{kind=link}

How Will Rising Interest Rates Impact Growing Budget Deficit?

Since 2016 the U.S. budget deficit has expanded from 2.2% to 4.5% of GDP. While it’s not unusual for deficits to expand during periods of rising unemployment, it is almost unprecedented for deficits to grow during the advanced stages of an economic expansion as unemployment rates continue to fall.

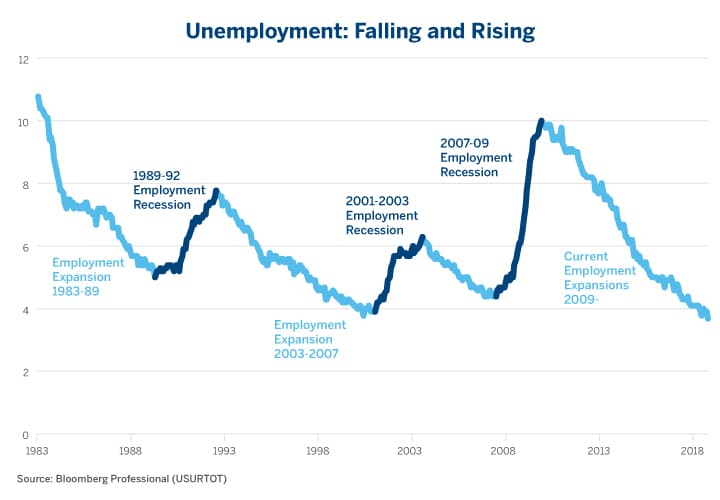

Since 1983, the U.S. has experienced four employment expansions, which we define as periods of declining unemployment rates, and three employment recessions that are characterized by rising unemployment rates (Figure 1).

Figure 1: Unemployment Hit its Lowest Since 1969 but Deficits are Unusually Large.

