{kind=link}

Australian Wheat Sways With the Ruble, USD and Renminbi

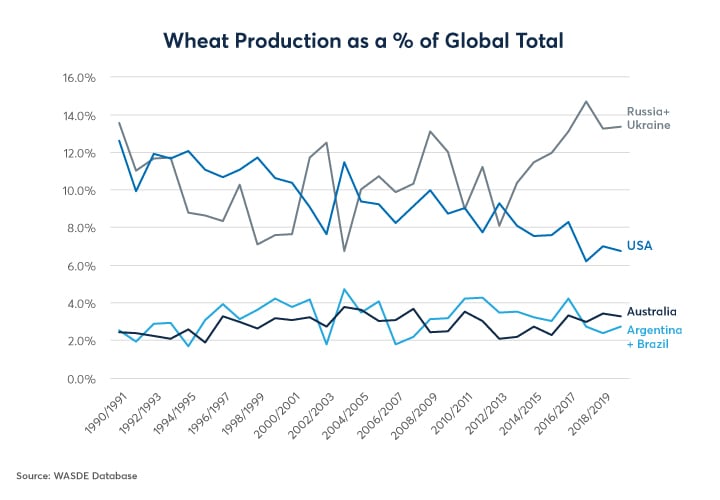

Like their US and South American counterparts, Australian wheat farmers are increasingly at the mercy of economic events in places such as China and Russia. While Australia is undeniably an important wheat producer (around 3% of global total) and exporter (about 1.9% of global production), it’s role now pales in comparison to the rising dominance of the Black Sea region (Figures 1 and 2). The global cost of wheat production is heavily influenced by events in the Black Sea area, and the Russian ruble.

Figure 1: Black Sea Production Now Dominates.

{kind=link}

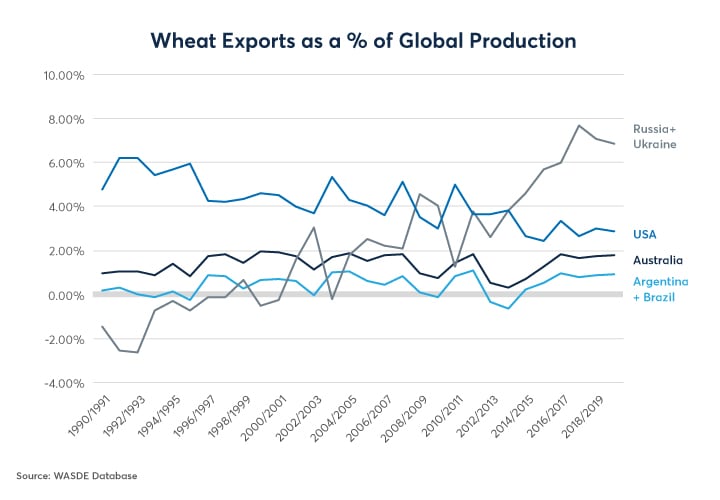

Figure 2: Black Sea Region Wheat Exports Outpace Other Producing Regions.

{kind=link}

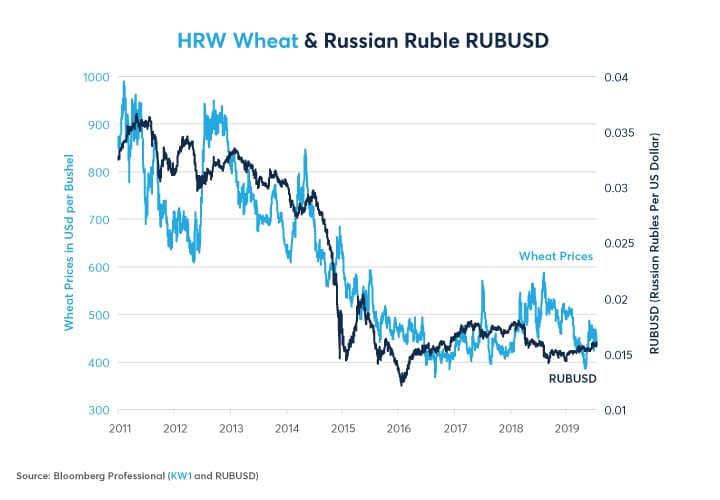

Given the dominance of the Black Sea region’s production, it comes as little surprise that wheat prices in U.S. dollars (USD) broadly sway with the ups and downs of the Russian ruble (RUBUSD). Since Russia and neighboring Ukraine are by far the world’s biggest wheat exporters, changes in the value of their currencies go a long way towards changing the marginal cost of production for wheat (Figure 3), corn and other commodities.

