https://www.cmegroup.com/content/dam/cmegroup/education/images/articles/bnr-erik-norland.jpg

{kind=link}

Glimmer of Hope for Battered Brazilian Real

Over the past year, Brazil has taken a beating on the economic front. The Real (BRL) has tumbled nearly 35% versus the US Dollar (USD), driven lower by a number of factors, including:

If China continues to devalue the Renminbi, it will likely contribute to downward pressure on emerging market currencies in general.

- A general rise in the USD versus other currencies as US labor market continues to strengthen, and as the Federal Reserve gears up for a rate increase.

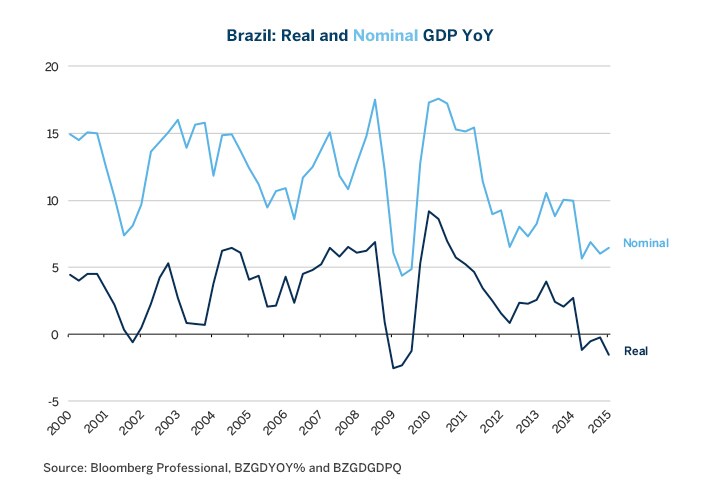

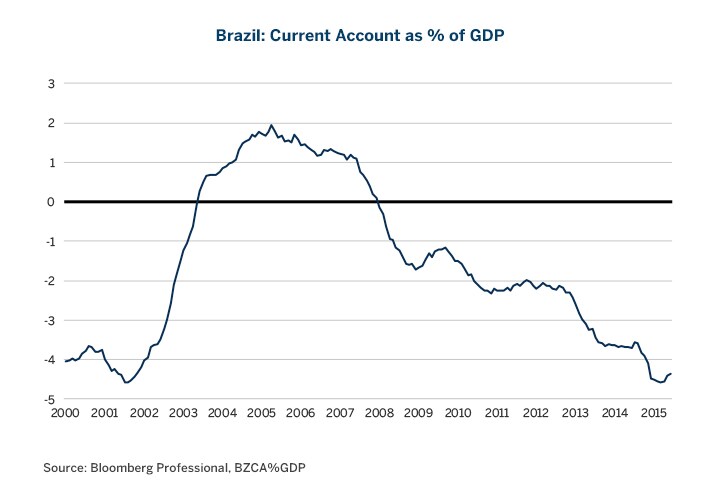

- Brazil’s economy has fallen into recession, and has a large trade deficit (Figures 1&2).

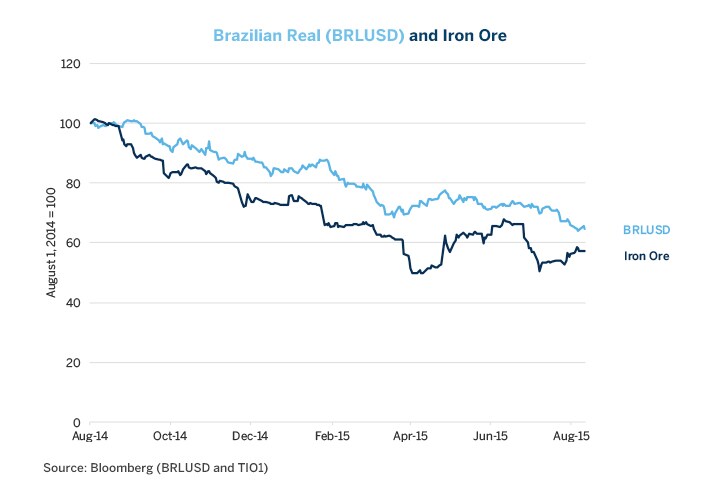

- A plunge in prices of iron ore (Figure 3), of which Brazil is the world’s second largest exporter, has shaved up to 0.7% off the country’s GDP.

