italy is forbidden in the two weeks prior to the election so there’s no data to assess more recent voter developments.

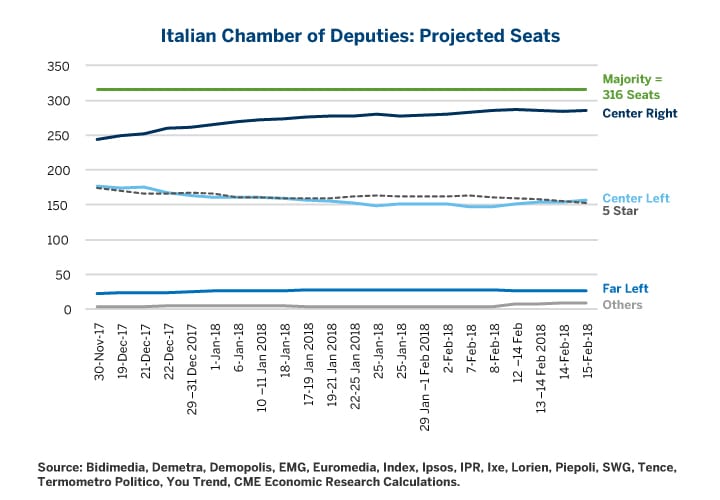

Of the 133 surveys taken since October, not one puts the center-right with an outright majority in either the lower or upper house, namely, the Chamber of Deputies and the Italian Senate, respectively (Figure 3). But some of the polls do put it within striking distance, with as many as 295 or 297 of the 316 seats necessary for a lower-house majority. If the center-right was to achieve an outright majority, this might spark a relief rally in the euro as it would reduce concerns that the 5-Star Movement will derail deeper European integration.

Figure 2: Center Rights Leading with 37% of the Vote.

{kind=link}

Figure 3: In the Lead but Short of a Majority.

{kind=link}

Even so, the size of the protest vote for both the 5-Star Movement and the far-left might be enough to shift Italy away from its current fiscally conservative stance and towards greater spending and/or tax cuts in a bid to revive one of Europe’s slowest growing economies. The main constraint in doing so is Italy’s colossal public-sector debt, which totals 134.7% of GDP – the second highest in Europe after Greece. As such, any attempt at fiscal stimulus might make the Italian bond market nervous and could provoke a flight to quality towards the German Bund, U.S. Treasury or other safe-haven assets. This would be especially true as the European Central Bank (ECB) further curtails monetary support later this year and as investors look ahead to ECB President Mario Draghi’s replacement at the end of 2019 – possibly with the more hawkish German economist Jens Weidmann.

The SPD’s Dilemma

Following the disastrous outcome that it suffered in the most recent election, SPD’s leaders initially refused to consider re-entering a grand coalition with Merkel. Being in opposition held three advantages. First, it would allow them to rebuild party support and cohesion while being out of power. Second, it’s always easier to blame the government for whatever goes wrong (and things inevitably go wrong) than to take responsibility as a part of the governing coalition. Third, being in the minority would prevent the nationalist Alternative für Deutschland (AfD) from becoming the official voice of the opposition in the Bundestag/parliament.

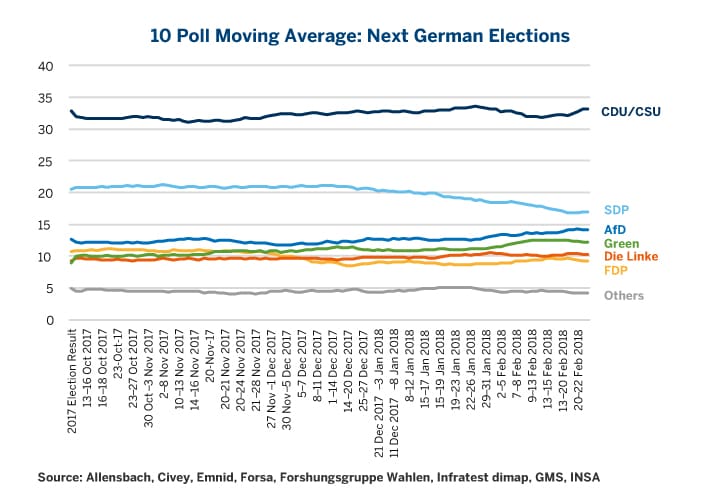

After Merkel failed to assemble a coalition with the Free Democrats (FDP) and the Greens, the SPD was obliged to come back to the negotiating table. While its leaders have agreed to coalition terms with Merkel, its rank and file are currently voting on the prospect of a third go-around with Merkel’s CDU/CSU coalition. They’re not happy about it. Since entering into coalition talks, support for the party has cratered, based on polling (Figure 4). Recently, they have been polling at around 17%, down from an already humiliating and historic low of 20.5% in the elections last fall.

Figure 4: Less and Less Grand – the Sinking Fortunes of the CDU/CSU/SPD Grand Coalition.

{kind=link}

In addition to sinking at the polls – largely to the benefit of the Greens and AfD – the SPD has been ravaged as Merkel’s junior coalition partner on two previous occasions, just as the FDP was on one occasion (Figure 5). If the SPD rank and file neglect to join this latest pact with Merkel, the euro could suffer. On the other hand, if they approve, some of those cheap call options on the euro might stand a better chance of paying off.

Figure 5: Merkel’s Junior Partners Suffer at the Polls.

| Episode 1 | Election: | 2005 | 2009 | Swing |

| Leader | CDU/CSU | 35.2% | 33.8% | -1.4% |

| Junior Partner | SPD | 34.2% | 23.0% | -11.2% |

| Episode 2 | Election: | 2005 | 2009 | Swing |

| Leader | CDU/CSU | 33.8% | 41.5% | 7.7% |

| Junior Partner | FDP | 14.6% | 4.8% | -9.8% |

| Episode 3 | Election: | 2005 | 2009 | Swing |

| Leader | CDU/CSU | 41.5% | 32.9% | -8.6% |

| Junior Partner | SPD | 25.7% | 20.5% | -5.2% |

If the SDP rank and file reject the deal with Merkel, she could limp along with a minority government, attempting to form parliamentary majorities ad hoc, on an issue-by-issue basis, or she could call for fresh elections. If the SPD rank and file reject the deal with Merkel, she could limp along with a minority government, forming coalitions on an ad hoc basis or she could call for fresh elections. The latter seems likely to produce another inconclusive outcome, albeit one with a strengthened AfD which would make the task of forming a coalition after the next election even more difficult.

Either way, if the SPD rejects the grand coalition, Germany will likely be a weak and unreliable partner for France’s Macron and might find itself pushed towards loosening the purse strings on fiscal policy to forestall a further rise in support for the extreme right. Fiscal expansion might be bearish for the euro and bonds but a positive for European and, perhaps, global equities. Should the agreement get approved, Germany might still adopt a looser fiscal stance but, under the influence of the SPD, might more enthusiastically embrace a deeper European integration than it has in the past. This last item will still be a tough sell, however, with the CDU/CSU which has the Euroskeptic AfD breathing down their neck and threatening to steal more of their voters.

Bottom Line:

- Euro call options are cheap compared to puts going into this weekend’s events

- Italy’s vote looks likely to produce no governing majority but a center-right outright win is still possible

- The SPD’s internal vote on a coalition with Merkel will determine if there’s another grand partnership, if Germany has to call for new elections or move to a minority government

Sunday Event Risk

Italians go to the polls on Sunday, March 4, to elect a new government while on the same day German Chancellor Angela Merkel will find out if she can form a grand coalition government in her fourth term in office. Manage risk with greater precision with Wednesday EUR/USD options.