{kind=link}

Fed's Fork in the Road: Even Higher Rates or Pause

As has been the case several times in the current tightening cycle, there is a large gap between what the Federal Reserve (Fed) suggests it is likely to do and what the market believes the Fed will accomplish. The Fed’s “dot plot,” a survey of Federal Open Market Committee (FOMC) members’ expectations for future policy, suggests that the Fed will likely hike twice more in 2018, three times in 2019 and two times in 2020. That’s seven more rate hikes before the Fed calls it quits. Moreover, unless long-term bond yields rise, seven more rate hikes would be enough to invert the curve and bring short-term interest rates to around 75 basis points (bps) over 30-year rates.

Market participants belong to a different school of thought than the Fed. While the forward curve agrees with the Fed that a September 2018 rate is very likely, as of 20 August, a December 2018 rate hike was priced with just a little less than a two-thirds probability. For 2019, the market prices one or two rather than three rate hikes and it does not price any further rises in 2020. Basically, the market view is about half of what the Fed’s dot plot suggests: three or four more 25bps rate hikes rather than seven.

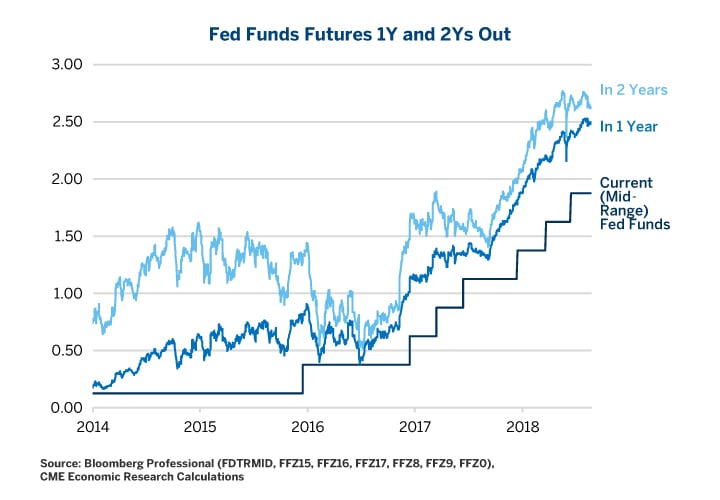

To be fair, this isn’t the first time that the market and the dot plot have diverged during the current tightening cycle and so far, when it has diverged, for the most part the Fed has come out on top. For example, investors spent most of 2016 doubting the Fed’s resolve to raise rates in 2017. They spent much of the summer of 2017 doubting that the Fed would tighten in 2018. The Fed tightened anyway (Figure 1).

Going forward, the challenge for the Fed is three fold:

- Determining what is neutral policy.

- Not moving past neutral policy and overtightening.

- Remembering lag time between monetary policy changes and the impact on the economy.

Neutral Policy

Part of the challenge in not raising rates too much is figuring out what neutral policy is. There seem to be three broad definitions based upon the dot plot, inflation and the yield curve. The closest that the Fed comes to telling us what it thinks neutral policy might be is once again in the Fed’s dot plot. Currently, FOMC members estimate that the longer term equilibrium for the Fed funds rates to be 2.875%. That’s close to the current level of yields (as of mid-August 2018) of both 10Y and 30Y U.S. Treasury yields. This suggests that unless there is a sell off at the long-end of the curve, that the “neutral” level for the Fed funds rate would bring the yield curve to flat. This is surprising given that flat yield curves often occur ahead of economic slowdowns and recessions. We note, though, that FOMC members may also be expecting the future to bring higher long-term Treasury yields, reflecting a higher inflation risk premium.

Figure 1: Not on Board, Investors Don’t Buy Fed’s Seven More Hikes in Two Years.

{kind=link}

Even 3% rates sound pretty low by historical standards. At the end of the 1980s expansion, the Fed funds rate was at 9.75%. At the end of the 1990s expansion, then Fed chair Alan Greenspan set it as 6.5%. In 2006, when Ben Bernanke took over, the policy rate was 5.25%. That said, the neutral policy rate has probably shifted lower over time for two major reasons: debt and subdued inflation.

