{kind=link}

Chinese Yuan: Beware of Boundaries

Boundaries impact market behavior, whether they are explicit or embedded. For the Chinese yuan (CNY), the psychological boundary is 7.0 to the U.S. dollar (USD). Market participants need to pay attention to the economics of boundary-value dynamics. As trade tensions escalate, volatility may be dampened near the boundary even as risks rise for a sharp currency devaluation. Alternatively, if trade tensions ease, there can be an orderly drift toward appreciation.

FX Politics of the Ebb and Flow of Trade Tensions

The Chinese yuan, or renminbi, is very sensitive to developments in the trade war. When tensions ease, as they did at the end of 2018 and early 2019, the Chinese currency tends to appreciate against the USD. When tensions escalate, like in May 2019 as prospects for a trade deal evaporated, the Chinese currency depreciates. Interestingly, there are both psychological and hidden policy agenda limits as to how far the currency might depreciate, with huge implications for market behavior.

In this intense trade war environment, when the Chinese felt a deal was possible they have been willing to allow market pressures to appreciate their currency toward 6.7 yuan per dollar, as market participants expressed expectations that a deal might allow for U.S. tariffs to be removed. A stronger currency makes Chinese exports cost more and this comes on top of the U.S.-imposed tariffs, so currency appreciation only occurs when it looks like a deal can happen and the tariffs might go away. And, if tariffs were to go away, equities might well take off to the upside.

Our related content:

- Trade War: The Perils of Escalation

- Trade War: Lose-Lose Outcome?

- Looking at China’s Growth Past the Trade War

Chinese Yuan Appreciates Against U.S. Dollar When Tensions Ease, and Vice Versa

{kind=link}

The Magic of Seven

By contrast, when the U.S. ratchets up pressure on China and prospects for a deal fall apart, market participants tend to take the view that the U.S.-imposed tariffs will be permanent. Expectations of permanent tariffs contributes to depreciation pressure on the yuan.

What has become apparent from the data is that when the trade war escalates, the Chinese currency heads toward 7 per USD and then takes a pause. Is CNY 7 per USD a ceiling? Yes, the ceiling may well exist because the Chinese authorities do not want their currency to depreciate so much that it would make already bad trade relations worse. The Chinese authorities may well want to hold the line at CNY 7 per USD until the economic pain outweighs the risks of further angering the US. The reasoning here is that a further depreciation of the Chinese yuan works to make Chinese exports cheaper and offsets the tariffs. The decision to allow depreciation past CNY 7 per USD would not be taken lightly or easily, so it is not a base case scenario. Further depreciation is a risk that rises when the pain from the trade war on the Chinese economy intensifies and prospects of rapprochement with the US seem distant.

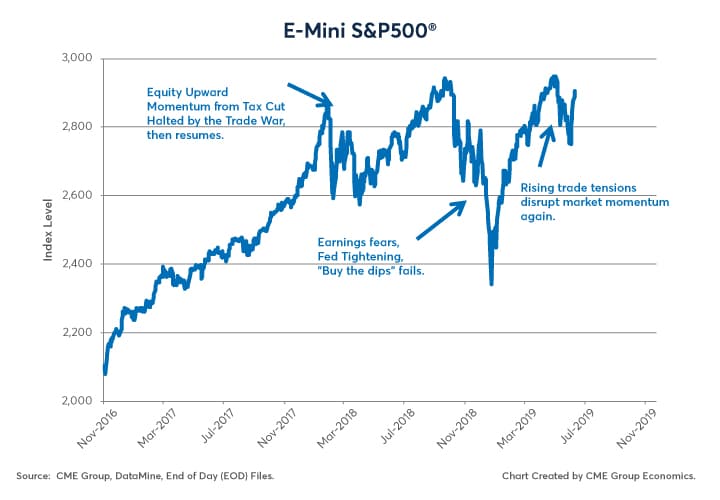

Trade War Has Disrupted Market Momentum

{kind=link}

Boundary-Value Economics

Boundary-value economics is fascinating. “Goodhart’s Law,” which is the economic version of the Heisenberg's Uncertainty Principal, applies here. According to the late Professor Goodhart, when a central bank targets a metric, market participants change their behavior toward the metric, and the time line and volatility pattern of the metric changes.

When applied to the apparent boundary or ceiling at CNY 7 per U.S. dollar, we have two observations based on Goodhart’s law. First, if the ceiling is ever breached, the currency may well move fast and far above the old ceiling. It is like pressure building up and then being quickly released – a very explosive behavior pattern. Second, while the pressure is building even though the ceiling has not been breached, observed market volatility is extremely low even while future risks are rising rapidly. The message is clear. Be especially aware of the risk management complexities when boundaries are present.

Emerging Market FX

CME FX delivers greater certainty for trading emerging market currencies such as the Renminbi, Rupee, Won, Peso, Real, Rand and Ruble in every market condition.

{kind=link}

https://www.cmegroup.com/insights/trade-war.html?itm_source=trade_war_developments_article_page&itm_medium=cmegroup&itm_campaign=economic_research_trade_war&itm_content=right_rail_banner