{kind=link}

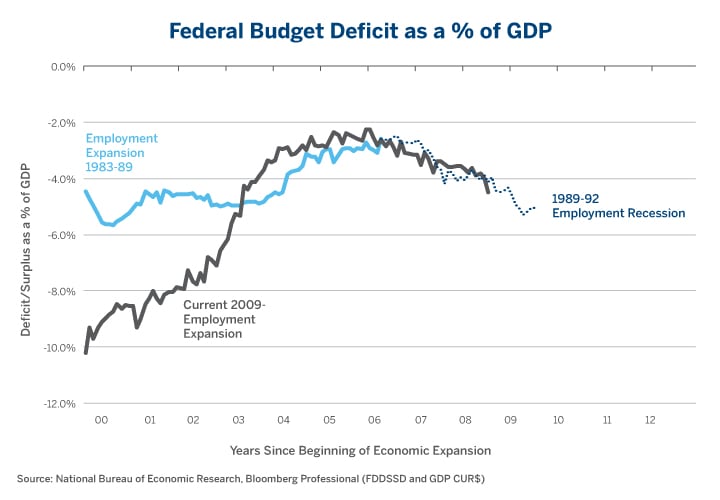

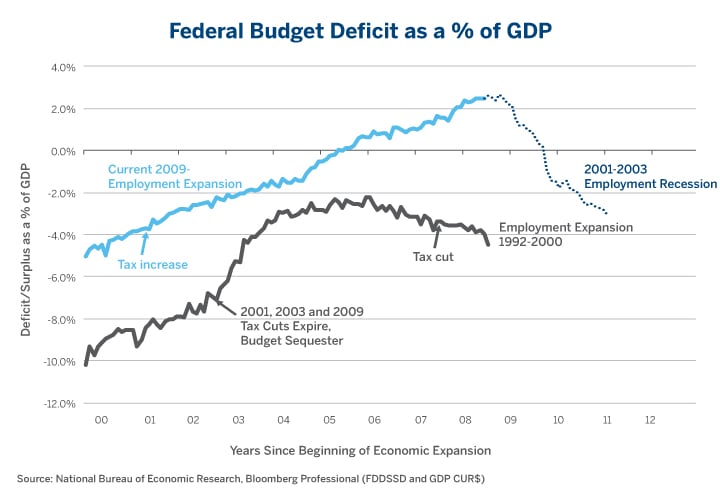

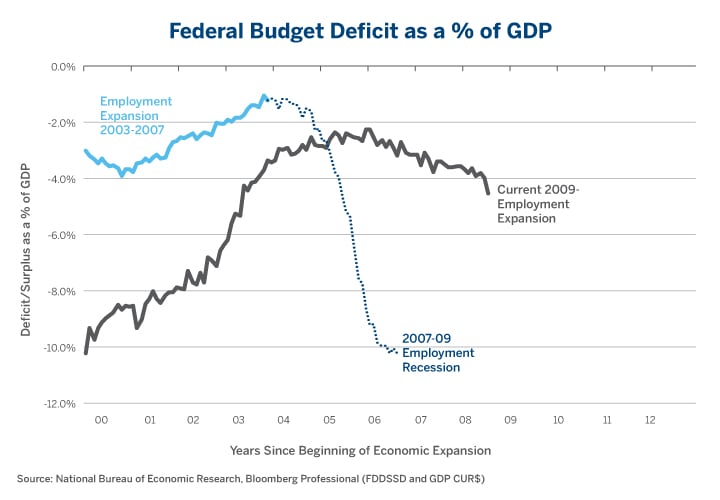

During the employment expansions, budget deficits typically shrink. Greater employment means more taxpayers and fewer people collecting government benefits. As such, deficits shrank as the economy added jobs between January 1983 and March of 1989 (Figure 2), July of 1992 and December 2000 (Figure 3) and between June 2003 and April 2007 (Figure 4). This was also the case during the current employment expansion which lasted from November 2009 to the end of 2016.

Figure 2: Deficits Shrank from 5% to 2.5% of GDP During the 1980s Expansion.

{kind=link}

Figure 3: 1993 Tax Hike Helped Turn a 5% of GDP Deficit into a 2% of GDP Surplus by 2000.

{kind=link}

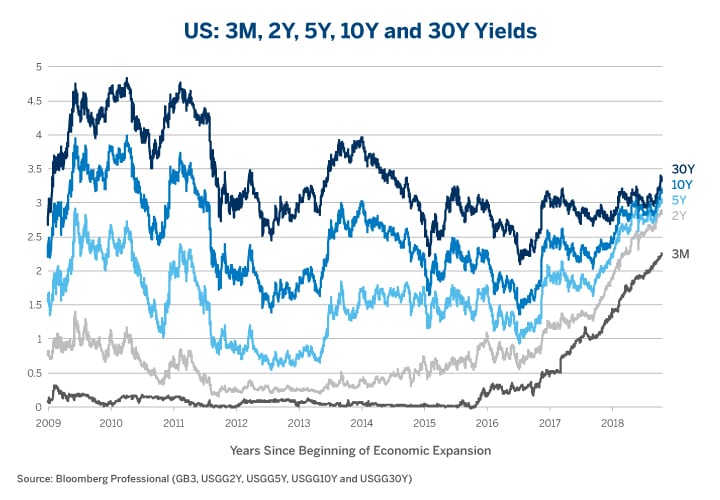

As deficits shrank from 10% of GDP in late 2009 to 2.2% in 2016, short-term interest rates stayed low and long-term interest rates fell. Part of the reason for this was that with little fiscal support, the Federal Reserve (Fed) shouldered the burden for fostering the economic recovery. In 2011, the budget sequester sharply limited spending growth and at the end of 2012 a series of tax cuts enacted in 2001, 2003 and 2009 expired, sending taxes soaring on January 1, 2013. Amid strong fiscal headwinds, it was up to the Fed to keep the expansion going with low short-term interest rates. Moreover, as deficits dwindled, the yield on the 30Y bond fell from a range of 4.0-4.7% in 2009 and 2010, to a range of 2.2-3.2% by 2016. Low short and long-term interest rates spurred sufficient economic growth to offset fiscal tightening.

Figure 4: In the 2003-2007 Expansion, Deficit Shrank from 4% to 1% of GDP.

{kind=link}

By contrast now, with tax cuts and surging government spending, fiscal policy is stoking economic growth. Interest rates are moving higher across the board as deficits soar (Figure 5). Fiscal policy has relieved monetary policy of the burden of stimulating the economy and interest rates are going higher. Higher rates, however, threaten a further expansion of fiscal deficits. As Treasury bills and bonds roll into maturity, they will have to be reissued at higher rates, expanding the deficit. As such, an easy fiscal policy is expanding deficits, allowing for higher interest rates, which in turn expands the budget deficit even further.