Debt levels, public and private, grew from 125% of GDP in 1980 to 250% by 2008 and subsequently there has been no deleveraging, only some shifting of debt from the private to the public sector. As such, one reason why neither the Fed nor the bond market seems to think that rates can go beyond 3%, is that the only way in which the economy can maintain such a high debt burden is through very low rates. But given the high debt levels, is 3% Fed funds rate too much?

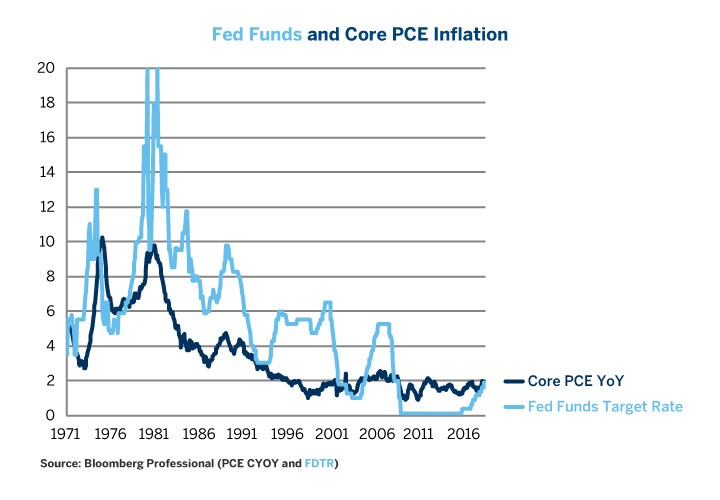

Another reason for ever lower peaks in the Fed funds rate is that inflation has been subdued for 25 years. Market participants are much more complacent about inflation, and do not require the high risk premium of the past. Considering inflation relative to short-term rates also provides another perspective on what constitutes neutral rates. When the Fed started hiking in 2015, one hypothesis was that it wanted to get policy back to neutral by raising Fed funds rate to the level of core inflation. The idea was that, if negative real rates (Fed funds rate below inflation) was accommodative, and if positive real rates (Fed funds rate above the rate of inflation) was tight, then the Fed funds rate at or close to the rate of inflation would be neutral. By some measures, the Fed has already met this definition of neutrality. Core inflation as measured by the personal consumer expenditures (PCE) index is at 1.9% YoY (Figure 2). The Fed funds rate currently averages 1.875%. Core CPI is at 2.4%. Two more rate hikes could put the Fed funds rate at that level before the end of the year. So, if bringing the Fed funds rate up to the rate of inflation is neutral then by that measure, we’re already there.

