{kind=link}

China, Brazil and the Soybean Crush

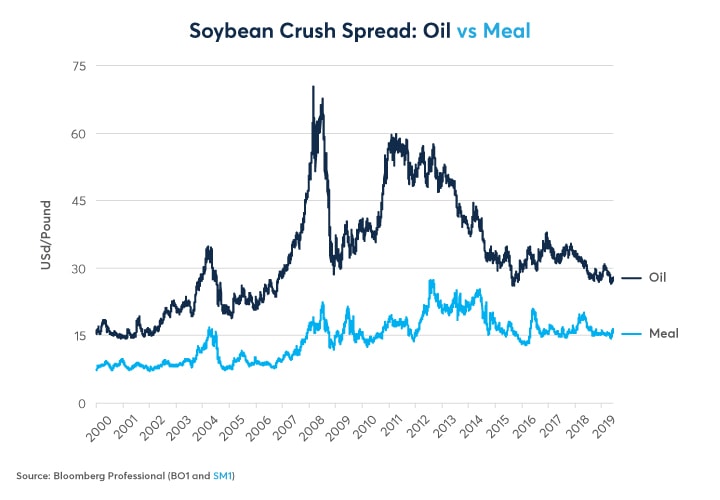

Soybeans have two main uses: oil, which is mainly used for cooking, and meal, which is primarily used as animal feed. Of the two, soy oil worth a lot more on a pound for pound basis. Over the past 20 years soy oil prices have averaged 2.35x as much per pound as much as soy meal but the spread is far from constant, varying from a low of 1.4x to a high of 3.1x (Figure 1).

Figure 1: Soybean Oil Averages 2.3x the Price of Soybean Meal Per Pound.

{kind=link}

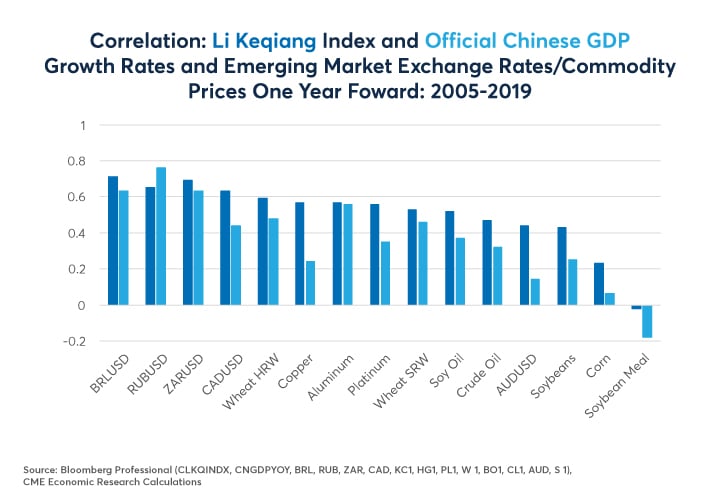

Not only do soy oil and soy meal have very different uses and prices, one is strongly influenced by economic developments in places like China and Brazil while the other is not. Chinese growth appears to exert a strong influence on the price of soybean oil but a much weaker and even counterintuitive influence on the price of soybean meal. Notice how soy oil prices are among the most highly correlated with the Li Keqiang Index, a narrow measure of Chinese economic growth that focuses on electrical consumption, rail freight volumes and the number of bank loans. By contrast, soy meal prices have been negatively correlated with changes in the Li Keqiang proxy of Chinese economic growth (Figure 2). In other words, stronger Chinese growth typically sends soy oil prices higher over the next 12 months whereas stronger Chinese growth might send soy meal prices lower.

Figure 2: Stronger growth is China is typically good for Brazilian real and soy oil but not for soy meal

{kind=link}

So why is that? Why would stronger Chinese growth potentially send soy oil prices soaring while soy meal prices might fall under the same circumstance? The answer lies in the relative price of the two commodities and in their different end uses. First, since soy oil typically trades at more than 2x the price of soy meal, much of the value of the soybean is as an oilseed rather than as a source of protein. When China grows more quickly, it tends to send the price of energy and industrial metals higher and often creates a boom in emerging markets that export raw materials to China. One of the first things that people do as they become better off is to consume more vegetable oil. Moreover, as crude oil prices surge, it tends to raise the price of biodiesel, sending ethanol and vegetable oil prices higher as well. In fact, these markets often do a good job of forecasting future returns in the crude oil market itself, a topic that we have written extensively.

If soybean oil prices surge, that often pulls the price of soybeans higher as well, although not the same extent. Nevertheless, higher soybean prices impact planting decisions and have the potential to increase the global output of soybeans in one year’s time. So therefore, a higher price for soy oil can translate into a greater production of soybeans in general which, in turn, can boost the supply of both highly valued soybean oil and generally less expensive soybean meal.

Increased supply isn’t great news for soybean meal prices. Just because China grows more quickly doesn’t mean that our livestock will eat more soybean meal – at least not in the short-term. As such, the increased supply of soybean meal typically acts as a mild depressant on soybean meal prices.

