{kind=link}

Aluminum: In Search of an Asian Trading Hub

Base Metals in a Global Supply Glut

China and euro zone economic woes have been headline news recently. In the United States, attention has been focused on interest rates. Should the Federal Reserve raise U.S. interest rates this year, the expected appreciation of the U.S. dollar (USD) could lead to a rise in the cost of commodity imports for the construction and manufacturing industries in China.

China’s objective is to have greater influence on global metals prices...as such, this might be a conducive time for China to participate in the global aluminum derivatives market.

The Chinese economy is maturing, and investments are gradually shifting away from fixed asset industries towards the service sector. Sentiment across all commodity markets has been weak, particularly for

base metals.

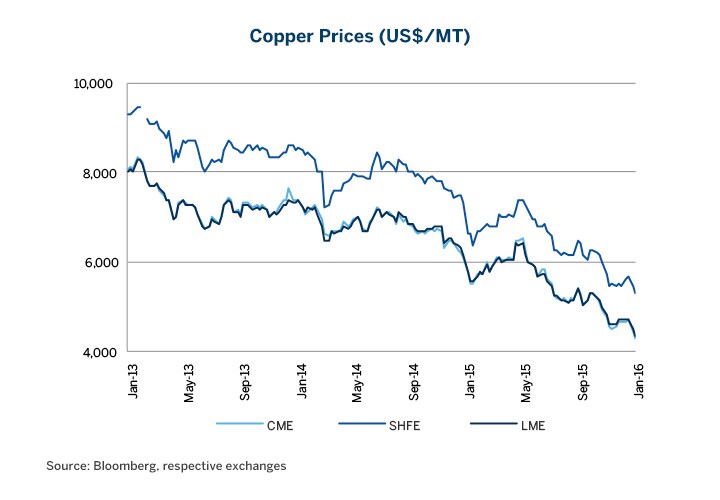

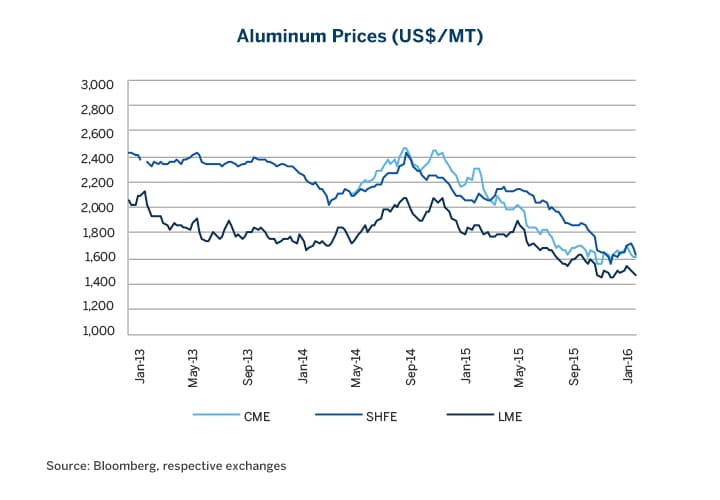

Base Metals Prices Slide

Copper prices have been on a downtrend since 2013. Aluminum held out until November 2014, but has since also been on a continuous decline. Since the early 1990s, metals consumption in China had grown by 14% annually, while demand in the rest of the world grew at a meagre 0.4% -- due, in part, to the offshoring of manufacturing operations to China. The offshoring mode has largely run its course. As new supply comes on, it will outstrip demand and this could force higher-cost manufacturing firms to close down.

Hard for Physical Players to Exit Market

Despite the supply glut, there is no easy way out of the sector for some. On the one hand, the Chinese government is under pressure to maintain domestic employment in these industries. On the other, Chinese traders are stuck with Take-or-Pay (ToP) contracts, and the surviving firms have to maintain production even if it means having to take losses on their exports.