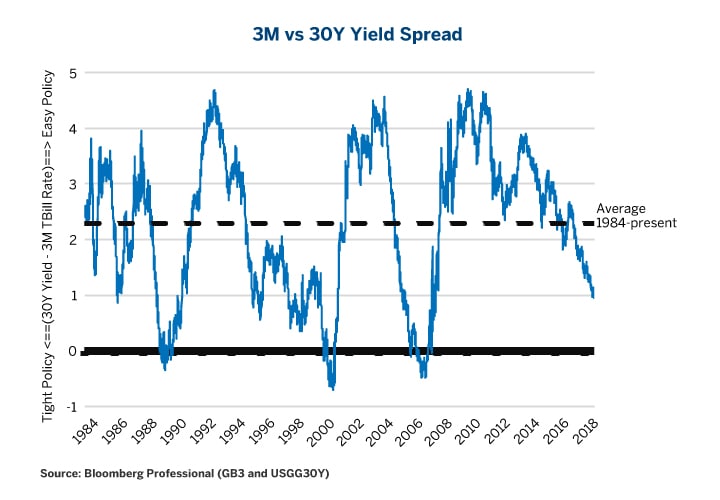

Finally, there is the yield curve measure. The yield curve provides no exact definition of what neutral policy is. Early yield curve theorists suggested that bond yields should bear a higher risk premium than short-term rates, arguing that time to maturity increases risk. Based on this view, a neutral yield curve would be modestly positively sloped. That said, the yield curve does have a long history. Between 1983 and the present– spanning 35 years and four business cycles—30-year U.S. Long Bond yields have averaged 230bps over three month T-Bill rates (Figure 3). By this measure, the current 100bps difference between 3M and 30Y is already tight. Viewed differently, 2 year–10 year spreads have averaged around 100bps since 1977. Currently, that spread is down to around 25bps. These yield curve measures suggest that the Fed has already moved past neutral and into “tight” territory.

Figure 2: Are We Already at Neutral?

{kind=link}

One could argue that years of quantitative easing, both in the U.S. and abroad, have distorted the yield curve as a measure of Fed policy tightness. Indeed, QE may have artificially flattened the yield curve. That said, the Fed’s QE ended almost four years ago and it has been actively shrinking its balance sheet for the past 12 months. Meanwhile, the European Central Bank (ECB) and the Bank of Japan (BoJ) have been scaling back the pace of their bond purchases. As such, whatever distortions exist in the yield curve are probably being unwound. Finally, it bears mentioning that whatever distortions QE might have created, the yield curve was steep from 2008 until recently and that a steep yield curve, despite QE, accurately presaged a long economic expansion.

Figure 3: 3M-30Y has Averaged 230bps for the Past Quarter Century.

{kind=link}

Moving Past Neutral

There are arguments for and against moving past neutral and deliberately slowing the economy. If the central bank believes that the economy risks overheating, the logical response is to tighten policy to engineer a soft landing. During the past four decades, the Fed successfully engineered two such soft landings: 1986 and 1995. In both cases the Fed managed to slow growth enough to prevent inflation from running out of control while at the same time not producing a recession. In both cases growth rebounded (1987-89 and 1996-2000) before recessions eventually began following further policy tightening (1990-91 and 2001).