Figure 5: Deficits Shrank, Interest Rates Fell from 2010-16. These Trends Reversed in 2017.

{kind=link}

With the deficit as large as it is, what happens if the economy heads into a downturn? This question is especially pertinent given the possibility that the Fed may inadvertently overtighten policy and raise the risk of a downturn in 2020 or 2021. Over the last eight downturns in the employment market, the deficit expanded by 4% on average with a range of 1.2% to 9.2% (Figure 6).

Figure 6: Recessions Expand Deficits.

| Budget Surplus/(Deficit) Before and After Recessions | |||

| Employment Recession | Before | After | Change |

| 1957-58 | 0.9% | -2.4% | -3.3% |

| 1960-61 | 0.1% | -1.2% | -1.3% |

| 1969-70 | 0.3% | -2.0% | -2.3% |

| 1974-75 | -0.4% | -3.9% | -3.5% |

| 1979-82 | -1.5% | -5.7% | -4.2% |

| 1989-92 | -2.6% | -5.0% | -2.4% |

| 2001-03 | 2.4% | -3.0% | -5.4% |

| 2007-09 | -1.0% | -10.2% | -9.2% |

| Average | -0.2% | -4.2% | -4.0% |

Source: https://www.thebalance.com/us-deficit-by-year-3306306 for date prior to 1983;

Post-1983, Bloomberg Professional (FDDSSD and GDP Cur$)

If the economy does go into a downturn, the budget deficit could easily expand from its current 4.5% of GDP towards 8-10% of GDP. This could make it even more difficult to offer fiscal stimulus than it was in 2008 and 2009. When that recession began the deficit was only 1% of GDP. If a recession were to begin in 2020 or 2021, the deficit could be close to 5% of GDP before any downturn even gets underway.

During the 1980s and early 1990s, tackling the deficit became a major political priority. The 1986 tax reform was revenue neutral and not a tax cut. The Gramm-Rudman-Hollings Deficit Reduction Act of 1985 limited the growth in spending.

Perhaps the lack of appetite for reducing U.S. budget deficits is a lesson of history. Tax increases in 1990 and 1993 proved politically toxic for incumbent parties amid the expiration of a series of tax cuts in 2013. Voters didn’t reward incumbent parties for reduced deficits and instead punished them at the polls for having raised taxes. As such, growing budget deficits might be in store in the future, which could eventually weigh on the U.S. dollar and crowd out investment and growth in the private sector.

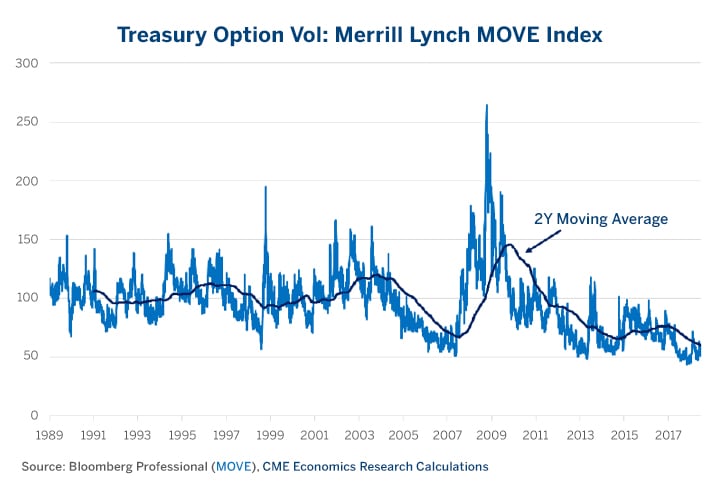

For the moment, options markets seem unconcerned about the direction of fiscal policy. Treasury options are trading near record lows even after a recent miniature spike in volatility (Figure 7). Given the U.S. fiscal outlook and the possible increased volatility that could come in both equity and bond markets as yields push higher, one must wonder if Treasury options traders are complacent in the face of growing fiscal and market risks.

Figure 7: Options Markets Seem Remarkably Unconcerned About U.S. Fiscal Trajectory.

{kind=link}

Try the Liquidity Tool

Assess market liquidity across asset classes with the Liquidity Tool that tracks the three vital components of book depth, bid-ask spread and the cost to trade across time zones. When is it best to trade a certain number of contracts in a particular product from anywhere in the world? Ask the tool.