{kind=link}

Grains: Midsummer Rallies Turn to Fall Nightmares

Almost like clockwork for the past five years, corn rallied in the spring and early summer before topping out between May 30 and July 15. Similarly, wheat experienced midsummer rallies that were especially notable in 2015, 2017, 2018 and this year. In the case of wheat, the peaks came between late June and early August. In each case, these rallies related to concerns about the state of the North American planting and growing season. This was especially true this year when weather in the US Midwest was especially inclement, with extensive flooding delaying planting.

Yet, in each case the price of corn and wheat came crashing down as the growing season wore on and both acreage and yield turned out to be not as bad as feared, as was evident in the August 12 crop report and subsequent 5% single-day declines in corn and wheat prices. The crop report showed severe, localized damage to crops in certain areas: Southeastern South Dakota and Southwestern Minnesota, parts of Northern Illinois and Northeastern Ohio. Other regions were showing more average production, and certain areas like Northern Iowa and parts of Kansas and Nebraska even showed higher production.

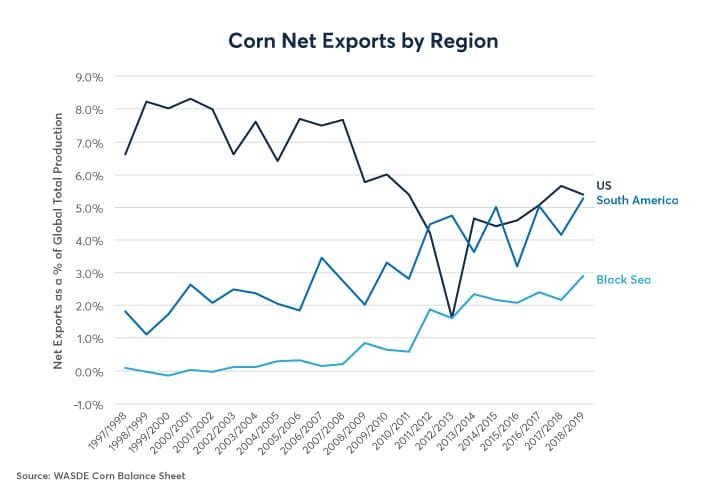

Corn’s inability to sustain a summer rally is intertwined with soaring production in the Black Sea region and South America, where the global cost of production is increasingly being determined. Over the past decade, South America went from exporting the equivalent of 2% of global corn production to about 5.5% – rivaling the US. Meanwhile, the Black Sea region has gone from essentially producing a domestic-only supply to exporting the equivalent of 3% of global corn production (Figure 1).

Figure 1: South American and Black Sea Corn Exports are Soaring.

{kind=link}

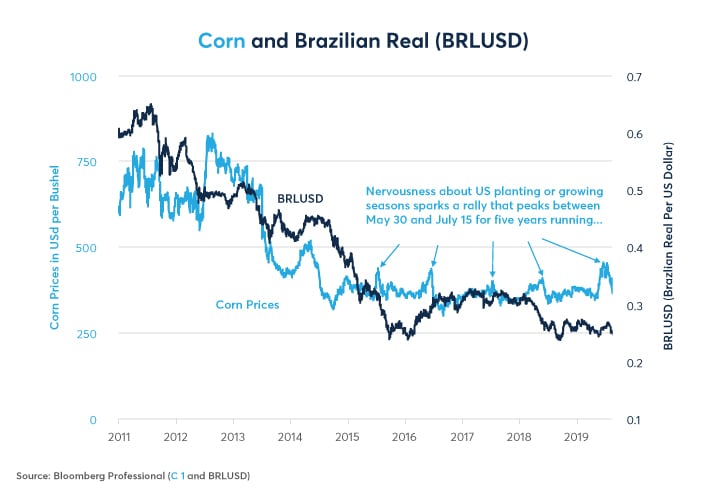

Little surprise then that corn prices track both the Brazilian real (BRL) and Russian ruble (RUB) (Figures 2 and 3). When those currencies fell versus the US dollar in 2014 and 2015, it lowered their marginal cost of production from a USD perspective. That marginal cost of production appears to serve as a soft floor – the price below which supply will likely be taken off the market. Increased corn exports from South America and the Black Sea region also diversify global production and make the markets less reactive to inclement weather in the Midwestern United States.

Figure 2: Corn Follows the Brazilian Real Closely.