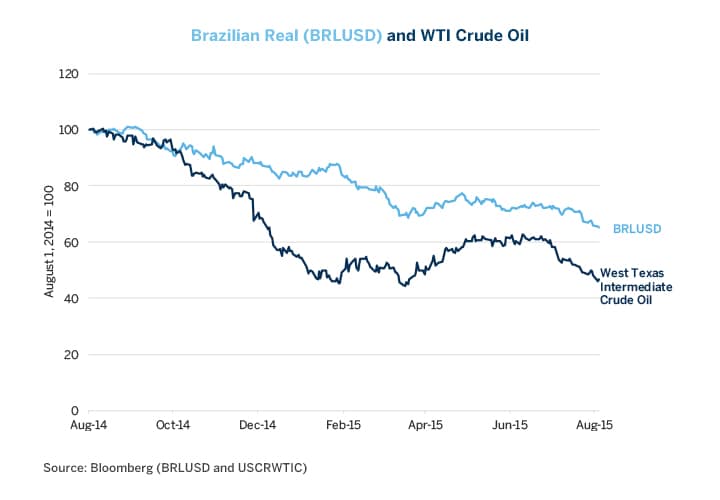

- Collapsing crude oil prices have hurt further investments in the sector in Brazil (Figure 4).

- A scandal involving state-run oil company Petrobras has rocked Brazil’s establishment.

Figure 1: Back in Recession.

{kind=link}

Figure 2: Brazil's Trade Gap is Beginning to Narrow.

{kind=link}

Figure 3: Brazil is the World’s Third Largest Producer and Second Largest Exporter of Iron Ore.

{kind=link}

Figure 4: Collapsing Crude Oil Prices are Curtailing Investment in (and hopes for) Brazil's Oil Sector.

{kind=link}

Outlook: It Depends on your Perspective of the BRL.

Whether the Real is undervalued and about to hit bottom or has further downside depends upon how one views the currency, and to what it is compared to.

Spot USD Perspective: Versus the USD, spot BRL probably has further to go on the downside. The US Federal Reserve is, by all appearances, determined to raise rates. Barring weak employment numbers, a renewed collapse in commodity prices or a sharp sell-off in the equity market (any of which could happen), the hike could come as soon as September.

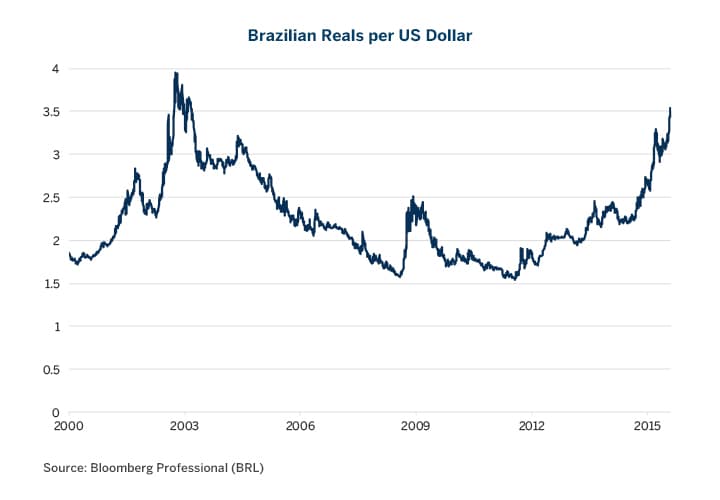

As such, it wouldn’t be surprising if the Real makes a move to test its all-time low from 2002 of 4 BRL per 1 USD (Figure 5). This is less than 15% below the current rate.