Check out our article on the Australian economy:

Can Australia’s 28-Year Record-Setting Expansion Keep Going?

Figure 3: The Ruble Helps to Determine Wheat’s Global Cost of Production.

{kind=link}

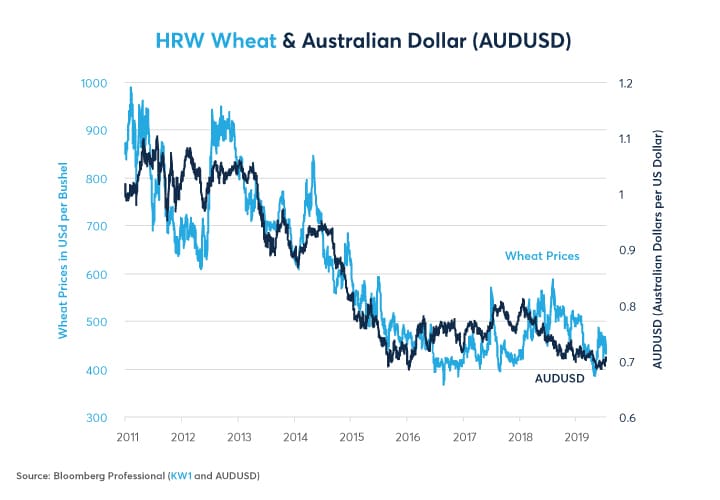

Australian wheat farmers can find some solace in the fact that the Australian currency partially buffers them from movements in wheat prices. Figure 4 shows a significant degree of co-movement: when wheat prices fall, the Australian Dollar (AUD) tends to weaken and vice versa. As such, locally denominated costs for Australian farmers such as wages, salaries and property taxes tend to move in the same direction as the global price of wheat. What is harder to discern from Figure 4, however, is the degree of relative volatility with the AUD’s actual volatility magnified by the choice of scale.

Figure 4: The Australian Dollar Absorbs Some of the Australian Wheat Farmers’ Price Risk.

{kind=link}

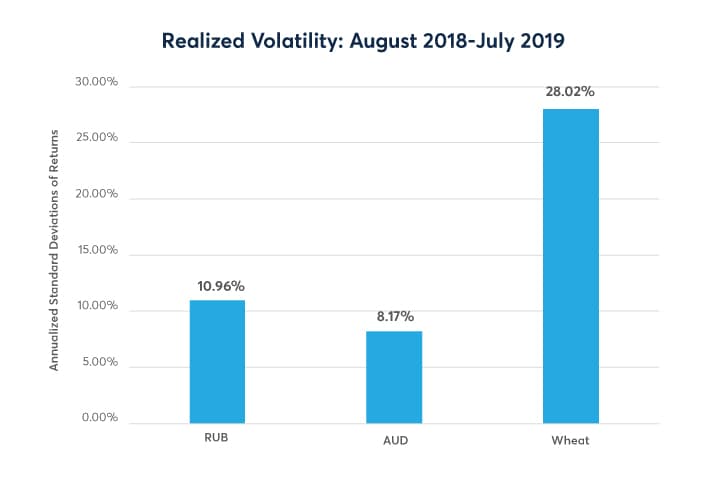

Wheat prices are about 3.5x as volatile as the AUDUSD (Figure 5). As such, the co-movement of the AUDUSD with wheat prices absorbs less than 30% of the risk from the movement in wheat prices. Moreover, it’s not helpful in buffering any global costs of wheat production such as the price of fuel, pesticide, fertilizer, farm equipment and other products. As such, if one assumes that roughly half of the cost of farming is locally determined and the other half determined globally, the co-movement of AUDUSD with the price of wheat probably absorbs only about 15% of an Australian farmer’s overall price risk. This implies that hedging can still be useful.

Figure 5: Wheat Prices Are 3.5x as Volatile as the AUDUSD Exchange Rate.

{kind=link}

Despite their differences in volatility, AUDUSD, RUBUSD and wheat prices all share a common denominator: they respond strongly to economic conditions in China. When China’s growth picks up, it tends to send the price of energy and industrial metals higher, which, in turn, strengthens the currencies of major resource exporters such as Russia, Brazil and Australia. Stronger commodity exporting currencies increase the marginal cost of production for wheat, corn, soy oil and other agricultural commodities. The opposite happens when China slows: weaker growth reduces demand for energy and metals, typically lowers the value of commodity-exporting currencies and thereby lowers the marginal cost of production for key agricultural products, including wheat.