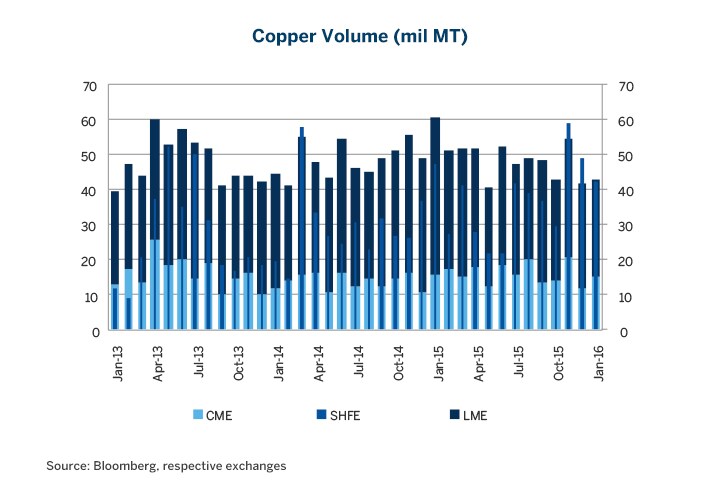

Base Metals Volatility Up

As for traders, the heightened volatility has enabled metals derivatives volumes to remain vibrant. At CME Group, the average daily volume (ADV) of its copper futures, at 67,000 lots/day, grew by 16% in 2015 versus 2014. The ADV for CME’s suite of aluminum contracts grew by 300%.1

Even on the Shanghai Futures Exchange (SHFE) in China, its copper and aluminum futures volumes grew by 125% and 164%, respectively, from 2014 to 2015.2

Anecdotally, it appears that, even as physical trade volumes declined, Chinese traders had switched to trading the metals’ derivatives on exchanges in the Mainland and overseas to continue to bring in U.S. dollars to their coffers.

Figure 1

{kind=link}

Figure 2

{kind=link}

Copper and Aluminum Production Patterns

China was the engine driving global production capacity growth during the commodities boom from 2009 to 2011. China is still the single largest producer of aluminum globally at 54%, and the top importer of copper at 45%, in 20143.

However, much of the capacity was tied to the non-economical production by State Owned Enterprises (SOE). China is facing an unprecedented decline in imports of copper and aluminum. Since the economic slowdown in 2015, the government has scaled down SOE subsidies and electricity pricing schemes. Users are also buying more from domestic sources and less from foreign producers.

How They Differ in Terms of Raw Material Flows

In terms of primary production, China has been and remains the top importing country for raw copper, accounting for 41% of global imports. In terms of trade flows, China dominates the physical trading of raw copper cathodes. However, China is self-sufficient in the production of primary aluminum.

Dwindling Copper Financing Deals in China

Copper financing deals had also inflated Chinese demand for physical copper in the past. With interest rates in China relatively lower than in most other countries, copper financing deals have become less profitable. Still, despite the slowdown in the Chinese economy, speculative activities remain vibrant on SHFE, as explained earlier.

Copper imports dominated by China

| Primary Copper - Global $62-64 billion in 2014 | |||

| Top Exporters | Share | Top Importers | Share |

| Chile | 28% | China | 41% |

| Zambia | 11% | Germany | 8% |

| Japan | 6% | Italy | 7% |

Source: International Trade Centre

Copper Volumes in China Match Overseas’ Tally

With the waning of copper financing trades, a more sensible relationship between physical trade flows and derivatives volumes has returned to futures exchanges.

China accounts for roughly half of the global demand for copper. Trading activities on SHFE are about that of the combined volumes traded on CME Group Globex and London Metals Exchange (LME), the two major international metal exchanges.

Please refer to CME Group’s report “Copper: Supply and Demand Dynamics” for further insights.4

Development of Copper Derivatives

Globally

Historically, copper derivatives markets have been flush with liquidity. There are liquid copper futures trading volumes across the three geographical regions – New York, London and Shanghai. With very liquid futures markets, price discovery has not been an issue for copper prices.