Figure 5: Retesting the 2002 Low and Heading Back to 4 Reals / 1 USD on Spot?

{kind=link}

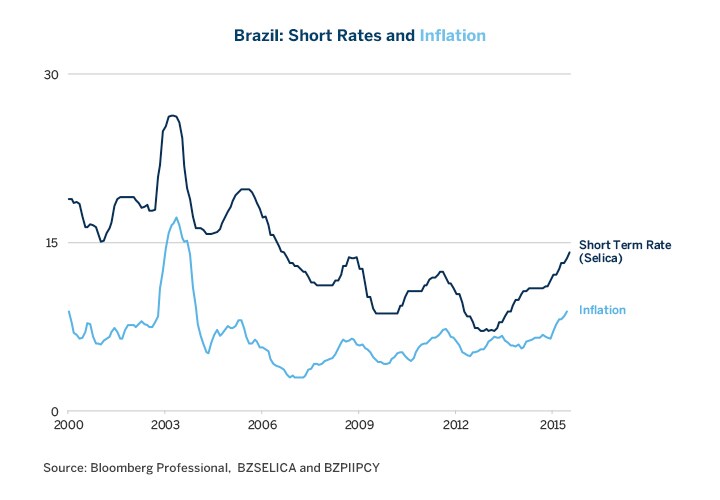

An Interesting Carry Trade versus USD: Investors typically don’t earn the spot return; they earn the spot return + the interest rate differential. While the Federal Reserve has been busy contemplating a fairly notable move from its current range of 0-0.25% rates to, perhaps, 0.25%-0.50%, Banco Central do Brasil has been on a tear, raising rates to 14.15% (Figure 6). Thus, between the BRL and USD, there is about a 14 percentage point gap in interest rates. This gives a lot of cushion to long positions in BRL, even if the Real continues its downward course vs. the USD, with carry accumulating at over 1% per month. Moreover, while real rates in the US are either close to zero (headline inflation) or negative (core inflation), Brazilian real rates are solidly positive. With the SELIC (Special System for Settlement and Custody) rate at 14.15%, and inflation at 8.89%, real rates in Brazil are five percentage points above inflation – something that the US hasn’t seen since the 1980s.

Figure 6: Banco Central do Brasil is on a Tear with Rates 14% above US levels, Generating Strong Carry.

{kind=link}

In addition to strong carry, there are other reasons to be cautiously optimistic regarding the BRL. First, Brazil’s trade deficit will probably narrow. The lag effects of the recent decline in the currency combined with the weakness in domestic demand should curtail imports significantly while the weaker BRL lifts exports. On the export side though, Brazil has tough competition from countries and regions whose currencies have also weakened, notably Chile, Colombia, Japan, and the eurozone. If China continues to devalue the Renminbi, it will likely contribute to downward pressure on emerging market currencies in general.

Another factor in the BRL’s favor is the Petrobras scandal. That probably sounds counterintuitive, especially since we cited it as a reason for the BRL’s recent weakness. What could possibly be good about prosecutors alleging that high-ranking officials may have taken as much as four billion BRL (about $1.2 billion) in bribes from the state-run oil producer? Nothing, in the short-to-intermediate term. Like the Watergate scandal, which contributed to downward pressure on the US Dollar in 1973 and 1974, among other things, Petrobras-gate hasn’t been kind to the BRL in 2014 or 2015. That said, Watergate proved that the US Constitution and legal system works in the face of a high-level scandal, which led to President Richard Nixon’s resignation. Similarly, the fact that Brazilian prosecutors have been able to level charges against high level officials from the administrations of President Dilma Rousseff and her predecessor Luiz Inacio Lula da Silva, indicates that the country has evolved into a stable, mature democracy governed by rule of law. In the long run, this is good news for the BRL.

Lastly, with the Federal Reserve seemingly getting ready to hike rates, comparing any emerging market currency to the US Dollar is a difficult task. Therefore, there is less reason to compare the BRL to the USD than to a close peer like the Mexican Peso (MXN).