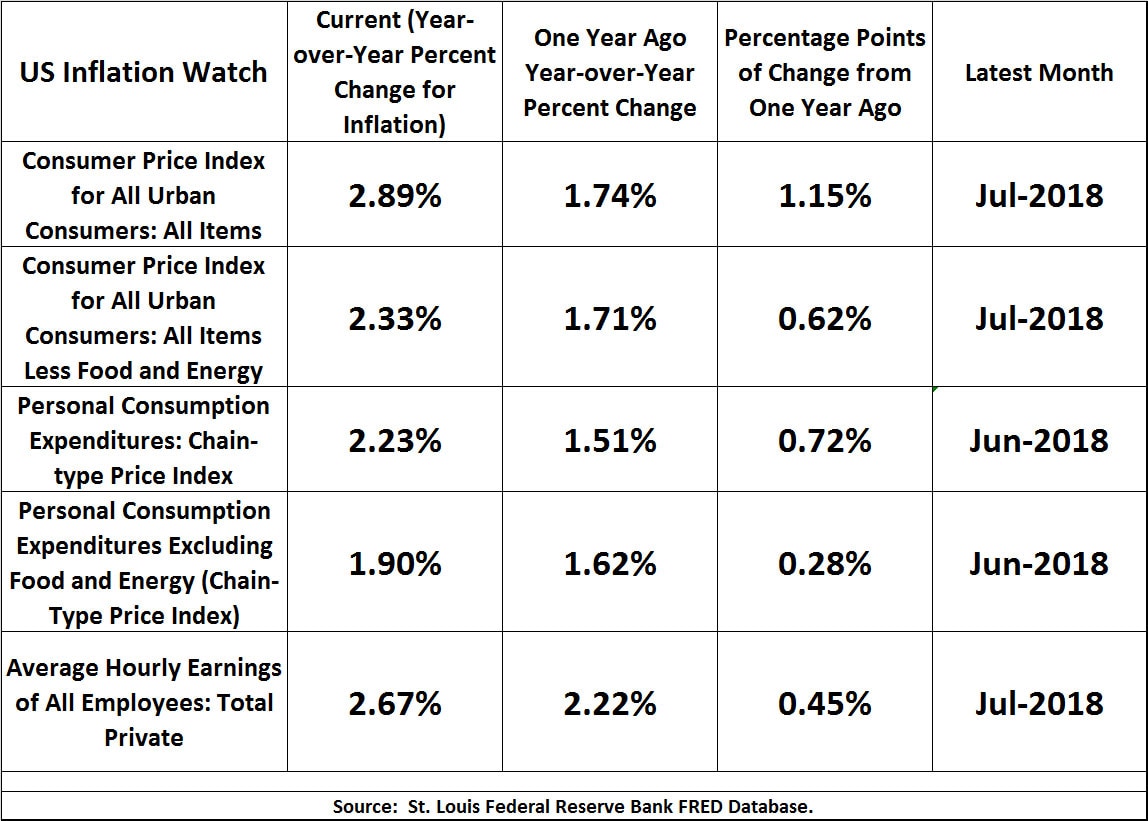

For the moment, there are few concrete signs of overheating. Core CPI has picked up a few tenths of one percent but remains well within its range of the past quarter century and well below levels from the 1970s and 1980s. Core PCE, a broader measure, often preferred by the Fed, is even less alarming. Wages are rising by 2.7% year on year, which is slower than at similar stages in past economic cycles, despite exceptionally low levels of unemployment. The gig economy might produce low unemployment rates but even nine years of economic expansion hasn’t yet produced much of an uptick in inflation.

That said, the Fed might be concerned that if the unemployment rate continues to decline, that it will eventually produce a surge in wages and inflation towards 3-4% per year, which might come as a shock to long-term bond markets. The Fed may see its current policy tightening as a means of preventing such an eventuality. Finally, the Fed may also be worried about asset bubbles and not just consumer price inflation. There is nothing in its mandate that explicitly mentions asset prices, but with the S&P 500® up 300% from its 2009 lows and NASDAQ up 600% over the same period, the Fed may be worried about asset prices getting too carried away. If so, it’s keeping it quiet.

Figure 4. Inflation has Already Moved Above the Fed’s 2% Target by Most Measures.

{kind=link}

Lag Times

So, if the Fed is already at or past neutral, why is the economy so strong? Part of the answer is the fiscal boost stemming from tax cuts and a surge in government spending. The Federal deficit has already grown from 2.2% of GDP in 2016 to around 4% in the 12 months ending in June. It will likely continue to expand towards 6% over the next two years. Fiscal expansion helped to boost first-half 2018 real GDP growth, even if the stimulus is unlikely to last.

In addition to fiscal stimulus, there is one other key reason why the economy remains strong: most of the rate hikes are too recent to have had much impact. Typically, it takes six months to two years (so about 15 months on average) for monetary policy to bear fruit. As such, there is no reason to expect that the Fed’s one rate hike in 2015 or one rate hike in 2016, both of which left policy rates well below the rate of inflation and yield curves extremely steep, would be having much impact. The same can be said of the first two rate hikes in 2017. The most recent policy tightening won’t likely be felt until 2019 or even 2020. As such, the great risk is that the Powell Fed, seeing a continuation of strong incoming data, keeps raising rates, ignoring a potentially substantial slowdown that could result from the cumulative impact of the rate hikes that it has undertaken during the lag period –the period after the rate hikes but before the economy shows a response to tighter policy.

Of course, Fed officials know about lag times and they even mention them occasionally in their public statements. Our advice: treat these statements like a silent movie. Don’t listen to what the Fed says about lag times. Instead, watch what they do and what the “dot plot” suggests they plan to do.

A Fork in the Road – Take It.