The warehousing issues of last year, have, however, somewhat shifted the trading liquidity among CME, LME and SHFE. Given the status of copper as the default indicator for base metals, in general, this may generate interesting dynamics in determining the global benchmark for base metals in the future.

Figure 3

{kind=link}

The fact of higher gold prices is in some ways bad news for gold investors, at least to those who intend to hold the metal over the long term, because they will incentivize more gold mining production. In addition to being highly sensitive to short-term changes in U.S. rate-hike expectations, gold prices show a strong long-term sensitivity to mining production (Figure 5). In 2014, the all-in cost of gold mining was below $1,000 an ounce and the cash flow cost was below $700 (Figure 6).

Correlation Between Copper Futures

The correlation of futures prices was analyzed, for one-year periods, over the past four years. Results were fairly consistent. Copper prices at CME and LME influence each other during the same day’s trading, while copper prices on SHFE seem to follow what happens at CME and LME on a one-day lag.

An 70%+ logarithmic correlation between SHFE and the two international exchanges means that there are regional price differentials which provide spread trading opportunities for market participants. (In fact, a linear correlation puts the respective figures at 0.99.)

| Correlation | Same Day | One Day Lag |

| CME vs LME | 0.87 | - |

| CME vs SHFE | 0.10 | 0.73 |

| LME vs SHFE | 0.10 | 0.76 |

Source: CME estimates for two-year logarithmic return correlation (2014-2015)

Arbitrage Copper Differentials Across Exchanges

While copper futures are also listed on other Asian exchanges in Hong Kong and India, and in the UAE, liquidity during Asian trading hours remains dominated by CME, LME and SHFE.

With an average of 1.9-4 million MT of open interest, and average daily volumes of 0.7-1.6 million MT, there are enough commercial and proprietary traders, banks and hedge funds to take opposite sides of market positions when arbitraging copper futures prices among these three exchanges.

| Copper Futures 2015 | Average Daily Volume (000 MT) | Open Interest (000 MT) |

| CME | 716 | 1,892 |

| LME | 1,588 | 3,998 |

| SHFE | 1,628 | 3,554 |

Source: CME, SHFE, Bloomberg

Aluminum Flows are More Even Across Regions

China is self-sufficient in the production of primary aluminum. It is, in fact, a net exporter of unwrought aluminum, with US$1.4 billion exported versus US$0.7 billion imported in 2014.

Unlike copper, the American, European & Asian regions each have a fair market share of physical trade flows of aluminum. No country accounts for more than 13% of the import or export market. Japan, the largest importer in Asia, only has 11% market share of global aluminum imports.

The absence of a dominant aluminum hub in Asia might be the reason aluminum futures volumes are relatively light on the exchanges in China and India, and hardly traded on the exchange in Japan. Historically, aluminum derivatives trading has been concentrated in London.

Development of Regional Indexes for Aluminum

However, as large physical volumes flow in and out of Asia and North America, there needs to be some way to price the regional differences. Due to the lack of liquid physically-deliverable futures contracts in these regions, traders have turned to Price Reporting Agencies such as Platts and Metal Bulletin for price discovery.