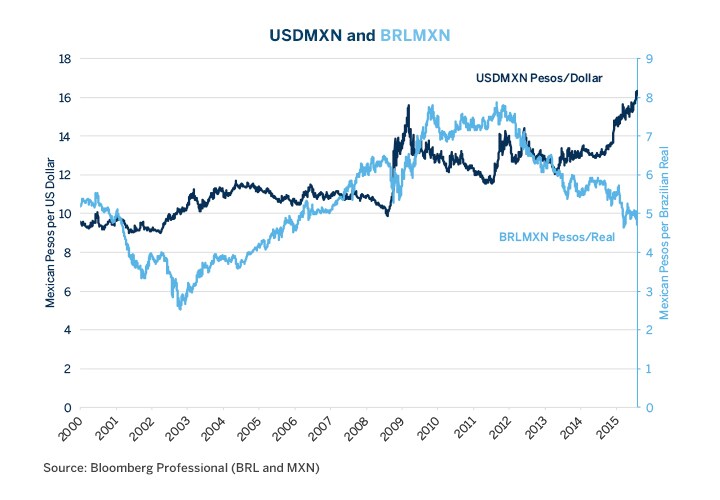

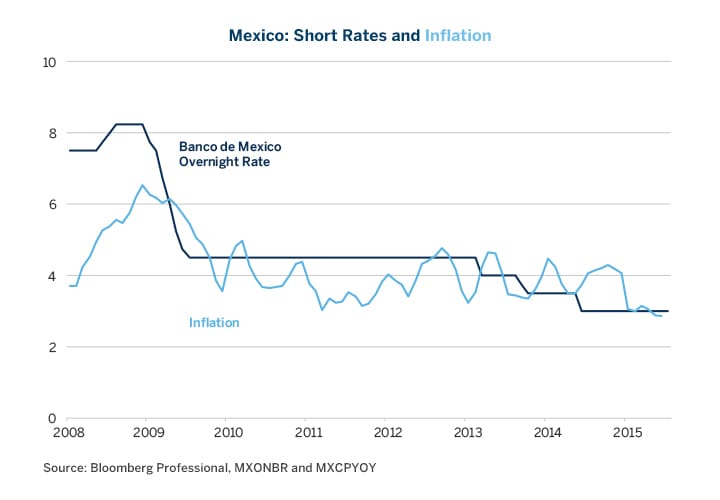

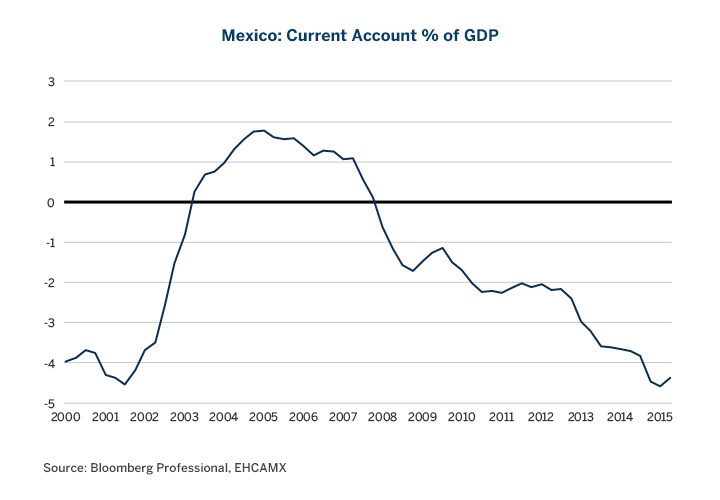

MXN has also been weakening against the USD but not to the same extent as the BRL (Figure 7). Moreover, Mexican interest rates are stuck at 3%, 11.15 percentage points below those in Brazil. Thus, the BRLMXN carry trade is nearly as attractive as BRLUSD. Additionally, Mexican short-term interest rates are about the same as Mexico’s rate of inflation (Figure 8), which might also bode poorly for the currency, which has recently weakened to a record low versus USD. Lastly, Mexico’s current account deficit is also about 4% of GDP (Figure 9), similar to Brazil’s. Trade deficits aren’t a problem if a country is attracting investment flows to boost future productivity and output. That doesn’t appear to be the case though in Latin America, where countries like Brazil and Mexico have been attracting speculative capital fleeing low-rate environments in the eurozone, Japan, the UK, and the US and, to a large extent, using that capital for unproductive purposes such as funding real estate speculation and consumer spending. That’s why higher US rates are a threat to both the Real and Peso, but not more so to one than the other –making for a potentially interesting relative value trade.