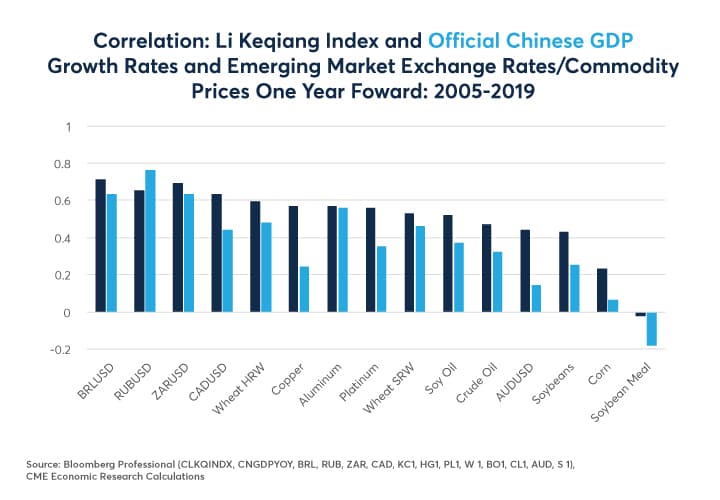

There are several ways to measure Chinese growth. While the official gross domestic product is the most widely observed yardstick of China’s economic progress, alternative measures like the “Li Keqiang Index” correlate strongly with subsequent, one-year-ahead movements in exchange rates and commodity price levels (Figure 6). The Li Keqiang measure is especially useful because it targets the performance of China’s industrial economy by focusing on electricity consumption, rail freight volumes and the amount of bank loans. The industrial economy, much more so than the services sector, influences global demand for energy and industrial metals and by extension commodity-exporting currencies and agricultural production costs.

Our articles on the Li Keqiang Index:

Figure 6: RUBUSD, Wheat Prices and AUDUSD Respond to Fluctuations in Chinese Growth.

{kind=link}

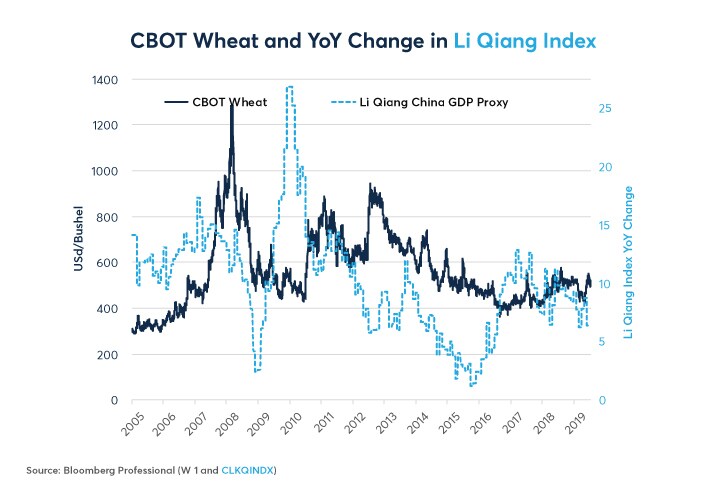

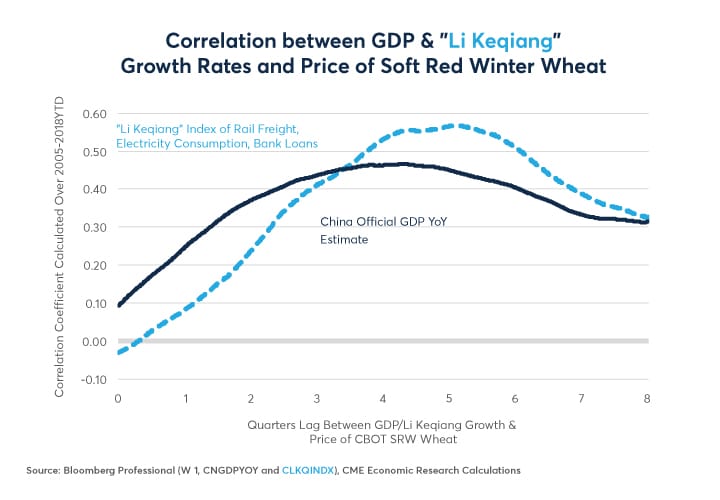

While official Chinese GDP has shown a high degree of stability for the past seven years, owing in large part to the increased role of services and domestic consumption in the economy and a reduced reliance on exports, the Li Keqiang index shows a much greater variance of economic growth, with a much steeper slowdown from 2011-2016 and a much sharper rebound in 2016-17, followed by some further slowing since (Figure 7). Wheat prices tend to follow these movements with a lag of about a year (Figures 8 and 9).