Aluminum distributed across the regions

| Primary Aluminum - Global $58-53 billion in 2014 | |||

| Exports | Share | Imports | Share |

| Asia Pacific | 30% | Asia Pacific | 28% |

| Europe | 36% | Europe | 41% |

| Americas | 16% | Americas | 18% |

| World | 100% | World | 100% |

| Top Exporters | Top Importers | ||

| Canada | 12% | USA | 13% |

| Russia | 11% | Germany | 12% |

| UAE | 10% | Japan | 11% |

Source: International Trade Centre

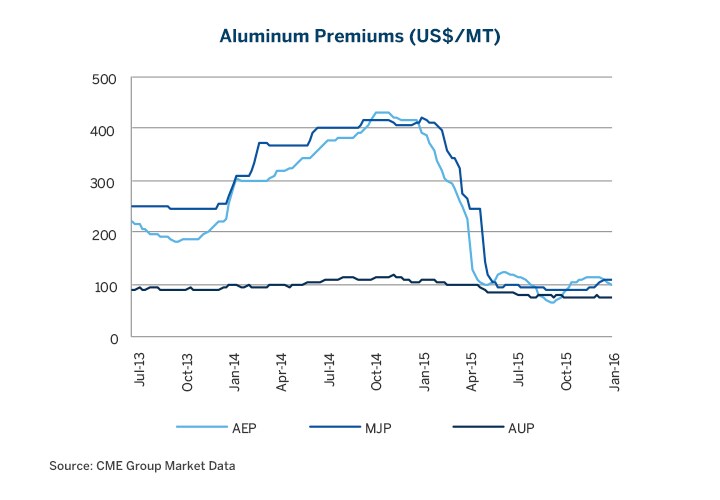

CME Group a Relative Newcomer in Aluminum

CME Group entered the aluminum derivatives space in April 2012, and currently has three aluminum regional premium contracts, which are cash settled against Indexes. The U.S. Midwest Premium contract (code: AUP) was launched in April 2012, followed by the European Premium contract (code: AEP) in September 2015 and the Japan Premium contract (code: MJP) in December 2015.

The prices for the Midwest and Japanese contracts are based off the Platts indices, and the European contract is based off the Metal Bulletin index. The contract specifications are summarized at the end of the report.

Trading volumes are very encouraging. On an annualized basis, CME’s total aluminum futures volumes in 2015 grew by over 300% compared to 2014, albeit from a low base.

Take a Trade View of CME Aluminum Premiums

The impetus for the launch of the premium contracts was the extreme volatility in the physical aluminum markets in 2014. Large regional price differences arose due partly to the loading and unloading bottlenecks at certain warehouses.

The bottleneck issues have since been addressed and regional premiums have fallen back to their historical $100 to $200 levels. Nevertheless, traders are still actively trading CME’s aluminum premium futures to hedge their physical exposures and to take a trading view of the market.

Figure 4

{kind=link}

FAQ 1: Do Futures Need Warehouses to Work?

CME Group’s launching of its European and Asian aluminum premium contracts in the second half of 2015 generated a lot of market interest. There were, however, two frequently recurring questions.

The first is whether the aluminum premium futures need to be physically deliverable to work?

This is a reasonable question since a few physically-settled aluminum regional premium contracts were launched in the last quarter of 2015.

There are valid reasons for physical delivery.

The rationale for such a contract is that traders can hedge the regional “all-in” price on one exchange, given that the premium surcharges are priced against the underlying aluminum price.

Physical delivery provides a mechanism for a logical conclusion to a futures contract. This, in turn, would lead to convergence between Futures vs Spot prices. CME is also exploring physical delivery locations outside the U.S. for our base metals suite. We currently offer warehousing for Lead in the EU, South Korea and Malaysia.

Cash Settlement Against Index also Valid

CME’s aluminum premium contracts are cash-settled against Indexes. What is crucial for futures to work is that the index must be robust.

As a proof of concept – all three contracts are trading on a regular basis.

The AUP contract was the first to be launched, in April 2012. Monthly volumes have averaged almost 4,000 contracts in 2015, with a record high of 7,276 contracts in January 2016. Open interest currently stands at over 25,000 contracts.5

FAQ 2: Will China Use MJP Aluminum Premium?

The second question frequently asked is: for the MJP to work, do Chinese traders need to adopt the MJP as the regional price point?