Figure 7: MXN has Fallen relative USD but Risen versus BRL.

{kind=link}

Figure 8: Mexico’s Short Term Rates are Below the Rate of Inflation.

{kind=link}

Figure 9: Like Brazil, Mexico’s Current Account Deficit is also Around 4% of GDP.

{kind=link}

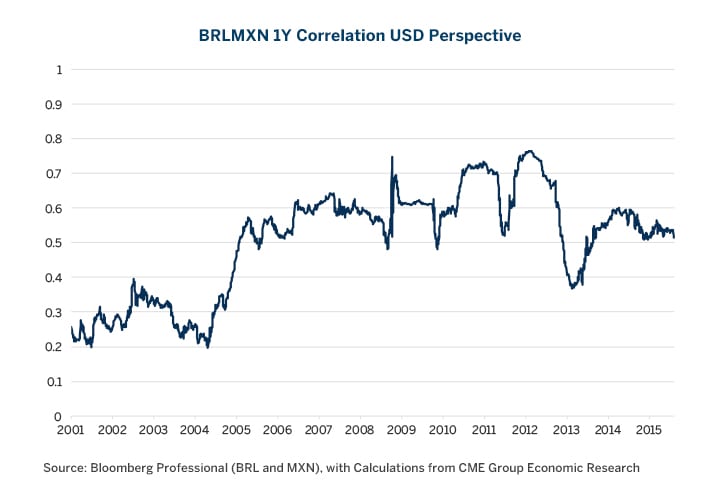

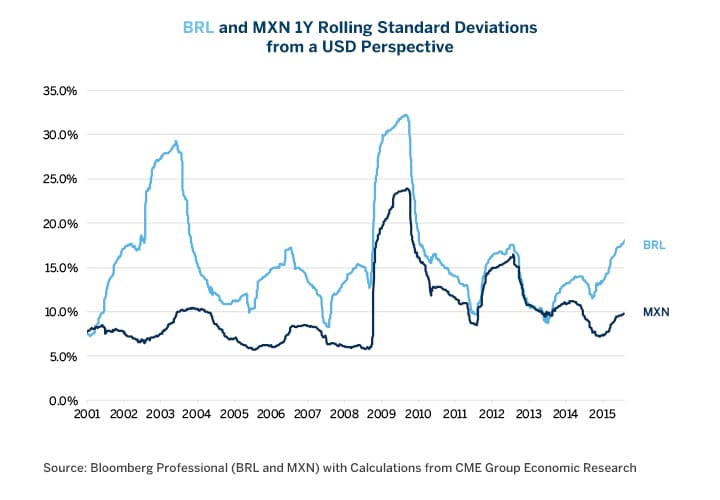

From a USD perspective, the BRL and MXN have had a +0.54 correlation (daily price changes) so far this year, making the Peso an interesting, if imperfect, hedge for the Real. 0.54 is close to the average correlation for the past ten years (Figure 10). It is also worth noting that BRL is often significantly more volatile than MXN versus USD measured over most periods (Figure 11).

Figure 10: Real and Peso Have Exhibited Between +0.35 and +0.75 1Y Rolling Correlation Since 2005.

{kind=link}

Figure 11: BRL has Almost Always Been More Volatile than MXN from a USD Perspective.

{kind=link}

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Recommended For You

View this article in PDF format.