Figure 7: The Li Keqiang Index Shows a Wide Variance of Industrial Growth Rates in China.

{kind=link}

Figure 8: Wheat Prices Often Respond to Chinese Growth Rates With a Delay of About One Year.

{kind=link}

Figure 9: Chinese Growth-Wheat Correlation Peak Out After About 4-6 Quarters.

{kind=link}

Macroeconomic Outlook for Wheat

Australian wheat farmers can take some comfort from the robust fiscal conditions in Russia. The Kremlin runs a budget surplus of 2-3% of GDP and has extremely low levels of debt. It’s fiscal health could make the ruble a relatively strong currency among emerging markets to the likely benefit of wheat farmers in the US, Australia and elsewhere. That said, Russia is still extremely reliant on commodity exports, and China’s economy still plays an outsized role. China’s GDP is 5x India’s, 6x Brazil’s and 7x Russia’s. It consumes 40-50% of most industrial metals and 67% of iron ore, one of Australia’s two biggest exports along with coal. In short, no other country or group of countries can easily replace China’s demand should it falter.

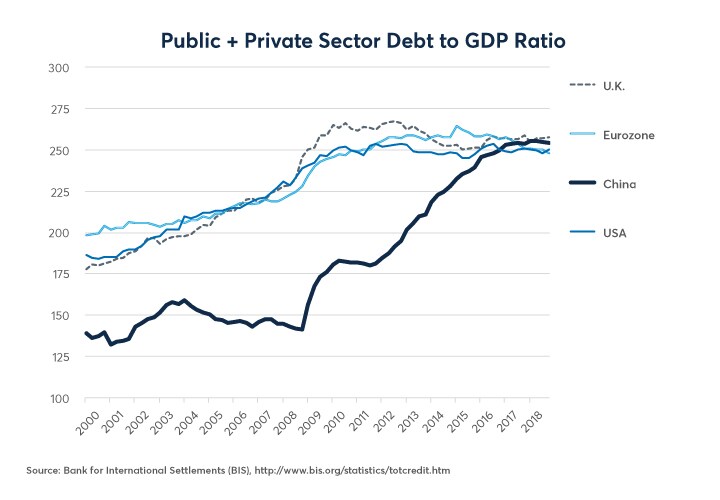

While China’s economy has held up well under the trade war – China’s stimulus measures have largely offset the negative impact of higher US tariffs – the country during the 2020s must confront several structural issues, including a decline of 5% in the working age population by 2030, a slowing of productivity gains from the rural-urban transition and extremely high levels of debt (Figure 10). These factors could contribute to a significant slowing of the Chinese economy in the 2020s irrespective of the outcome of the trade war.

Figure 10: Chinese Debt & Demographics Could be a Negative for Australian Wheat in the 2020s.

{kind=link}

What happens in Washington also matters, especially since the USD is the other side of the AUDUSD exchange rate. For the past eight years, USD has been a strong currency, rallying against AUD and most other currencies since 2011. A weaker AUD has helped Australian farmers to maintain competitiveness despite the decline in USD prices for wheat. Expanding US budget and trade deficits could cause USD to weaken. If so, that could put the USD price of wheat under upward pressure, perhaps counteracting some of the negative impact from any slowing in China.

What happens to the AUD price of wheat depends on whether AUD benefits from the USD’s weakness. It seems likely that the main beneficiaries of USD weakness would be low-interest-rate currencies whose central banks will have a difficult time easing further, such as the euro, pound, Swiss franc and yen. Given Australia’s reliance on China to buy its exports and the particular vulnerability of Australia’s two main exports (coal and iron ore), Australia’s wheat farmers might survive a bout of USD weakness so long as AUD doesn’t strengthen significantly.

Bottom Line

- Global wheat prices are increasingly determined by Black Sea production.

- China exerts a strong, indirect influence on wheat prices via energy, metals and foreign exchange rates.

- Australian currency movements buffer only a small amount of wheat’s volatility.

- China’s economy may slow down as a result of high debt and demographics.

- Any Chinese slowing could weaken AUD as well as wheat and other commodity prices.

Wheat futures

Our Australian Wheat FOB (Platts) futures will allow you to gain or reduce price exposure to Australian wheat exports. The contract is based on the Platts APW Wheat FOB Australia assessment, a daily price assessment of the spot physical price for Australian Premium White (APW) wheat.