{kind=link}

Brexit Endgame: Interest Rate Scenarios

Brexit is about to head into its most critical phase with a series of parliamentary votes beginning before next week. The most important of these will likely be the vote on Prime Minister Theresa May’s Brexit agreement with the European Union (EU). It looks as though support for the agreement is gaining momentum but it’s passage in parliament is not yet a done deal. Should the agreement fail, there will likely be a vote to either extend the negotiating period or to leave the EU with no deal. Leaving the EU with no deal is unlikely as a majority of parliament opposes it. Oddsmakers give “no deal” a 15% probability, at most. Meanwhile, opposition parties including Labour, the Scottish National Party and the Liberal Democrats, support a second referendum to give the British people a final say on any deal. To say the least, March 12 will set off an interesting and determinative series of votes that will have wide ranging consequences for Britain’s future as well as the evolution of the economy and interest rates.

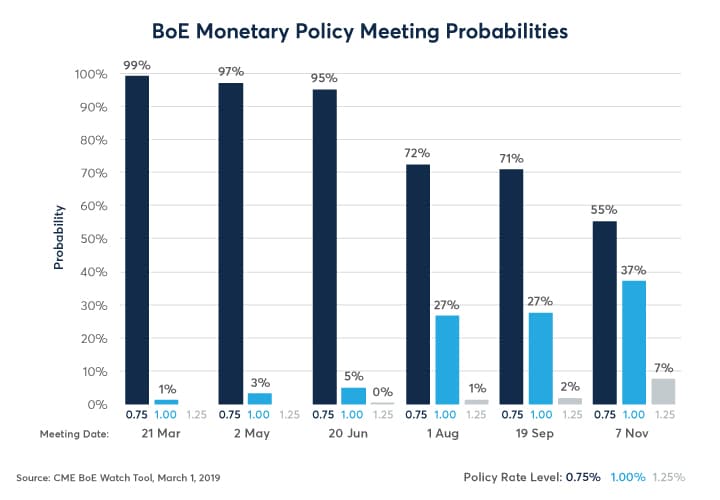

Going into this critical week, UK interest rate futures price little in the way of monetary policy change by the Bank of England’s (BoE) Monetary Policy Committee (MPC). Using data presented on CME’s BoEWatch tool, SONIA (Sterling Overnight Index Average) futures price a low probability of rate changes at the meetings on March 21, May 2 or June 20. For the August 1 and September 19 MPC meetings, the likelihood of a rate hike is slightly less than one third. By the November 7 meeting, the probability that the BoE will have hiked rates approaches 50% (Figure 1).

The problem with these rate expectations is that they reflect contradictory scenarios, some of which are likely to be eliminated before the Ides of March. On the one hand, SONIA traders must grapple with the possibility that the BoE will cut rates in the event of a no-deal Brexit. On the other hand, the futures market must also price the likelihood that the BoE will lift rates further and faster than the market currently prices if a deal is approved, lifting the cloud of uncertainty that has been hanging over the UK economy and financial markets. As such, interest rate probabilities are likely to change significantly during and immediately after the parliamentary votes.

With unemployment a 4.0%, it’s easy to imagine the BoE hiking rates by 25 basis points (bps) in short order if Parliament agrees to the deal. With inflation falling below 2%, the BoE might remain on hold through the end of June but, assuming that the economic data holds up, they could easily hike in August. This would imply a significant steepening of the SONIA curve. If Parliament passes a deal, that would also imply a stronger pound, which would be disinflationary and would limit any upside move in rates to probably one or at most two rate hikes this year. That said, even just one rate hike in 2019 is significantly more than what the market currently prices.

If Theresa May’s deal fails again, all bets are off. However improbable, a no-deal Brexit would imply an almost immediate rate cut to 0.50%, with the possibility of further reductions to 0.25% or even lower. A more likely scenario is that the negotiating period is extended. An extension implies a fairly status quo scenario for the SONIA curve as the current uncertainties would remain until the new deadline, at which time UK markets would face another cliffhanger. Delaying Brexit would require the consent of all 27 EU members and would likely come with strings attached and could also result in UK voters being asked to vote, once again, in EU Parliamentary elections even as their government continues to negotiate its departure. Finally, a second referendum would also keep the uncertainty in place and result in another binary outcome – although what kind of binary outcome it would be is unknowable until we get the exact wording of the question in such a referendum. In the runup to a hypothetical second referendum, the BoE and interest rate markets would still likely be in a state of paralysis.

In any case, UK interest rate markets are likely to have a great deal to chew on, especially during the week of March 11. The CME BoEWatch tool provides a venue for watching how the probabilities for future rate decisions are changing in real time in response to decisions being made in Westminster.

Figure 1: Interest Rate Probabilities for the Next Six MPC Meetings as of March 1.

{kind=link}

Bottom Line

- The week of March 11 will likely see a series of determinative Brexit votes.

- These votes will eliminate certain interest rate scenarios and endorse others.

- Watch for a great deal of movement in MPC meeting probabilities as Parliament votes.

- If May’s deal passes, a stronger currency could buffer expectations of an interest rate rise.

British Pound

A series of Brexit votes over the next week in the British parliament could have wide-ranging consequences for the economy, interest rates and the British pound depending on whether the votes favor a deal with the European Union, the UK crashing out of the bloc or a possible second referendum. Hedge your portfolio with futures and options.