Trade aspects of the Adjusted Interest Rate (AIR) Total Return futures contract

{kind=link}

Adjusted Interest Rate Total Return futures, or AIR TRFs, provide total return exposure with an overnight floating rate built in. AIR Total Return futures are comprised of three components:

- S&P 500 Total Return Index performance

- Daily accrued financing

- Daily financing spread adjustment

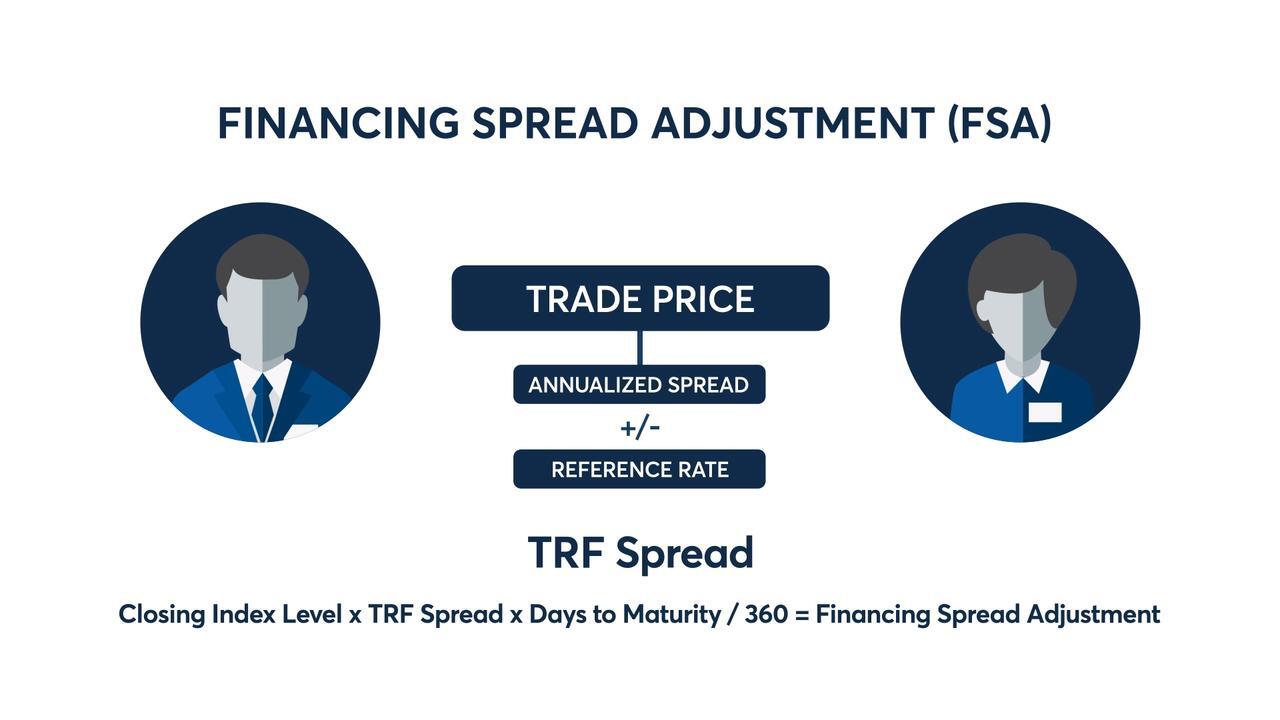

Financing Spread Adjustment

When trading an AIR Total Return futures contract, the counterparties will agree to a trade price in terms of an annualized spread plus or minus to the reference rate. This is known as the Total Return Futures spread (TRF spread). The financing spread adjustment (FSA) is calculated as the closing index level x TRF spread x days to maturity / 360.

{kind=link}

The seller of the AIR TRF might hedge the equity exposure by buying the component stocks to replicate the index. Purchasing the single stocks will require capital, and let’s assume the cost to fund this exposure is at a premium with a positive spread to the Effective Federal Funds Rate (EFFR). The seller of the futures would cover the increased funding costs by demanding a higher price at which to sell the futures. Similarly, if the cost to fund the underlying equity stock exposure requires a negative spread to EFFR, the seller of the futures could afford to sell the futures at a lower price.

This is what the financing spread adjustment (FSA) component does. A positive TRF spread will increase the FSA and subsequently, the price of the AIR TRF, and a negative TRF spread will decrease the FSA as well as the AIR TRF price. The AIR TRF price increase is dependent upon the magnitude of the spread in relation to the EFFR and the time left to expiration. As the time to maturity decreases, the impact of the FSA reduces and will eventually be equal to zero at expiry.

Differences between equity index exposure and the AIR TRF contract notional value

The price of the AIR TRF should not be assumed to be the same value as the equity index exposure underlying the contract. This is due to the accrued financing and financing spread adjustment components being subtracted from and added to the equity index price that in turn impacts the notional value of the AIR TRF contract without impacting the underlying equity exposure. To calculate the number of contracts needed to obtain an exact equity index exposure, one cannot just use the futures price or contract notional to do so.

Number of futures contracts x Equity Index Level x Contract Multiplier = Equity Index Exposure

It is important to remember when trading AIR TRFs, the embedded equity index exposure equals the number of futures contracts x the equity index level x the contract multiplier.

Initial accrued financing level

When it comes to the accrued financing component, the initial starting value is not material, but rather the actual difference in the value of the accrued financing over the holding period.

{kind=link}

Looking at two examples that have the same assumptions with varying accrued financing levels at the start – example 1 with 200 and example 2 with zero. In both cases, the accrued financing changes by 20 between time 1 and time 2. The difference in valuation in both examples is 75, despite the difference in the initial value of the accrued financing.

Online tools and resources

The latest accrued financing amount for each AIR TRF contract is published daily and available in a .csv file. Additionally, an online calculator is available to convert the price of any TRF spread into the AIR TRF price once the closing index level for the day is known.