{kind=link}

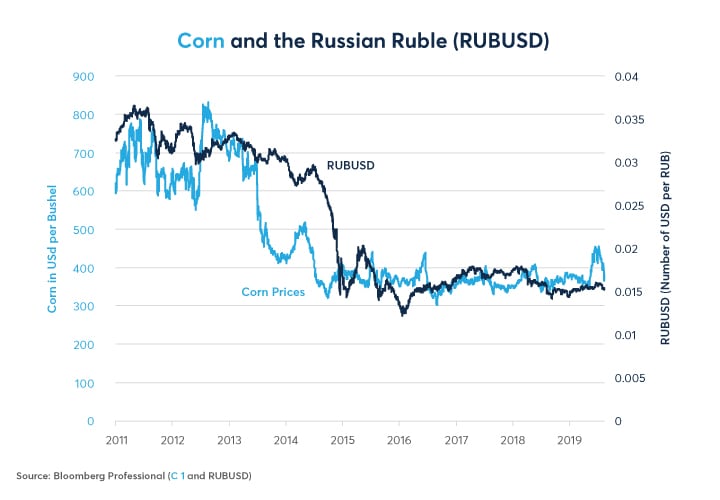

Figure 3: Corn is Also Increasingly Tied to the Fate of the Russian Ruble.

{kind=link}

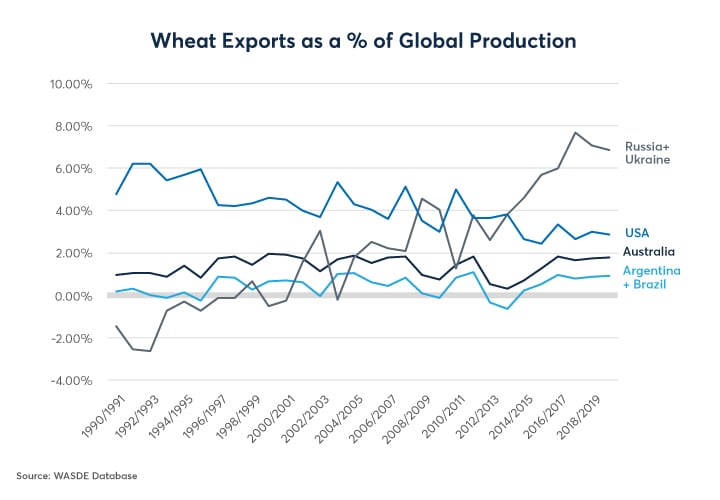

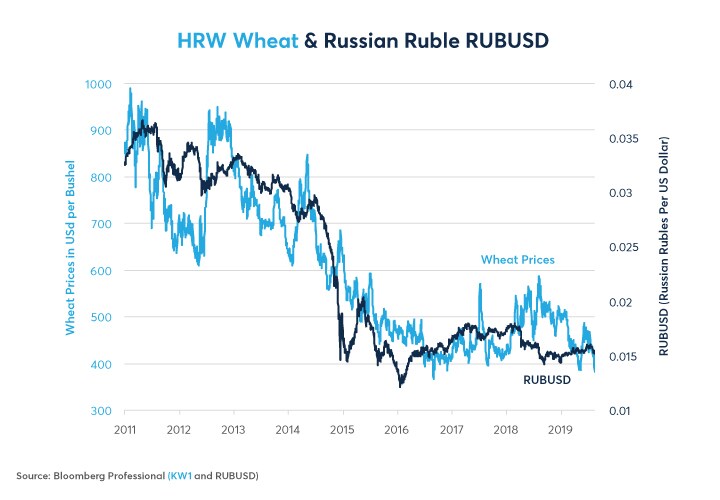

Wheat also has a more diversified set of global growing regions as exports from the Black Sea now dwarf those from North America (7% versus 3% of global production – Figure 4). As such, wheat prices move broadly in line with the Russian ruble (Figure 5). Other currencies like the Canadian and Australian dollars also exert some influence and both of those currencies have tracked commodity prices (as well as the real and the ruble) lower versus the US dollar, putting American farmers at a competitive disadvantage.

Figure 4: Black Sea Wheat Exports Now Dominate Those from the US and Other Regions.

{kind=link}

Figure 5: Wheat Prices Increasingly Track the Ruble as Russian Farmers Set Marginal Costs.

