{kind=link}

Is Oil Rally Getting "Stop" Signal from Soybean Oil?

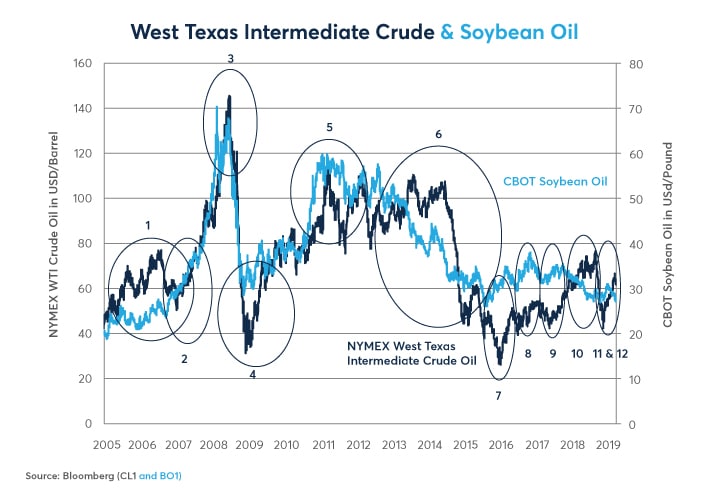

For the past 15 years, soybean oil prices have often forerun movements in crude oil prices, a phenomenon possibly tied to biofuel mandates in 65 countries and the relatively small size of the vegetable oil market compared to crude oil. By our count, there have been a dozen major episodes of soybean oil either topping out or hitting bottom ahead of crude oil over the past 15 years (see list below).

Soybean oil prices peaked on February 6 this year and have since fallen by 14%. Over the same period, prices for West Texas Intermediate (WTI) crude oil have advanced by 14%. If past cycles are any indication, the current rally in crude oil may not turn out well. In fact, crude oil’s rally peaked (thus far) on April 23, 2019. Indeed, the economics of crude oil remain dominated by further gains in vehicle efficiency and soaring U.S. production. Both factors are bearish for crude oil.

Figure 1: Soybean Oil Prices Often Lead Crude Oil Prices.

{kind=link}

Our related content:

- Crude Oil’s Next Move? Clues from Soybean Oil

- Is Crude Oil Taking Cue from Vegetable Oils?

- Veg Oil vs Crude Oil: Tail Wagging the Dog?

- The Short and Long of Oil

If there is something that could make soybean oil ineffective as a momentum indicator of crude oil going forward, it is politics. Faced with tougher U.S. sanctions, Iran will not abide by portions of the Joint Comprehensive Plan of Action (JCPOA), commonly known as the Iran nuclear agreement. Additionally, the US has accused OPEC-member Iran of posing a threat to U.S. forces in Iraq and elsewhere in the Middle East and has sent an aircraft carrier strike group to the region.

In addition to the Iranian situation, Algeria, another significant oil producer, is attempting to negotiate a peaceful transfer of power after President Bouteflika abdicated last month. Meanwhile, the situation in Venezuela remains as chaotic after opposition leader Juan Guaido’s failed attempt to oust President Nicolas Maduro from power.

In the past, such escalation of the tension has caused crude oil prices to rally above where soy oil prices would suggest they should be for months or even years on end. That was the case in 2013 and for most of 2014 when vegetable oil prices were crashing but the consequences of the Arab Spring and the Iran nuclear issue kept crude oil prices high. At the end of 2014, as the Iran nuclear negotiations were getting underway, Saudi Arabia pulled the plug on supporting oil prices, leading to a 76% crash in WTI prices over the next 15 months. A similar vegetable oil-crude oil price divergence occurred in 2018 -- in Q2 and Q3 2018 when the U.S. initially pulled out of the Iran nuclear deal. Crude oil prices ignored a 20% spring- and summer-time slide in soy oil prices before crashing 40% in Q4.

Here is a list of the previous episodes:

-

From January 2005 to August 2006 WTI crude oil prices nearly doubled from $43 to $77 per barrel. Soybean oil showed little enthusiasm for this rally, peaking at 27.54 U.S. cents per pound in early July 2006 before dipping around 10% ahead the peak in WTI the next month. WTI prices crashed from $77 to $51 by January 2007, catching up with soybean oil prices on the downside.