If China slows, this sends the whole process into reverse. Slower growth in China typically means inadequate demand growth for industrial metals and energy which, in turn, means slower growth in emerging markets and less growth in demand for vegetable oils and biodiesel. This tends to depress soybean prices and may negatively impact planting decisions, which constricts growth in both soybean oil and soybean meal supply, potentially putting a bid in the latter since its demand growth as a food and as animal feed tends to be less connected to global economic growth.

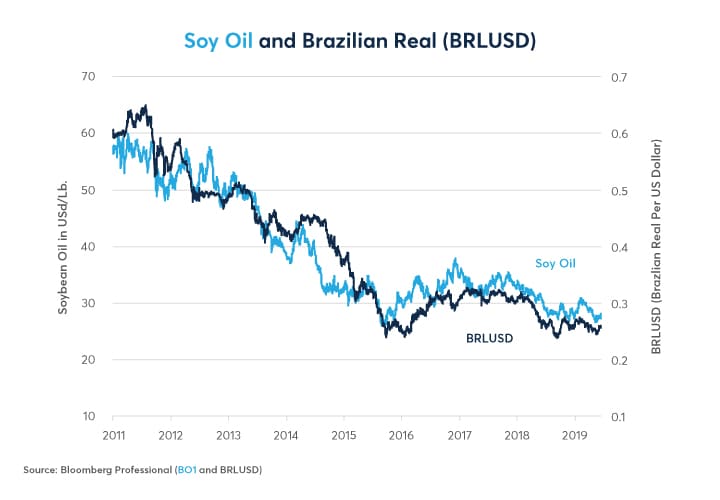

Also notice how closely related soybean oil prices are to the fate of the Brazilian real (Figure 3). Brazil is now the primary exporter of soybeans and what happens to the Brazilian real goes a long way towards determining the global cost of production, which acts as a sort of soft floor on the U.S. dollar price of soybeans. As we observe in Figure 2, the Brazilian real is also extremely strongly influenced by the Li Keqiang measure of growth in China. In addition to exporting a great deal of agricultural goods to China, Brazil is also the second largest exporter of iron ore to China.

Figure 3: Soy Oil Moves In Lockstep with the Brazilian Real.

{kind=link}

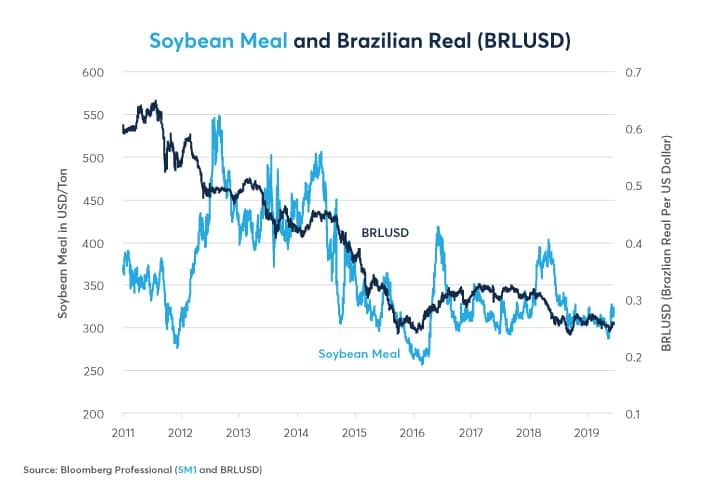

By contrast, soy meal prices tend to show a great deal more variance with respect to the Brazilian real than soy oil. To be sure, the real still exerts an influence but that influence is much weaker than it is for soy oil (Figure 4).

Figure 4: Soy Meal’s Relationship With the Real is Much Looser.

{kind=link}

As such, if the trade war results in a significant slowdown in China, that could result in lower prices for energy, metals, emerging market currencies and vegetable oil prices but, conversely, it might turn out to be slight positive for soybean meal, especially if farmers plant fewer soybeans as a result of the drop in soy oil prices. On the other hand, if China succeeds in offsetting the negative impact of the trade war through easier monetary and fiscal policies, that could keep energy, metals EM currencies and soybean oil prices supported but might not do much to help soybean meal.

Bottom Line

- Chinese growth exerts a strong, positive correlation to soy oil.

- Chinese growth has a weaker and even inverse relationship with soy meal prices.

- Soy oil is typically about 2-2.5x more expensive than soy meal per pound.

- Soy oil has a stronger influence on planting decisions than less valuable soy meal.

- Soy oil moves in lockstep with the Brazilian real.

- Soy meal has a much weaker relationship with Brazilian growth.

Livestock Futures and Options

Feed costs can account for a significant portion of a livestock operation's budget and uncertainty in prices can be an added challenge. Manage the risk inherent in livestock production and processing with CME Group Livestock products including Live Cattle, Feeder Cattle, and Lean Hogs.