The Fed is coming to a fork in the road. It has moved its policy rates up to the rate of inflation. By some measures, it’s around neutral policy already – or perhaps even past it. The Fed’s dot plot suggests a continuation of the current trajectory of tightening but, beyond an eighth rate hike in September, markets aren’t on board. Market participants seem to think that the Fed will take a much slower approach to tightening policy after September. If they have this one right, the Fed might succeed in engineering a soft landing like it pulled off in 1986 and 1995. In that scenario, the economy will likely slow in 2019 or 2020 without the economy experiencing a significant rise in unemployment or a downturn in output. It can then perhaps enjoy a prolonged economic expansion into the early to mid-2020s.

One argument in favor of the Fed pausing is that it is aware of the dangers of inverting the yield curve and may stop short of putting short-term policy rates too close to or above the levels of long-term yields. That said, the yield curve isn’t a light switch. It’s not either on or off. It’s more like a dimmer switch. A rather flat but not quite flat or inverted curve might signal problems ahead anyway. The question really should be, how flat will the Fed allow the yield curve to become and how long will it allow the yield curve to stay there?

If, on the other hand, the Fed, myopically focuses on strong incoming data, forgets about the lag time between its policy actions and their eventual impact upon growth and follows its dot plot towards dramatically higher rates, the risks of a recession around 2020 or 2021 will grow immensely. If the Fed keeps tightening at anything like its current pace, not only is a recession probable but also a sharp rise in market volatility and a dramatic widening of credit spreads as we move into the new decade. As such, at the September FOMC meeting, watch closely for any signs that the Fed might be backing off their intention to tighten policy towards 3% by the end of the decade. The dot plot and other public statements are ultimately more interesting than the Fed’s September policy move, which barring some unforeseen catastrophe, seems to be baked into the cake.

Outlook

Go on Hold in 2019? Our base case scenario is that the Fed is very close to going into a holding pattern. The argument that the Fed might raise rates twice more and then go on hold rests on several assumptions. First, the Fed appears very aware of the rise in both public and private debt to record levels. Rising rates increase the cost of servicing debt and raise the risks of recession. Second, and related, the yield curve has flattened considerably over the past 12 months. By our analysis the yield curve already indicates that the Fed has achieved a “neutral” interest rate policy, meaning that more tightening which might completely flatten or even invert the yield curve and could be the trigger for a 2020 recession. Third, so far, the U.S.-driven trade war is not impacting the U.S. economy very much, but global growth does appear to be slowing and many emerging markets are feeling the pressure. A global slowdown would decelerate U.S. growth, even if it does not cause a recession. Our analysis disagrees with the futures market consensus, as we put a 60% probability on just two more rate rises before the Fed goes on hold.

Looking to 2020, recession risk is at 33% and rising. The current U.S. economic expansion will soon be the longest on record. We do not think economic expansions end because of old age – it takes a domestic policy mistake or a serious external disruption. As indicated above, with rapidly rising debt loads, a nearly flat yield curve, escalating trade wars and disruptions in emerging market currencies and economies, there is no shortage of factors which might serve as a catalyst for ending the current expansion. By our analysis, the probability of a recession in 2020 appears to have risen to 33%. As we move into 2019, if it appears that our base case scenario for the Fed is wrong, and the Fed keeps on raising rates, then we will be adjusting our probability for a 2020 recession even higher.

Finally, we note that a 33% probability of a recession also means there is a 33% probability of a rate cut by the Fed, should a recession occur. And, please appreciate that when the Fed cuts rates, it does not necessarily do so in 25 bps increments or even at a regularly scheduled FOMC meeting. Remember, since former Fed Chair Alan Greenspan’s aggressive tightening in 1994 was widely viewed as a mistake, rates have only gone up in well-defined 25 bps increments. On the way down, though, rates can be cut quickly and sharply once recession-like data starts showing up in the employment situation report or we see credit market spreads widening dramatically and indicating severe financial pain.

Hedging Fed Rate Hikes

The Fed has indicated that it would raise rates two more times this year, and another five times through 2020. But there is some skepticism in the market because of the high debt load that could become difficult to service if rates are increased as many times as signaled by the Fed's "dot plot." Protect your investment portfolio from the uncertainty with futures and options on Interest Rate products