-

While crude oil prices were in the process of crashing to the level of soybean oil prices, soybean oil prices hit bottom in November 2006 – two months before crude oil— and began an enormous rally that took prices from 23.58 U.S. cents to 71.26 U.S. cents by March 2008. WTI prices waited two months to get on board this mega-rally and went from $51 in January 2007 to $147 in July 2008.

-

After peaking in March 2008, soybean oil prices fired a shot across the bow of the still rallying crude oily. Soybean oil prices fell from 71 U.S. cents to 48 U.S. cents – more than a 30% drop before rebounding to 68 U.S. cents on June 16, 2008. Even this second, lower peak in soybean oil prices occurred nearly one month before crude oil peaked at $147 on July 11, 2008. By the time WTI hit its all-time high, soybean oil prices were 5% off their June peak and nearly 10% below the March 2008 all-time high.

-

During the financial crisis, soybean oil prices cratered to 28 U.S. cents on December 5, 2008, before staging a rally into year’s end. By contrast, crude oil prices didn’t hit bottom for another three weeks on December 24, 2008, when they closed at $35.35. In 2009 and 2010 as both markets recovered, soybean oil again led crude oil in most of the minor zigs and zags on the way upward.

-

Soybean oil prices peaked on February 3, 2011 at just below 60 U.S. cents, having more than doubled their late 2008 low. WTI prices didn’t peak for nearly three months when they hit $114 on April 29, 2011.

-

At this point, soybean oil and WTI began their great divergence. In the wake of the Arab Spring, perceived geopolitical risks kept WTI and other oil benchmarks trading within about 25% of their 2011 highs for the next three-and-a-half years. Soybean oil prices, by contrast, had fallen 40% off their 2011 highs by early 2014 and after a brief bounce began crashing again in the summer of 2014 until they got to around half of their April 2011 levels. This presaged the late 2014 collapse in crude oil prices which eventually took WTI to as low as $26.

-

Once again, soybean oil prices hit bottom first, reaching a low of 25 U.S. cents in August 2015 – a 60% fall from the April 2011 peak. WTI prices hit bottom in February 2016 – a full six months later— at $26 per barrel, down over 75% from the local high in 2011.

-

By the time crude oil hit bottom on February 11, 2016, soybean oil prices were more than 20% off their lows. They reached a local peak of 41 U.S. cents on April 19, 2016 – a gain of more than 60% from the lows. Crude oil prices followed them higher but peaked almost two months later on June 8, 2016, at just over $50, up almost 100% from their lows.

-

When crude oil prices reached their local high of $51 on June 8, soybean oil prices had already fallen as much as 12% and eventually hit bottom on July 22, 2016, at 29 U.S. cents. WTI prices hit bottom two week later on August 2, 2016 at $39.

-

Soybean oil prices peaked at 37 U.S. cents on December 27, 2016, and by April 11, 2017, had fallen to around 31 U.S. cents. Meanwhile, WTI prices plateaued at around $54 between December 12, 2016, and March 7,

2017, before eventually correcting lower to $43 by June 22, 2017 – lagging soybean oil by about three months.

-

Soybean oil prices peaked out at 35 U.S. cents on November 9, 2017, and made a double bottom on September 18 and November 26, 2018, at 27 U.S. cents. Supported by a perceived increase in U.S.-Iran tensions, WTI didn’t peak until October 3, 2018, at $77 before falling to $43 on December 24, 2018.

-

Soybean oil prices rallied from $27 to $31 U.S. cents between November 26, 2018, and February 6, 2019, anticipating the rebound in WTI from $43 the day before Christmas Day to a peak (so far) of $66 on April 23.

-

Soybean oil prices fell back to 27 U.S. cents from their peak of 31 U.S. cents in February. Although oil has not yet surpassed its $66 peak as of this writing, it remains unclear if it will follow suit to the downside. That may depend on events in the Middle East and elsewhere.

Bottom Line

- Soybean oil prices often forerun changes in crude oil prices.

- The recent plunge in soybean oil prices might foreshadow a slump in crude oil prices.

- A rise in political tensions in the Middle East and elsewhere could let crude oil defy the downward trend in soy oil prices.

Ag Options

Agricultural Options offer the flexibility for effective risk management, as well as the ability to execute volatility strategies or event-driven trades. Our portfolio of Grain, Oilseed, Livestock, and Dairy products provides an array of opportunities from outright and spread options.