{kind=link}

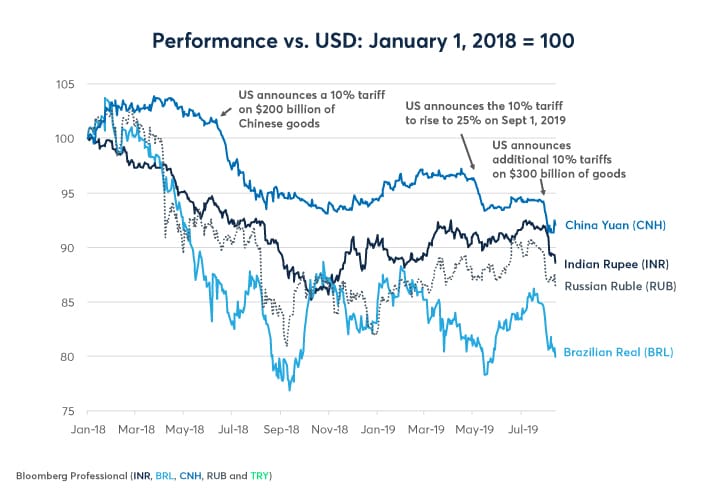

This is where the trade war is hurting US corn and wheat farmers. Although they are not directly impacted by the Sino-US trade dispute in the manner that soybean farmers are, the escalation of tensions is sending the dollar higher and the yuan (CNY) lower. As CNY falls, it is pulling BRL and RUB down with it and could take corn and wheat lower as well (Figure 6). Although RUB and BRL got a boost from Brazil and Russia’s pension reforms, both nations are now on the verge of a recession. As such, the trade war escalation augurs as poorly for corn and wheat farmers as it does for soybean producers.

Figure 6: Escalating Trade War Could Further Weaken Yuan Taking BRL, RUB, Corn, Wheat with It.

{kind=link}

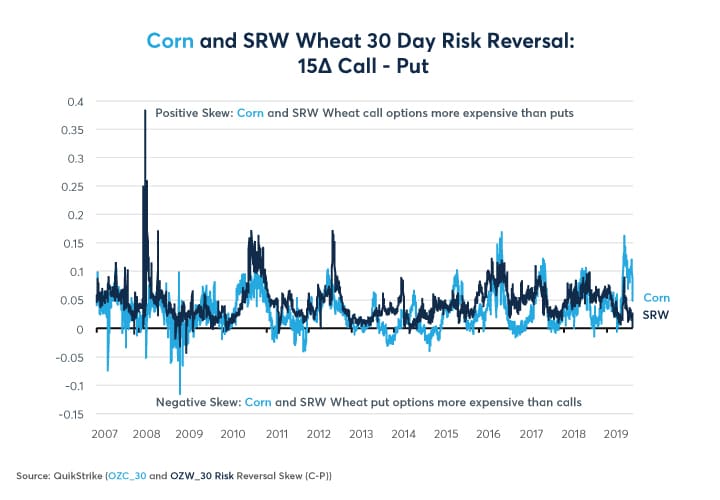

What’s particularly intriguing is how wrong the options market got the latest moves in corn and wheat. Both markets were sharply skewed to the upside: out-of-the-money (OTM) calls were much more expensive than OTM puts. Traders were anticipating a great deal more potential extreme upside than downside (Figure 7).

Figure 7: Corn, Wheat Options Skewed Positive Before the August 12 Selloff.

{kind=link}

As we have noted in past research, it is nearly always the case the OTM calls are more expensive than OTM puts in corn and wheat even though there is no evidence that either market actually experiences more extreme upside than downside moves on a daily basis. The greater diversification of growing regions, surging South American and Black Sea production as well as the potential harm of an escalating US-China trade war further call into question the persistent upside skew (or “risk reversal”) in agricultural options prices.

Bottom Line

- Corn and wheat markets have failed to sustain rallies for five summers in a row.

- Each time fears over the US planting and growing seasons proved exaggerated.

- Corn production increasingly dominated by the Black Sea region and South America.

- Wheat production is increasingly concentrated in the Black Sea region.

- Greater crop-exporting diversification makes North American weather less impactful on price.

- The trade war threatens to weaken the yuan and take BRL, RUB, corn and wheat down, too.

Ag options

Take advantage of hedging flexibility with Short-Dated New Crop options on Corn, Soybeans, Soybean Meal, Soybean Oil, South American and Wheat futures.

{kind=link}

https://www.cmegroup.com/insights/trade-war.html?itm_source=trade_war_developments_article_page&itm_medium=cmegroup&itm_campaign=economic_research_trade_war&itm_content=right_rail_banner