China itself produces 2,700 MT/month of aluminum, and until last year most of it was domestically consumed. Even with the economic slowdown, China has not cut its output as producers are still making money. According to commodity pricing specialist, CRU, smelting costs are below $1,800/MT in China, compared to the domestic selling price of $2,000/MT.6

Despite the impending overcapacity in domestic production, the amount of aluminum exported from China has remained fairly steady at 7,000 MT per year. With Indonesia banning base metal exports to feed its own domestic operations, China has to rely on bauxite imports from Australia. Aluminum production is energy intensive and China does not have cheap energy resources. This is partly why significant amounts of China’s aluminum production have not flowed into the market despite the government removing the 15% export tax.

Overall, the market is not anticipating a flood of Chinese aluminum into the export market. As such, whether China’s aluminum will likely be priced off MJP, the Asian premium, is unclear at this stage.

China’s objective is to have greater influence on global metals prices. Year to date, global aluminum futures prices have slumped from $1,800/MT in 2014 to $1,600/MT,7 and U.S. premiums (AUP) from $530/MT to $195/MT, with prices still groping for a bottom. As such, this might be a conducive time for China to participate in the global aluminum derivatives market.

Conclusion

With over half of the industry making losses, supply cuts are needed. The last tranche of aluminum supply cuts, initiated by Alcoa, led to a mini-recovery in aluminum prices in 2014. Alcoa followed up with a further shuttering of 500 ktpa U.S. smelting capacity, to be completed by the first quarter of 2016.

This might have done the trick in the past -- when the base metals world was neatly divided into two parallel universes – China and the rest of the world, separated by China's 15% export tax.

However, with the weak Ruble, Russian aluminum giant RUSAL is under no pressure to follow suit, and Chinese curtailments are being resisted by local governments wanting to keep employment up. With others not following Alcoa’s lead, the aluminum market may remain oversupplied for some time.

With the demise of copper financing trades in China, copper hedging and price movements are returning to a more sensible relationship to physical trade flows. Average daily volumes of CME’s copper futures for the first two months of 2016 are 18% higher than the same period in 2015, and 27% higher than the 2015 full-year average.

Contract Specifications

| Copper Futures | |

| Popular Name | COMEX Copper |

| Contract Code | HG |

| Contract Unit | US cents per pound |

| Contract Size | 25,000 pounds |

| Price as at 22 Feb 2016 | US$ 2.113 / lb |

| Average Daily Volume | 67,000 lots |

| Open Interest | 180,000 lots |

| Settlement | Physical |

| Aluminum MW US Transaction Premium Platts (25MT) Futures | |

| Popular Name | Aluminum Mid-West Premium |

| Contract Code | AUP |

| Contract Unit | US Dollars per metric ton |

| Contract Size | 25 metric tons |

| Price as at 22 Feb 2016 | US$ 0.09021 / pound (about US$ 195 / MT) |

| Average Daily Volume | 190 lots |

| Open Interest | 25,000 lots |

| Settlement | Cash settled |

| Aluminium European Premium Duty-Unpaid (Metal Bulletin) Futures | |

| Popular Name | Aluminium European Premium |

| Contract Code | AEP |

| Contract Unit | US Dollars per metric ton |

| Contract Size | 25 metric tons |

| Price as at 22 Feb 2016 | US$ 91.07 / MT |

| Average Daily Volume | 40 lots |

| Open Interest | 5,050 lots |

| Settlement | Cash settled |

| Aluminum Japan Premium (Platts) Futures | |

| Popular Name | Aluminum MJP |

| Contract Code | MJP |

| Contract Unit | US Dollars per metric ton |

| Contract Size | 25 metric tons |

| Price as at 22 Feb 2016 | 106.50 |

| Average Daily Volume | 80 lots |

| Open Interest | 1,450 lots |

| Settlement | Cash settled |

References

- CME Group market data

- SHFE Monthly Data

- World Aluminum, U.S. Geological Survey

- https://main--www--cmegroup.aem.page/education/featured-reports/copper-supply-and-demand-dynamics

- CME Market Data

- Commodities Research Unit (CRU)

- LME market data

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Recommended For You

View this article in PDF format.